Top Pharmaceutical E-commerce Company in 2016 Reports Revenue of RMB 1.33 Billion and Net Profit of RMB 88.6 Million

March and April mark the peak season for the disclosure of annual reports by listed companies, with a flurry of articles analyzing these reports being published. Investors and analysts, having accumulated questions about specific companies over the past year, look to these annual reports for answers. They sift through the subtle clues hidden in financial statements, attempting to gain a straightforward, data-driven understanding of a company’s operations.

For listed pharmaceutical companies with e-commerce operations, their annual reports reveal the extent of their achievements in this sector, ranging from “falling short of expectations” to “turning losses into profits.”

VCBeat (WeChat: vcbeat) collected and organized the annual reports of seven listed pharmaceutical companies, obtaining revenue data for their affiliated pharmaceutical e-commerce brands. It was found that the notion of pharmaceutical e-commerce “turning losses into profits” is a false premise, as all the pharmaceutical e-commerce platforms included in the statistics have already achieved basic profitability.

Let us first define the meaning of pharmaceutical e-commerce to avoid misinterpretation. Generally, pharmaceutical e-commerce refers to online pharmacies that sell drugs directly to individual consumers, primarily focusing on over-the-counter (OTC) medications, while also offering health supplements, disinfection products, household medical devices, and adult products. In a broader sense, pharmaceutical e-commerce also includes business-to-business (B2B) transactions of pharmaceuticals and medical devices conducted by manufacturers through third-party platforms or their own websites.

It is relatively unfair to compare consumer-facing (B2C) businesses with business-facing (B2B) businesses, as there are certain differences in their transaction categories and structures. B2B businesses can easily scale up volume but have lower profit margins; whereas B2C businesses, targeting the general consumer population, require extensive exposure and brand awareness, resulting in significant marketing investments.

The O2O (Online-to-Offline) model for pharmaceuticals has gained significant traction. At its core, this business model is fundamentally anchored in brick-and-mortar pharmacies, which serve as the essential infrastructure. It is worth noting that market entry strategies vary considerably among players. For instance, Alibaba Health established the “Pharmacy Pioneer Alliance,” where customer orders are placed via the Alibaba Health app, and drug delivery is handled independently by offline pharmacies. KuaiFang and Dingdang Kuaiyao primarily rely on offline pharmacies and currently operate only in Beijing. Haoyaoshi’s medication delivery service is an integral part of its online pharmacy platform and is also underpinned by physical stores. Recently, JD.com launched its “Health to Home” service, leveraging JD Bang to provide delivery support for partner pharmacies.

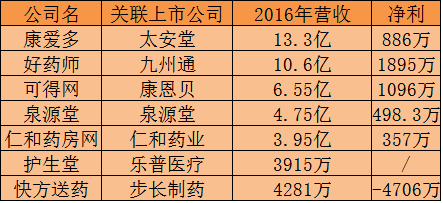

In terms of online pharmacies, most are backed by publicly listed companies. In addition to the few included in the statistics above, Baiyang Health Online Pharmacy, Jianyi.com, Tongrentang Online Pharmacy, Qilekang, and Sinopharm Online Pharmacy are all directly controlled by listed companies. Those not affiliated with listed companies include 111.com, Jianke, and Kaixinren. This is easily understood: before the State Council abolished the B and C licenses for pharmaceutical e-commerce, applicants for online pharmacy licenses were required to be brick-and-mortar pharmacies. This explains why Alibaba acquired Guangzhou Wunianfang Pharmacy and why JD.com acquired pharmacies in Qingdao to operate its own direct-sales business.

Data illustrating the competitive landscape of the pharmaceutical e-commerce market shows that prior to the cancellation of Class B and Class C licenses, there were 40 enterprises approved by the China Food and Drug Administration (CFDA) with Class A licenses (third-party platforms), nearly 200 with Class B licenses, and nearly 600 with Class C licenses. Both Class A and Class B licenses pertain to business-to-business (B2B) operations, while Class C licenses relate to business-to-consumer (B2C) operations. Following the removal of the approval requirement for the latter two categories, a short-term surge is inevitable. In the long run, however, growth must remain aligned with the core businesses of affiliated enterprises to prevent a chaotic rush into the market.

In terms of market size, although statistics from various sources differ, a general estimate places the total scale of pharmaceutical e-commerce at around RMB 100 billion, with continuous growth. Among this, the scale of online pharmacies has more precise data, reaching RMB 25.6 billion for the full year of 2016.

The target audience for B2C businesses is relatively clear, whereas that for B2B businesses is more diverse and hierarchical. This includes upstream e-commerce platforms for traditional Chinese medicine (TCM) decoction pieces; midstream industrial manufacturers to distributors; mid-to-downstream distributors to medical institutions and pharmacies; as well as direct distribution to medical institutions and pharmacies via platforms. Representative enterprises exist in each category, such as Zhongyaocai Tiandi for herbal material trading; self-built e-commerce websites by Jointown Pharmaceutical and Huadong Medicine; and third-party platforms like My Medicine, Drug Terminal, Yaodou.com, Yaoyaohao, and Maxconla.

The competitive edge in B2C business lies in supply chain and brand strength, including the timeliness and stability of the supply chain, bargaining power, and brand recognition among end users. In contrast, B2B business primarily relies on distribution channels. Since the existing distribution of pharmaceuticals and medical devices remains predominantly offline, individual distributors and agencies play a crucial role in penetrating products down to end-demanders. Disrupting this established workflow is challenging, as it would impinge upon the interests of multiple stakeholders, making market promotion difficult.

It is worth noting that, driven by policies such as the replacement of business tax with value-added tax (VAT) and the “two-invoice system,” B2B pharmaceutical e-commerce has garnered increasing attention from all stakeholders in the industry chain. For pharmaceutical manufacturers, this model enables compliant downstream distribution of products to end-user facilities, while platform-generated statistics provide clear insights into market demand, offering valuable guidance for production and sales strategies. For end-user medical institutions, B2B platforms enhance information transparency, and centralized, platform-based procurement strengthens bargaining power, thereby helping to reduce costs.

Returning to the issue of rankings in pharmaceutical e-commerce, B2B and C2C businesses should be categorized separately. Sales data for B2B operations are less frequently disclosed to the market. Huadong Medicine’s business platform reports figures exceeding RMB 10 billion (it includes data from centralized procurement platforms in its pharmaceutical e-commerce metrics). Other platforms, such as Yaodou.com, Yaoyaohao, and Putian Pharmaceutical & Medical Device Network, publicly report annual sales volumes exceeding RMB 1 billion.

In the B2C sector, in addition to data disclosed by listed companies, publicly available figures for 1YaoWang, Qilekang, and Jianke all exceed RMB 1 billion. Among them, Jianke reported RMB 1.5 billion in sales and projected that its 2017 sales would reach RMB 2.5 billion. Based on these various data sources, a general assessment of the ranking of online pharmacies in the market can be made.

Certainly, internet healthcare and mobile health platforms have recently been venturing into the pharmaceutical business. For instance, WeDoctor acquired Jinxiang.com and established the “Smart Pharmacy Alliance”; Chunyu Doctor has partnered with industrial enterprises; and DXY has long maintained a section dedicated to promoting pharmaceuticals and medical devices. Conversely, online pharmacies are also expanding into healthcare services. Examples include Qilekang launching an internet hospital in Yinchuan and Jianke introducing its “Jianke Doctors” platform.

“Healthcare + Pharmaceuticals” or “Pharmaceuticals + Healthcare” is inherently relative; diagnosis, treatment, and medication form a natural closed loop. This integration trend is expected to persist in the future, with business models becoming more deeply intertwined.

Judging from the broad perspective of pharmaceutical e-commerce, despite multiple existing constraints—such as the difficulty in disrupting the established B2B channel structure, restrictions on the online sale of prescription drugs in B2C operations, and challenges in integrating with medical insurance systems—the industry consensus is that the scale and prospects of pharmaceutical e-commerce are predictable. Consequently, various stakeholders are actively pursuing this market, and the development of pharmaceutical e-commerce may enter a new phase this year.