Prescription Diversion Trend Analysis: Projected Market Scale to Reach RMB 800 Billion by 2020

Recently, the State Council’s Office of Healthcare Reform released the “Key Tasks for Deepening the Healthcare System Reform in 2017,” once again bringing the issue of prescription outflow to the forefront. Building on last year’s policy that hospitals should not restrict prescription outflow, this year’s efforts will focus primarily on the retail pharmacy sector.

The Office of Healthcare Reform has proposed that the Ministry of Commerce, the Ministry of Human Resources and Social Security, the National Health and Family Planning Commission, the China Food and Drug Administration, and other pharmaceutical regulatory authorities collaborate to explore tiered management of retail pharmacies nationwide, encourage the development of chain pharmacies, and promote the interconnectivity and real-time sharing of prescription information from medical institutions, medical insurance settlement data, and retail drug consumption records.

This signifies that the previously existing issues with prescription outflow—namely, misaligned health insurance integration, settlement difficulties, and the inability of retail pharmacies to accommodate the outflow market—have gained significant attention. Consequently, facilitating the external circulation of prescriptions will be a key focus of this year’s healthcare reform initiatives. Therefore, VCBeat (WeChat ID: vcbeat) has drafted a preliminary report on prescription outflow trends to provide a brief discussion on the issue of external prescription circulation.

I. The Outflow of Prescriptions from Hospitals Is an Inevitable Trend

1. The Broader Context of Separating Medical Services from Pharmaceutical Sales

Since the launch of healthcare reform, "separating medical services from pharmaceutical sales" has been a key component. The underlying reason is that a significant portion of the revenue for public medical institutions and their staff in China comes from pharmaceuticals. Using drug revenues to subsidize medical care has led to opaque funding sources and distribution mechanisms, as well as inadequate regulatory oversight, thereby fostering issues such as pharmaceutical bribery, overprescribing, and high medical expenditures.

“The separation of pharmaceuticals from healthcare” aims to exclude drug revenue from the income of medical institutions, sever direct financial ties among drug bidding and procurement processes, medical institutions, healthcare professionals, pharmaceutical manufacturers, and drug distributors, and establish a mechanism in which clinical diagnosis and treatment operate independently from medication prescription.

In terms of policy, the origins can be traced back to the “Guiding Opinions on the Reform of the Urban Medical and Health System” issued by the State Council’s Office for Medical Reform in 2000. This document first stipulated that pharmaceuticals should be subject to “separate accounting, distinct management, unified remittance, and reasonable refund.” This meant maintaining two separate sets of accounts within hospitals: drug revenues were to be accounted for separately under the new financial and accounting system. Meanwhile, the surplus from drug revenues and expenditures was to be remitted to health administrative departments, deposited into a special fiscal account for social security funds, and then reasonably refunded to medical institutions after assessment and coordinated allocation.

However, the “separation of prescribing from dispensing” has encountered numerous challenges in practical implementation. The most immediate issue is that, after drug revenue is decoupled from healthcare institutions, the compensation received by medical personnel no longer aligns with their workload and professional efforts, due to the absence of an adequate benefit-compensation mechanism. In this context, the “separation of prescribing from dispensing” has become linked with efforts to improve the remuneration of healthcare professionals, gradually leading to the exploration of supplementary measures such as raising consultation and treatment fees and establishing pharmaceutical care service fees.

The “Beijing Healthcare Reform,” implemented in April this year, represents a relatively comprehensive attempt at the operational level to separate pharmaceutical sales from medical services. According to the “Implementation Plan for the Comprehensive Reform of Separating Pharmaceuticals from Medical Services” issued by the Beijing Municipal Government, its primary objective is to transform the operational mechanisms of public medical institutions by eliminating drug markups and establishing medical service fees, thereby standardizing medical practices.

In terms of specific implementation, Beijing’s healthcare reform has reduced the prices and costs of pharmaceuticals, medical devices, and consumables through measures such as transparent procurement of medical products and health insurance cost containment. Furthermore, Beijing’s healthcare reform has established a dynamic price adjustment mechanism. This mechanism dynamically adjusts the prices of pharmaceuticals, medical devices, consumables, and medical service fees by monitoring changes in the operational costs and revenue structures of public medical institutions. This approach ensures that the overall cost burden for patients seeking medical care and purchasing medications does not increase significantly, while clearly recognizing the professional value of healthcare workers’ labor.

Overall, the policy of “separating pharmaceuticals from medical services” works in synergy with measures such as controlling the drug revenue share, abolishing drug markups, and implementing health insurance cost containment in public healthcare institutions. These combined efforts transform drugs from a source of revenue into a cost item in the operation of public healthcare institutions, thereby compelling them to advance the reform of separating pharmaceuticals from medical services.

2. Policies Related to the Outflow of Prescriptions

During the implementation of the comprehensive reform to “separate pharmaceuticals from medical services,” a key focus has been the outflow of prescriptions or their circulation outside hospitals. This means that drug supply and pharmaceutical care services, previously shouldered by hospital pharmacies, are gradually being shifted to other drug distribution channels—primarily retail pharmacies—to ensure patients’ medication needs are met.

Regarding specific policies, regulators’ stance on the outflow of prescriptions has become increasingly clear. This evolved from the 2014 exploration of a “new model allowing patients to independently purchase medications at medical institutions or retail pharmacies with prescriptions,” which encouraged patients; to the 2015 mandate that “hospitals are prohibited from restricting prescription outflow,” which pushed hospitals to comply; and most recently, to the 2017 healthcare reform task of “exploring the interconnectivity and real-time sharing of prescription information from medical institutions, health insurance settlement data, and drug retail consumption information,” aiming to systematically remove barriers to the circulation of prescriptions outside hospitals.

Overview of Policies on “Prescription Outflow”

The progressive nature of these policies also reveals that regulators aim to achieve the separation of prescribing and dispensing by facilitating the outflow of prescriptions. The first step is to mobilize patient initiative and remove barriers to prescription outflow, thereby empowering patients to decide independently where to purchase their medications. The second step involves enhancing patients’ medication-purchasing experience at community pharmacies or through other channels by integrating medical insurance systems and enabling interoperability of prescription information, thus creating a substantive “diversion” away from hospital pharmacies.

II. How Does Prescription Outflow Impact the Industry?

1. Transformation of the Pharmaceutical Distribution Structure

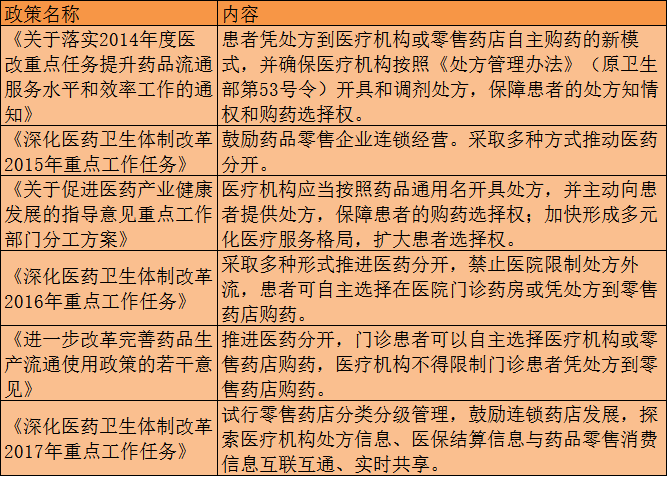

Following the outflow of prescriptions, the most visible change has occurred in pharmaceutical retail channels. Drug sales, previously dominated by in-hospital channels, are gradually shifting toward social pharmacies and online pharmacies. Two sets of relevant data illustrate this trend.

First, regarding the overall size of the pharmaceutical retail market, according to data from China Business Industry Research Institute, the domestic terminal sales volume of pharmaceuticals reached RMB 1.38 trillion in 2015. From the perspective of the three major terminals, public hospitals (the first terminal) accounted for 69%, retail pharmacies (the second terminal) accounted for 22%, and public primary healthcare institutions (the third terminal) accounted for 9%, reflecting an overall ratio of approximately 7:2:1.

Pharmaceutical Retail Market Data

In terms of the prescription drug market, IMS data shows that in 2015, China's prescription drug market size was approximately RMB 990 billion, accounting for about 70% of the total pharmaceutical market. Regarding specific channels, since prescription drug sales must rely on prescriptions and medical advice issued by doctors, the proportion of in-hospital sales is higher compared to the overall pharmaceutical market. According to IMS, the shares of the three major channels (hospitals, retail pharmacies, and third-tier terminals) in the 2015 prescription drug market were 77%, 10%, and 13%, respectively.

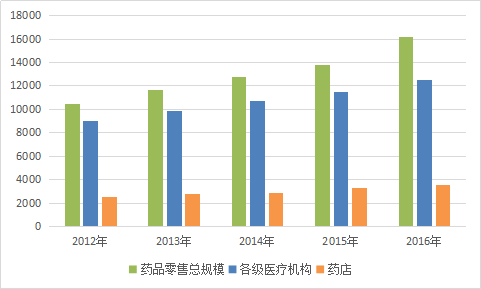

Based on industry estimates regarding the volume of prescriptions that can be diverted outside hospitals during the separation of prescribing and dispensing, it is broadly projected that over the next five years, outflowed prescriptions will account for approximately one-fifth of total prescriptions, with rapid growth expected. Considering the overall expansion of the pharmaceutical retail market, prescription outflows are anticipated to generate incremental revenue exceeding RMB 250 billion for retail pharmacies by 2018. By 2020, out-of-hospital prescription purchases are expected to reach one-third of total prescriptions issued, with the market size approaching RMB 800 billion.

Prescription Outflow Market Forecast

2. What is the impact of prescription outflow on the upstream and downstream segments of the industry chain?

It is important to note that the change in market size resulting from the outflow of prescriptions does not represent “incremental growth,” but rather a restructuring of the existing pharmaceutical distribution landscape. Such restructuring inevitably leads to a reallocation of interests among industry stakeholders and, from the perspective of end patients, necessitates changes in their processes for seeking medical consultation and purchasing medications.

We analyze the industry chain from top to bottom. For pharmaceutical manufacturers, having long focused their marketing efforts on in-hospital channels, they have developed a marketing system centered on academic promotion and medical representatives. If sales channels shift, these companies must promptly adjust their strategies for out-of-hospital channel promotion. In addition to the costs required to adapt to out-of-hospital marketing needs, such adjustments involve reallocating interests within existing marketing teams. Internal interest-allocation mechanisms may well lead to delayed responses to market changes, ultimately resulting in the loss of some out-of-hospital market share.

For pharmaceutical distribution companies, excluding those primarily engaged in distribution models, most enterprises in the market still rely mainly on pure sales and other methods. Once prescription outflow occurs, it means that their handled market share will shrink significantly. This will also lead to operational difficulties for some small pure-sales enterprises, or they may seek mergers. For medical individuals who play an important role in the pure sales channel, the impact could be even more devastating because their business logic is broken; the market no longer needs them as a business link point, and the medical resources they control cannot be converted into greater drug circulation volumes.

For medical institutions, the primary consideration at the top level is to eliminate opaque extra benefits from pharmaceuticals. However, it is difficult to improve their compensation through administrative measures in the short term after such cuts. Even with compensation mechanisms such as medical service fees and consultation fees, there will be a significant shrinkage compared to the original drug revenue. Meanwhile, supporting policies for the separation of prescribing and dispensing, such as controlling the drug proportion, zero mark-up, and the two-invoice system, will further erode the ground for gray practices and compress the profit margin.

For patients, the originally integrated one-stop process of seeking medical care and purchasing medications has been split into two separate stages, easily leading to a fragmented experience. Correspondingly, when obtaining medications through out-of-hospital channels, patients are more likely to prioritize the legitimacy and safety of the drugs, as well as clarify liability in the event of adverse incidents. Compared with in-hospital purchases, out-of-hospital medication acquisition also suffers from insufficient professional service quality. These factors constitute persistent barriers to patients’ adoption of out-of-hospital medication channels and will remain in the long term.

III. How to Capture Outflowing Prescriptions

1. How Retail Pharmacies Can Accommodate the Outflow of Prescriptions

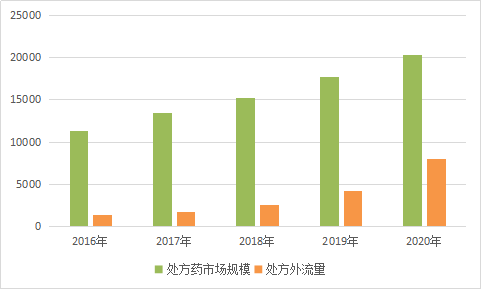

As indicated by the relevant plans issued by the State Council, retail pharmacies will become the primary entities responsible for absorbing prescriptions dispensed outside hospitals. If this transition proceeds smoothly, the scale of the retail pharmacy sector is expected to double within a few years, which undoubtedly represents significant positive news for retail pharmacies.

Scale and Growth Rate of Retail Pharmacies in China (Data Source: CBNRI)

Data on the scale of retail pharmacies also reveals that although the market size has continued to grow over the past five years, the growth rate has declined significantly from its peak. Retail pharmacies are in urgent need of identifying new growth drivers to address the sluggish momentum.

From the perspective of the development patterns of retail pharmacies in China, several major issues exist. First, the chain store penetration rate is low. Statistics from the China Food and Drug Administration (CFDA) show that by the end of 2015, there were 4,981 pharmaceutical retail chain enterprises nationwide, operating 204,000 chain stores, while the number of independent pharmacies stood at 243,000, resulting in a chain store penetration rate of 45.5%. A low chain store penetration rate hinders large-scale operations, leading to a lack of economies of scale in cost control and overall quality management.

Second, market concentration is low, with no nationwide industry leaders. Data show that in 2015, the combined revenue of China’s top ten pharmacy chains accounted for only 17.04% of the retail sector. By comparison, the top three players in the pharmaceutical distribution industry held nearly one-third of the total market size.

Third, there is a shortage of specialized services, most visibly reflected in the deficit of licensed pharmacists. According to data released by the Licensed Pharmacist Qualification Certification Center of the China Food and Drug Administration, as of December 31, 2016, the total number of registered licensed pharmacists nationwide was 342,109, with 303,329 registered in retail pharmacies and medical institutions. This equates to an average of only 2.2 licensed pharmacists per 10,000 people. Based on the approximately 440,000 pharmacies across China, the average number of licensed pharmacists per pharmacy is less than one, meaning that patients are unable to access professional pharmaceutical care services at retail pharmacies.

To address patients' concerns about the legitimacy of medications and medication safety, retail pharmacies must also strengthen their supply chain assurance and brand building to meet patients' service needs.

Furthermore, as an innovative retail model, Direct-to-Patient (DTP) pharmacies hold certain advantages in accommodating the outflow of prescriptions from hospitals. However, they entail higher requirements than conventional pharmacies in terms of capital investment, licensing qualifications, and professional services. Therefore, retail pharmacies should carefully weigh the costs against the expected returns when entering the prescription outflow market through the DTP model.

Overall, the outflow of prescriptions from hospitals will bring significant opportunities to retail pharmacies. However, retail pharmacies should also continuously optimize their operations to ensure both soft and hard capabilities are strengthened. In terms of specific product categories, medications for chronic and common diseases serve as an excellent entry point.

2. How Internet Healthcare Facilitates the Outflow of Prescriptions

In addition to offline retail pharmacies, internet healthcare players—such as pharmaceutical e-commerce platforms, online-to-offline (O2O) pharmaceutical services, and stakeholders associated with internet hospitals—will also benefit from the outflow of prescriptions.

The prerequisite for this judgment is the rapid promotion and widespread adoption of “telemedicine” and “e-prescriptions.” These two innovations have resolved the challenges faced by internet healthcare enterprises, namely the lack of medical resources and the inability to issue prescriptions. By integrating into telemedicine pathways, connected physicians can conveniently provide patients with follow-up consultations, ongoing monitoring, rehabilitation, and other diagnostic and therapeutic services, while simultaneously issuing electronic prescriptions. This re-links the previously separated interaction between medical care and pharmaceuticals, ensuring continuity in the patient experience of seeking medical attention and purchasing medications.

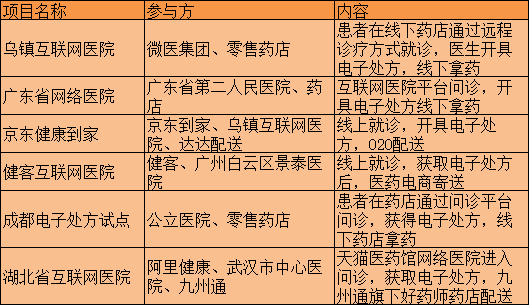

Based on implemented cases, there are both government-led pilots for tiered diagnosis and treatment and electronic prescriptions, as well as “closed-loop” systems sought to be built by internet healthcare companies and pharmaceutical e-commerce platforms. We have collected several cases for analysis of their specific operational models.

Of course, numerous issues exist in the aforementioned cases. For instance, telemedicine cannot accurately assess patients’ conditions, and prescription volumes are difficult to regulate. Driven by considerations of therapeutic efficacy, physicians may be inclined to overprescribe or prescribe high-potency medications, leading to excessive prescribing. Furthermore, given the targeted nature of the collaboration between the parties involved, there may be conflicts of interest, fostering gray-area practices akin to pharmaceutical bribery.

The impact of prescription outflow varies across internet healthcare, pharmaceutical e-commerce, and pharmaceutical O2O (Online-to-Offline) enterprises. Internet healthcare platforms must provide channels for doctor-patient communication and hold qualifications for issuing electronic prescriptions, while offline pharmacies, pharmaceutical e-commerce platforms, and O2O services serve as the ultimate providers of medications. In this process, internet healthcare providers (including internet hospitals) generate revenue from offering doctor-patient communication platforms, whereas offline pharmacies, pharmaceutical e-commerce platforms, and O2O services derive their income from drug sales. Although some companies are trending toward creating a closed-loop “pharmaceutical ecosystem,” it remains essential to distinguish among these different revenue streams, as no single enterprise can fully cover the broad-scale integration of online diagnosis and treatment with medication purchases.

Overall, the out-of-hospital circulation of prescriptions represents a major transformation in the pharmaceutical distribution structure driven by policy. It involves all segments of the drug supply chain and directly impacts the core interests of industry stakeholders; therefore, proactive strategic planning is essential to adapt to these changes.