Over $13 Billion Raised in Just Five Months: A Five-Year Financing Analysis of Liquid Biopsy Companies in the U.S. and China | Company Landscape 2.0

“I was filled with anxiety all day long. That night, I underwent a fine-needle aspiration biopsy; the doctor inserted an endoscope through my throat, down into my stomach, and then into my intestine. He used a needle to puncture my pancreas and extracted some cells from the tumor...” In 2003, Steve Jobs was diagnosed with pancreatic cancer, and he once recalled his experience battling the disease in these words.

What Jobs described was his experience undergoing an organizational biopsy. Clearly, this procedure was painful. Although subsequent advanced treatment regimens afforded him a longer survival time than the average pancreatic cancer patient, Apple ultimately lost its great leader because his disease had already progressed to an advanced stage at the time of diagnosis.

According to the World Health Organization, there are approximately 14 million new cancer cases worldwide each year, with about 8.8 million deaths, resulting in a mortality rate as high as 63%!

In fact, many cancers are curable in their early stages. Unfortunately, because patients typically do not experience noticeable symptoms during the early phases of cancer development, most cases are diagnosed at an advanced stage. Detecting tumor traces at an early stage holds the promise of fundamentally reducing cancer mortality rates.

The advent of liquid biopsy technology has made this possible. It is a non-invasive blood (or other exocrine fluid) testing technique capable of detecting circulating tumor cells (CTCs) and circulating tumor DNA (ctDNA) fragments released into the bloodstream by tumors or metastatic lesions.

This technology was included in MIT Technology Review’s “10 Breakthrough Technologies of 2015” and was rated by Forbes as one of the “Five Disruptive Technologies Shaping the Future of Healthcare.”

Compared with clinical needle biopsy, liquid biopsy offers greater advantages in terms of cost, operability, and real-time performance. More importantly, this technology enables early cancer screening and dynamic monitoring of patients’ disease status.

This technology has attracted a surge of investors and entrepreneurs. Abroad, companies such as Arch Venture Partners, Google Ventures, and Johnson & Johnson have made strategic investments in this field; in China, Livzon Pharmaceutical Group, Da An Gene, and Tencent have also placed their bets. Start-ups have emerged in large numbers, with their quantity increasing sharply in recent years—14 related enterprises were established in China in 2014 alone.

In March 2017, Grail successfully completed a substantial $900 million financing round as scheduled, setting a new record for fundraising in the liquid biopsy market. Additionally, despite lacking Grail’s inherent advantages, Guardant Health, Freenome, and RareCyte have also secured significant funding amounts, leveraging their proprietary technologies and the industry’s favorable growth trajectory. Notably, Guardant Health raised $360 million this year, second only to Grail in terms of financing volume.

Although only five months have passed in 2017, capital market investments in the oncology liquid biopsy sector have exceeded $1.3 billion. We screened 109 liquid biopsy companies from the VCBeat database, comprising 71 Chinese enterprises and 38 U.S. enterprises. We compiled and analyzed their financing data (from 2015 to present) to identify differences between China and the United States and gain insights into future trends.

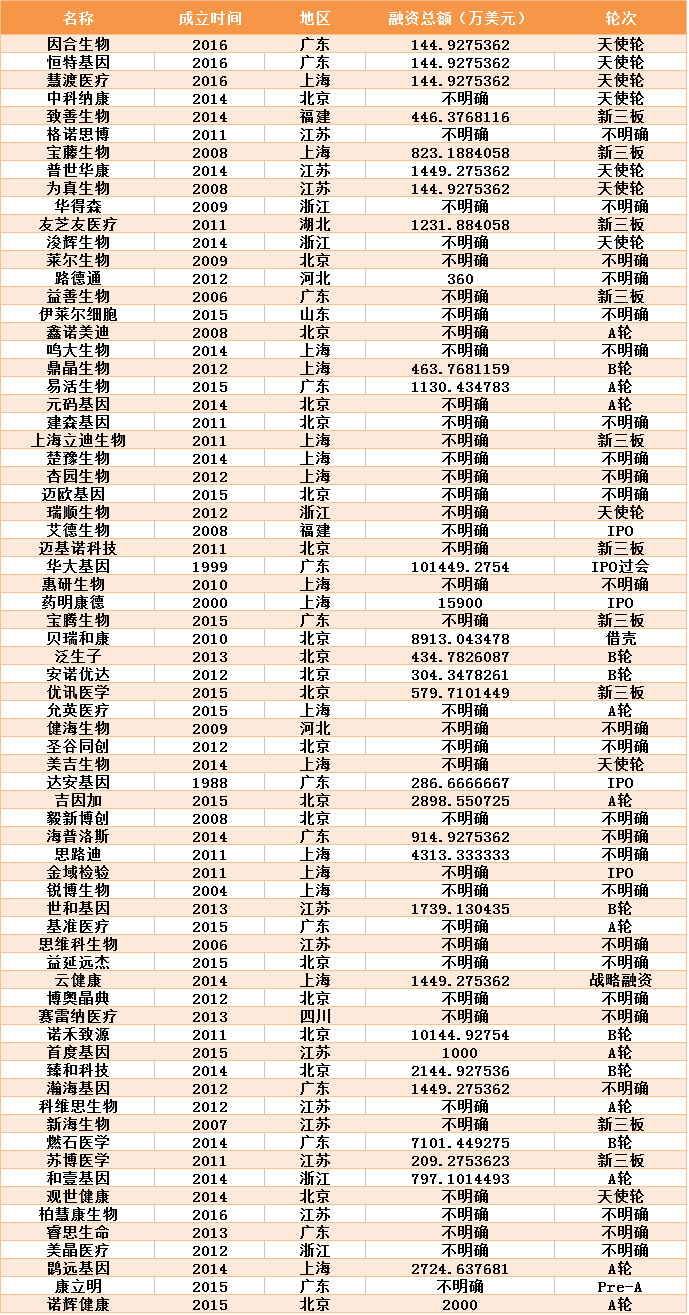

Scan of Liquid Biopsy Companies in China and the United States

China

Note: Financing amounts described as “tens of millions” or “several tens of millions” are all calculated at RMB 10 million, and so on; the RMB-to-USD conversion uses an exchange rate of 6.9.

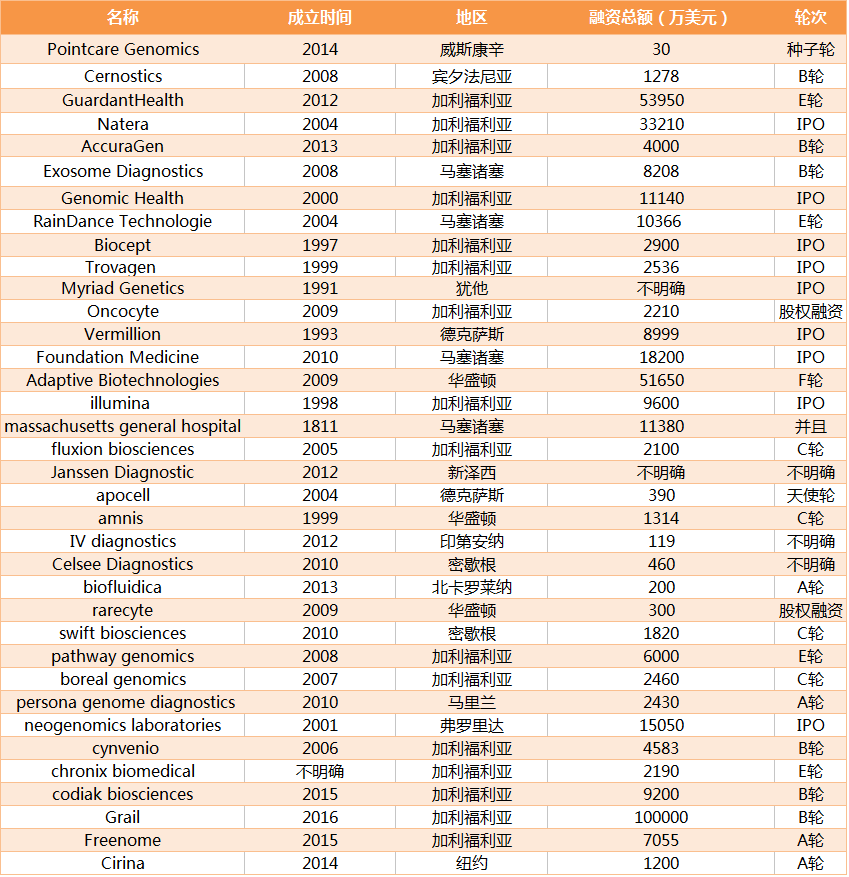

United States

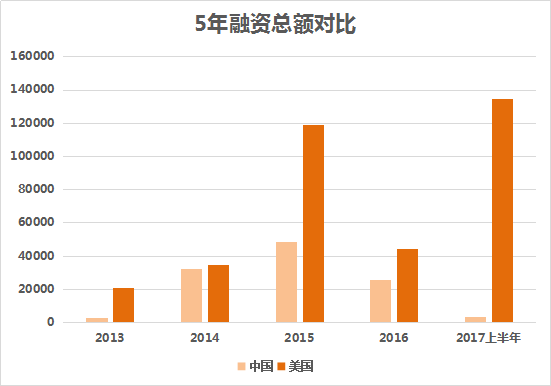

Overall, the trends in total investment in China and the United States over the past five years have been largely consistent, with both countries experiencing a minor peak in 2015. That year, liquid biopsy was included by MIT Technology Review among its “10 Breakthrough Technologies of 2015.”

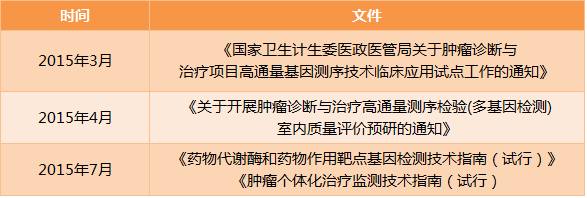

In 2015, President Obama announced the launch of the Precision Medicine Initiative. As a key component, gene technology has seen substantial development.

The Chinese Ministry of Science and Technology has decided to invest RMB 60 billion in the development of precision medicine by 2030. Subsequently, the National Health and Family Planning Commission and the Ministry of Health have issued a series of documents and guidelines related to cancer diagnosis and high-throughput sequencing.

China

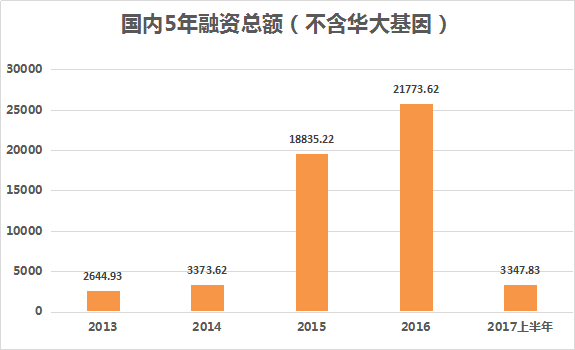

Since 2016, total domestic investment has been on a decline. However, a closer analysis reveals that BGI Genomics completed substantial financing rounds in both 2014 and 2015. As tumor liquid biopsy constitutes only a portion of BGI Genomics’ business portfolio, it is inappropriate to attribute its entire financing amount to the total funding raised for tumor liquid biopsy.

Excluding BGI Genomics' financing amounts for 2014 and 2015, the following data are obtained:

Total financing in China's liquid biopsy sector surged in 2015 and continued to grow in 2016.

In 2017, as of May 31, there were a total of four financing events in the field of tumor liquid biopsy in China. It is not difficult to find that these companies all take tumor liquid biopsy as their core business.

The later the time period, the more financing events are seen among companies primarily focused on liquid biopsy for tumors.

United States

The total annual financing in the field of oncology liquid biopsy in the United States saw a small peak in 2015 and declined in 2016, with the total amounts being $812.26 million and $439.29 million, respectively.By 2017, the U.S. marketThe financing volume has surged, with the total amount raised in just five months exceeding $1.28075 billion.。

It is evident that the surge in financing volume in 2017 was closely tied to Grail’s Series B funding round. Additionally, Guardant Health secured $360 million in its Series E financing. Together, these two companies accounted for 98% of the total financing amount during the first five months of the year. Furthermore, dark horses Freenome and Codiak Biosciences also achieved substantial fundraising amounts over the past two years.

This year, there have been a total of seven financing deals in the United States, with several star companies securing the majority of the funds. It can be inferred that a watershed moment has emerged among companies in this sector in the U.S., and competition is about to reach a fever pitch.

United States

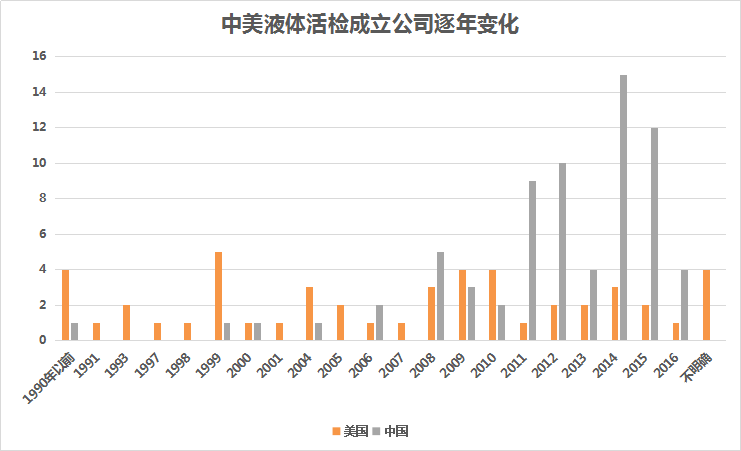

Among these companies, eight were established before 2000. Most of these long-established enterprises have become representative and powerful publicly listed companies, such as Biocept, Trovagene, Illumina, and Myriad Genetics.

Furthermore, since 2008, the number of startups in the United States has seen a continuous increase. Companies such as Guardant Health, Exosome Diagnostics, Foundation Medicine, and Pathway Genomics were established successively. After years of development, these companies have either gone public through initial public offerings (IPOs) or secured substantial financing. They have become the backbone of the industry.

After 2014, emerging players such as Codiak Biosciences, GRAIL, and Freenome were founded. Shortly after their establishment, these companies rapidly secured backing from prominent investors including Founders Fund, Google Ventures, and ARCH Venture Partners, with even tech titans like Bezos Expeditions and Bill Gates making significant investments. Within just two to three years, these companies had risen to become industry leaders.

Companies such as Guardant Health and Foundation Medicine have already captured a portion of the market share; Codiak Biosciences completed technology transfer within just six months; and products from Grail and Freenome are currently in clinical trials.

China

Unlike in the United States, the number of startups in China has grown steadily over time, peaking in 2014.

Early-stage companies either offered comprehensive services, such as BGI Genomics; or focused on upstream segments like reagents, consumables, and chips, such as AmoyDx; or were pharmaceutical companies like WuXi AppTec that established a presence in the liquid biopsy field. In short, few early entrants concentrated on the midstream sector.

Around 2012, midstream service companies such as Berry Genomics, Genetron Health, Annoroad Gene Technology, 3D Medicines, and Novogene were established. Among them, Genetron Health and 3D Medicines focused on tumor liquid biopsy as their core business.

Since 2014, a surge of entrepreneurship has erupted in China’s genomics industry. Against this backdrop, more liquid biopsy companies have been established, such as Genetron Health, Helios Genomics, Gene+ (Jiyinjia), and Hengte Genomics. Between 2015 and 2016 alone, 14 new companies were founded, with the majority focusing on early cancer screening as their core business.

Currently, the midstream sector has the highest enterprise density, but 83.3% of companies in this segment are “new-generation” firms established after 2011. Startups account for half of the midstream landscape, marking the most pronounced difference between the Chinese and U.S. markets. In China, the absence of dominant legacy players has somewhat alleviated competitive pressure on domestic startups.

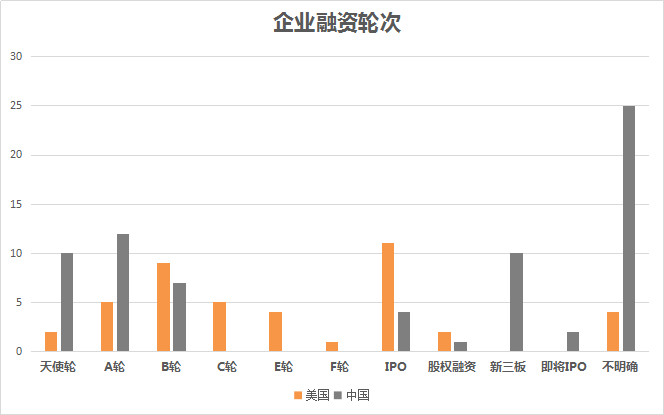

U.S. companies are more concentrated in Series A, B, and C funding rounds, while those in China lag slightly behind by one round. Although Chinese enterprises previously trailed the U.S. market by several years, they are now catching up by building on the experience gained in the U.S. market and gradually narrowing the gap.

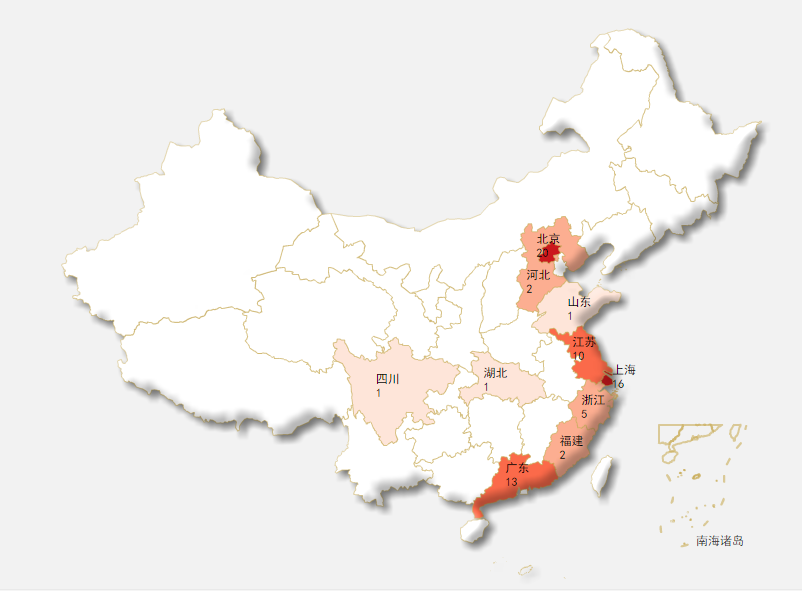

Domestic enterprises are almost exclusively distributed in coastal or near-coastal cities. The Beijing-Shanghai-Guangdong region has the highest concentration, with 19 companies in Beijing, 15 in Shanghai, and 12 in Guangdong Province. This is followed by the Jiangsu-Zhejiang region, comprising 10 companies in Jiangsu Province and 5 in Zhejiang Province.

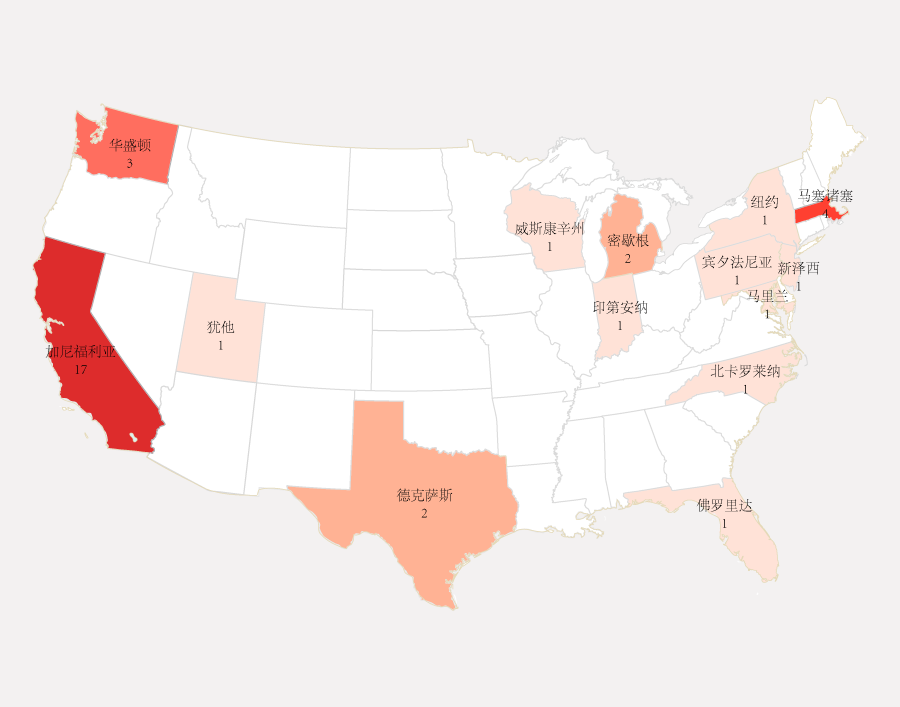

U.S. corporate divisions are more concentrated, with nearly half of the companies clustered in California. This region brings together all the leading enterprises in the industry, such as Guardant Health, Natera, Illumina, Codiak Biosciences, Grail, Freenome, and others.

China

According to public data, Chongde Investment, Northern Light Venture Capital, Cowin Capital, and Sinoway Capital have emerged as the most active investment firms in China. Each of these four firms has invested in three companies:

Both Chongde Investment and Northern Light Venture Capital tend to favor relatively mature startup projects, investing in companies that are more established within the startup ecosystem.

Cowin Capital invested in Daan Gene as early as 2000, and further invested hundreds of millions of RMB in BGI Genomics in 2014; both companies are giants in China’s genomics industry.

Shenhe Capital first invested in BGI Genomics in 2014. Later, through a joint investment with BGI Genomics in GenePlus, Shenhe Capital, along with Chende Capital and Lilly Asia Ventures, invested $20 million in Genetron Health in 2016.

United States

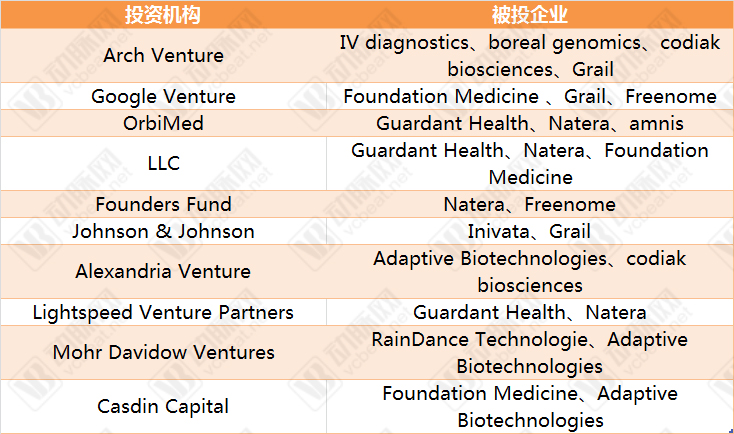

In the United States, Arch Venture Partners, Google Ventures, and OrbiMed are the most active.

Arch Venture has invested in a total of four companies: IV Diagnostics, Boreal Genomics, Codiak Biosciences, and Grail.

Here, it is necessary to introduce the dark horse Codiak Biosciences. This California-based liquid biopsy company was founded in 2015. Unlike companies such as Grail, Genomic Health, Pathway Genomics, and Qiagen, which rely on CTC- or ctDNA-based assays, Codiak employs exosome-based detection technology.

Why Is It Called a Dark Horse? This Company Achieved Technology Commercialization in Just Six Months. Codiak Biosciences’ core product is an exosome-based pancreatic cancer detection assay. This technology boasts high specificity and sensitivity, and more importantly, it can differentiate chronic pancreatitis from early- or late-stage pancreatic cancer.

Google Ventures is a highly active investor in the genomics sector and has also demonstrated strong performance in the niche field of liquid biopsy. “Star enterprises” and “emerging innovators” appear to be the key investment themes for Google Ventures. Its portfolio companies include Foundation Medicine, Grail, and Freenome.

OrbiMed has invested in three companies: Guardant Health, Natera, and Amnis. Among them, Natera is publicly traded with a market capitalization exceeding $550 million.

In addition to the three companies mentioned above, several investment institutions are also highly active.

LLC has invested in Guardant Health, Natera, and Foundation Medicine. Among these, Natera and Foundation Medicine are publicly traded companies; Guardant Health has secured Series E financing and holds significant influence globally.

In addition, star investors such as Founders Fund and Alexandria Venture each invested in two companies, while pharmaceutical giant Johnson & Johnson also established a presence in this sector through investments in two companies.

Goldman Sachs previously predicted that the market potential for liquid biopsy would reach $23 billion globally and $14 billion in the United States, with the market expected to take 5–15 years to fully mature.

Chinese companies are still in their growth phase, while the U.S. market has already begun to show differentiation.Market competition is about to reach a fever pitch.