Health Insurance Emerges as the Next Growth Engine in Internet Insurance: Challenges and Opportunities for Innovative Insurtech Startups

By Lin Kai, Xipan Capital Research Report

As internet technology and applications permeate various sectors, including finance and consumer goods, a new wave of online consumers has emerged—primarily composed of the post-80s generation, characterized by higher education levels, higher incomes, and modernized insurance consumption concepts. This trend has spurred the proliferation of internet insurance startups around 2015, aiming to disrupt an insurance market known for its operational complexity, high entry barriers, and established monopolies. The health and medical insurance sector involves policy regulations, insurance giants, and social medical resources, presenting a complex commercial and social challenge. However, upon careful examination, clear classifications and developmental logic can be identified. Therefore, this report on “Internet Insurance + Health Insurance” will adopt the following perspectives:⻆——

Traditional B2C insurance is categorized into property insurance, life insurance, health insurance, and personal accident insurance, whereas the health insurance sector that this report aims to study actuallyIn practice, this refers to health insurance covering outpatient and inpatient expenses for diseases and health-related conditions that fall outside the scope of social security coverage.Property insurance, or all health insurance not covered by social security, thus life insurance and health (supplementary medical) insurance outside of property insurancea collective term for property insurance and personal accident insurance.

Innovative Insurance Models in the United States:

Mode I: The model of establishing an HMO (Health Maintenance Organization) system, integrating traditional insurance companies,Hospitals/clinics, patients, and a third-party independent system are interconnected to form a closed-loop healthcare system. Continuous cost control and improvement within the systemHigh-quality medical care and continuous improvement of members' health have minimized the transaction costs in the tripartite healthcare market. For example, Kaiser PermanenteTherapy (KAISER)

Kaiser Permanente’s Positioning and Characteristics: Low-Cost “Blue-Collar Insurance” and Higher-Quality Medical Services. Highly Informatized KaiserSaha Medical continuously collects and analyzes data to better optimize resource allocation, enabling robust quality monitoring and data-drivenrisk control capabilities.

Mode II: Insurance Claims Processing and Cost Control Management Model, by providing convenient, accurate, and fastFast, cost-controllable online insurance claims services that connect insurers, patients, and healthcare providers to establish a preferred networkPreferred Provider Organization (PPO) Network, e.g., Multiplan

Multiplan Positioning and Features: A provider of health cost-containment management solutions for healthcare payers and a builder of PPO networksPatient Acquisition for Healthcare Service Providers. Currently, it has 900,000 contracted healthcare providers and approximately 70 million users, leveraging its onlineThe network and solutions reduce the offline processing of 40 million medical reimbursement claims annually. Online processing of patients' medical health and utilizationDrug data further optimizes health insurance products for insurers, helping them better cope with unpredictable expenses and competitive pressures.

Model III: C-end Online Consultation Service Model. Through front-end free online inquiry, consultation, and price comparison services, back-endEstablishment of Exclusive Provider Organization (EPO) designated medical service providers within the network systemHealthcare service providers deliver services to users; unlike HMOs, users are not required to designate a fixed primary care physician or obtain referrals from one.Designated experts provide services, and the agreement covers all physicians at the designated service hospitals. For example: Oscar

Oscar’s Positioning and Features: On the front end, it provides free online query, consultation, and price comparison services to individual consumers, and simply...underwriting clauses to sell medical insurance plans, while contracting with backend providers of basic services for medical insurance; currently, there are more than 70 medical...hospitals and 40,000 healthcare providers.

Entry Models of Chinese Insurtech Startups:

Mode I:

Sales-driven: Companies that enter the market through agent platforms, brokerage sales, or online direct sales, such as Aofu Insurance, Datebao, Xiaoyusan Insurance, and Xiangrikui Insurance.

Product-Driven: Platforms offering comprehensive coverage of internet insurance products, such as ZhongAn Insurance; companies entering the market with innovative insurance products, such as H.S.O.’s chronic disease insurance for pre-existing conditions.

Service-Driven: Companies that enter the market through cost-control technologies, claims services, or customized insurance services, such as YiYong Health and Baoxian Geeker.

Mode II:

2B: Companies that customize employee health insurance for enterprises, such as Baoxian Geeker

2B2C: Companies that drive innovation in consumer-facing health insurance products and concentrate sales through offline insurance channels, such as Yi Yong Health.

2C: Innovation in consumer-facing health insurance products by companies utilizing online direct-to-consumer sales channels, such as ZhongAn Insurance and DaTeBao.

Differences in Market Entry Models for Insurance Innovation Between China and the United States:

The U.S. insurance model is trending toward a winner-takes-all landscape. While the entry points differ, the underlying architecture remains consistent: positioning insurers as payerscompanies, hospitals and health institutions as healthcare providers, and insured individuals;

China's insurance models are increasingly focusing on specific segments within the health insurance ecosystem, such as sales, product innovation, and services.in a monopolistic position. Moreover, China’s basic medical insurance still accounts for a significant proportion, and the public healthcare system operates independently of commercial insurance; therefore, forChina's insurance sector draws on the U.S. development logic, namely: whether a key entry point can be identified to form“Winner-Takes-All”The situation? StillIt is a problem.

Part 1 The Market Size of China's Health Insurance Industry — A Trillion-Yuan Market Is Just Around the Corner

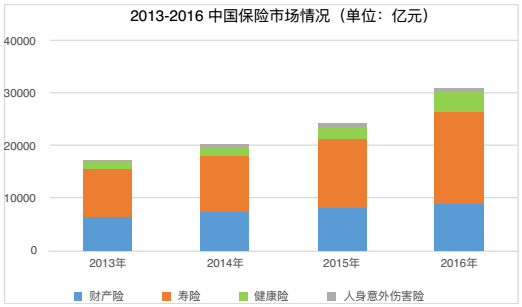

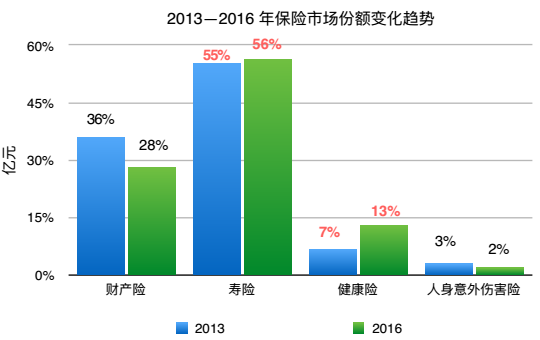

In 2014, the total size of the insurance industry exceeded RMB 2 trillion, and it easily surpassed RMB 3 trillion in 2016. The total premium volume continued to grow; however,Behind the overall development of the insurance market, the situation varies across different types of insurance. Among them, as the largest market for health insurance in ChinaThe growth rate of life insurance market share has remained strong in the past two years, while health insurance, represented by social security supplementary insurance, has shown a slightly higher growth rate.Other Insurance Types.

In 2016, the scale of China's health insurance market was: life insurance at RMB 1.6 trillion and health insurance at RMB 400 billion. These two categories constitute the primary sectors of the health industry.Insurance's share of the total market rose from 62% to nearly 70%.

In terms of premium volume, life insurance companies currently account for 70% of the health sector’s market share; even within the health insurance segment,“Life-insurance-style” health insurance products offered by life insurers still dominate the market. Indeed, among the early-stage health insurance investors we have engaged withAmong them, there is no shortage of voices making trend judgments: the pattern in which life insurance accounts for the vast majority of China’s health insurance market will persist.Consumer health insurance is also primarily offered in the form of supplemental coverage for large enterprises, with its market volume significantly smaller than that of life insurance (56:13).

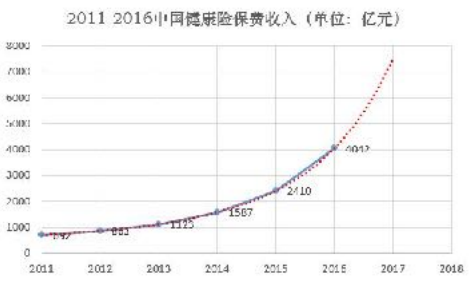

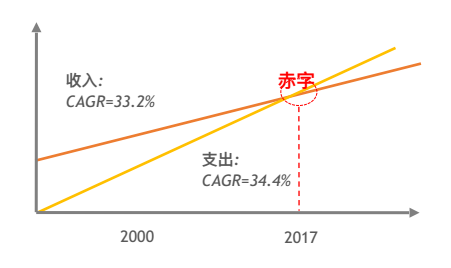

However, let us look separately at the premiums of domestic health insurance in China from 2010 to 2016, with revenue growing from RMB 69.172 billion toRMB 404.25 billion, a 4.8-fold increase, with its share of life insurance premium income rising from 6.37% to 18.2%, accounting for the entire industry’sThe proportion of fee income increased from 4.66% to 13%.

Over the next few years, consumer health insurance will become a trillion-yuan marketmarket. Meanwhile, the penetration rate of health insurance increased from 0.17% in 2010 to 0.54% in 2016; the density of health insurance in 2010RMB 50 per person increased to RMB 292.3 per person in 2016.

So, will the landscape dominated by life insurers in health-oriented insurance undergo significant changes in the coming years?

Behind the rapid development of consumer-oriented health insurance, there are three driving forces: economic growth, population aging, and the construction of the social security system.The issue is becoming increasingly severe, with the elderly population reaching an unprecedented scale. Consumer demand for health insurance is primarily driven by two factors:

Improving healthcare quality and reducing healthcare costs. The former is the core demand of the new generation of the middle class: they are health-conscious and possessA sense of crisis: inability to afford the high costs of premium private hospitals, coupled with dissatisfaction with the medical experience at most public hospitals.

The latter represents the core need of the elderly population: compared with younger individuals, they experience a higher frequency of illness and face a greater probability of severe disease, i.e.Even with social health insurance, medical expenses remain substantial. Therefore, the combined forces of two major trends—economic growth and population aging,This has driven Chinese consumers’ demand for health insurance to unprecedented levels.

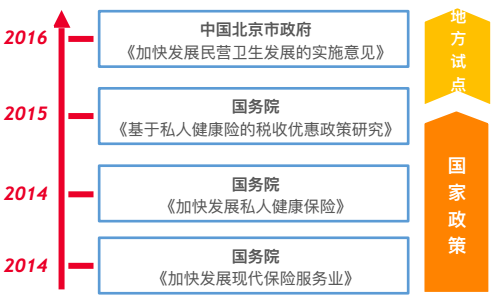

Addressing the deficit of the social security fund has become an urgent priority for the government to improve the social security system. Since 2014, the State Council and local governmentsSince [year], a series of preferential policies have been introduced to support the development of commercial health insurance, aiming to alleviate pressure on the social security fund by diverting demand at its source., and together with social insurance, form a multi-tiered social security system.

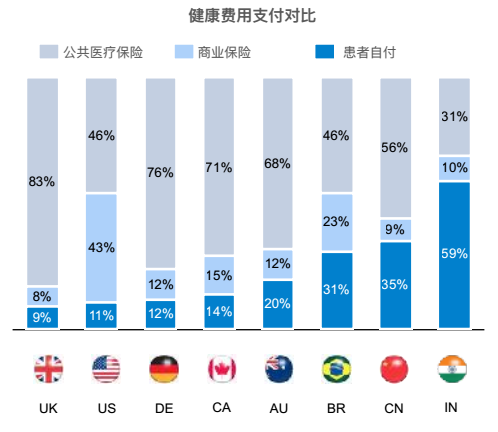

So, in comparison to the global proportions of public health insurance, commercial insurance, and out-of-pocket payments by patients, our current position and development trendsWhat should the trend be?

China and India have excessively high out-of-pocket payment ratios. As developing countries with huge populations, they should adopt the European model of high taxation and high welfare.The guarantee pathway appears unrealistic; relatively speaking, vigorously developing commercial insurance better aligns with China’s national conditions.

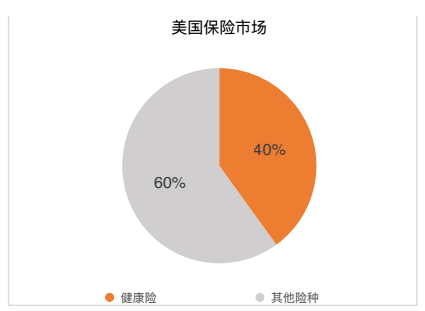

The proportion of commercial health insurance in the United States reaches 43%, yet its out-of-pocket payment ratio is nearly identical to that of European high-welfare countries. U.S. healthThe insurance market size has approached $1 trillion, more than 10 times that of China.

We believe that although China and the United States exhibit significant structural differences in areas such as the economy and healthcare, fundamentallyAnalysis: China’s healthcare demand is no less than that of the United States, and policy guidance clearly indicates that commercial insurance should assume a greaterresponsibility. In the future, as the economic gap between China and the United States narrows and their levels of physical therapy and health outcomes gradually converge, consumers’ insurance awareness andInsurance consumption habits are gradually converging, and the mature scale of China’s health insurance market has the potential to reach the current level of the United States, namelyTrillion-dollar scale.

Part 2 The Health Insurance Business Chain and Market Entrants

Investors and entrepreneurs’ attention to the integration of the Internet and insurance emerged in the context of the convergence of the Internet and finance (FinTech).after startups began to emerge as unicorns. On one hand, this is because the consumer side of the insurance market has reached a relatively mature stage since ancient timesThere is still a certain gap in the domestic private lending market, and on the other hand, insurance, as a niche segment of finance, inIt is also a gradual process to further develop fintech after its overall development trend has taken off.

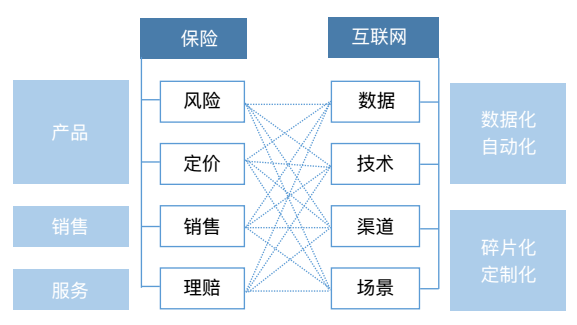

Integrating the four key components of traditional insurance operations—risk, pricing, sales, and claims settlement—with internet technology willWhat improvements in efficiency or fundamental disruptions have occurred?

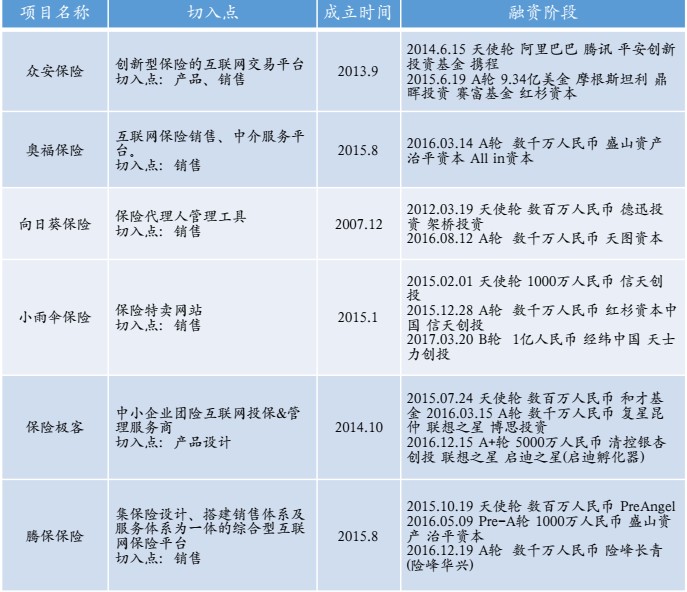

Currently, there are numerous players in the internet insurance sector with varying strategic approaches, yet their underlying motivations and entry points can all be summarized within this framework. TakingBelow is an overview of selected internet insurance startups that have secured their next round of financing:

The selection of the entry point determines whether it is possible to leverage the entire chain of complex health insurance business, and subsequently, each link in the chainThe choice of benchmarking against niche markets and operational models also determines the connectivity of the entire business logic, ultimately delivering lower costs to users....prices, higher-quality services, and insurance products with better health coverage.

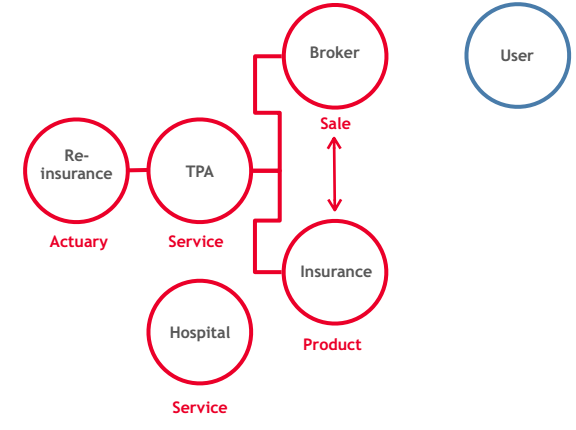

The key components of the health insurance business chain include: reinsurance companies (Reinsurance), insurance companies(Insurance), insurance agency and sales channels (Broker), third-party claims service companies (TPA), hospital(Hospital):

Closest to the end-user is the sales channel, which traditionally comprises direct sales by insurance companies and insurance brokers from insurance agencies.(Broker), practitioners of Internet-driven transformation such as Datebao and Xiaoyusan first established insurance sales platforms, offering low prices,Diverse product offerings and targeted internet traffic acquisition drive user purchases, thereby stimulating synergy across the entire value chain and strengthening competitive barriers.Lei. Among its star projects, “Da Te Bao” focuses on becoming China’s leading health insurance platform, renowned for offering high-cost-performance insurance products.It is reported that since its launch, the company has completed four rounds of financing, achieving a valuation of $200 million and accumulating 5 million registered users. By leveraging typical “Internet thinking,” it firstFirst, subsidize the sales of low-priced products and acquire traffic by burning cash; after achieving scale in user base, begin research and development of health insurance.R&D and service optimization, with a layout across the entire value chain.

The essential resource for entering the sales side is traffic. However, traffic is a resource that can only be leveraged by major players, except for those with exceptionally strong financing capabilities.In addition to Da Te Bao, there is another insurer—ZhongAn Insurance, founded by Ma Mingzhe, Chairman and CEO of Ping An Insurance, and AlibabaAn internet insurance platform jointly launched by Alibaba Group Chairman Jack Ma and Tencent Holdings Chairman and CEO Pony Ma, with its main businessIt collaborates with internet companies to provide insurance products in the automotive, healthcare, and online shopping sectors for young Chinese users.

PublicAnbao Insurance’s first round of financing amounted to RMB 9 billion, with a valuation of RMB 64 billion. The company achieved profitability in the second, third, and fourth quarters of 2016; however,Return shipping insurance accounts for over 70% of total insurance premium income. Innovative products like return shipping insurance feature low premiums and short coverage periods, making it difficult toresulting in a limited premium scale and thus constrained profit margins. "Zunxiang Yisheng," launched in August 2016, as a product covering medium-to-severe medical conditionshealth insurance products covering treatment risks set a daily sales record for a single internet health insurance product during that year’s “Double 11” shopping festival. Initially in con-Focus on indemnity-based health insurance.

When making insurance purchasing decisions, consumers prioritize the efficiency of claims settlement services over merely seeking high quality at low prices. By focusing on service, startups canThe company temporarily bypasses the “traffic-burning” model that it cannot afford in the early stages, and seeks to leverage data and internet technologies to build an absolute competitive moat.Key. Yi Yong Health, a company founded in 2014 that specializes in health insurance claims services, through IT coding and system researchenable fully automated, multi-layered logical claims adjustment and payout, delivering efficient and accurate claims services that significantly reduce labor and operational costs.Data, algorithms that accumulate and undergo continuous iteration can effectively control costs, further facilitating lean pricing for insurance products.

Yi Yong asA third-party claims administration (TPA) company that is not particularly high-profile in the industry, yet its insurance clients includeNearly all major health insurance brands, including PICC, ZhongAn Insurance, Li'an Life Insurance, China United Property Insurance, and Alltrust Insuranceand life insurance companies, cumulatively processing 1 billion invoices for 5 million insured individuals, achieving over 90% automated claims adjudication and 24-hour self-serviceClaims Services. In October 2016, Yi Yong Health secured risk underwriting from Swiss Re, leveraging its robust cost-containment capabilities.backing, it launched Yi Yong Changxiang Rensheng, a health insurance product featuring low premiums and high coverage, with a primary focus on populous regions such as Jiangsu and Chongqing.Densely populated major provinces, with a focus on penetrating Grade A hospitals (Nantong First People's Hospital and Chongqing Xinqiao Hospital) as key regions for provincial-level promotion.Provide insured individuals in the region with on-the-ground direct billing services for consumer health insurance. Proactively address the rigid demand of "poverty caused by illness" by applying commercial insurance principles.Required.

Part 3 Challenges Across All Links in the Health Insurance Value Chain

In summary, the chain can be understood as comprising three key links: products, services, and sales. So, internet insurance in these threeAre there any distinctive characteristics in this segment that differ significantly from other industries, necessitating consideration of its unique business logic aligned with the specific attributes of the insurance industry?

1. Product

The China Insurance Regulatory Commission regularly evaluates the solvency risk management of insurance companies; therefore, the pricing and riskControl is of paramount importance. As soon as any major insurance company launches a health insurance product targeting the same demographic with the samequasi-diseases, with no significant differences in risk assessment outcomes; therefore, the scope for product innovation and barriers to entry are actually not high. In factCurrently, insurance companies face severe homogenization in product design, making it difficult for their brand value to command a premium, ultimately leading to price competition.fierce battles; if issues arise with services and claims settlement, insurance companies also incur the notorious label of “scammers.” Internet insurance drives product innovationIt has added a glimmer of hope, but the inherent nature of insurance requires “risk control,” making it difficult for mutual insurance companies to sustain their operations by relying on “burning cash.” ByThus, the path to achieving truly “low-cost insurance” may lie in cost containment.

2. Services

Services include: claims settlement and medical services.

Traditional TPA companies have shouldered the critical responsibility of claims processing services for traditional insurers; however, these conventional TPA firms rely on labor-intensive operationsThe method of processing documents and settling claims is still adequate for handling claim services for life insurance, critical illness insurance, and corporate supplementary medical insurance, but it is also atAmid the dilemma of difficulty in expansion and a single profit model. The optimistic prospects for China's health insurance industry have made claims services crucial for rapid singleIntelligent systems for data processing and automated claims adjudication require automation and digitalization to cope with the future surge in health insuranceHigh volume, high-frequency claims.

How to Learn from the U.S. HMO Model (Kaiser Permanente) in China’s Relatively Closed and Independent Healthcare System, and Integrate MedicalIntegrating services (hospitals, clinics, and health institutions) into the overall commercial insurance system to create an insurance model centered on cost containment.+The closed-loop medical service system creates a high cost-performance experience for policyholders, representing another approach to achieving competitive advantage through service.

3. Sales

The most significant feature that distinguishes insurance products from other consumer goods is:

1) Preventing adverse selection:

The profit model of insurance is to proactively sell products to currently healthy individuals, and once the insured experiences health issuestopic, it enables leveraging small investments for significant returns, using lower premiums to address frequent or high-cost medical expenses. Therefore, preventing beingInsurers’ adverse selection must be inherently factored into insurance product design. Moreover, compared with critical illness insurance and life insurance, health insuranceRisks and property insurance involve complex claims clauses, numerous trigger conditions, a higher likelihood of adverse selection, and high difficulty in identification, posing challenges for controlFees have created potential enormous pressure.

2) Heavy after-sales claims service:

Compared to other insurance products such as critical illness insurance, life insurance, and property insurance, health insurance is characterized by a higher frequency of claims and a greater degree of product personalization.The claims clauses are complex, and insured individuals have high expectations for the speed of claims settlement services.

Consequently, this may lead to a situation where “the higher the sales volume, the more out of control cost containment becomes,” and “the higher the sales volume, the less able claims services are to keep up, resulting in faster system paralysis.”consequences. Whether sales methods without potential user control on the Internet have truly improved the efficiency of the insurance industry remains to be seenConsideration and Verification.

4. Cost Control

On the insurance value chain we have mapped, the vitality of an insurance product is determined not only by its affordability and quality that offer convenience to users, but also hinges onOngoing Risk Control Monitoring by Reinsurers. The booming health insurance market is a fact long taken for granted in the insurance industry, yetThe persistent obstacle preventing reinsurers and insurers from vigorously launching health insurance products is the difficulty in cost containment for health insurance. In addition to the annual averageThere is no better strategy than a 20% premium increase.

The difficulty in controlling costs outside the social security system is mainly because cost control needs to be based on a large amount of actual medical data (disease treatment, medicationmethods and costs), however, the closed nature of the healthcare system makes insurance companies (including government-managed medical insurance funds, which are not profit-oriented(for profit, lacking incentives for cost control) neither participates in upstream medical services nor engages in patient health management and care coordination,Information related to medical procedures remains siloed within hospitals of varying sizes. Health insurance faces difficulties in penetrating medical services and pharmaceutical distribution.the process, corresponding cost-control measures cannot be implemented.

Part 4 Opportunities in Health Insurance

Based on an analysis of the current pain points across the value chain, we believe that the opportunities in health insurance do not lie in the sales segment. The heavily entrenched challenges are difficult to overcome.The core of our service lies in claims processing and healthcare services. Throughout the service delivery process, it is essential to build a robust health and medical insurance framework.a closed-loop cost control system, while leveraging technological automation to rapidly process data and employing algorithmic logic to synthesize and iteratively refine data, thereby enablingSystematic Cost Control.

This may still be just a blueprint in China, but U.S. TPA companies have already expanded from digitizing claims processing services toNew Operational Model: TPA provides health management and medical network services to insured individuals, enabling data integration across healthcare andInsurance cost control, thereby reducing the loss ratio and moral hazards such as fraudulent claims. In the United States, Multiplan processes $40 million annuallyof claims reimbursement documents, the volume of data enables it to control the entire supply chain, while simultaneously providing health management services to users and insurance companiesProvide cost control services.

Currently, its network has partnered with 900,000 healthcare providers. In 2016, the five-year PE firmHellman & Friedman acquired from Starr Investment Holdings and Partners Group for $7.5 billionAfter exiting Multiplan, Starr’s President Maurice R. Greenberg, former Chairman of AIG, just two years earlier (2014billion) to acquire MultiPlan for $4.4 billion. It was a mysterious yet successful investment. MultiPlan’s success may have validatedFocusing on “services” is the optimal entry point for health insurance to achieve a “winner-takes-all” outcome.

Lin Kai, the author, is a founding partner at Xipan Capital, focusing on research-driven financial advisory in the early-stage TMT sector.

The author welcomes corrections and discussions: kay.lin@xipanfa.com