Cancer Immunotherapy: Global Giants Battle as Chinese Innovators Accelerate in the $46.5B PD-1/PD-L1 Arena

Immunotherapy is aA novel cancer therapy approach that enhances anti-tumor immunity within the tumor microenvironment by activating the patient’s own immune system, thereby controlling and eliminating tumor cells. This approach has gained industry recognition in recent years.Among themPD-1/PD-L1is a popular target for immunotherapy. Since Bristol-Myers Squibb launched the firstPD-1DrugOpdivoSince then, major pharmaceutical companies have joined the immunotherapy race. Merck & Co.’sKeytruda, Roche'sPD-L1InhibitorTecentriqSuccessively ObtainedFDAApproved, and the Chinese pharmaceutical community has even more soPD-1/PD-L1Full of anticipation.

What Are PD-1 and PD-L1 Drugs?

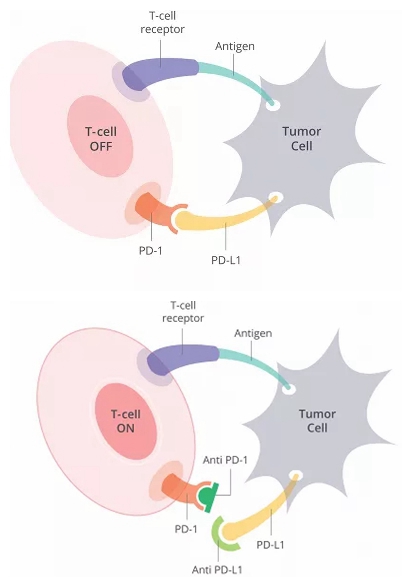

PD-1, or programmed death 1, also known as programmed cell death protein 1, is a crucial immunosuppressive molecule initially cloned from apoptotic mouse T-cell hybridoma 2B4.11. Immunomodulation targeting PD-1 holds significant importance for anti-tumor and anti-infective therapies, the treatment of autoimmune diseases, and improving survival rates in organ transplantation. PD-L1 is the ligand for PD-1 and can also serve as a therapeutic target; corresponding antibodies can exert similar effects.

T cells are a crucial component of the human immune system, capable of identifying and eliminating tumor cells. However, tumor cells are highly cunning and employ various mechanisms to evade recognition and attack by the host immune system, thereby enabling their survival and proliferation within the body. With advancing understanding of the tumor immune microenvironment, it has become evident that immune evasion by tumor cells is a significant driver of tumor progression. The PD-1/PD-L1 signaling pathway, identified in recent years as a negative immune co-stimulatory axis, plays a pivotal role in tumor immune evasion.

Mechanism of Action of PD-1/PD-L1 Inhibitors

When the PD-1 receptor binds to its ligand, PD-L1, it causes T cells to cease functioning. In other words, blocking this interaction allows T cells to function normally. PD-1/PD-L1 inhibitors are a class of drugs that prevent this binding, thereby reactivating human T cell function. Such medications have ushered in a new era in cancer treatment.

Foreign Landscape: A Fragmented Market

In July 2014, Bristol-Myers Squibb’s PD-1 inhibitor Opdivo (nivolumab) was approved in Japan, becoming the first PD-1 inhibitor approved globally. Shortly thereafter, Merck’s PD-1 drug Keytruda (pembrolizumab) received FDA approval, becoming the first PD-1 inhibitor approved in the United States.

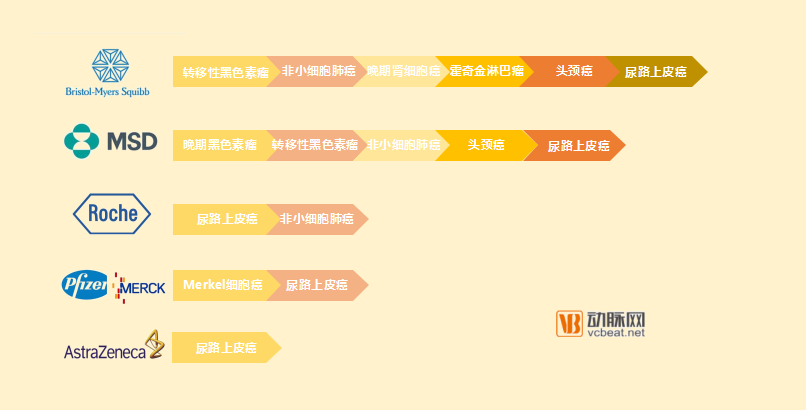

On one front, Bristol Myers Squibb and Merck & Co. hold a slight lead; on the other, Roche is in hot pursuit. As industry giants including Bristol Myers Squibb, Merck & Co., Merck KGaA, Pfizer, Roche, and AstraZeneca have successively secured market entry approvals, the already turbulent PD-1/PD-L1 battlefield has grown increasingly tense, with a showdown for supremacy poised to erupt at any moment.

The Tripartite Standoff: A Battle for Supremacy

In February 2017, Bristol-Myers Squibb announced that its PD-1 inhibitor, Opdivo, had received FDA approval for the treatment of bladder cancer. This marked the sixth major indication approved for Opdivo, following melanoma, non-small cell lung cancer, renal cell carcinoma, classical Hodgkin lymphoma, and head and neck cancer. For Bristol-Myers Squibb, which had previously faced a string of misfortunes, this was indeed a welcome breakthrough.

In August 2016, Bristol-Myers Squibb suffered a rare setback, announcing the failure of the Phase III clinical trial of Opdivo as first-line treatment for lung cancer. Subsequently, the company’s stock price plummeted.19%。

The failure of first-line lung cancer trials also set the stage for a showdown between Opdivo and Keytruda. Just one month later, Roche’s Genentech released Phase III clinical data for Tecentriq, its PD-L1 immunotherapy, in patients with previously untreated non-small cell lung cancer (NSCLC). In October, Merck & Co.’s competing drug, Keytruda, made history by receiving FDA approval as a first-line treatment for NSCLC. Thus, these companies intensified their competition in the lung cancer immunotherapy market.

Although Opdivo had previously captured more than 80% of the PD-1 market in the United States and other major markets, the failure of clinical trials has allowed competitors to achieve successive breakthroughs, undoubtedly challenging Bristol-Myers Squibb’s leadership position.

As early as 2014, Bristol-Myers Squibb and Merck & Co. became embroiled in a dispute. In September 2014, the FDA granted accelerated approval to Merck’s Keytruda. Shortly after Merck received FDA approval, Bristol-Myers Squibb filed a lawsuit against it in federal court.Bristol-Myers Squibb and its Japanese partner, Ono Pharmaceutical, stated that Merck & Co. infringed on the patents for Opdivo, a PD-1 inhibitor jointly marketed in Japan.

Bristol-Myers Squibb is no pushover. After setbacks in the lung cancer market, the company has taken a two-pronged approach: tying up competitors in patent litigation while pivoting to other oncology indications. Opdivo remains its crown jewel. According to Bristol-Myers Squibb’s 2016 annual report, the company’s total annual revenue exceeded $19.4 billion, a 17% increase from 2015, with Opdivo making a significant contribution. Naturally, Bristol-Myers Squibb would not stand idly by as competitors gradually encroached on its market share. As early as June 2016, given the promising clinical data for the PD-1 antibody Opdivo in bladder cancer, the U.S. Food and Drug Administration (FDA) granted Opdivo Breakthrough Therapy Designation for this indication. The FDA approval secured this February indeed allowed the company to flex its muscles against rivals.

Furthermore, numerous Phase III clinical trials of Opdivo are currently underway, with the potential for continued expansion of its indicated indications. These Phase III studies primarily involve evaluating the efficacy and safety of Opdivo in treating a variety of tumors, including melanoma with brain metastases, gastric cancer, bladder cancer or upper urinary tract urothelial carcinoma, esophageal cancer or gastroesophageal junction cancer, hepatocellular carcinoma, and malignant glioma.

While the competition here is heating up, Roche has not been idle.In April 2017, two months after Bristol-Myers Squibb’s Opdivo received FDA approval for the treatment of bladder cancer, Roche announced that Tecentriq had also gained accelerated FDA approval for bladder cancer treatment. This marked the third FDA approval for Tecentriq in the U.S. market in less than a year.

Tecentriq is the first PD-L1 antibody drug approved by the FDA for market launch. In May 2016, it received accelerated approval from the FDA for the treatment of common types of bladder cancer (UC)—a full four months ahead of schedule. The drug is primarily indicated for locally advanced or metastatic urothelial carcinoma and metastatic non-small cell lung cancer.,Roche also has high hopes for Tecentriq, aiming to use it to shrink Opdivo’s market share.Roche is currently evaluating the efficacy of its treatments in ovarian cancer, renal cell carcinoma, triple-negative breast cancer, bladder cancer, melanoma, colorectal cancer, and other indications.

On May 10, 2017, Roche updated the results of a Phase III study evaluating Tecentriq (atezolizumab), a PD-L1 monoclonal antibody, as a second-line treatment for patients with advanced bladder cancer. Surprisingly, the study, codenamed IMvigor211, failed to meet its primary endpoint. The safety profile of Tecentriq in this trial was consistent with previous findings. This outcome may precipitate a crisis for Roche’s PD-L1 franchise.

Turning to Merck & Co., as previously mentioned, Bristol-Myers Squibb filed a lawsuit against Merck in federal court. This legal battle, also known as the global patent war between the blockbuster PD-1 inhibitors Opdivo and Keytruda, lasted from 2014 to 2017.

Between 2014 and 2015, Bristol-Myers Squibb successively filed three complaints with the U.S. District Court for the District of Delaware, alleging that Merck & Co. infringed three separate patents. Because the parties involved in all three cases were identical and the factual backgrounds largely overlapped, Judge Stark of the District Court had originally scheduled an eight-day trial before a single jury for April 3, 2017, to hear all three cases together.

Yet just three days after jointly submitting a pre-elevation resolution drafted by both parties to the court, the two sides unexpectedly reached a settlement. Merck & Co. and its rival shook hands on the PD-1 dispute, but Bristol Myers Squibb secured the PD-1 patent and will receive billions of dollars in annual patent licensing fees from Merck.

Despite suffering a minor setback in the patent dispute, Merck & Co. found consolation elsewhere. Following the approval of Keytruda as a first-line treatment for non-small cell lung cancer (NSCLC), Merck submitted an application in January 2017 for Keytruda in combination with chemotherapy as a first-line therapy for lung cancer. Bristol-Myers Squibb, which favors combination drug development, chose to withdraw its application for accelerated approval of the Opdivo and Yervoy combination for first-line lung cancer treatment after analyzing existing clinical data. As a result, Merck not only gained an opportunity to advance in the competitive landscape but also further solidified its position in the first-line lung cancer market.

On May 10, 2017, Merck & Co. announced the accelerated approval of Keytruda combination therapyFirst-line treatment for metastatic non-squamous non-small cell lung cancer (NSCLC). Previously, Keytruda was the only approved PD-1/PD-L1 inhibitor for first-line treatment of NSCLC. From a market perspective, Keytruda has established an overwhelming advantage in the lung cancer field, far surpassing other PD-1/PD-L1 inhibitors rather than merely leading by a narrow margin.

Nine days later, Merck’s Keytruda received accelerated approval from the FDA again, expanding its indication to first-line treatment for locally advanced or metastatic urothelial carcinoma.

Yet this pales in comparison to the news that followed. On May 24, 2017, the FDA delivered another major announcement: it granted accelerated approval to Merck’s Keytruda as the first anticancer therapy agnostic to tumor origin.This marks a milestone as the first antitumor therapy approved by the U.S. FDA that is differentiated based on biomarkers rather than tumor origin.

Bristol-Myers Squibb’s FDA approval of Opdivo for bladder cancer treatment had barely settled when Merck & Co. launched a relentless offensive. Keytruda has already surpassed Opdivo in the lung cancer segment and is now gradually overtaking Roche in the bladder cancer space. Coupled with its established dominance in melanoma, Keytruda has become the first therapy approved for treating cancers regardless of tumor origin. With this formidable momentum, Merck & Co. is steadily advancing toward the throne of market leadership.

A large wave of clinical studies on Keytruda for the treatment of other types of cancer is currently underway, including Hodgkin's lymphoma, advanced liver cancer, advanced gastric cancer or gastroesophageal junction cancer, and triple-negative breast cancer.

Newcomers to the Battlefield: Pfizer, Merck, and AstraZeneca

Beyond the “Big Three,” other competitors are also striving to catch up. In April 2017, avelumab, a PD-L1 antibody jointly developed by Pfizer and Merck, received FDA approval for marketing. The antibody was approved for the treatment of a rare skin cancer—Merkel cell carcinoma (MCC). This marks the first PD-L1 therapy approved for MCC.

However, the prospects for avelumab are not particularly bright if it is targeted solely at the treatment of Merkel cell carcinoma (MCC). Merck’s Keytruda is also expanding into this indication, and given that MCC is a rare cancer, its market size is inherently small. As the fourth PD-1/PD-L1 inhibitor to reach the market, avelumab may struggle to compete effectively against its rivals.

Pfizer and Merck are undoubtedly well aware of this, and both companies are seeking breakthroughs for avelumab in other indications. Just this May, the FDA approved avelumab for the treatment of patients with advanced or metastatic urothelial carcinoma (UC).

The two companies had already registered and initiated the Phase III JAVELIN Lung 100 study of avelumab for non-small cell lung cancer as early as October 2015.

However, according to information on ClinicalTrials.gov, Pfizer/Merck expanded the planned number of patients to be enrolled from 420 to 1,095 in March, and the trial is not expected to complete data collection until April 2019.Clinical data on the primary endpoint. This timeline has been delayed by two years compared to the previous schedule. Pfizer and Merck’s recent protocol amendments are aimed at securing more compelling and competitive clinical data; however, this strategy carries risks—namely, whether competitors will launch superior products during this period. It remains highly uncertain whether Pfizer and Merck can outpace both time and their rivals.

In May 2017, AstraZeneca’s PD-L1 antibody drug, Imfinzi, received FDA approval for the treatment of locally advanced or metastatic urothelial carcinoma. It was the third approved PD-L1 inhibitor for the treatment of advanced or metastatic urothelial carcinoma.

Furthermore, clinical trials evaluating Imfinzi as a first-line monotherapy and combination therapy for urothelial carcinoma are ongoing, while research and discussions on its application in lung cancer, head and neck cancer, liver cancer, and hematologic malignancies are also underway.

BMS, Merck & Co., and Roche form a tripartite dominance, while Pfizer & Merck KGaA and AstraZeneca are also catching up.

Domestic Market: Undercurrents Stirring, the Last Calm Before the Storm

Compared with overseas markets, the domestic market appears much calmer. Yet everyone knows that a storm is brewing beneath this tranquility.

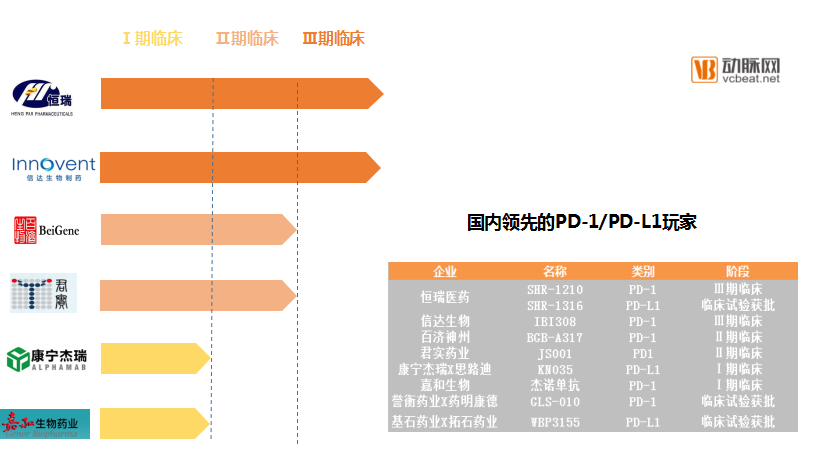

The domestic PD-1/PD-L1 market can be described in one phrase: beyond imagination. According to data from PharmaCube, there are six developers of PD-1/PD-L1 inhibitors that have entered clinical trials in China.

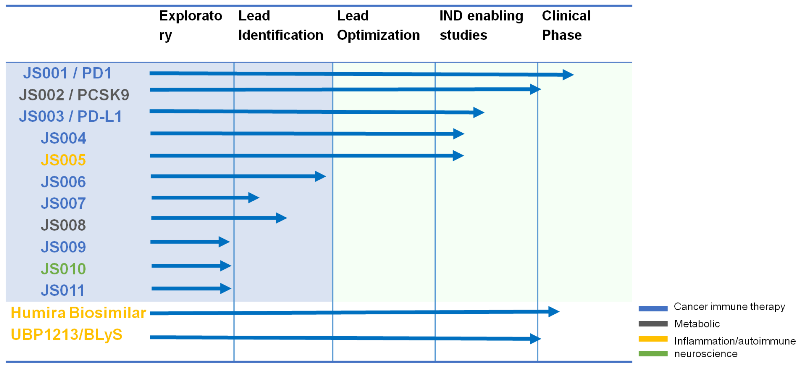

Junshi Biosciences was among the first domestic companies to obtain clinical trial approval for a PD-1 inhibitor. In December 2015, Junshi Biosciences’ recombinant humanized anti-PD-1 monoclonal antibody injection (JS001) received clinical trial approval from the China Food and Drug Administration (CFDA) and has currently entered Phase II clinical trials. In addition to PD-1, Junshi Biosciences has also pursued a dual strategy targeting PD-L1. Its PD-L1 candidate, JS003, is currently in the preclinical IND-enabling studies phase, prior to filing an investigational new drug (IND) application.

Image from the official website of Junshi Biosciences

Hengrui Medicine has since taken the lead, announcing in April this year the trial registration for its Phase III clinical study of “SHR-1210, a PD-1 monoclonal antibody, in combination with chemotherapy as first-line treatment for patients with advanced non-small cell lung cancer.” This marks SHR-1210 as the first PD-1 monoclonal antibody in China to enter Phase III clinical trials. Additionally, its PD-L1 inhibitor, SHR-1316, has already received approval for clinical development.

As it stands, Hengrui Medicine is indeed the leader among domestic developers of PD-1/PD-L1 inhibitors.

Notably, as early as September 2015, Hengrui Medicine sold the overseas rights to SHR-1210 to U.S.-based Incyte Corporation for an upfront payment of $25 million (with a potential total value of up to $770 million). This marked the first time a Chinese enterprise had transferred the rights to an innovative biopharmaceutical product.

BeiGene is also a leader in the domestic PD-1 field. Currently, its PD-1 monoclonal antibody, BGB-A317, has entered Phase II clinical trials for Hodgkin lymphoma. BGB-A317 can be used in combination therapy for patients with B-cell lymphoma and has received clinical trial approvals in Australia, New Zealand, and the United States. To date, more than 200 patients have been enrolled in overseas clinical trials covering 26 different tumor types.

Like the previous two, BeiGene has also chosen to develop PD-L1 drugs, and this antibody drug is currently in the clinical candidate stage.

On the occasion of its fifth anniversary in September 2016, Innovent Biologics received a significant gift from the China Food and Drug Administration (CFDA)—the clinical trial approval for its PD-1 inhibitor, IBI308. Preclinical data indicated that IBI308 exhibited superior efficacy compared to existing marketed anti-PD-1 therapies. This high-potential asset successfully attracted the attention of Eli Lilly and Company, which incorporated Innovent’s PD-1 monoclonal antibody into all three antibody development agreements reached between the two companies. Notably, Eli Lilly even suspended its own internally developed PD-1 program. In this regard, Innovent may well be Hengrui Medicine’s most formidable competitor.

On May 18, 2017, Innovent Biologics announced on the National Clinical Trial Registration Platform the initiation of a Phase III clinical study of its PD-1 monoclonal antibody IBI308 as second-line treatment for advanced or metastatic squamous non-small cell lung cancer. This made Innovent the second domestic pharmaceutical company to enter Phase III clinical trials for PD-1/PD-L1 inhibitors, following Hengrui Medicine. Additionally, Phase II trials of IBI308 for esophageal cancer and Hodgkin lymphoma are ongoing.

In late November 2016, Alphamab Oncology and 3D Medicines announced that KN035, a recombinant humanized PD-L1 single-domain antibody, had passed the U.S. FDA review and received approval to commence clinical trials. Reportedly, this marks the first antibody-based innovative drug independently developed by a Chinese enterprise to enter clinical trials in the United States.

One month later, Jiahua Bio, a subsidiary controlled by Yunnan Walvax Biotechnology, also successfully entered the PD-1 clinical trial pipeline. Genolimzumab injection is the first PD-1 monoclonal antibody drug approved for Jiahua Bio, with major potential indications including various hematologic malignancies, melanoma, non-small cell lung cancer, renal cell carcinoma, and multiple solid tumors.

In addition, WBP3155, a PD-L1 inhibitor jointly developed by CStone Pharmaceuticals and TopAlliance Biosciences, and GLS-010, a PD-1 inhibitor developed through the collaboration between WuXi AppTec and Hybio Pharmaceutical, have both received approval for clinical trials and will commence these studies in due course. Clinical trial applications have been submitted for the recombinant humanized anti-PD-1 monoclonal antibodies from Akeso Biopharma, HanZhong Biologics, and HanSi Biologics, as well as for Bio-Thera Solutions’ candidate; Kelun Pharmaceutical’s PD-L1 inhibitor, KL-A167, has also filed for clinical trial approval. Oriental Biotech and Anke Biotechnology are intensifying their preclinical research efforts.

Progress of Clinical Trials in China and Leading Players

Challenges for Domestic Enterprises

Currently, the earliest PD-1 drugs developed in China have entered Phase III clinical trials. Against the backdrop of strong policy support for innovative drug development, it is expected that products will reach the market within as little as two to three years. In 2015, the National Health and Family Planning Commission’s Major New Drug Development Special Project designated PD-1/PD-L1 as a key therapeutic target and established expedited review pathways (“green channels”) for multiple new drug research and development programs. In this favorable environment, more players are entering the field, and an increasing number of drugs are progressing into clinical trials and eventually reaching the market.

Despite an unprecedented environment for innovation, these companies also face challenges. Once drugs enter the market, their primary challenge is competition from foreign pharmaceutical giants. The Chengmei International Medical Center of Hainan Cancer Hospital is the first medical institution in mainland China to offer imported PD-1 inhibitors. Furthermore, according to data from the China Food and Drug Administration (CFDA), both Bristol-Myers Squibb and Merck & Co. have obtained regulatory approval. Foreign products have already entered the Chinese market at a time when no comparable domestic products had yet been launched.

However, domestic companies are not without advantages. In their clinical trials, data from Chinese patients account for a significant proportion, meaning these products are better tailored to the Chinese market. More importantly, domestically produced drugs hold a price advantage. According to a report by CICC, the peak market size for PD-1 inhibitors in China is projected to reach $62.5 billion, with the ratio of patients choosing domestically produced PD-1 inhibitors versus imported ones being approximately 8:2. The price of domestically produced PD-1 inhibitors is about one-third that of imported drugs, allowing them to capture a market share worth approximately RMB 35.2 billion.

Another challenge lies in how Chinese enterprises can expand overseas while ensuring stable and sustainable growth. If R&D is conducted in accordance with international standards, it is inevitable that products will enter the global market upon launch. For domestic companies, expanding their influence internationally is, in essence, also a way to enhance their influence within China.

However, the issue lies in the fact that foreign giants have already established a strong market presence for many years compared to domestic companies, with each vying for market share. According to data from CICC, the global PD-1 market is projected to reach $35.8 billion by 2025, while the PD-L1 market is expected to be approximately $10.7 billion.

According to EvaluatePharma’s analysis, Opdivo’s sales are projected to reach $8.8 billion by 2020, while Keytruda’s sales are expected to hit $5.5 billion. If we conservatively extrapolate these 2020 sales figures to 2025, these two products alone would account for 40% of the global market.

Other major players include Merck, Roche, AstraZeneca, and Pfizer. In July 2015, Sanofi also invested $2.17 billion in Regeneron to develop the PD-1 inhibitor REGN2810. Reportedly, REGN2810 has entered the clinical trial stage. Eli Lilly and Amgen are also actively strategizing their positions. Beyond these industry giants,More than400A project in the clinical trial phase.

Random order, no priority implied

If global players seek to further expand this market, they will face common challenges. First, immunotherapy itself has limitations, namely a low response rate. This alone causes a significant proportion of patients to miss out on PD-1/PD-L1 inhibitors. Furthermore, the persistently high prices of PD-1/PD-L1 drugs deter another segment of patients.

According to Hainan Cancer Hospital, the preliminary price for the 50 mg specification of Keytruda exceeds RMB 20,000. In the Hong Kong and Macau regions, the price for 100 mg of Opdivo is approximately RMB 21,000 (with a dosage of 3 mg/kg administered every two weeks); the price for Keytruda at an equivalent dose is approximately RMB 38,000 (with a dosage of 2 mg/kg administered every three weeks).

However, from another perspective, it seems overly harsh to compare foreign giants with domestic enterprises. It is truly remarkable that these young companies have managed to catch up with world-class giants in just a few years. It is difficult to predict the full extent of their explosive growth potential in the future.But one thing is certain:In the future, opportunities and challenges will coexist.