Startup Health Releases Q1 2017 Digital Health Funding Report: Total Investment Reaches $2.5B, Seed-Stage Funding Drops 50% Year-over-Year

As one of the most influential digital health startup accelerators globally, Startup Health has continued to expand its reach in recent years. Its portfolio now comprises nearly 200 companies across five continents and 18 countries. The various rankings it regularly publishes have also garnered widespread attention from all sectors of the industry.

As soon as the first quarter of 2017 concluded, Startup Health released its Q1 2017 Funding Report (with data current as of March 31, 2017). VCBeat (WeChat ID: vcbeat) brings you the full translated text of the report without delay; see below for details.

StartUp Health has invested heavily in 10 “Health Moonshots,” committing to improving global human health across all dimensions over a 25-year period. Each “Health Moonshot” has the potential to benefit at least one billion people.

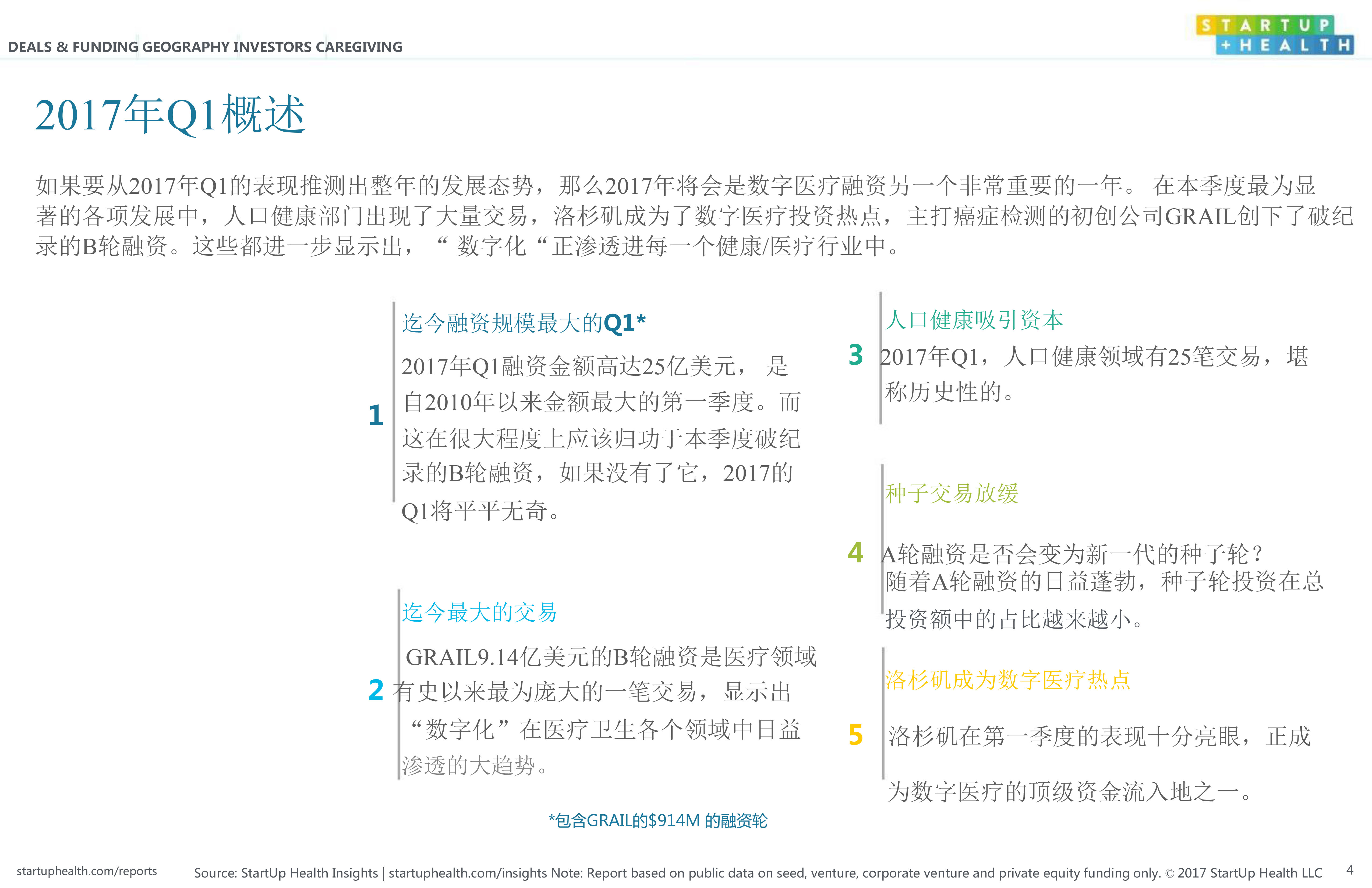

Among the most notable developments this quarter, the population health sector saw a surge in transactions, Los Angeles emerged as a hotspot for digital health investment, and GRAIL, a startup specializing in cancer detection, set a record with its Series B financing round. These trends further demonstrate that “digitalization” is permeating every segment of the healthcare and medical industries.

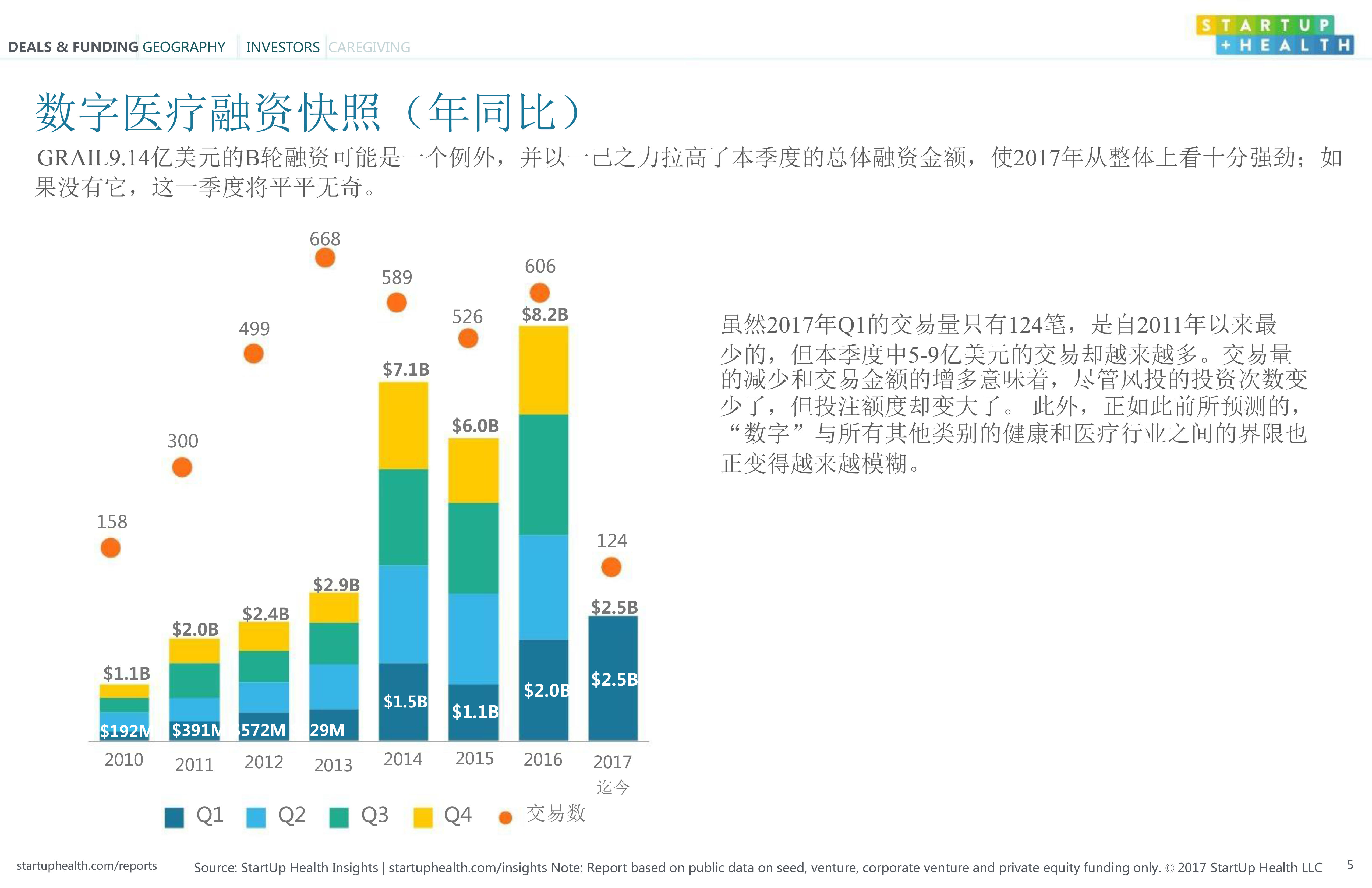

In Q1 2017, the number of transactions stood at only 124, the lowest since 2011; however, deals valued between $500 million and $900 million became increasingly frequent. The decline in transaction volume coupled with the rise in deal size indicates that although venture capital firms reduced the frequency of their investments, they significantly increased the amount committed per deal.

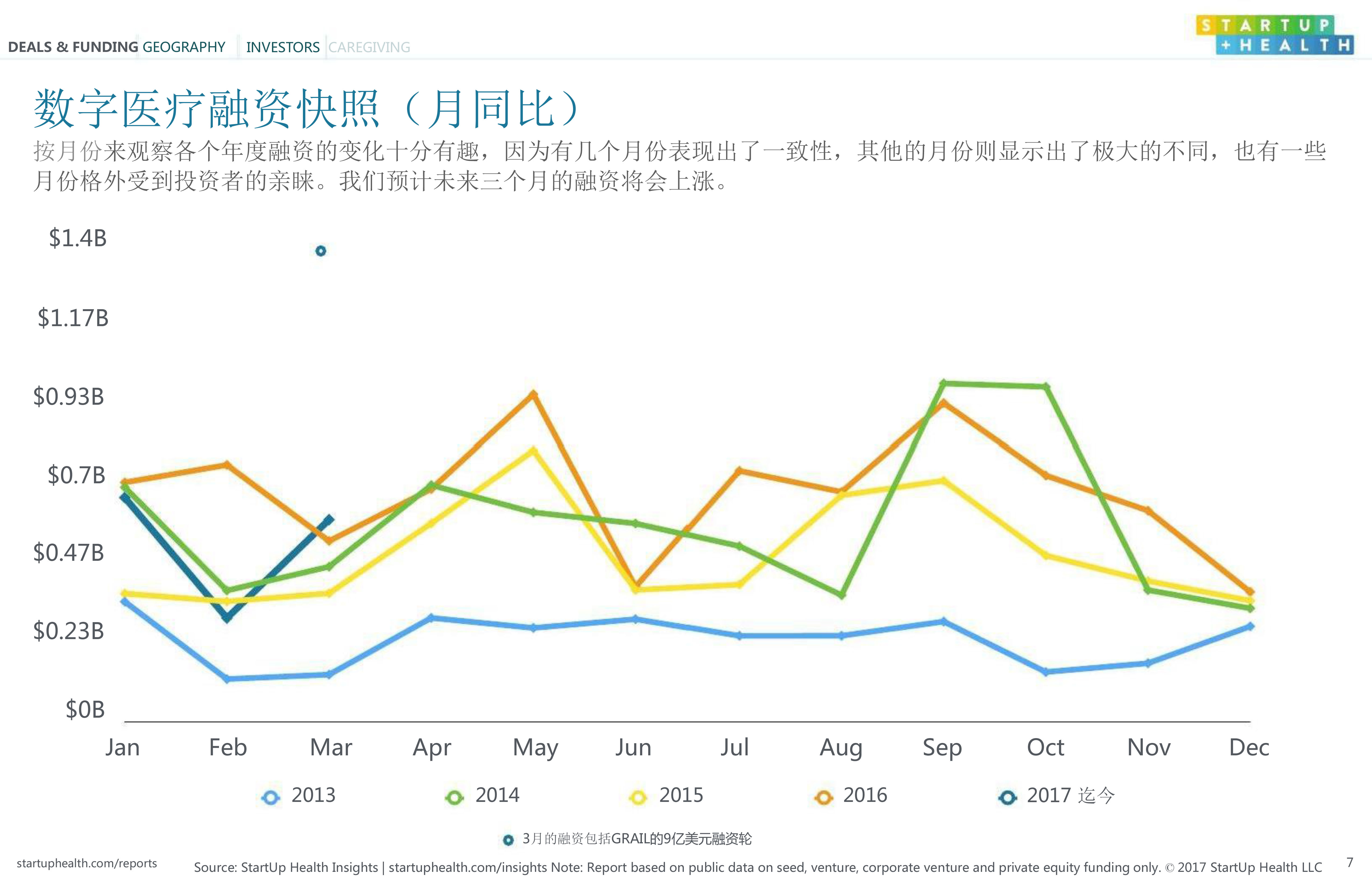

Q1 2017 continued to show varied financing trends, but overall remained in positive territory, indicating that the digital health industry is continuing to develop. March 2017 has now become the month with the largest financing scale in history.

An overall observation of the changes in financing across different years is quite intriguing. Several months have shown consistency, while others have exhibited significant variations. May and September, in particular, have been highly favored by investors. We anticipate that financing will increase over the next three months.

Among the top ten deals in Q1 2017, many were distributed across subsectors that had rarely seen large-scale transactions. This indicates that 2017 presented a breakthrough year for solutions in population health, EHR innovation, and e-commerce.

If patient populations cannot be stratified by risk, providers (including hospitals and healthcare organizations) will struggle to triage patients, implement disease prevention measures, and deliver personalized care. Last year, some providers began adopting population health platforms for population segmentation and as a foundation for building more advanced solutions. Year-to-date, there have been 23 transactions in this sector, with funding amounts nearly double those of other fields.

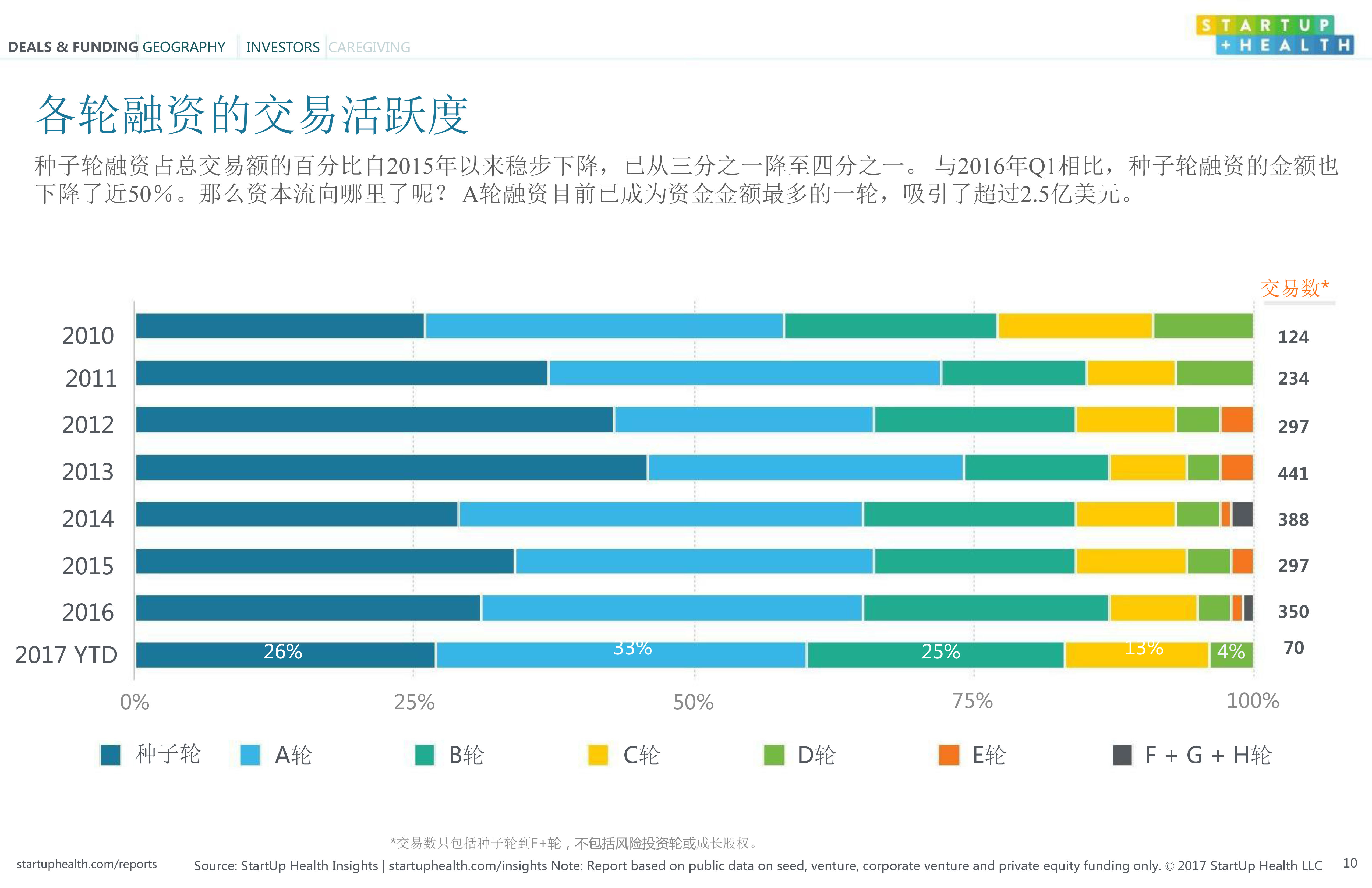

The percentage of seed-stage financing in total transaction value has steadily declined since 2015, dropping from one-third to one-quarter. Compared with Q1 2016, the amount raised in seed-stage financing has also decreased by nearly 50%. Series A financing has now become the round with the largest capital inflow, attracting over $250 million.

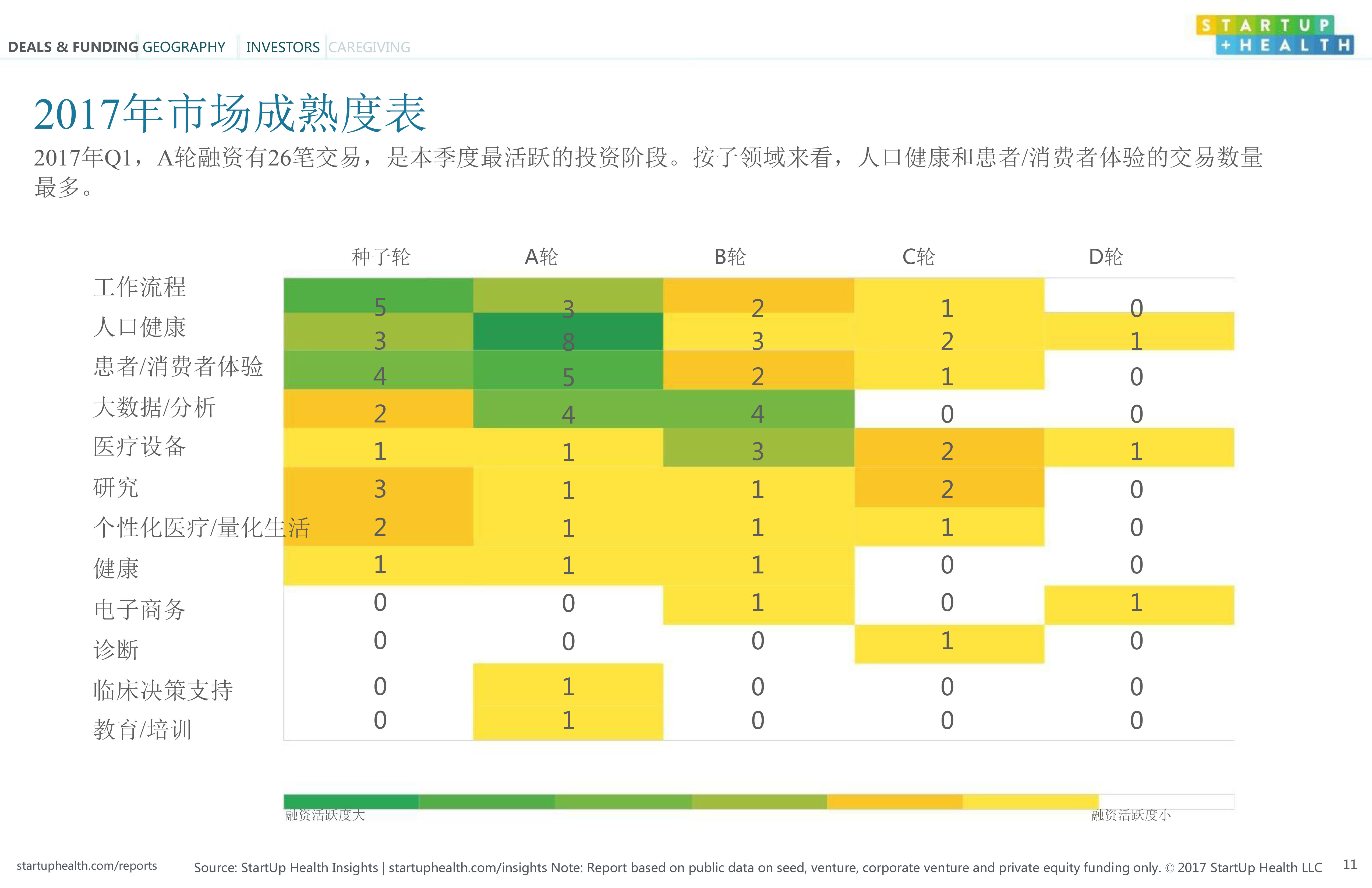

In Q1 2017, Series A financing saw 26 deals, making it the most active investment stage of the quarter. By subsector, population health and patient/consumer experience recorded the highest number of transactions.

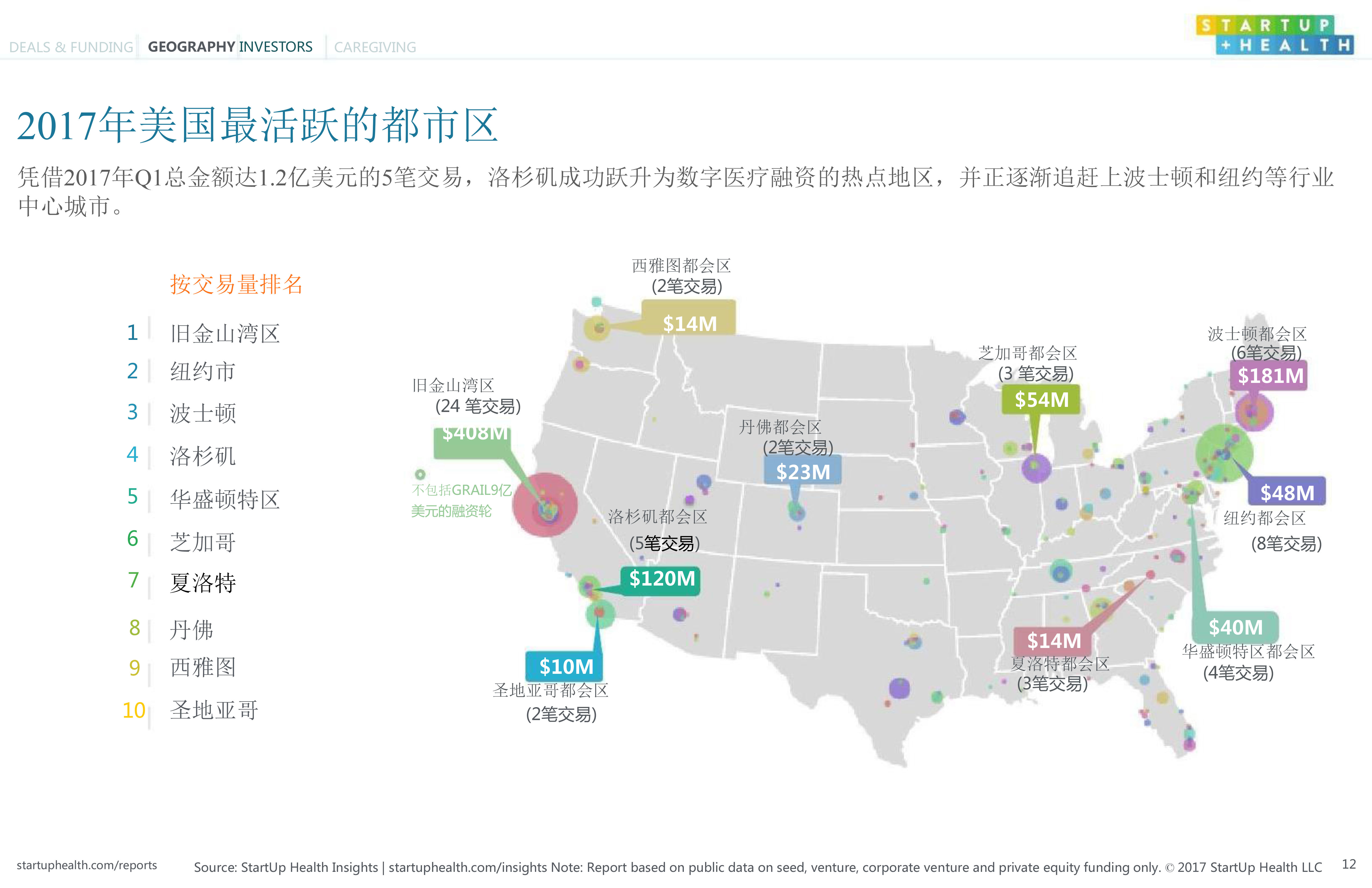

With five deals totaling $120 million in Q1 2017, Los Angeles has successfully emerged as a hotspot for digital health financing and is gradually catching up with industry hubs such as Boston and New York.

Venrock took the lead this quarter with four investments. Many other investors also closed two to three deals, marking an increase compared to their transaction volumes in the first quarters of previous years.