Express Scripts vs. Haihong Holdings: A Comparative Analysis of PBM Models in the U.S. and China

Eight years ago, Haohong Holdings signed a strategic cooperation agreement with ESI, the largest pharmacy benefit manager (PBM) in the United States, marking the beginning of the PBM narrative in China.

Over these eight years, ESI’s market capitalization once soared to $56 billion. As a comparable case, Haihong Holdings’ stock price also peaked in mid-2015, with its market cap reaching RMB 72.5 billion at its highest. This scale would still easily place it among the top 20 listed pharmaceutical companies on China’s A-share market today, underscoring the clear boost from the PBM (Pharmacy Benefit Management) concept.

Since the emergence of Haihong Holdings, an increasing number of companies in China have ventured into the PBM (Pharmacy Benefit Management) business, with several even designating it as their “core business,” thereby serving as a powerful tool to attract investors.

However, compared with ESI, which covers more than 95% of retail pharmacies across the United States, has nearly 100 million contracted members, and reviews over 1.4 billion prescriptions annually, Chinese companies appear much less prominent.

PBM’s China Story: Year Eight. As ESI Posts $3 Billion in Annual Net Profit, the PBM Market in China Remains Uncertain.

A Cost-Control Product Under the U.S. Healthcare System

PBM, short for Pharmacy Benefit Management, is a specialized third-party healthcare service.

Strictly speaking, PBM is a product of the U.S. healthcare system. Unlike the universal health coverage systems in China and some European countries, where health insurance funds are centrally managed by the government, the U.S. healthcare model relies on employers purchasing insurance for their employees, with commercial insurance serving as the primary payer.

In this context, insurance companies have devised various strategies to control medical expenses in order to reduce costs. Examples include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Point of Service plans (POS), and Accountable Care Organizations (ACOs).

Its primary operational approach involves transitioning from a fee-for-service model to managed care with end-to-end monitoring, strictly controlling healthcare expenditures through mechanisms such as health management, disease prevention, and diagnosis-related group (DRG) payment systems, thereby reducing costs for insurance providers and employers.

Similar to the cost-containment methods mentioned above, Pharmacy Benefit Management (PBM) is also a approach to controlling healthcare insurance costs, with its primary focus on pharmaceuticals. By collaborating with insurance providers, pharmaceutical companies, and healthcare institutions, PBMs intervene in the medication process. They review and modify prescriptions—such as substituting originator drugs with lower-priced generics—without compromising patient treatment outcomes, thereby achieving the goal of controlling healthcare insurance expenditures.

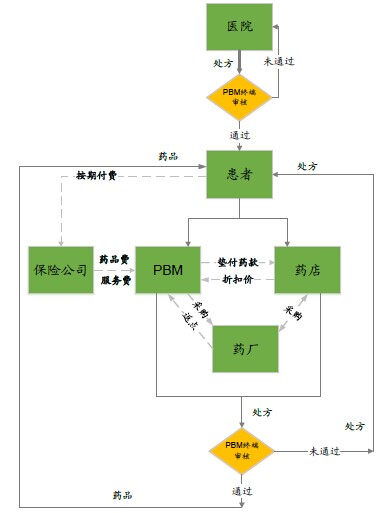

So, how does PBM achieve the goal of cost control? In other words, how can it ensure that interventions in prescriptions are effective?

PBM Organizational Process

Source: Tiantuo Consulting

The main operational methods of PBM can be summarized into four aspects:

1. Medication Use Management.This section represents the core focus of Pharmacy Benefit Managers (PBMs). Their primary operational strategies include: first, collaborating with relevant research and medical institutions to develop a formulary (similar to social insurance or essential medicine lists), requiring affiliated healthcare providers to prioritize medications within this formulary for reimbursement eligibility; second, implementing prior authorization, whereby the use of new drugs or those not included in the formulary requires approval from both the PBM and the insurer to curb the utilization of high-cost medications; third, issuing drug interaction alerts, where prescriptions are uploaded after being written by physicians to screen for potential drug-drug interactions and adverse effects; and fourth, controlling overall prescription volumes to prevent excessive or inappropriate prescribing.

2. Intervention in Drug Access Methods.The pharmaceutical distribution structure in the United States differs significantly from that in China, with the primary distribution channels being outside hospitals. Prices through hospital-based channels are higher than those through out-of-hospital channels. Pharmacy Benefit Managers (PBMs) have leveraged this disparity by recommending that patients obtain medications through retail pharmacies or mail-order services to reduce drug costs.

3. Differentiated Reimbursement Rates.PBMs have designed different payment methods for various types of prescription scenarios. First, different reimbursement rates are set for brand-name drugs and generic drugs, with a recommendation to use generics and lower-cost alternatives. Second, insurance reimbursement ratios are dynamically adjusted based on negotiation outcomes with pharmaceutical companies, with costs exceeding the covered amount paid out-of-pocket by patients. Third, caps are placed on the proportion and absolute amount of insurance coverage within total medication expenses, requiring patients to cover any costs beyond these limits.

4. Chronic Disease Management.Given that a significant proportion of individual members covered by Pharmacy Benefit Managers (PBMs) are patients with chronic diseases, PBMs have designed long-term dynamic monitoring mechanisms tailored to this population. Through sustained patient education, these initiatives aim to enhance medication adherence and reduce the risk of severe health complications.

In terms of its revenue model, PBMs primarily charge self-insured large employers, insurance carriers, pharmaceutical companies, and retail pharmacies. Specifically, fees from large employers and insurance carriers are justified by the effective reduction in their medical cost expenditures; meanwhile, collaborations with pharmaceutical companies and retail pharmacies mainly serve to drive sales volume.

In addition, pharmaceutical retailers such as CVS also operate PBM businesses, integrating PBMs with retail pharmacy and mail-order services to boost drug sales.

More importantly, the primary reason PBM companies have become the critical link connecting the upstream and downstream segments of the pharmaceutical industry chain is their ability to effectively balance the interests of all stakeholders. Through systematic operations by third-party entities, PBMs integrate pharmaceutical demanders, suppliers, and payers. By securing scaled corporate and individual memberships on the front end, they gain bargaining leverage against pharmaceutical manufacturers and retail pharmacies. This approach not only ensures a stable supply of pharmaceuticals but also enhances satisfaction among healthcare consumers.

Case Study of U.S. PBMs: ESI Group

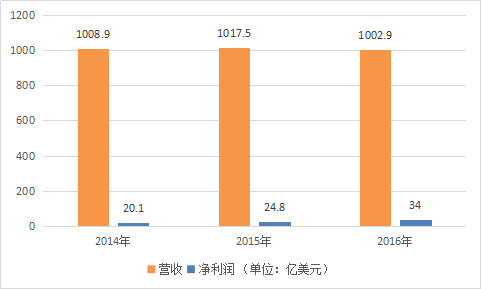

ESI Group, fully known as Express Scripts, is the largest company in the United States engaged in PBM (Pharmacy Benefit Management) services. According to its 2016 annual report, it covered more than 95% of retail pharmacies nationwide, with annual revenue reaching $100.2 billion and net profit amounting to $3.4 billion.

ESI was founded in 1986 through the merger of Medicare Glaser Inc. and Sanus Corp. At its inception, it operated only 79 retail pharmacies, with its headquarters located in St. Louis, Missouri.

In 1993, ESI began releasing its Annual Report on Drug Trends and hosting thematic seminars on outcomes, publishing detailed utilization reports on prescription drug expenditures. The report provided a comprehensive analysis of competition in the U.S. prescription drug market and began to examine competitive dynamics from the perspective of controlling prescription drug spending.

In 1998, the rapidly growing ESI embarked on its acquisition and expansion journey. In April of that year, it acquired ValueRx, the pharmacy benefit management (PBM) subsidiary of Columbia/HCA Healthcare Group. The following year, ESI made another move, acquiring DPS, a company under SmithKline Beecham, for $70 million.

In December 2006, ESI sought to acquire another PBM company, Caremark, but faced opposition from CVS, a giant in the chain pharmacy industry. Considering the potential monopoly concerns (the U.S. government's commerce department might issue an antitrust ruling), Caremark was ultimately acquired by CVS for a transaction price of $26.5 billion.

Apart from this single failure, the list of companies acquired by ESI during the first decade of the new century is extensive. It includes NPA, CuraScript Specialty Pharmacy, ConnectYourCare, the pharmacy services division of MSC, and NextRx, a subsidiary of WellPoint, among others.

In 2011, ESI made a $29.1 billion acquisition offer for Medco, which once served over 30 million insured individuals and was the second-largest PBM company in the United States. The deal was officially approved in March of the following year after undergoing a six-month antitrust investigation by U.S. regulatory authorities.

This transaction also positioned the new ESI Group as the most influential PBM company in the United States, covering over 80 million insured individuals, processing 1.4 billion prescriptions annually, and driving the group’s annual revenue beyond $100 billion.

ESI Group’s Headquarters in Missouri

In 2017, ESI launched the Inside Rx program, through which its holding subsidiaries would provide prescription drug discounts to uninsured or underinsured individuals.

ESI’s core business comprises four key areas:

Pharmacy Benefit Management.This business primarily provides pharmacy benefit management (PBM) services for large employers, insurance companies, and government agencies. ESI participates in the design of insurance and benefits plans, cost review, claims payment, formulary management, and clinical pathway management. Meanwhile, ESI also collaborates with healthcare providers to secure discounts in exchange for patient referrals.

Pharmaceutical Informatics Services.This business primarily involves electronic prescription platforms, prescription review platforms, and data storage.

Pharmaceutical Retail.In fact, ESI has become the third-largest pharmaceutical retail organization in the United States, after CVS and Walgreens. It provides medication supplies to more than its managed members through mail-order and online pharmacies, including new specialty drugs and investigational drugs.

Medical Service Management and Disease Management.This business primarily provides services such as physician evaluations, analysis and comparison of prescribing patterns, new drug information, and disease-related knowledge. It also offers individual members services including disease prevention, medication management, and dietary recommendations.

ESI Revenue and Net Profit Data (Source: Yahoo Finance; Unit: USD 100 million)

Haikong Holdings' 8-Year PBM Journey

In 2009, Haihong Holdings partnered with ESI Group to launch pilot programs for medical insurance cost containment, making PBM the core business promoted by Haihong Holdings.

Notably, 2009 also marked the launch of a new round of “healthcare reform,” with healthcare insurance cost containment being one of its key tasks. It can be said that Haihong Holdings entered the healthcare insurance cost containment business at an opportune moment.

Haihong Holdings’ approach is to operate as a third-party tool provider, entering into cooperative agreements with local healthcare security administrations to build an intelligent prescription audit assistance platform and deliver refined management services for medical insurance funds.

In the following years, Haihong Holdings successively entered into partnerships with the Zhanjiang Social Security Fund Administration, the Zunyi Social Security Bureau, the Yueyang Medical Insurance Fund Management Office, and the Chengdu Medical Insurance Bureau. It provided third-party services for local medical insurance fund management in areas such as intelligent auxiliary review of medical insurance claims and medical insurance big data, with the government purchasing these services as the payment model.

According to Haihong Holdings’ 2016 annual report, by the end of 2016, the company’s medical insurance cost containment business had expanded to cover nearly 200 prefecture-level cities across 24 provinces and municipalities directly under the central government in China. Meanwhile, projects in nearly 30 regions were either under construction or had already achieved full-process management encompassing pre-event prevention, in-process control, and post-event intelligent auditing.

Meanwhile, Haihong Holdings has also actively ventured into the business of managing medical insurance funds. Its third-party fund management model is being promoted in cities such as Zhanjiang and Chengdu. The scope of its services has expanded from the original review of medical bills to include auxiliary services for payment method reforms, such as Diagnosis-Related Groups (DRGs) and entrusted medical insurance payment standards. Additionally, it provides supplementary payment system services for medical insurance, commercial insurance, and insured individuals, as well as health management services for the insured.

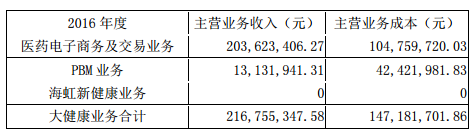

So, how has the revenue from this segment performed? According to the annual reports of Haihong Holdings, its PBM business generated no actual revenue in 2009 and 2010. Since 2012, the annual revenue from this business has remained at approximately RMB 10 million. Over the years, the revenue growth for this segment has been modest.

Taking its 2016 data as an example, its PBM business generated RMB 13.132 million in main business revenue, incurred RMB 42.422 million in business costs, and recorded a net loss of approximately RMB 30 million.

Table 1: Revenue Composition of Haihong Holdings in 2016

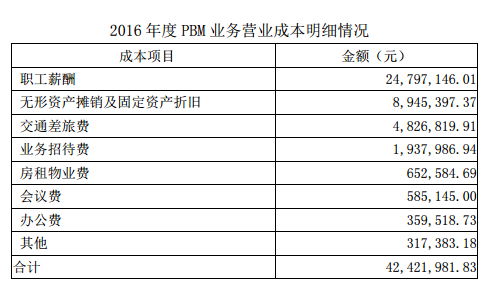

Table 2: Breakdown of Costs for Haihong Holdings’ PBM Business

Within its overall business framework, Haihong Holdings stated that it will continue to use intelligent health insurance audit services as its entry point, deeply leverage big data analytics, and extend its operations into areas such as fund management, commercial insurance services, chronic disease management, and collaborations with pharmaceutical manufacturers.

In terms of its business model, Haihong Holdings will charge service fees to medical insurance administrators based on the scope of services provided. Meanwhile, it will engage in innovative collaborations with pharmaceutical manufacturers, charging them information service fees and value-added service fees. Additionally, the company aims to achieve breakthroughs in revenue generation through patient-side health management services and third-party services for commercial insurance institutions.

However, Haihong Holdings also stated that due to varying degrees of business progress across different regions, a unified fee structure has not yet been established. Building on its existing business foundation, Haihong Holdings is actively exploring various pricing models, such as fees based on service content and proportional fees based on fund size, while maintaining active communication with relevant authorities.

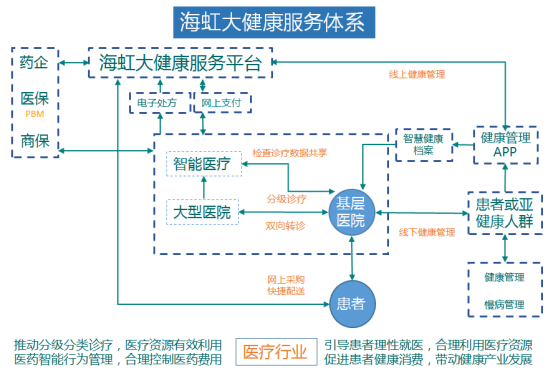

Table 3: Haihong Holdings' Big Health Service System

Source: Supplementary Announcement to Neusoft Healthcare's 2016 Annual Report

"Oranges Grown in Huainan"

“When orange trees grow south of the Huai River, they bear oranges; when they grow north of the Huai River, they bear trifoliate oranges. Their leaves look similar, but their fruits taste different. Why is this so? Because the soil and water are different.”

The differing trajectories of PBMs in China and the United States have prompted industry practitioners to reflect on the adage that “orange trees grown south of the Huai River yield different fruit.” A securities analyst who has long tracked the pharmaceutical and healthcare industry told VCBeat that the success of PBMs in the U.S. is attributable to the fact that healthcare expenditures are primarily borne by employers and commercial insurers, which have a direct need for cost containment. Additionally, given the high level of health information technology adoption in the U.S., PBM companies benefit from abundant data sources, enabling evidence-based practices that have garnered recognition from all stakeholders, including patients.

In contrast, in China, social insurance accounts for a substantial proportion of healthcare expenditures. The pressure to control costs falls primarily on medical insurance administrative authorities, which rely mainly on administrative measures rather than market-based mechanisms. Consequently, the role of third-party cost-containment platforms has not been effectively leveraged.

However, as the payment pressure on medical insurance funds becomes increasingly prominent, local medical insurance authorities are also considering introducing third-party tools through government procurement of services. Influenced by this trend, medical informatics companies, commercial health insurers, pharmaceutical distributors, and retail companies have successively turned their attention to this market, leveraging their own resources to explore China-style PBM (Pharmacy Benefit Management) businesses. In addition to Haihong Holdings, Ping An Insurance, Sinopharm Health, and Jiashitang have all made strategic moves in this area.

However, the challenges faced by various companies are largely similar to those of Haihong Holdings: “a unified fee schedule has not been established,” and the revenue generated fails to cover the incurred costs.

In addition to the distinct differences in payers, factors such as limited health information exchange among hospitals, conflicts of interest related to prescription rights, and difficulties in standardizing prescription formularies have also constrained the development of PBM businesses to some extent.

A mid-level executive at a health insurance company also stated in an interview with VCBeat that part of the reason PBM faces difficulties in China is that the vested interests tied to prescriptions are hard to disrupt. Although the separation of prescribing and dispensing is now required, hospitals still derive significant benefits from the prescription circulation process. Since the core function of PBM lies in the review and modification of prescriptions, it is difficult to persuade hospitals to relinquish this authority in the short term.

She also pointed out that another core aspect of PBM isFormularyHowever, given that medical insurance formularies across different regions have yet to be unified, it is impractical to establish a nationwide solution. Furthermore, the authority to formulate these formularies currently rests with the medical insurance administrative departments. Unless this authority is delegated or distributed to commercial insurance companies, Pharmacy Benefit Management (PBM) will inevitably remain confined to small-scale development.

In addition to the practical challenges encountered, some industry insiders have identified favorable developments within the sector. Lu Sheng, Senior Partner at Shengrui Pharmaceutical Consulting, told VCBeat that the long-term deficit in the basic medical insurance fund has prompted regulatory authorities to explore diversified cost-containment measures, includingIntroduction of Third-Party Administrators (TPAs) and Collaboration with Commercial Health Insurancemanner.

He pointed out that, regarding collaboration between basic medical insurance and commercial health insurance, Shanghai began piloting in 2015 the use of surplus funds from personal medical insurance accounts to purchase commercial insurance, with subsidy amounts determined by disease categories. Last year, 25 counties and cities in Anhui Province also launched a model in which commercial insurance companies handle the reimbursement, compensation, and settlement for urban and rural residents’ basic medical insurance.

However, commercial health insurance currently exhibits certain deficiencies in the areas of health and medical insurance, including a limited range of products, inefficient underwriting and claims processing, and a lack of professional medical data—precisely the areas where Pharmacy Benefit Management (PBM) excels.

In addition to participating in the management of medical insurance funds, PBMs can also collaborate with commercial insurance companies by providing professional services such as insurance product design, claims process optimization, and medical data support. This has been the foundation for the development of the PBM industry in the United States.

In addition, research institutions have noted that pharmaceutical retail is a major revenue source for PBM companies, aside from their income derived from healthcare cost containment.Taking ESI as an example, its annual revenue in 2013 was $104.1 billion, of which only $1.231 billion came from service fees, with the remaining $102.8 billion derived from pharmaceutical distribution.

This also provides domestic companies aspiring to engage in PBM business with greater possibilities in terms of business models. If pharmaceutical distribution and retail-related companies begin to lay out PBM operations, or choose to collaborate with established PBM firms, they can enhance the self-sustaining capability of PBM services to a certain extent, thereby ensuring their practical implementation.

Overall, PBM has a solid foundation for growth in China. Relevant companies should first establish a strong base by focusing on clinical data and formulary directories, then seek deeper collaboration with basic medical insurance and commercial health insurance. By leveraging pharmaceutical retail as a revenue breakthrough point, they can enhance multi-tiered services spanning from the payer side to the patient side.