China's Pharmaceutical and Biotech Industry Investment White Paper 2017: Transitioning from Extensive Growth to Refined Quality Enhancement

Background and Outlook: The Past Decade and the Eve of Qualitative Change

In October 2016, the State Council issued the Outline of the “Healthy China 2030” Plan (hereinafter referred to as the “Outline”), elevating the concept of “Healthy China” to a strategic priority for development. The Outline explicitly sets targets for the total scale of the health service industry to exceed RMB 8 trillion by 2020 and RMB 16 trillion by 2030. The “Healthy China” strategy is poised to become a key driver for the development of China’s medical and health industry.

Before delving into the next decade, let us briefly review the past ten years.

During the previous five-year period from 2007 to 2011, the Chinese government continuously increased healthcare expenditure. In particular, the new round of healthcare reform launched in 2009 injected nearly RMB 1 trillion into initiatives such as expanding coverage of the medical security system and establishing the National Essential Medicines System, significantly boosting industry prosperity. Meanwhile, the expansion of medical insurance coverage for urban employees and urban residents drove rapid industry growth.

During the latter five-year period from 2011 to 2015, following the substantial nationwide expansion of medical insurance coverage, some regions began to experience payment pressures on their medical insurance funds. As healthcare reform entered a more complex and challenging phase, various localities started exploring diverse measures for controlling medical insurance costs. With strong policy intervention, tighter terminal payment controls slowed the release of “rigid” medical demand.

Since 2015, cost-containment measures within the basic medical insurance system have begun to yield initial results. In both 2015 and 2016, the urban basic medical insurance fund recorded revenues exceeding expenditures, with revenue growth outpacing expenditure growth. Meanwhile, commercial health insurance is emerging as a new payer in the pharmaceutical and healthcare sectors. Although many regions across the country continue to face increasing pressure on the sustainability of their medical insurance funds, the substantial expansion of the overall healthcare market and the general improvement in multi-tiered payment capabilities have established a solid foundation for the effective implementation of various new healthcare policies. Over the next 5–10 years, China’s healthcare industry will undergo a genuine qualitative transformation driven by reform.

These qualitative changes include:

“Created in China” will rise powerfully on the global stage of new drugs.According to Pharmaprojects statistics, by the end of 2015, a total of 147 Chinese companies were engaged in original drug development. In terms of the number of R&D enterprises alone, China has surpassed Japan to become Asia’s largest country for new drug research and development. With the introduction of the priority review policy by the China Food and Drug Administration (CFDA) and the significant expansion of staff at the Center for Drug Evaluation (CDE), China’s concepts and operational practices in new drug review are increasingly aligning with international standards. Meanwhile, as a large number of professionals with years of experience at multinational pharmaceutical giants return to China, the Chinese pharmaceutical industry has seen comprehensive improvements in basic scientific research, laboratory R&D, process and manufacturing, and quality control. It is understood that there are currently more than 10 Chinese new drug R&D companies that are globally leading and have entered or completed Phase III clinical trials, while over 50 companies have advanced to Phase I and Phase II clinical stages. It is anticipated that as these companies grow and mature, China will produce a cohort of innovative and original drug companies equipped with globally leading technologies, bringing their blockbuster new products to the global market.

China Has the Opportunity to Lead the World in Precision Medicine.In the upstream sector of sequencing instruments, U.S. companies hold an absolute advantage. However, the core of precision medicine research requires extensive data collection and analysis, an area in which China has a distinct edge. Among the hundreds of Chinese companies providing gene sequencing services, BGI Genomics has emerged as the global leader in non-invasive prenatal testing (NIPT). In the CAR-T cell therapy sector, which holds the most promise for treating hematologic malignancies, China ranks second only to the United States in the number of clinical trials, placing it in the first tier globally. As precision medicine represents the future direction of human healthcare, China is well-positioned to achieve a leading role on the global stage in this field.

Wearable Devices + Telemedicine + Artificial Intelligence Will Completely Disrupt Traditional Diagnosis and Treatment Services.Not long ago, IBM’s supercomputer Watson, having digested and absorbed 25,000 medical cases and concluded its two-year “intensive training,” traveled all the way to China to unveil the application of artificial intelligence in the Chinese healthcare sector at Zhejiang Provincial Hospital of Traditional Chinese Medicine. The most significant pain point in China’s healthcare service system is the supply–demand imbalance surrounding scarce medical resources. However, with the widespread adoption of internet hospitals, medical wearable devices, and third-party imaging centers, artificial intelligence is poised to play an increasingly vital role in disease prevention, diagnosis, and treatment. Technological breakthroughs and the rapid advancement of AI are making it increasingly clear that traditional healthcare delivery models may be disrupted.

Against this backdrop, we believe that on the eve of a qualitative transformation, investors in the primary market of the healthcare sector should pay close attention to the following areas during 2017–2018:

· Industry Reshuffling of Generic Drugs Driven by Consistency Evaluation

· The Impact of Changes in Review Efficiency and Philosophy on the Development of China’s New Drug R&D Enterprises

· Development of Domestic Biopharmaceuticals, Innovative Drugs, and Precision Medicine

· Consolidation in the Commercial Sector Under the Two-Invoice System

· Import Substitution for High-End Medical Devices

· Cross-Border Acquisition of High-End Medical Devices

· Applications of AI and Robotics in Healthcare

· Accelerated Development of Tiered Diagnosis and Treatment Systems and Specialized Chain Medical Service Platforms

Pharmaceuticals and Biotechnology Sector

Industry Trends

Industry TrendsIn 2016, the market size of terminal pharmaceutical sales in China’s healthcare industry reached RMB 1.4774 trillion, with the growth rate slowing to 7.3%. Amid stricter healthcare insurance cost-containment measures and increasingly stringent industry policies targeting hospitals, the growth pace of the pharmaceutical sector has further decelerated. It is anticipated that future industry growth will broadly align with GDP growth rates. In the coming period, structural adjustment will dominate industry trends. The pharmaceutical industry will gradually transition from extensive, volume-driven expansion to refined, quality-oriented improvement.

Data Source: Southern Institute of Pharmaceutical Industry Economics

In this market environment, growth drivers are concentrated in the expansion of medical insurance coverage, the launch of new products, continuous improvement and refinement of healthcare infrastructure and services, the rapid rise in chronic disease incidence, provincial/municipal-level reimbursement for high-value drugs, and private investment in healthcare. Foreseeable challenges and market pressures mainly manifest in stricter overall controls on medical insurance funds, more stringent tendering processes, quality consistency evaluations, rational drug use policies, reduction of the drug revenue share in hospitals, and national price negotiations for patented medicines.

From the perspective of national policiesThe three most critical policies for forecasting future trends are the Quality and Efficacy Consistency Evaluation for Generic Drugs (hereinafter referred to as “Consistency Evaluation”), the “Two-Invoice System + VAT Reform,” and the new National Reimbursement Drug List (NRDL). With the intensive rollout of policies related to the Consistency Evaluation, the scope of drugs subject to this evaluation has been defined, and clear deadlines have been established. Consequently, the wait-and-see attitude and uncertainty among pharmaceutical manufacturers will rapidly shift into a race to comply. The Two-Invoice System is clearly defined; it will be implemented first in 11 pilot provinces for comprehensive medical reform and 200 pilot cities, with the aim of nationwide implementation by 2018. Strict invoice management will be enforced, requiring consistency among invoices, goods, and accounts during drug acceptance and warehousing. An additional invoice is permitted at the township level. The effects of the “Two-Invoice System + VAT Reform” will be released at a steady pace, leading to significant structural adjustments in the pharmaceutical commerce sector. The new NRDL includes a total of 2,535 drugs, representing a 15.4% increase. Among these, there are 1,297 Western medicine varieties (an increase of approximately 11.4%), including 402 Class A and 895 Class B drugs. There are 1,238 Traditional Chinese Medicine (TCM) varieties (an increase of approximately 20%), including 43 additional ethnic medicines, with 192 Class A and 1,046 Class B TCM drugs. The transformations brought about by the new NRDL will begin to show initial results within one year.

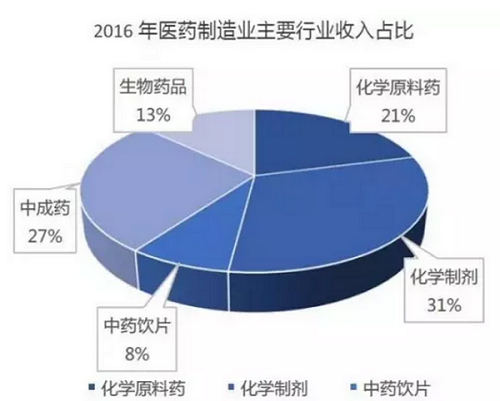

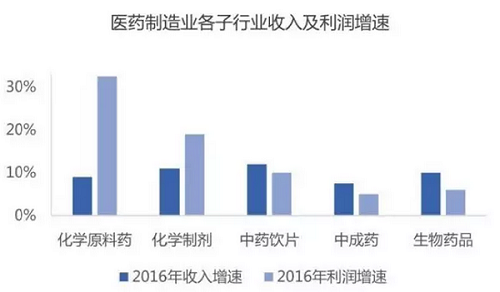

From the perspective of sub-sectors: Since 2015, driven by the rise in prices of bulk active pharmaceutical ingredients (APIs), chemical drug formulations have remained the leader in the pharmaceutical manufacturing industry, with gradually improving performance. In 2016, the market size of this sub-sector reached RMB 753.47 billion, a year-on-year increase of 10.8%, while total profits amounted to RMB 95.05 billion, a year-on-year increase of 16.8%. With the advancement of the generic drug consistency evaluation policy, the upgrading and structural adjustment of China’s pharmaceutical industry will inevitably be promoted. In the future, the chemical drug formulation industry will trend towards survival of the fittest and increased market concentration. The biopharmaceutical sector continues to grow rapidly, although its profit growth rate has slowed; it is expected to maintain significant room for expansion in the future. The traditional Chinese medicine (TCM) industry benefits from favorable policies. It is anticipated that the relaxation of policies related to production, clinical application, and medical insurance will drive rapid growth in the TCM formula granules sector, while the TCM decoction pieces sector will continue to maintain relatively fast growth. The recovery of the API industry since 2015 may peak in the next two years, presenting short-term investment opportunities. Domestic new drug research and development is burgeoning. Platform-type R&D enterprises that master blockbuster products and key technologies, targeting both the Chinese and global markets, will be favored by capital. Targeted drugs guided by the concept of precision medicine entail high capital costs and R&D risks. Domestic pharmaceutical companies tend to obtain exclusive licenses from foreign enterprises or select blockbuster drugs for introduction and development in the domestic market. New dosage forms of small-molecule drugs and new varieties of biologics will become the prevailing trends.

Data Source: Southern Institute of Pharmaceutical Industry Economics

Data Source: Southern Institute of Pharmaceutical Industry Economics

Looking ahead to the next three years, we anticipate the following changes in China’s pharmaceutical and biotechnology industry.

1. Consistency Evaluation Brings Generic DrugsMarket'sStructural Transformation

The fundamental purpose of the Quality and Efficacy Consistency Evaluation for generic drugs is to enhance the quality standards of domestically produced generics, ultimately achieving import substitution and controlling healthcare insurance expenditures. Although the consistency evaluation will reshape the landscape of the generic drug industry and create investment opportunities, this issue requires a dialectical perspective.

Consistency evaluation does not necessarily lead to an increase in the market share of domestic generic drugs in the short term, nor does it imply a reduction in pharmaceutical expenditures in the short term. During the period of structural adjustment, bioequivalence, manufacturing process standards, channel branding, and room for price reductions for varieties involved in consistency evaluation serve as criteria for assessing investment value amid the reshuffling of the generic drug industry. On one hand, for varieties where achieving bioequivalence and high manufacturing process standards is challenging, the level of manufacturing process becomes the key criterion for determining investment value. For varieties where bioequivalence and manufacturing process standards are easily attainable, the market is fully competitive, making channels and brand strength the primary criteria for assessing investment value. On the other hand, for generic drugs that are about to be launched or have recently entered the market, the key to their investment value lies in the extent of potential price reductions for the original branded products; this price reduction potential should be evaluated based on absolute values rather than percentages. Among companies that have met the standards, particular attention should be paid to those whose major products are required to complete generic drug consistency evaluation by the end of 2018 and have already submitted applications for such evaluation.

The scarcity of qualified clinical institutions capable of conducting bioequivalence studies, the lack of industry standards, and the insufficient supply of reference listed drugs are likely to hinder the timely completion of bioequivalence evaluations by the end of 2018, making policy adjustments inevitable. The current list of 289 drug varieties subject to bioequivalence evaluation is merely the first step; the subsequent introduction of broader bioequivalence evaluation policies is expected to have a more profound impact on the industry. Despite existing uncertainties, the short-term promotional effect of bioequivalence evaluation on leading generic drug manufacturers, contract research organizations (CROs), leading pharmaceutical excipient suppliers, and formulation export enterprises is unquestionable.

2. The “Two-Invoice System” Has Significantly Reduced Pharmaceutical Distribution Links and Increased Market Concentration in the Pharmaceutical Commerce Sector

With the introduction and implementation of the “Two-Invoice System” and the VAT reform, enterprises have been forced to shift from the previous “low-invoice” model to a “high-invoice” model, significantly increasing their fiscal and tax burdens. Small and medium-sized wholesale companies that integrate agency services, invoice pass-through, and distribution are facing elimination due to the unsustainability of invoice pass-through operations and pressure from extended payment cycles by medical institutions. These companies are urgently seeking acquisition by large circulation enterprises, which will substantially compress the distribution chain. Meanwhile, leading national and regional distribution companies are significantly expanding their terminal coverage through mergers and acquisitions.

Meanwhile, under the pressure of the “Two-Invoice System,” small chain pharmacies and retail outlets will face extensive consolidation as their inability to use cash transactions leads to higher operating costs and declining profits. Large chain pharmacies will continue to benefit from increased industry concentration. At the same time, emerging professional Contract Sales Organizations (CSOs) are poised for rapid growth, becoming a noteworthy niche within the pharmaceutical commercial sector.

3. The New National Reimbursement Drug List Drives Short-Term Industry Restructuring

The 2009 edition of the National Reimbursement Drug List (NRDL) gave rise to dozens of drug products with annual sales exceeding RMB 1 billion. The introduction of the new NRDL signals that the RMB 1.5 trillion pharmaceutical market is poised for restructuring.

The 2017 edition of the National Reimbursement Drug List (NRDL) added 339 new drugs, including 17 new products in the central nervous system (CNS) therapeutic area, while lifting usage restrictions on 21 products. Ninety-one new pediatric drug products were added. Meanwhile, high-cost medications such as tyrosine kinase inhibitors (TKIs) and DPP-4 inhibitors were newly included in the NRDL. Several traditional Chinese medicine (TCM) injection products already listed were restricted for use only in medical institutions at Level II or above, with stricter limitations on their approved indications. The updated NRDL demonstrates greater encouragement and support for proprietary Chinese medicines, pediatric drugs, innovative drugs, and medications for major diseases, while imposing tighter controls on areas such as TCM injections.

The 2017 edition of the National Reimbursement Drug List (NRDL) prioritized the review of new drugs launched after 2009, with further preferential consideration given to innovative medicines within this group. High-cost drugs with proven efficacy were simultaneously included in the proposed list for price negotiations. Among the innovative chemical drugs and biological products approved in China between 2008 and 2016, the vast majority were incorporated into the 2017 NRDL or covered under the negotiated drug program. It is anticipated that innovative drugs and high-end generic varieties characterized by high clinical value, significant market potential, and substantial entry barriers will be favored in the future.

4. The Dawn of the Era of New Drug Research and Development (R&D)

According to Pharmaprojects statistics, by the end of 2015, a total of 147 companies in China were engaged in original drug development. In terms of the number of R&D enterprises alone, China has surpassed Japan to become Asia’s largest country for new drug research and development. Domestic new drug R&D companies are on the eve of a qualitative transformation. With continuous policy support and ongoing conceptual updates from the CFDA and CDE; with the return of overseas talent and the improvement of supporting industries for new drug R&D; with the overall enhancement of industrial standards and the rapid development of technologies in fields related to new drug R&D (such as gene sequencing, molecular diagnostics, and precision medicine); and with a significant increase in the foresight and professionalism of venture capital firms, the new drug research and development industry is about to enter a period of rapid growth characterized by qualitative change. Platform-type new drug R&D enterprises that target the Chinese and even global markets and possess blockbuster products and key technologies, as well as blockbuster varieties with distinct clinical advantages, will be favored by capital.

The development of original new drugs targeting novel mechanisms and compounds entails high capital costs and R&D risks. In contrast, licensing in blockbuster drugs and pursuing differentiated, targeted development offers more controllable financial and R&D risks, thereby garnering greater recognition from investors. This strategy has spurred two key trends: On one hand, foreign pharmaceutical companies are inclined to divest China-specific licensing rights for their drugs due to compliance risks and promotional costs. On the other hand, domestic pharmaceutical companies possess unique advantages in regulatory compliance and low-cost marketing; securing exclusive licenses from foreign firms can rapidly enhance their competitiveness. Notable examples of this model include Tibet Pharma’s acquisition of Imdur, a cardiovascular drug under AstraZeneca; Hengrui Medicine’s licensing-in of Rolapitant, an antiemetic from Tesaro; and Yiteng’s acquisition of Ceclor and Vancocin, antibiotics formerly under Eli Lilly.

On the other hand, domestic innovative drug companies are actively selecting blockbuster drugs globally for development and launch in China. Zai Lab’s in-licensing of Hanmi Pharmaceutical’s investigational lung cancer drug HM61713, and PegBio’s in-licensing of Pfizer’s investigational diabetes drug GKA, both exemplify this model. In contrast, Soochow Pharmaceuticals’ acquisition of global rights to Eli Lilly’s clinically failed drug DB103 represents the re-development of an innovative drug. Most of these companies boast teams with extensive R&D experience at multinational pharmaceutical firms. The selected products typically feature high market potential, proven success or rapid progress in international markets, and substantial support from robust clinical data.

Future Trends in New Drug Development: Toward Greater Precision and SpecificityChemical innovative drugs typically offer high efficacy, broad-spectrum activity, and ease of oral administration, but they are often associated with significant side effects. Biologics, on the other hand, provide superior targeting and safety profiles, yet their efficacy may be limited, and they are generally not suitable for oral delivery. A growing trend in drug development is to create new therapeutics that combine the advantages of both modalities, such as novel formulations of small-molecule drugs (e.g., sustained-release and targeted delivery systems) or new classes of biologics (e.g., long-acting and orally administered agents).

The surge in biopharmaceutical R&D in developed countries in recent years is driven by multiple factors: (1) the declining success rate of small-molecule drug development, leading to a significant increase in average costs; (2) the high safety profile of biologics, resulting in higher R&D success rates; and (3) well-established social payment systems in developed nations. For domestic new drug R&D enterprises in China, the overall R&D costs for small-molecule drugs (particularly clinical trial costs) are relatively low. Furthermore, "Me-too" and "Me-better" new drugs can draw extensively on overseas experience, significantly improving success rates, while their prices remain affordable for the majority of the Chinese population. Therefore, substantial opportunities still exist for the R&D of new small-molecule drugs in China. In contrast, for domestic innovative biologics, excessive costs and pricing, coupled with payment constraints, may become key factors restricting their development. Currently, fueled by high industry expectations, the market for innovative biologics remains robust, but it will inevitably face market tests in the future.

5. Policy Support Driving the Upgrading of the Traditional Chinese Medicine Industry

Leveraging the advantages of traditional Chinese medicine (TCM)—namely its simplicity, convenience, affordability, and efficacy—the state has provided robust policy support to the TCM industry. However, for TCM to truly capitalize on these strengths, structural adjustments are inevitable. Mandatory national policy support on the healthcare service side lays the foundation for consumer demand, while significant standardization and modernization on the production side underpin industrial upgrading. Specifically, the TCM formula granules sector is expected to maintain an annual growth rate exceeding 30% over the next five years, driven by the substitution of TCM decoction pieces and favorable policies; however, intensified competition resulting from eased market access may become apparent within the next three years. Meanwhile, the TCM injection industry, propelled by enhanced regulatory compliance and re-evaluation policies, will undergo a painful period of consolidation, characterized by market shakeouts and emerging investment opportunities, with high-safety injectable formulations holding greater investment value.

6. Precision Medicine Leads the Trend in New Drug Development

Drug development guided by precision medicine is based on personalized medicine, integrating genomic sequencing technologies and bioinformatics big data to develop targeted therapies for specific genetic mutations in individual patients. In 2016, the market size of China’s precision medicine industry reached RMB 40 billion, with the targeted drug market accounting for RMB 13 billion, representing a 32.5% share of the precision medicine market. The sector is projected to grow at an annual rate exceeding 20% over the next five years.

The emergence of precision medicine has led to more refined disease classification and a substantial increase in the number of disease subgroups, making it increasingly difficult for large pharmaceutical companies to maintain a complete monopoly on the innovative drug R&D market. Compared with traditional drug development models, precision medicine-guided new drug development can significantly reduce R&D costs and timelines while improving clinical success rates. Small and medium-sized enterprises (SMEs) and startups that possess core technologies face greater opportunities, can respond rapidly to emerging trends, and thus offer higher investment value. Chinese SMEs are no less innovative than their foreign counterparts in terms of product technology and business models in the field of precision medicine. Typical representatives include 3D Medicines, which focuses on developing tumor-targeted therapies for specific gene mutations, and Soontai Bio, which leverages whole-genome scanning and clinical big data technologies to guide the re-development of previously failed drugs.

In 2017, the following sectors will attract significant capital attention· Innovative Drug and Biopharmaceutical Companies in Chronic Diseases and Oncology, and Chemical Drug R&D Platforms

· Generic drug manufacturers with the strength to be the first to pass the consistency evaluation, and CRO/CMO companies deeply associated with the consistency evaluation and the refined division of labor in the pharmaceutical industry chain

· Modern Traditional Chinese Medicine (TCM) Technology Platform: Safe and Effective TCM Advantageous Varieties

Major A-Share Players in the Pharmaceutical Sector· Strategic Layout in New Drug R&D:Hengrui Medicine, Hisun Pharmaceutical, Livzon Group, Taikang Asset Management, SDIC Innovation, Legend Capital

· Channel and Sales Layout:Rikang Pharmaceutical, Shanghai Pharmaceuticals, Sinopharm Accord

· Strategically positioning for mergers and acquisitions of high-quality overseas assets:Luye Pharma, Fosun Pharma, Humanwell Healthcare

· Ramp up R&D and manufacturing of biopharmaceuticals:3SBio, WuXi Biologics, Innovent Biologics

· Introduction of Overseas New Drug Projects:Zai Lab, Hua Medicine, Hengrui Medicine, PegBio

· Strategic Layout of Non-Medical Industry Companies:Sanpower Group, Baihuacun, Jinshi Oriental

Source: China Renaissance Capital

Authors: Li Gang, Cai Hua, Zhu Yunpeng, Hu Minjie, Xu Dingliang, Zhang Xiao, Liu Zeyuan, Xu Lichen, Wei Wei