Independent Hemodialysis Centers: A Niche Sector with a RMB 150 Billion Market Opportunity

By the end of December 2016, the National Health and Family Planning Commission successively issued the basic standards and management regulations for four categories of independently established medical institutions: medical imaging diagnostic centers, medical laboratories, hemodialysis centers, and pathology diagnostic centers, and provided interpretations on issues of public concern.

The successive introduction of relevant policies has led to a sustained increase in capital market attention toward independently established medical institutions, such as clinical laboratory testing centers, hemodialysis centers, and imaging centers. VCBeat (WeChat ID: vcbeat) will analyze the current development status of these types of medical institutions in China and provide in-depth profiles of selected benchmark enterprises. This article focuses on hemodialysis centers. What exactly are independent hemodialysis centers? How significant is their growth potential? Which companies serve as industry benchmarks? What is the state of development in foreign markets? You will find answers to all these questions in this article.

Independent Clinical Laboratory Market Analysis:We Analyzed 20 Years of U.S. Data: China’s Third-Party Testing Market Could See a Tenfold Surge

What Is an Independent Hemodialysis Center

In the document No. 67 [2016] of the National Health and Family Planning Commission, titled “Basic Standards for Hemodialysis Centers (Trial)” (hereinafter referred to as the “Standards”), issued at the end of last year, an independent hemodialysis center is defined as a separately established medical institution that provides hemodialysis treatment to patients with chronic renal failure, excluding hemodialysis departments set up within other medical institutions.

The Standard defines independent hemodialysis centers for the first time, with the key aspect being thatThe hemodialysis center is “independently established,” not affiliated with other medical institutions, operates as an independent legal entity, independently bears corresponding legal liabilities, and is subject to establishment approval by the provincial-level or higher health and family planning administrative departments.Secondly, independent hemodialysis centers can provide specialized nephrology diagnosis and treatment services, and may also establish departments such as clinical laboratory, radiology, and pharmacy, or outsource testing and examination tasks to other medical institutions. Finally, another crucial point is that,The state encourages hemodialysis centers to develop along the lines of chain operations and group-based models, and to open up to private capital.

Analysis of Policies Related to Hemodialysis Centers

In August 2012, six ministries and commissions jointly issued the "Guiding Opinions on Launching Critical Illness Insurance for Urban and Rural Residents," introducing critical illness insurance to further improve the medical security system for urban and rural residents, establish a multi-tiered medical security framework, and address poverty caused or exacerbated by medical expenses. Rather than simply defining critical illnesses by specific disease types, the document determines eligibility based on a comparison between the high medical costs incurred by patients and the economic burden-bearing capacity of urban and rural residents. Reimbursement under critical illness insurance is no longer limited to items within the policy scope; as long as the medical expenses are reasonable and remain out-of-pocket for critical illness patients after basic medical insurance reimbursement, more than 50% of these costs will be additionally reimbursed.

In February 2014, the Office of the State Council Leading Group for Healthcare Reform issued a notice on accelerating the implementation of critical illness insurance for urban and rural residents, to implement the requirements set forth in the “Guiding Opinions on Launching Critical Illness Insurance for Urban and Rural Residents,” and comprehensively roll out pilot programs for such insurance across China in 2014. With end-stage renal disease (ESRD) included in the critical illness coverage framework, reimbursement rates have increased, helping to extend patients’ survival and significantly alleviating their financial burden. The enhanced affordability for patients has provided strong momentum for the growth of the hemodialysis market.

In March 2014, the Medical Administration Bureau of the National Health and Family Planning Commission issued the “Letter on Soliciting Opinions on the Basic Standards and Management Specifications for Hemodialysis Centers,” drafting the standards and management specifications for the establishment of hemodialysis centers. Subsequently, several provinces successively released policies to encourage the development of independent hemodialysis centers.

In November 2016, the National Health and Family Planning Commission (NHFPC) issued the “Decision on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions (Draft for Comments),” which listed “hemodialysis centers” as a standard category of medical institutions under Article 3, Item (10). In December 2016, the NHFPC promulgated the “Basic Standards and Management Specifications for Hemodialysis Centers (Trial),” stipulating that hemodialysis centers must be equipped with at least 10 to 20 hemodialysis machines and have at least two licensed physicians.

Current Status of China's Dialysis Market

Loss of renal function is usually irreversible. Kidney failure is typically caused by type I and type II diabetes, hypertension, polycystic kidney disease, chronic autoimmune attack on the kidneys, and long-term urinary tract obstruction. End-stage renal disease (ESRD) represents the advanced stage of kidney damage,In addition to kidney transplantation,Ongoing dialysis treatment is required to sustain life. Dialysis artificially removes toxins, water, and salts from the patient’s blood,The two dialysis modalities are hemodialysis and peritoneal dialysis, with a patient ratio of approximately 9:1 between hemodialysis and peritoneal dialysis.Patients with ESRD typically require hemodialysis at least three times per week.

In our previous analysis, we found that the policies have consistently referred to hemodialysis.Hemodialysis is a treatment for end-stage renal disease (ESRD) that diverts blood outside the body, where waste products are removed through a semipermeable membrane. This process eliminates metabolic wastes and excess fluid while maintaining electrolyte and acid-base balance. Peritoneal dialysis utilizes the patient’s own peritoneum as the dialysis membrane. By infusing dialysate into the peritoneal cavity, solutes and water are exchanged with plasma components in the capillaries on the other side of the peritoneum. This clears retained metabolic products and excess fluid from the body, while also replenishing essential substances via the dialysate.

Under the current policies issued by China’s National Health and Family Planning Commission, facilities are explicitly designated as hemodialysis centers for providing hemodialysis services, while it remains uncertain whether they are permitted to offer peritoneal dialysis services. In clinical practice, however, hemodialysis and peritoneal dialysis should be used in combination based on patient needs; therefore, peritoneal dialysis services also need to be decentralized to the community level and operated through chain networks. Notably, the two leading international chain dialysis providers offer both hemodialysis and peritoneal dialysis services.

China currently has a high incidence of chronic kidney disease, and end-stage renal disease is not receiving adequate dialysis treatment. According to data from the "Epidemiological Survey of Chronic Kidney Disease in China" published in 2012,The prevalence of chronic kidney disease among adults in China is as high as 10.8%, and the growth rate of chronic kidney disease is expected to exceed 17% over the next decade.At this rate, China currentlyApproximately 150 million people suffer from varying degrees of renal impairment, with over 2 million patients progressing to end-stage renal disease (ESRD). According to data from the Ministry of Health’s 2012 “Green Book on China’s Health Development,” the average annual direct treatment cost per hemodialysis patient is RMB 75,085.92, exceeding the financial capacity of most ESRD patients and resulting in a low treatment rate. Currently, only about 290,000 dialysis patients are registered in China, with an estimated actual figure of approximately 330,000, including around 300,000 undergoing hemodialysis.Of the 2 million patients with end-stage renal disease (ESRD) in China, only 300,000 undergo hemodialysis. Based on an annual dialysis cost of RMB 75,000 per patient, the current market size for hemodialysis in China is approximately RMB 22.5 billion.

With 2 million ESRD patients all undergoing hemodialysis treatment, and an annual treatment cost of RMB 75,000 per patient, the theoretical market size for hemodialysis centers amounts to RMB 150 billion.Compared with the 90% treatment rate for end-stage renal disease (ESRD) in developed countries, there is a significant gap. Therefore, compared to the theoretical market size, China’s hemodialysis market still has over RMB 120 billion in potential; even calculated at a 90% treatment rate, there remains nearly fivefold room for market growth.

VCBeat analyzes that there are two main reasons for this gap.First, China’s hemodialysis centers previously faced significant policy barriers, with strict regulatory entry requirements limiting the service sector primarily to public general hospitals.This characteristic has led to the concentration of most hemodialysis centers in large cities, with a scarcity of such facilities at the primary care level. However, patients with end-stage renal disease (ESRD) require long-term, frequent hemodialysis treatment. Due to the limited availability of hemodialysis centers at the grassroots level, patients are forced to seek care at major hospitals or forgo treatment altogether. Consequently, there is a significant mismatch between the supply and demand for hemodialysis services provided by medical institutions in China.

Prior to the issuance of the Standards, very few enterprises with private capital in China were able to enter the hemodialysis sector. In an article titled “In-Depth Interpretation: The Liberalization of Policies for Hemodialysis Centers in China,” written by Zhang Yongqiang of Aishen Medical and published by VCBeat in December last year, the development trajectory of third-party hemodialysis centers in China was reviewed. Around 2009, Shenyang Sansheng Pharmaceutical (a domestic producer of erythropoietin [EPO]) established the “Sansheng Kidney Friends’ Home” in Jinzhou and other locations in Liaoning Province, initiating efforts to build a “chain of primary-care hemodialysis centers.” In December 2010, Shandong Province approved pilot programs involving Weigao Group and the Bethune Foundation Management Committee. Amidst policy uncertainty at the time, these three private enterprises launched pilot third-party hemodialysis centers through arrangements such as affiliations.

Second, the scope of medical insurance coverage is insufficient.Currently, the coverage of China's basic medical insurance has reached 95%, and critical illness insurance can reimburse approximately 90% of hemodialysis costs. For patients with end-stage renal disease (ESRD), assuming a frequency of three sessions per week at a cost of RMB 500 per session, their annual out-of-pocket expenses can be kept below RMB 10,000 after insurance reimbursement. However, the significant expansion of medical insurance coverage is a development that has occurred only in the past two years. In earlier periods, low insurance coverage among ESRD patients, coupled with the substantial financial burden of hemodialysis, resulted in low treatment rates.

According to a research report by Orient Securities, there are currently 3,637 hemodialysis centers in China, which are mainly concentrated in large public hospitals and hold an absolute monopoly.Following the expansion of critical illness insurance coverage, the number of ESRD patients undergoing hemodialysis will increase significantly.With more than 3,000 hemodialysis centers, supply falls severely short of demand for China’s vast patient population; it is estimated that China needs 30,000 hemodialysis centers.The massive gap cannot be filled by the continued expansion of hemodialysis centers in public hospitals; the remaining substantial market space will be occupied by private institutions, a sector that remains largely undeveloped and ripe for exploration.

In addition, the current penetration rate of hemodialysis centers is low, and their significant expansion will benefit the entire dialysis industry chain, including dialysis machines, dialyzers, dialysis consumables, and dialysis drugs. However, the dialysis machine market is currently dominated by foreign brands such as Fresenius, with a domestic production rate of only 16%, while the localization rate for other hemodialysis consumables and drugs is gradually increasing. Given the high barriers to entry in this sector and the broad benefits to related industries following market expansion, this article will not discuss changes across the entire industry chain.

From a policy perspective, the state has opened hemodialysis centers to private capital and issued corresponding detailed management rules and regulations. It is foreseeable that private capital will subsequently enter this field in large numbers. Early entrants such as 3SBio Inc. and Weigao Group are already positioned within the hemodialysis industry chain, primarily manufacturing related hemodialysis pharmaceuticals and hemodialysis machines. Like industry leader Fresenius, it is a logical progression for these companies to establish dialysis centers and provide dialysis services after entering the chain to produce dialysis products. Therefore, after 2017, the landscape of private hemodialysis centers is likely to witness a flourishing diversity.

Analysis of Overseas Dialysis Service Providers

The business model of chain hemodialysis centers has long been validated internationally. Currently, the two largest global chains in hemodialysis services are Fresenius and DaVita. Fresenius holds a significant market share for hemodialysis machines and consumables, positioning it as an industry giant within the hemodialysis supply chain, while its dialysis centers also command a substantial presence in Europe and the United States. In contrast, DaVita focuses primarily on providing hemodialysis services and is the only company that captures a large share of the hemodialysis service market without having its own line of hemodialysis products.

DaVita

DaVita Inc. is a leading provider of dialysis and related laboratory services for patients with end-stage renal disease (ESRD), comprising two major divisions: DaVita Kidney Care and DaVita Medical Group (DMG, formerly known as HealthCare Partners or HCP). Kidney Care provides hemodialysis, peritoneal dialysis, and related laboratory services, while DMG offers patient- and physician-focused integrated healthcare and management services.

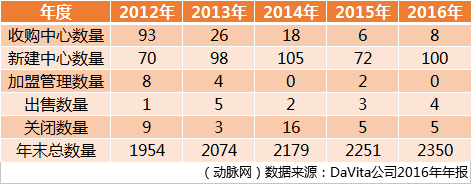

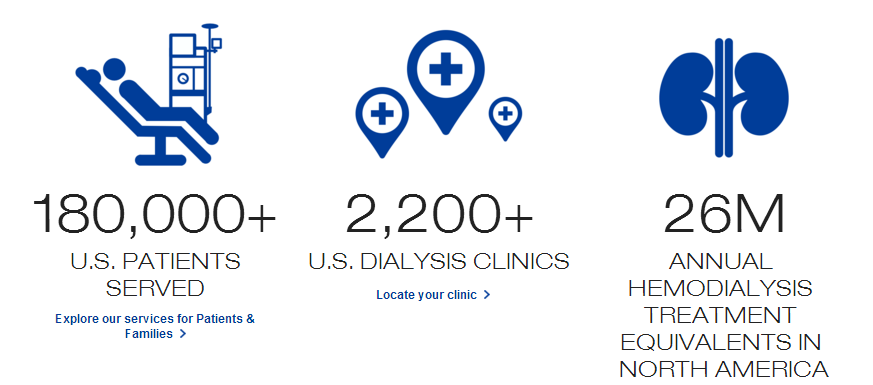

As of December 31, 2016, DaVita operated 2,350 affiliated dialysis centers in the United States. According to statistics from the United States Renal Data System (USRDS), approximately 477,000 patients with end-stage renal disease (ESRD) underwent dialysis in the U.S. in 2014, with DaVita serving a substantial proportion—more than one-third—of these patients. VCBeat reviewed DaVita’s corporate materials and found that in recent years, the company has been adding more than 100 dialysis centers annually. DaVita typically expands its network of affiliated dialysis clinics through three approaches: acquisition, de novo construction, and managed affiliations.

Among these three models, new dialysis centers established before 2012 were primarily acquired, gradually shifting towards newly built facilities, while the franchise management model accounted for a very small minority. As of 2016, among DaVita’s 2,350 dialysis centers, 2,316 were company-owned. Of the 34 managed franchise centers, 27 had non-controlling equity interests, and 7 were wholly owned by third parties.

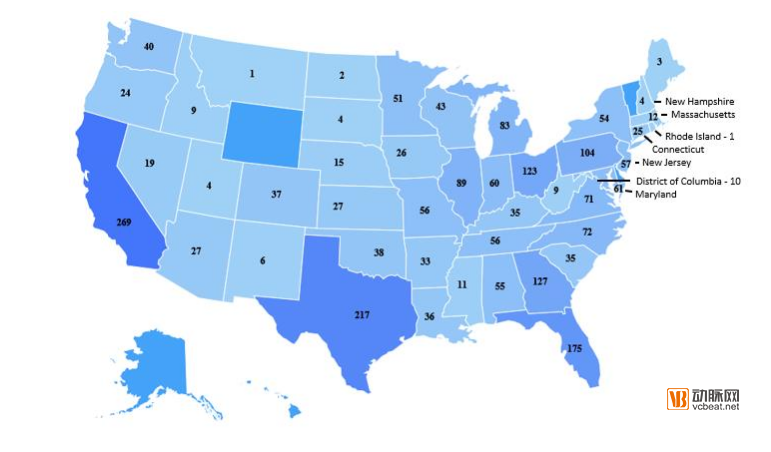

Distribution of DaVita's Dialysis Centers in the United States

In addition to its operations in the United States, DaVita operates 154 dialysis centers globally, primarily in Southeast Asia, with Malaysia having the largest number at 38. In China, DaVita has established three dialysis centers through collaborative partnerships with local hospitals, such as those co-established with Shanghai Yangpu Antu Hospital and Shandong Shunjing Kidney Disease Hospital.

Establishing a new standard DaVita chain dialysis center requires an average investment of $2.8 million, with upfront costs covering leasing, renovation, equipment, and one year of working capital. A new chain dialysis center typically opens within one year of signing the property lease agreement, achieves operating profit in the second year after Medicare certification, and recoups its costs within three to five years. Acquiring an existing dialysis center demands a larger investment, but profitability and cash flow usually normalize more quickly, and performance is easier to predict. Dialysis centers under affiliate management are generally wholly or majority-owned by third parties, with DaVita providing management services and charging management fees based on operational performance.

When providing dialysis services to patients with end-stage renal disease (ESRD), DaVita developed a composite index to measure improvements in clinical outcomes, known as the DaVita Quality Index (DQI). Clinical outcomes measured by the DQI have improved in recent years, and DaVita attributes the direct reduction in mortality among ESRD patients to its high-quality services. The patient mortality rate decreased from 19.0% in 2001 to 13.8% in 2015.

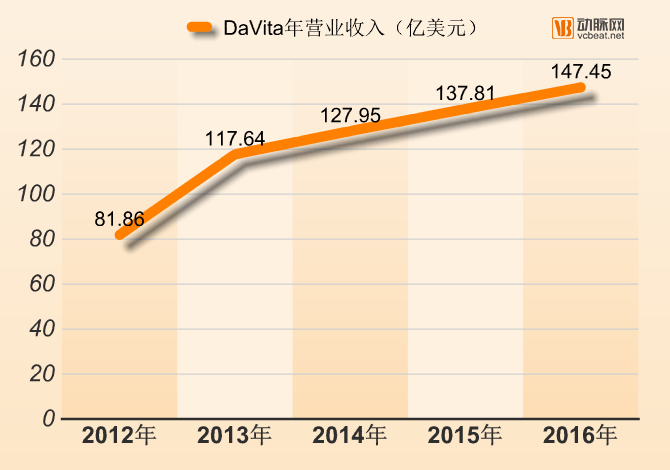

DaVita’s total revenue comprised $9.138 billion from dialysis and related laboratory services, $4.114 billion from DMG medical services, and $1.621 billion from other ancillary services and strategic initiatives; after deducting negative segment revenues, the consolidated net revenue amounted to $14.745 billion.

In addition to providing services through its 2,350 affiliated dialysis centers across the United States, DaVita also delivers acute inpatient dialysis services in approximately 900 hospitals and related laboratory settings. In terms of U.S. dialysis market share in 2016, DaVita and Fresenius held a dominant position, collectively accounting for 72% of dialysis treatments. In 2016, DaVita served approximately 187,700 patients with end-stage renal disease (ESRD), representing an estimated 36% of the U.S. patient population; Fresenius also accounted for 36%, while the remaining 44% of patients received dialysis treatment at hospitals or other non-profit organizations.

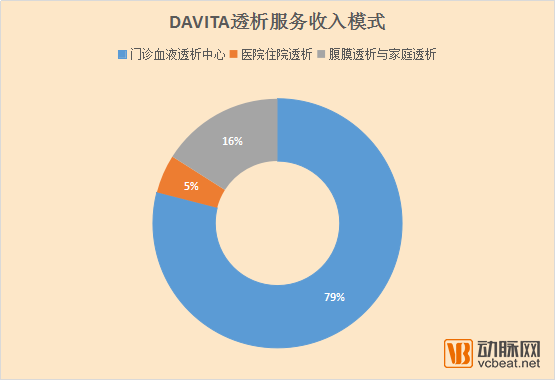

In 2016, dialysis and related laboratory services under DaVita’s Kidney Care segment accounted for approximately 62% of the company’s total revenue. A further breakdown reveals that 79% of the revenue from dialysis and related laboratory services was generated from outpatient hemodialysis services at 2,316 U.S. dialysis centers wholly owned by DaVita; 5% came from hospital-based dialysis services; and the remaining 16% was derived from peritoneal dialysis and home dialysis services. Although the majority of DaVita’s revenue is generated from hemodialysis, peritoneal dialysis still constitutes a significant proportion of its business.

Fresenius

Fresenius Group was founded in 1912 and is headquartered in Bad Homburg, Germany. Fresenius is a healthcare company that provides products and services for dialysis, hospital care, and patient home medical care. In addition to owning and operating outpatient dialysis centers worldwide, Fresenius Medical Care (FMC) also manufactures a full range of dialysis supplies and equipment. This gives Fresenius a cost advantage in operating outpatient dialysis centers, as it has the capability to produce the products it uses.

The Fresenius Group comprises several major divisions. Fresenius Medical Care (FMC) is the world’s leading provider of dialysis equipment, products, and medical services, and it operates dialysis outpatient centers. Fresenius Kabi is a leader in intravenous drugs, infusion therapy, clinical nutrition, and medical devices. Fresenius Helios is one of Europe’s largest and medically advanced hospital groups. Fresenius Vamed provides design, construction, and operational management services for healthcare projects. Therefore, the Fresenius entity relevant to this article is FMC.

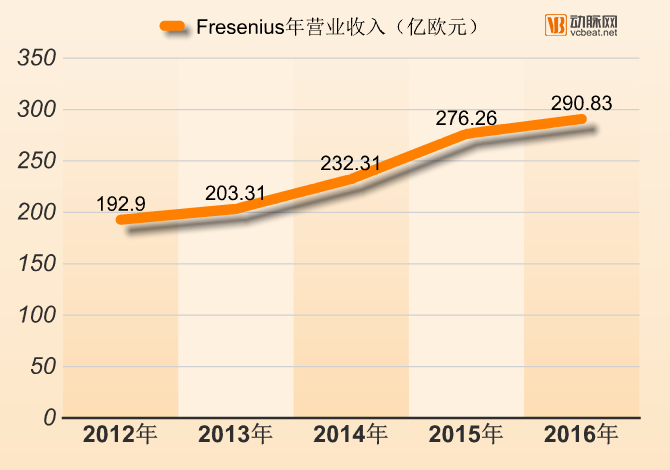

In 2016, the Fresenius Group reported total revenues of €29.083 billion, representing a modest 5% increase from 2015. However, this followed substantial growth in preceding years, with revenues rising by nearly €10 billion compared to 2012. Among its four divisions, Fresenius Medical Care (FMC) generated $17.911 billion in revenue (reported in USD), accounting for the largest share of the Group’s total income. The other divisions reported revenues as follows: Fresenius Kabi at €6.007 billion, Fresenius Helios at €5.843 billion, and Fresenius Vamed at €1.16 billion. In 2016, the Fresenius Group’s profit amounted to €4.327 billion, with a pre-tax margin of 14.9% and a 12% growth in net income.

As a vertically integrated company, FMC’s business comprises two major segments, providing products and services across the entire dialysis industry chain. FMC’s dialysis products are sold in 120 countries worldwide, with production facilities established in 37 countries. The outpatient dialysis centers we focus on fall under FMC’s dialysis services segment. As of the end of December 2016, FMC had operated 3,624 dialysis centers globally, serving 208,471 patients throughout the year.

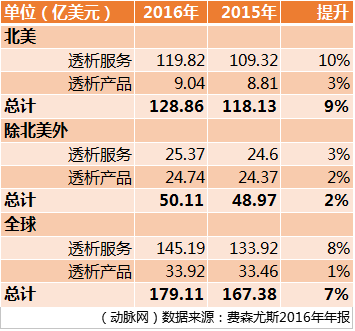

In Fresenius Group's annual report, 2016FMC's total revenue amounted to $17.911 billion.After excluding sales revenue from dialysis products, the revenue from dialysis services amounted to $14.519 billion, which is very close to the turnover of DaVita, a company dedicated solely to dialysis services. In North America, due to market saturation of dialysis centers, sales of dialysis machines and other related products were very low, totaling only $904 million—a mere fraction of the revenue generated by dialysis services. In markets outside North America, however, revenues from dialysis products and dialysis services were comparable. Globally, revenue from dialysis services far exceeded that from dialysis product sales, which explains why medical device manufacturers are leveraging their technological and cost advantages to enter the healthcare services sector.

FMC operates 3,624 clinics across 45 countries worldwide, with the United States remaining its key market. Among these, there are 2,306 dialysis centers in North America, 711 in Europe, the Middle East, and Africa, 233 in Latin America, and 374 in the Asia-Pacific region, representing a 6% increase in the number of centers compared to 2015. In 2016, FMC held a 38% market share in the United States, providing dialysis services to approximately 185,000 patients with end-stage renal disease (ESRD). Together with DaVita, the two companies accounted for 75% of the U.S. market (this figure slightly differs from DaVita’s annual report, which states that DaVita and FMC each held a 36% share, totaling 72%).

Based on the annual report data of the two companies, we can conclude that independent chain dialysis centers have achieved significant success in the United States. Chain dialysis centers have not only captured a substantial share of the overall dialysis market, facilitating patient care, and monopolistic chain enterprises have also emerged. Compared with hospitals, dialysis centers under chain management not only enjoy procurement price advantages in equipment and consumables but can also increase profits by improving management standards.

Current Status of the Chinese Market

Currently, there are approximately 3,600 registered hemodialysis centers in China, with fewer than 20 independent hemodialysis centers currently in the pilot phase. Following the relaxation of national policies, private hemodialysis centers, which are currently in a nascent and unregulated stage, may experience rapid growth in the short term.

Independent hemodialysis centers previously experienced relatively slow development. In addition to licensing challenges, there was a shortage of physician resources. Hemodialysis centers are subject to stringent management requirements regarding facilities, physicians, and nurses, and cultivating these capabilities requires a prolonged period. Most private hemodialysis centers in China previously adopted a collaborative model with hospitals, which not only helped secure patient referrals but also enhanced brand recognition. However, for future continued growth and expansion, particularly toward community-based and primary care-oriented services, a significant number of independent hemodialysis centers are expected to emerge.

The data provided in FMC's annual report shows that,In 2016, the global market for dialysis services (including renal pharmaceuticals) was valued at approximately $62 billion, while the market for dialysis products, such as dialysis machines, totaled around $14 billion. Given that the dialysis services market is substantially larger than the dialysis products market, domestic and international manufacturers of dialysis products are leveraging their cost advantages or specialized expertise to enter the dialysis services sector.

As previously mentioned, Shandong Weigao, which has already begun piloting independent hemodialysis centers, is a medical device manufacturer whose core business includes equipment and products related to blood purification. It collaborates with Japan’s Nikkiso to produce dialysis equipment, including dialysis consumables such as dialyzers and dialysis tubing.In 2016, Shandong Weigao's total revenue reached RMB 6.73 billion, with revenue from blood purification products amounting to RMB 1.094 billion (covering only hemodialysis products, excluding hemodialysis services).Leveraging its strengths as a manufacturer of hemodialysis equipment, Shandong Weigao undertook the pilot construction of “public welfare independent blood purification centers” initiated by the Ministry of Health. To date, it has invested in and established three independent blood purification centers in Weihai City, deploying more than 100 dialysis machines. However, its expansion pace remains too slow, and it has not yet rolled out operations comprehensively across Shandong Province or nationwide.

Tightening Risk Control

However, the policy-driven liberalization of hemodialysis centers does not warrant a relaxation of safety risk controls. In January this year, a serious hospital-acquired infection incident occurred in the hemodialysis unit of a hospital in Qingdao, Shandong Province, where nine patients contracted hepatitis B due to violations of infection prevention and control protocols. The National Health Commission’s “Basic Standards and Management Specifications for Hemodialysis Centers (Trial)” imposes stringent requirements on safety and infection prevention and control, some of which pose challenges to the development of private capital investment in this sector.

Hemodialysis treatment carries a high risk of infection and numerous complications, necessitating a balance between accessibility and safety. First, the document mandates that within a 10-kilometer radius of any hemodialysis center, there must be a general hospital at Level II or above with the capability to manage acute complications. The center must sign a medical service agreement with such a hospital for the treatment of patients experiencing acute hemodialysis-related complications, establish a “green channel” for expedited care, and ensure unimpeded patient referrals. Second, the hemodialysis center shall establish a collaborative relationship with at least one tertiary general hospital in the region that possesses the capacity to diagnose and treat chronic complications associated with hemodialysis. It must sign a medical service agreement with this hospital for the management of patients with chronic hemodialysis-related complications, create a “green channel,” and set up a two-way referral system.

These two agreements are mandatory documentation required during the annual inspection of hemodialysis centers. This regulation may ultimately position secondary and tertiary general hospitals as the “gatekeepers” for independent hemodialysis centers. Given that competition and challenges in implementing two-way referral systems already exist among public hospitals, signing these agreements poses a significant challenge for social capital–backed medical institutions.

In developed countries, the hemodialysis industry ranks as the second-largest niche market in healthcare services, whereas it is currently in its nascent stage in China. In the future, it will become a highly strategic segment within the medical services market. With the widespread adoption of critical illness insurance and the relaxation of national policies, the chain cooperation model for hemodialysis centers is poised for rapid development in China. Not only will domestic private enterprises enter this field, but DaVita and Fresenius, which have long coveted the Chinese market, will also rapidly capture market share. By providing specialized and segmented services, DaVita and Fresenius have become global leaders. Domestic companies can benchmark against them, drawing insights to uncover a new blue ocean in the healthcare sector within the hemodialysis service industry.