Jianzhijia, Dalianlin, and Shuyu Pingmin on the Verge of IPO: Is a Second Wave of Pharmacy Chain Listings Underway?

In 1994, 26-year-old Lan Bo headed south to Shenzhen, where he failed to find a job for three months—an experience he later described as “the most difficult period.”

Four years later, Lan Bo resigned from his position as Vice President of National Sales at Haiwang Xingchen Pharmaceutical and returned to his hometown of Kunming to establish Yunnan Jianzhijia Health Chain Store Co., Ltd.

In 2005, media reports referred to Lan Bo as the “Creator of Miracles.” At that time, Jianzhijia operated 135 stores in Kunming, ranking first among chain pharmacies in the city by store count, with annual sales exceeding RMB 200 million.

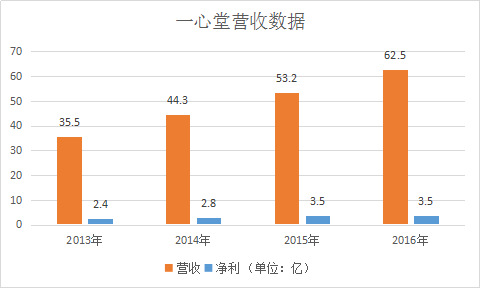

Since 2008, Jianzhijia has been planning its initial public offering (IPO), with the potential to become China’s “first listed chain pharmacy stock.” However, this distinction was ultimately claimed by its Yunnan-based peer, Yixintang.

In May 2017, Jianzhijia made another push for an initial public offering (IPO). In the blink of an eye, it has welcomed the second wave of listings among chain pharmacies.

Two Waves of IPOs

The first time the media used a headline like “Wave of Chain Pharmacy IPOs” was in 2011, when the Ministry of Commerce had just released the “12th Five-Year Plan for Pharmaceutical Circulation.”

The plan states that by 2015, the annual sales of the top 100 pharmaceutical retail chain enterprises shall account for more than 60% of the total sales of all pharmaceutical retail enterprises, with the chain store penetration rate increasing to over two-thirds.

According to data from the Ministry of Commerce, by the end of 2009, there were a total of 388,000 retail pharmacies across China, including 135,000 chain outlets, resulting in a chain affiliation rate just exceeding one-third. In terms of market share, the sales revenue of the top 100 pharmaceutical retailers accounted for 39% of the total sales revenue of all drug retail enterprises.

How to increase the chain ratio and market concentration? The options are limited to self-establishment, mergers and acquisitions, and franchising. The most critical shortage is capital, which has put the initial public offering (IPO) of retail pharmacy chains on the agenda.

At that time, the only independently listed pharmaceutical retail chain in China was Neptune Star—listed on NASDAQ in 2007. The domestic pharmaceutical market lacked a benchmark enterprise for independently listed pharmaceutical retailers, and capital markets were highly enthusiastic about this concept.

Driven by this momentum, several leading regional pharmaceutical retail chains, including Jianzhijia, Yixintang, Laobaixing, and Yifeng Pharmacy, have submitted their IPO prospectuses to the China Securities Regulatory Commission.

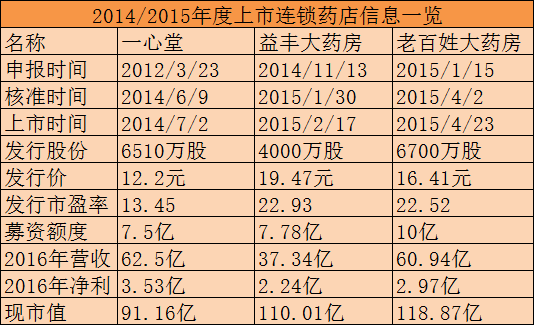

The entire process—from filing for listing, prospectus disclosure, regulatory feedback, preliminary review, and issuance review, to final approval—typically takes an average of 2–3 years, especially when compounded by policy-driven closures of the IPO window. Ultimately, Yunnan Yixintang emerged as the standout candidate, earning the distinction of being the “first publicly listed chain pharmacy stock.”

On July 2, 2014, Yixintang’s shares surged 44.02% on their debut trading day, followed by another limit-up close the next day, pushing its market capitalization above RMB 5 billion—a clear testament to strong market enthusiasm.

Following Yixintang, Yifeng Pharmacy and Laobaixing Pharmacy subsequently listed on the A-share market, with increasing fundraising amounts and sustained investor enthusiasm, marking the first wave of IPOs among chain pharmacies.

Data source: Prospectuses of respective companies; market capitalization as of the close on June 6.

Five years later, by December 2016, the Ministry of Commerce released the “13th Five-Year Plan for Pharmaceutical Distribution,” once again presenting significant policy-driven opportunities for major growth in the pharmaceutical retail industry.

Similar to the previous five-year plan, the “13th Five-Year Plan for Pharmaceutical Circulation” also outlines a timetable and roadmap. It requires that by 2020, the annual sales of the top 100 pharmaceutical retail enterprises account for more than 40% of the total pharmaceutical retail market, with the pharmaceutical retail chain rate exceeding 50%. This goal is considerably more “grounded” than that of the previous five-year plan.

According to the annual statistical report of the China Food and Drug Administration, as of the end of November 2016, there were 5,609 pharmaceutical retail chain enterprises across China, with 220,000 chain stores and 226,000 independent retail pharmacies. Based on these figures, the target of a 50% retail chain rate is approaching.

In terms of market share, data from the Ministry of Commerce shows that the top 100 Chinese retail enterprises generated a total revenue of RMB 95.6 billion in 2015. Based solely on the RMB 300 billion pharmaceutical retail market, the market share of the top 100 pharmaceutical retail enterprises still falls short by 10 percentage points.

If the first wave of IPOs among chain pharmacies enabled pharmaceutical retail enterprises to address the issue of low chain penetration, then the primary objective for the industry in the next phase will be to enhance market concentration.

The approach invariably involves enhancing the “soft power” of chain pharmacies through IT transformation, marketing, channel expansion, and service diversification. Capital remains a primary prerequisite, prompting chain pharmacies to embrace a second wave of IPOs.

Data source: Prospectuses of respective companies; Shuyu Pingmin data is for the first half of 2016.

Yixintang Case Study: How to Leverage the Role of Listed Companies

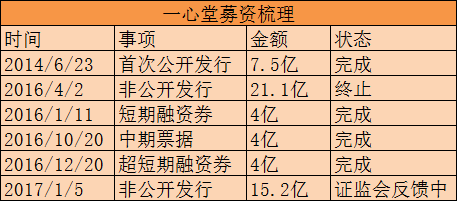

What to Do After Going Public? Clues May Be Found in Yixintang. According to its historical announcements reviewed by VCBeat (WeChat ID: vcbeat), in addition to raising funds through its initial public offering, Yixintang has also engaged in financing activities such as private placements, medium-term notes, and super short-term and short-term financing. Currently, Yixintang still has a private placement plan amounting to RMB 1.52 billion under review.

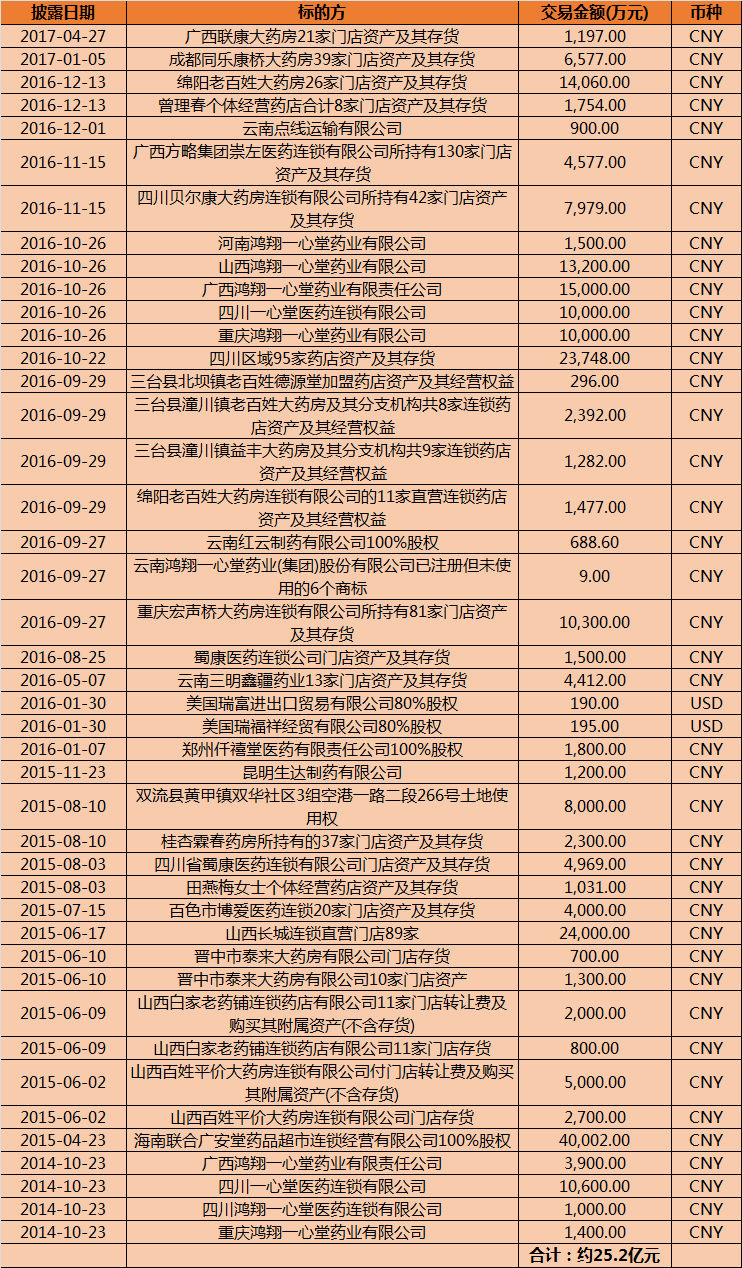

Corresponding to its financing information, the aspect of Yixintang that has attracted the most external attention is its “aggressive acquisitions.” Historical announcements show that since its listing, Yixintang has carried out 43 M&A transactions, with the targets primarily being pharmacies across various regions, while also involving pharmaceutical manufacturing companies and pharmaceutical commercial enterprises.

Data source: Compiled from Yixintang's announcements

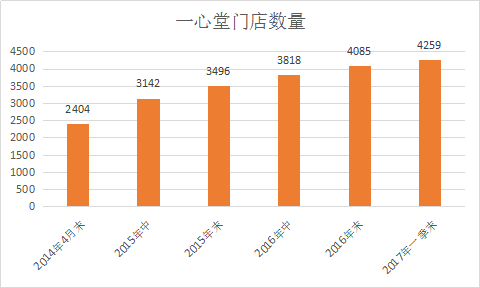

We can assess the completion status of Yixintang’s mergers and acquisitions by examining the changes in its store count.

Data Source: Compiled based on Yixintang's announcements

As can be seen from the table above, by the end of the first quarter of 2017, the number of Yixintang stores had increased by nearly 2,000 compared to the time of its IPO. Through new store openings and acquisitions, Yixintang adds 600–700 stores annually.

From a regional distribution perspective, Southwest China is its primary area of expansion. Yixintang’s first-quarter report also disclosed that as of March 31, 2017, Hongxiang Yixintang and its wholly-owned subsidiaries operated a total of 4,259 directly-run chain stores. Of these, 2,887 were in Yunnan, 336 in Guangxi, 326 in Sichuan, 212 in Shanxi, 160 in Guizhou, 165 in Hainan, 145 in Chongqing, and 28 in other provinces and municipalities.

Let us further examine the changes in Yixintang’s revenue, comprehensively analyzing the correlation between the number of stores and the parent company’s revenue.

Data source: Compiled from Yixintang’s announcements

As can be seen, while Yixintang’s store count has grown substantially, its revenue has increased, yet its net profit has remained relatively flat. This outcome stems from multiple factors: first, acquisitions require paying a certain premium to the sellers of the target assets; second, the acquired entities must complete procedures such as updating their licenses and permits before they can be consolidated into the financial statements of Yixintang’s parent company; and third, the profitability of these acquired targets lags significantly behind that of large-scale chain operators already benefiting from economies of scale, thereby affecting the listed company’s overall earnings performance.

Overall, after its initial public offering (IPO), Yixintang leveraged its status as a listed company to carry out a series of capital increases, channeling the funds into store expansion and the transformation of existing businesses, thereby significantly enhancing its comprehensive strength.

“Steady progress in organic growth, continuously expanding market share.” and “Prominent expansion through M&A, driving rapid growth in core business revenue.” This is how Yixintang explained the reasons for its performance growth.

Current State of Competition in China's Pharmaceutical Retail Market

Across the entire pharmaceutical retail market, the landscape is becoming increasingly dynamic: while the growth rate of total sales is slowing, favorable developments such as the separation of prescribing and dispensing and the outflow of prescriptions from hospitals are emerging. Coupled with consumption upgrades and the industry’s shift from pharmaceuticals to broader health services, these factors are reshaping the market environment.

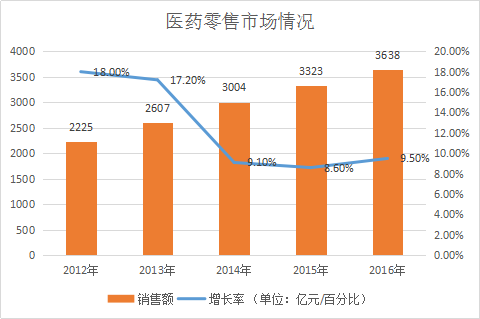

First, let us examine the market size. According to relevant data from the Ministry of Commerce, sales in the pharmaceutical retail market grew from RMB 127.5 billion in 2010 to RMB 332.3 billion in 2015. However, the overall market growth rate has declined from a peak of 47.8% to 8.6%. This lowest growth rate is now below the concurrent growth rate of total sales in the pharmaceutical distribution industry.

Data Source: Ministry of Commerce Statistical Bulletin and Industry Research

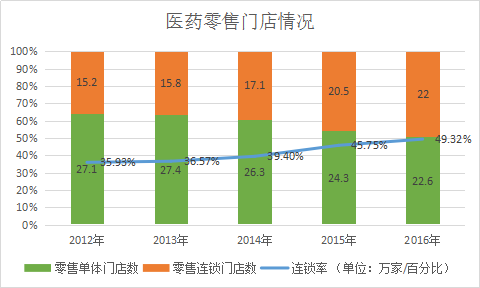

Additionally, as previously mentioned, the number of pharmaceutical retail outlets continues to grow, and the chain store penetration rate is steadily increasing. Here, we can examine the detailed data.

Data source: Statistical Bulletin of the China Food and Drug Administration; 2016 data are as of November.

As can be seen, in terms of store count, the industry is actually undergoing a process of “independent stores exiting while chain stores expand.” The total number of stores increased by only about 20,000, whereas the number of chain stores rose by nearly 70,000. In contrast, approximately 50,000 independent retail pharmacies effectively “disappeared.” Among the factors driving this shift were acquisitions of independent pharmacies by listed companies such as Yixintang.

Furthermore, the pharmaceutical retail market also has a “saturation standard” of 2,500 people per store. Based on 2016 data, with a population of 1.375 billion and 446,000 stores, the average number of people served per pharmacy was 3,082, indicating that the market is already approaching saturation. This implies that, barring significant demographic changes, the number of pharmaceutical retail outlets will not see substantial growth in the future.

It is also worth noting that the pharmaceutical retail industry already has a very high securitization rate, with industry leaders being either publicly listed companies or controlled by such entities.

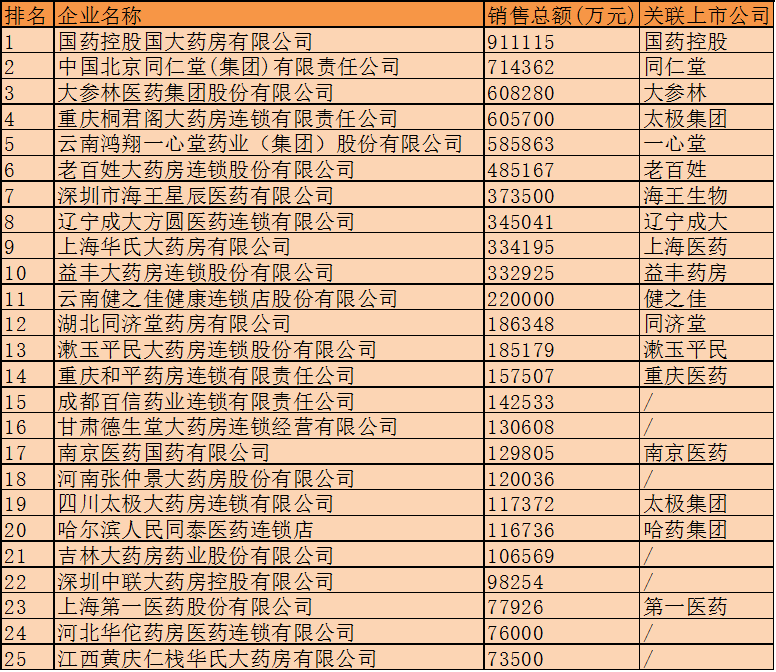

Data Source: Ministry of Commerce’s 2015 Top 100 Pharmaceutical Retailers List

According to the “Top 100 Pharmaceutical Retailers in 2015” released by the Ministry of Commerce, all of the top 10 companies have publicly listed backgrounds, and only three of the top 20 lack such backgrounds.

On June 6, Dashenlin’s initial public offering (IPO) application was approved by the China Securities Regulatory Commission (CSRC). The company plans to issue no fewer than 40 million shares, raising RMB 1.8 billion, thereby setting a new record for IPO fundraising in the pharmaceutical retail sector. Barring any unforeseen circumstances, Dashenlin is expected to launch its share offering within one to three months following the preliminary review, becoming the first listed company in the second wave of IPOs among chain pharmacy operators.

The chairman of Dashenlin is a native of Maoming, Guangdong. He speaks with a distinct western Guangdong accent and occasionally intersperses his speech with local slang. In his memory, the “most difficult period” was in 2011. That year, Dashenlin recruited Watsons China’s senior executive team at high salaries to implement diversification reforms. However, the initiative yielded unsatisfactory results, adversely affecting the company’s performance.

“2011 was a year of chaos for us, but great order emerges from great chaos, which aligns with the laws of history.” Two years later, Ke Yunfeng described that period in this way during an interview with the media.

Looking back, Dashenlin’s strategies at the time—diversified operations, building a comprehensive health group, capital maneuvers, and forming pre-IPO alliances—were all well aligned with the market conditions then. However, from the first wave of IPOs to the second, the competitive landscape has shifted significantly.