China's Medical Robotics Industry Landscape: 2 Listed Companies, 12 Funded Startups, and Nearly One-Third of Teams from Harbin Institute of Technology

The field of medical robotics has long been regarded as the “crown jewel” of both the broader robotics sector and the medical device industry. Due to its reliance on complex, cutting-edge multidisciplinary technologies and its potential to bring about significant impact and transformation for public welfare and industry alike, this high-barrier, high-value domain is often referred to as the “aerospace engineering” of the medical field. Nevertheless, robots offer unparalleled advantages in terms of precision, stability, strength, and endurance, making their application in the highly specialized field of medicine widely anticipated.

Medical robots are intelligent service robots available in various types. Based on their applications, they can be categorized into clinical medical robots (including surgical robots and diagnostic and therapeutic robots), companion robots, nursing robots, rehabilitation robots, patient transfer robots, and medication delivery robots. According to the currently prevalent classification system, they are divided into four categories: surgical robots, rehabilitation robots, assistive robots, and service robots.

According to data from Boston Consulting Group (BCG), as of January 2016, the global medical robotics industry achieved annual revenues of $7.47 billion. The compound annual growth rate is projected to remain stable at 15.4% over the next five years, paving the way for a trillion-dollar industrial chain in the future.

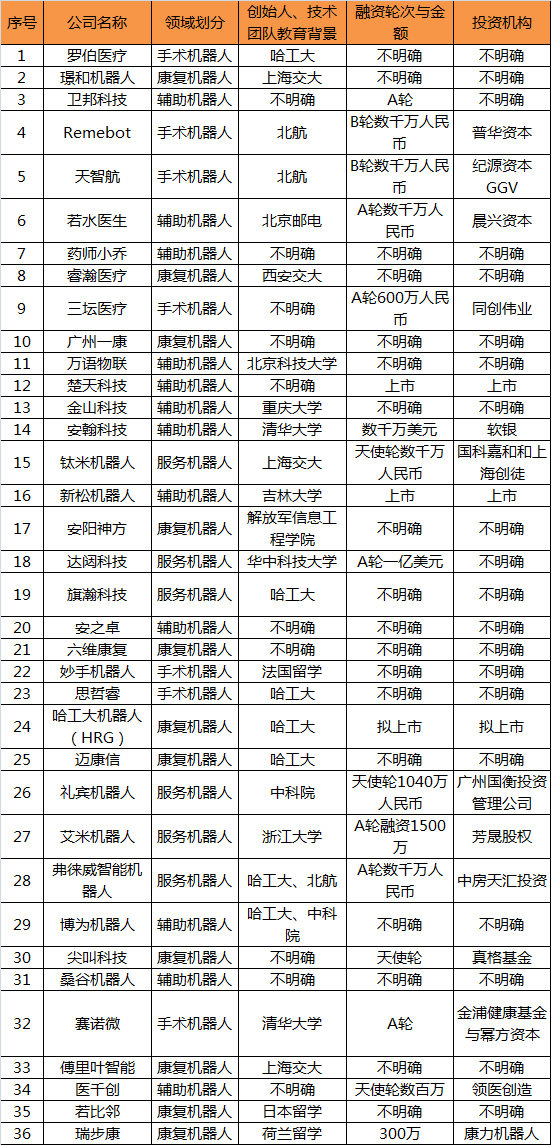

In this regard, VCBeat(WeChat:vcbeat)A Review of China’s Medical Robot Companies: Understanding the Current State of DevelopmentVCBeat has compiled a list of 36 medical robot companies in China. Among them, two are publicly listed: Chu Tian Technology and Siasun Robot & Automation. A total of 12 companies have secured financing, with the total funding amounting to approximately RMB 801.4 million (figures stated as “tens of millions” or “millions” were calculated as RMB 10 million and RMB 1 million, respectively).

Since the robotics sector is a tangible industry, and 18 companies have not disclosed their financing details, the actual total financing amount is significantly higher than RMB 800 million.

Additionally, during the inventory process,VCBeat has uncovered a surprising fact: among all founders or core technical teams whose educational backgrounds are publicly available, more than 28% attended Harbin Institute of Technology (hereinafter referred to as HIT), making HIT a veritable talent incubator for China’s medical robotics industry.。

//Due to constraints on time and information volume, we acknowledge that the data collected herein is not exhaustive. Enterprises and institutions not included are encouraged to contact us. Additionally, while research and development achievements by Chinese academic and research institutions in the field of medical robotics have been remarkable, they are not covered in this review but will be discussed separately in the article.//

Medical Robotics Company Landscape

Over 28% of the research teams and founders are from Harbin Institute of Technology

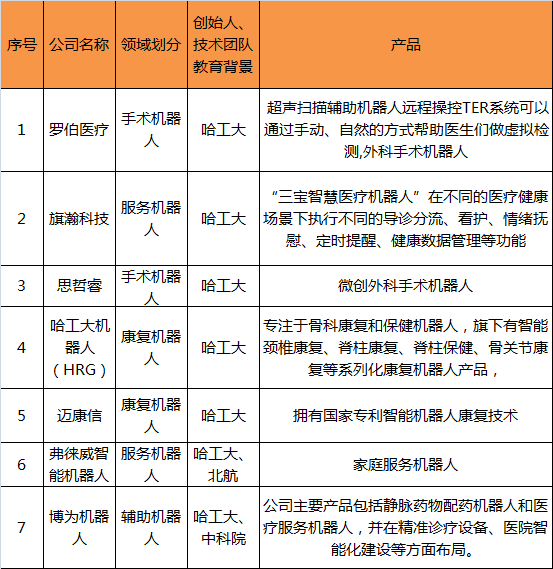

Among the 36 medical robotics companies collected, excluding 10 with unclear team information, 7 out of the remaining 25 companies had founders or core technical teams from Harbin Institute of Technology (HIT), accounting for over 28%.

Of course, besides Harbin Institute of Technology (HIT), there are two companies founded by Tsinghua University alumni, three by Shanghai Jiao Tong University alumni, and three by Beihang University alumni. However, these figures fall significantly short compared to HIT. Driven by curiosity, the reporter set out to explore why Harbin Institute of Technology is so formidable in the field of robotics.

Harbin Institute of Technology has a State Key Laboratory of Robotics and Systems., is one of the earliest institutions in China to conduct research on robotics. Its predecessor was primarily the Robotics Research Institute of Harbin Institute of Technology, established in 1986. As early as the 1980s, it developed China’s first arc welding robot and the first spot welding robot.

Harbin Institute of Technology’s excellence in talent cultivation is attributable not merely to its teaching quality, but more significantly to the integration of industry, academia, and research. It was jointly established through investments from Harbin Institute of Technology, the Heilongjiang Provincial People’s Government, and the Harbin Municipal People’s Government.Harbin Institute of Technology Robotics Group(HRG),There are 14 robotics-related enterprises under the Harbin Institute of Technology Robotics Group alone., with Harbin Tianyu Rehabilitation Medical Robot Co., Ltd. and Zhikang Medical Technology Co., Ltd. not yet included in this inventory.

InRepresentative Figures, I believe everyone is familiar with Professor Sun Lining, as he can be seen at almost most conferences and forums related to medical robotics. He is mainly engaged in research on nanoscale micro-actuation and micromanipulation robots, high-speed and high-precision mechanisms, industrial robot technology, parallel robots, medical robots, micro and small robots, humanoid arms, and robotic mechanisms and control.

Strength of Other Institutions

Of course, besides Harbin Institute of Technology, Beihang University also boasts extraordinary strength.Beihang University has a Robotics Institute., founded in 1987 by Academician Zhang Qixian, is a research entity integrating teaching, scientific research, and development. Its current medical and service robot products include:Small modular orthopedic robotic systems, spinal grinding navigation and robotic systems, curtain wall cleaning robots, digital operating tables, integrated bed-chair systems, and stereotactic brain robots.

Beihang University and the Navy General Hospital Jointly Developed a Brain Surgery Robot, obtained CFDA certification, has completed thousands of clinical surgeries.

Beihang University'sProfessor Wang TianmiaoHe is also renowned in this field, having achieved outstanding results in advanced robotics, including medical robots, bionic robotic fish, and embedded technologies. He currently serves as a Senior Technology Advisor to multiple investment firms, including ZhenFund and Yari Capital.

In September 2013, the Shenzhen Institute of Advanced Technology, Chinese Academy of Sciences (CAS), developed a spinal surgery robot capable of integrating with existing infrared tracking and positioning systems to achieve accurate, real-time intraoperative localization of surgical instruments.

The Hong Kong Polytechnic University has successfully developed the world’s first motor-integrated robotic system specifically designed for surgery, known as the Novel Surgical Robotic System (NSRS). This research leverages surgical clinical expertise from the Li Ka Shing Faculty of Medicine at the University of Hong Kong and has been successfully tested in animal trials. The technology is expected to enter clinical testing within two years, with a market launch anticipated as early as 2019.

In summary, Harbin Institute of Technology, Beihang University, Tsinghua University, and Tianjin University are the leading institutions in medical robot R&D in China. Their developed products span various categories, including surgical, rehabilitation, service, and assistive robots, essentially representing the highest level of medical robotics in the country. HR professionals from robotics companies seeking to recruit talent should act quickly to secure graduates from these universities.

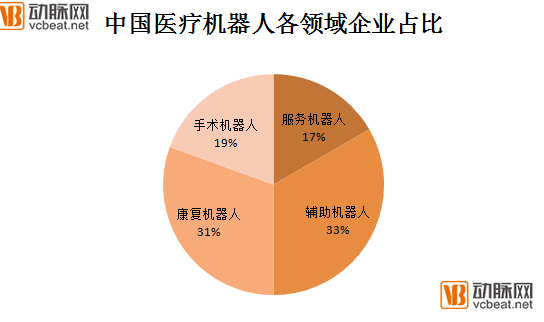

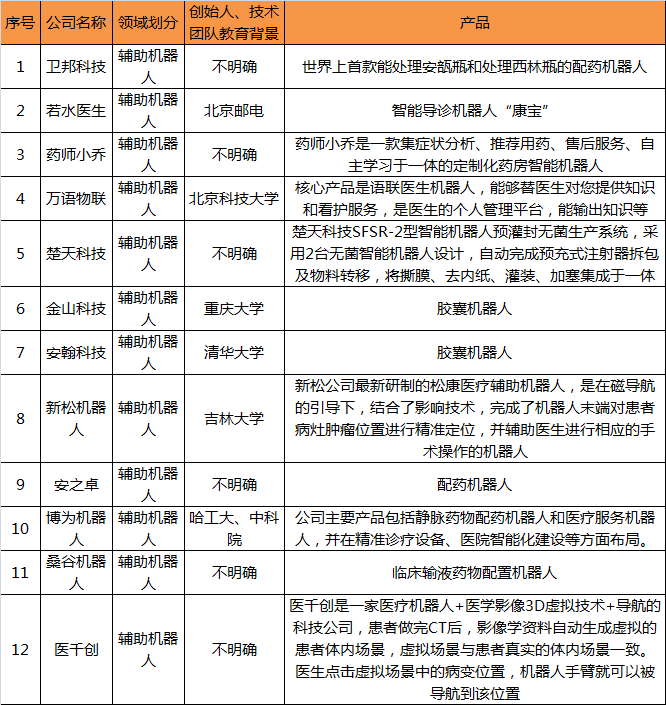

Among the 36 medical robotics companies listed by VCBeat, there are 7 surgical robot companies, 11 rehabilitation robot companies, 12 assistive robot companies, and 6 service robot companies.

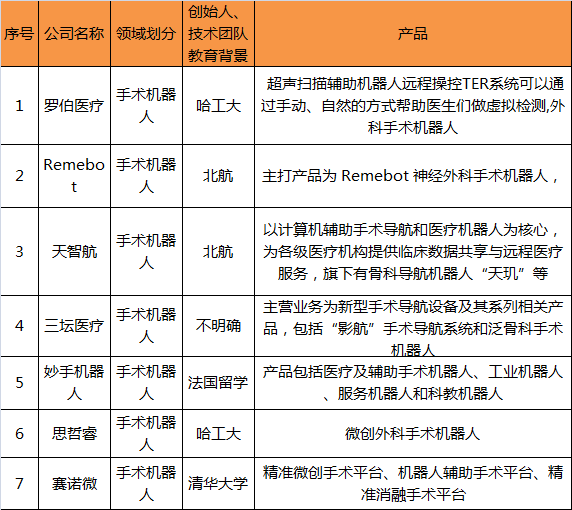

Surgical Robot

Surgical robots broadly include laparoscopic surgical robot systems, orthopedic surgical robot systems, neurosurgical robotic systems, steerable robotic catheters, and other clinical surgical robots.

China Investment Advisor stated in the "In-Depth Research and Investment Prospect Forecast Report on China's Medical Robot Industry (2016-2020)" that surgical robots account for more than 60% of the global medical robot market, representing the largest share. Among these, laparoscopy is the largest application area for surgical robots, accounting for 88.5% of the surgical robot industry. Other clinical surgical robots account for 11.5%. In the future, as minimally invasive surgery requires only incisions ranging from 5 millimeters to 1.5 centimeters, enabling complex surgical procedures with minimal patient trauma, the development prospects for surgical robots will become increasingly broad.

For example, the Shenzhen RoboMedical surgical robot-assisted system, or surgical robots in general, can help physicians perform various procedural steps by using computer and software technologies to control and maneuver surgical instruments through small incisions (minimally invasive) into the patient’s body.

Surgical robot-assisted systems include navigation functions that facilitate minimally invasive surgery and assist in navigating complex areas within the human body that are difficult to access, while also shortening postoperative recovery time. The device is not actually a robot, as it still requires human operation during surgery. Surgical computer replication systems typically consist of the following components:

A console for the surgeon to sit on during surgery. The console serves as the system's control center, allowing the surgeon to observe the procedure and instrument movements via images from an endoscope displayed on a 3D screen.

The cart beside the patient bed contains three to four chain-fixed robotic arms, a camera (endoscope), and surgical instruments controlled by the physician during the procedure.

Components separated from the cart include hardware and software support elements, such as an electronic surgical integration system, a suction-irrigation pump, and an endoscopic light source unit.

Most surgeons use a variety of surgical instruments to assist computer-assisted surgical systems, such as scalpels, medical forceps, graspers, dissectors, cautery devices, scissors, retractors, and irrigators.

Rehabilitation Robots

In this inventory, rehabilitation robot companies accounted for the highest proportion, at around 31%.The development of rehabilitation robotics enterprises is closely tied to shifts in demographic structure and disease patterns, favorable policies, a scarcity of market products, and the urgent need for intelligent rehabilitation solutions.

Population aging has increased the risk of disability and the number of people with disabilities. Due to age-related physiological decline, older adults face higher incidence rates and greater risks of disability from conditions such as cerebrovascular disease, osteoarthropathy, and stroke. Furthermore, the long-standing acute-care model for managing chronic diseases has led to increasingly high disability rates among chronic disease patients. Rehabilitation robots can facilitate efficient treatment and rehabilitation for patients with mobility impairments, including those resulting from stroke, traumatic nerve injury, spinal cord injury, limb disabilities, and age-related mobility limitations.

Since 2009, the State Council, the National Health and Family Planning Commission, and other ministries have successively introduced policies to encourage and support the growth and development of rehabilitation medicine. The "Several Opinions on Promoting the Development of the Health Service Industry" specifically proposed that public secondary general hospitals and enterprise-affiliated hospitals transform into rehabilitation hospitals, and that eligible institutions equip themselves with intelligent devices such as rehabilitation robots according to operational needs. At the State Council executive meeting chaired by Premier Li Keqiang on October 14, 2016, it was explicitly stated that the development of the rehabilitation assistive device industry should be vigorously promoted, and industrial upgrading should be facilitated through policies such as social insurance benefits and corporate income tax incentives.

In addition, in accordance with the "Notice on Including Additional Medical Rehabilitation Items in the Scope of Basic Medical Insurance Coverage" jointly issued by the Ministry of Human Resources and Social Security, the National Health and Family Planning Commission, and other departments, the number of rehabilitation items covered by medical insurance increased from 9 to 29 starting June 30, 2016. Furthermore, medical rehabilitation items previously included in the scope of medical insurance coverage in various regions were retained. Among these, kinesiotherapy, comprehensive limb training for hemiplegia, and hand function assessment are all included in the scope of medical insurance coverage.

According to data from the National Health and Family Planning Commission, by the end of 2012, among nearly 10,000 hospitals at Level II or above nationwide, approximately 3,288 general hospitals actually had rehabilitation departments. Additionally, according to statistics from the China Disabled Persons’ Federation, by the end of 2014, there were a total of 6,914 rehabilitation institutions across China, including 2,181 institutions providing rehabilitation training services for physical disabilities. Given the current human and material resources, these institutions can deliver rehabilitation training to 367,000 individuals with physical disabilities, whereas the number of people with physical disabilities in China exceeds 24 million.

Currently, the world's leading rehabilitation robotics companies include:Hocoma、Lokomat、Armeo、Erigoetc. Domestic companies, such as Guangzhou Yikang, have already marketed their products, which mainly include intelligent feedback training systems for the upper and lower limbs. Developed by simulating the movement patterns of human fingers and wrists in real time, these systems feature assessment capabilities for finger flexor and extensor muscle strength signals, enabling training for both the hand and wrist.

Ruihan Medical’s Wearable Hand Rehabilitation Robot. This device advances rehabilitation from basic muscle recovery to neuronal rehabilitation of the brain by utilizing residual electromyographic (EMG) signals from the hand to control the robotic exoskeleton. When the brain issues active motor commands, it induces changes in surface EMG activity of the hand; capture electrodes detect these signal changes, which are then processed to drive the movement of the robotic hand.

Currently, the prices of these domestically produced rehabilitation robots range from 200,000 to 600,000 yuan.

Assistive Robot

Auxiliary medical robotics companies accounted for 33% of this review. In fact, there is currently no precise definition of auxiliary medical robots; this review was conducted by VCBeat.Capsule robots, IV drug preparation robots, surgical assistance robots, virtual assistants, and patient guidance robots are all categorized as assistive robots.。

According to VCBeat, thermal ablation therapy has been recognized by major hospitals both domestically and internationally as a reliable method for tumor treatment. Consequently, the auxiliary robots used in conjunction with this technique have also garnered significant attention from these institutions, indicating substantial market growth potential. The newly developed Songkang Medical Auxiliary Robot by SIASUN Robotics integrates imaging technology under magnetic navigation guidance to precisely locate tumor lesions at the robot’s end-effector, thereby assisting physicians in performing surgical procedures.

Robots for Assisted Surgery: To ensure surgical precision, the Siasun robot can achieve multi-position and multi-angle positioning of the upper human body, and, guided by magnetic localization sensors, avoid interference from skeletal structures during needle insertion. In terms of process design, the medical assistance robot integrates the robotic main body, thermal ablation equipment, navigation system, and treatment bed into a single unit. The development of this robot is the result of multidisciplinary integration.

Infusion Drug Preparation Robot: With the advancement of medical technology, the preparation model for intravenous hazardous drugs has gradually evolved from preparation in general treatment rooms to centralized preparation in biological safety cabinets, and currently to an automated preparation model that replaces manual labor. The WEINAS Intelligent Intravenous Medication Preparation Robot, independently developed by Weibang Technology, is primarily designed for the preparation of hazardous drugs. Addressing clinical needs, it leverages a unique intelligent technology platform to handle the preparation of over 90% of vials and ampoules in current clinical practice, while supporting various solvents and infusion modes.

Capsule Robot: Anhan’s independently developed magnetically controlled capsule gastroscopy robot has revolutionized traditional gastroscopy with its innovative “tubeless” approach. Patients simply swallow a capsule-sized robotic gastroscope, enabling a painless, non-invasive, and cross-infection-free examination within 15 minutes—without the need for anesthesia. After the procedure, the capsule robot is naturally excreted through the digestive tract as a single-use, non-retrievable device.

Virtual Assistant: Leveraging advanced technologies such as cloud computing, IOE, and Web 3.0 semantics, Wanwu Yulian has developed a suite of cognitive technologies, including the SEMIOE Bio-Meta Engine—which features self-aware learning capabilities and can understand complex data and form structured knowledge akin to the human brain—thereby creating a comprehensive artificial intelligence system that leads the global industry. The company is dedicated to providing products, services, and solutions for the connectivity of intelligent medical devices, personal dataset management, and health knowledge operations.

Pharmacist Xiao Qiao is a customized intelligent pharmacy robot that integrates symptom analysis, medication recommendations, after-sales service, and autonomous learning.

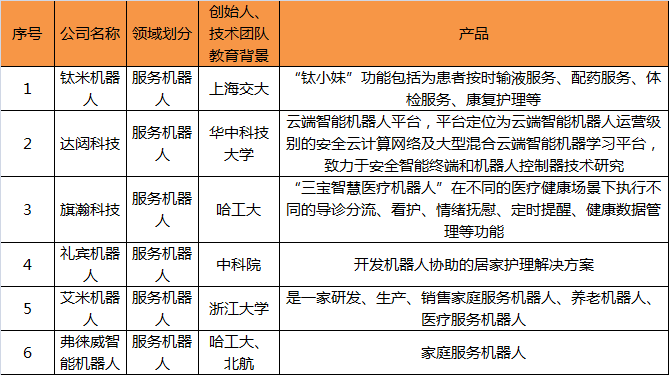

Service Robots

In this classification, service robots primarily include those that assist nurses with infusion services, medication dispensing, and physical examinations, as well as enterprise- and home-based care, service, and companion robots designed for emotional support.

The functions of Timi Robot's specialized medical service robots include scheduled infusion services, medication dispensing, physical examinations, and rehabilitation care. Physicians can also make diagnoses based on data collected by the robots. Furthermore, these specialized medical service robots can replace certain healthcare personnel in work environments with radiation or infectious hazards, thereby providing better protection for medical staff.

Companion robots are primarily designed to assist the elderly and children in their daily lives. They feature four core functions: service provision, safety monitoring, human-computer interaction, and multimedia entertainment.

Amy Robot’s product features primarily include pure voice-controlled interaction, smart home control, online health management, online educational tutoring, autonomous security patrols, intelligent navigation and positioning, customized shopping guidance, and remote video calling, thereby enabling diverse application scenarios.

For instance, AMY-A1 can provide intelligent services to users in areas such as smart homes, healthcare, online learning, emotional companionship, and home security. Meanwhile, AMY-M1 may be customized to meet the specific needs of different enterprises in the future, serving as a “shopping guide” in malls or a “roving nurse” in hospitals.

From the demand side, China’s medical robot market offers substantial growth potential. On the payment front, out-of-pocket expenses currently dominate, although the proportion covered by insurance is gradually increasing. From a supply perspective, the industry features certain technical barriers and remains in a phase of collective market expansion. Finally, from an investment standpoint, the sector has attracted significant capital interest and warrants continued attention.

As market demand requires cultivation and reimbursement from medical insurance payers remains limited, the investment payback period for medical robots is relatively long. However, profit margins are expected to gradually improve with sales expansion and economies of scale. We hope that China’s robotics industry will achieve sustainable long-term development, with enterprises comparable to “da Vinci” emerging as soon as possible. This will require concerted efforts from academic and research institutions, capital investors, enterprises, and the government.

Copyright Statement

This report is produced by VCBeat. All text, images, and tables contained herein are protected by applicable trademark and copyright laws. Portions of the text and data have been sourced from publicly available information, with ownership retained by the original authors. No organization or individual may reproduce or distribute this report in any form without prior written permission from our company. Any unauthorized commercial use of this report shall constitute a violation of the Copyright Law of the People's Republic of China, other relevant laws and regulations, and applicable international conventions.

Disclaimer

This research report is based on information that VCBeat considers reliable and currently publicly available. VCBeat strives to, but does not guarantee, the accuracy and completeness of such information. Due to limitations in research methodologies, sample sizes, and the scope of data collection, the data presented herein only reflects the basic conditions of the surveyed population during the survey period and serves solely for the current research purposes, providing a general reference for the market and clients. Furthermore, VCBeat does not guarantee that the views or statements contained in this report will remain unchanged. At different times, VCBeat may issue reports with information, opinions, and projections inconsistent with those contained in this report.

VCBeat does not consider recipients of this report as its clients by virtue of their receipt thereof. This report is distributed solely for informational purposes and only where permitted by applicable laws; it does not constitute any form of advertising. Under no circumstances shall the information contained herein or the opinions expressed be construed as investment advice to any person. Where permitted by law, VCBeat and its affiliated entities may hold equity interests in the companies mentioned in this report and may provide or seek to provide capital raising, financial advisory, or other related services to such companies.