450,000 Hemodialysis Patients, RMB 33.5 Billion Market: A Lucrative Opportunity in China's Independent Dialysis Center Sector

In April this year, VCBeat published an in-depth analytical article titled “An In-Depth Analysis of Independent Hemodialysis Centers: This Niche Sector Already Boasts a RMB 150 Billion Market Opportunity,” which attracted considerable attention from readers. The article provided a detailed examination of the business layouts, revenues, and number of facilities of DaVita and Fresenius, the two largest hemodialysis service providers globally, in North America, and pointed out that the hemodialysis market in China is currently in an untapped stage.

In late December 2016, the National Health and Family Planning Commission successively issued the basic standards and management specifications for four categories of independently established medical institutions: medical imaging diagnostic centers, medical laboratories, hemodialysis centers, and pathology diagnostic centers. The commission encouraged the opening of hemodialysis centers to private capital and promoted their development along chained and group-based lines. As the only patient-oriented institution among these four types of independent medical entities, hemodialysis centers have attracted significant attention from private investors due to their substantial growth potential.

So, what is the current state of development for independent dialysis centers in China? Which companies and institutions are involved, at what stage of development are they, and what are the major challenges they face? VCBeat has analyzed domestic dialysis data and interviewed several leading private independent hemodialysis service providers in China to provide a detailed overview of the current status and development trends in this niche sector, while identifying investment opportunities.

During the preparation of this report, VCBeat gained first-hand insights into independent hemodialysis centers in China through interviews. We extend our special gratitude to the following industry professionals for their support of VCBeat.

Chen Shaobo, Chairman of Beijing Dakang Medical Investment Co., Ltd.

AiShen Medical COO Zhang Yongqiang

Cheng Shaokai, Executive Director of Beijing Huansheng Medical Investment Co., Ltd.

Shengrenkang Medical Group VP, Chen Shi

Chongqing Aokailong Medical Technology Co., Ltd. General Manager and Board Secretary Jia Bei

Wang Wei, CEO of Beijing InforMed Information Technology Co., Ltd.

Su Yuanbin, Executive Director of Guangdong Weigao Blood Purification Medical Technology Co., Ltd.

This report consists of the following sections:

I. Dialysis Treatment Modalities for Patients with ESRD

II. The Market Potential in the Hemodialysis Service Sector Is Enormous

III. Distribution of the Hemodialysis Industry Chain

IV. China’s Policy on Liberalizing Independent Hemodialysis Centers

V. Case Study of a North American Chain Hemodialysis Center

VI. Case Studies of Independent Hemodialysis Centers in China

Through two months of interviews and data compilation, VCBeat has distilled key data and insights upon completing this report:

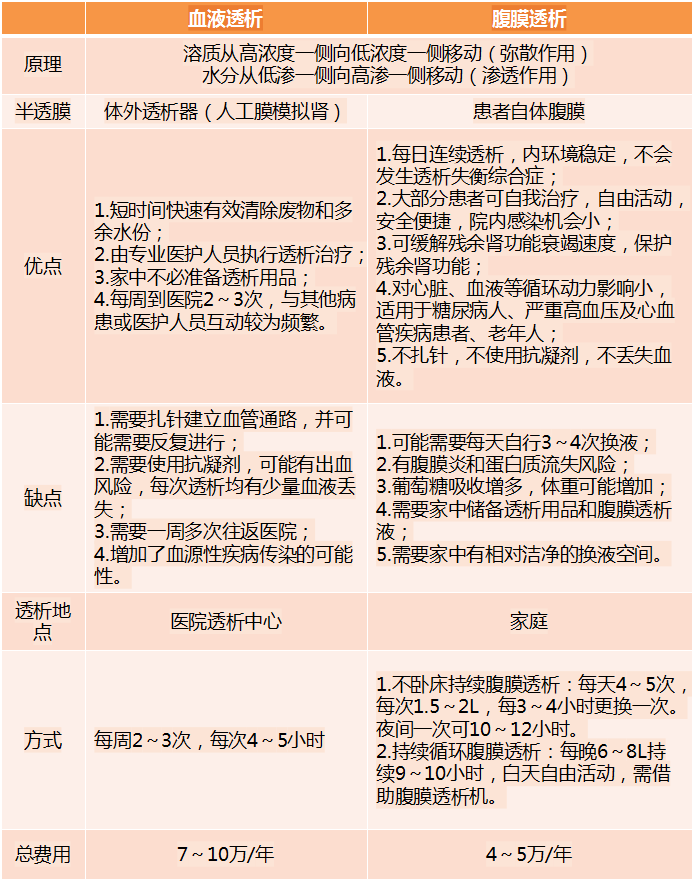

1. Hemodialysis and peritoneal dialysis differ in their underlying principles, each with its own advantages and disadvantages. In most countries worldwide, the majority of patients with end-stage renal disease (ESRD) primarily undergo hemodialysis, with an approximate ratio of 9:1 between hemodialysis and peritoneal dialysis patients.

2. In 2014, the number of patients with end-stage renal disease (ESRD) in China was nearly 2 million and is projected to reach 3.15 million by 2030.

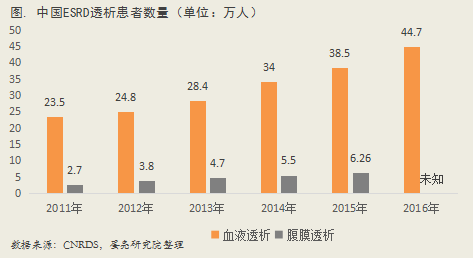

3. According to CNRDS statistics, the number of hemodialysis patients in China has increased significantly in recent years, reaching 447,000 in 2016.

4. In 2016, the scale of China's hemodialysis market reached RMB 33.5 billion, and it is expected to exceed RMB 35 billion in 2017.

5. In 2016, the global dialysis services market (including hemodialysis drugs) was valued at approximately $62 billion, while the market for dialysis products such as dialysis machines was valued at approximately $14 billion. The dialysis services market is significantly larger than the dialysis products market.

6. According to CNRDS registration data, there were 4,089 hemodialysis centers and approximately 1,100 peritoneal dialysis centers in China in 2016. Expert projections indicate that as the dialysis penetration rate continues to rise, China will require approximately 10,000 hemodialysis centers.

7. The budget for an independent hemodialysis center with a minimum configuration of 20 units is approximately RMB 4–5 million.

Below is Part I of the excerpt from the “Industry Report on Private Independent Hemodialysis Centers,” which primarily outlines the industry chain of the hemodialysis sector and analyzes its market potential. Part II will be released subsequently. Instructions for accessing the full report are provided at the end of this article.

I. Dialysis Treatment for Patients with ESRD

There are three treatment options for patients with end-stage renal disease (ESRD): hemodialysis, peritoneal dialysis, and kidney transplantation. Although kidney transplantation has the lowest average annual cost, due to the scarcity of donor kidneys, patients generally rely on hemodialysis and peritoneal dialysis to sustain life or as a bridge to transplantation.

1.1 Principles of Hemodialysis and Peritoneal Dialysis

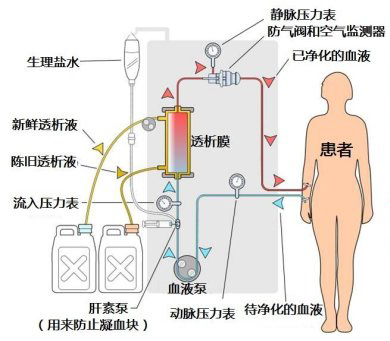

Hemodialysis involves diverting blood from the body to an extracorporeal circuit, where metabolic wastes are removed, electrolyte and acid-base balance is maintained, and excess fluid is eliminated through osmosis, diffusion, and ultrafiltration across a semipermeable membrane within the dialyzer, driven by concentration gradients of solutes on either side. The purified blood is then returned to the patient’s body.

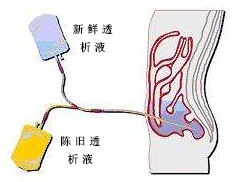

Peritoneal dialysis is a form of dialysis that utilizes the patient’s own peritoneum as a semipermeable membrane. The dialysate infused into the peritoneal cavity exchanges solutes and water with plasma components in the capillaries on the other side of the peritoneum, thereby removing retained metabolic waste products and excess fluid from the body, while simultaneously replenishing essential substances through the dialysate.

1.2 Advantages and Disadvantages of Hemodialysis and Peritoneal Dialysis

Hemodialysis and peritoneal dialysis differ in their principles, each with its own advantages and disadvantages. Both modalities partially or fully substitute for kidney function by removing toxins and excess fluid from the body. Neither dialysis method holds an absolute advantage over the other; however, peritoneal dialysis requires fewer consumables and entails less reliance on healthcare institutions, resulting in insufficient incentive for hospitals to promote its development.

In today’s era of relatively advanced medical technology, both dialysis modalities yield comparable therapeutic outcomes. In terms of overall costs, peritoneal dialysis incurs lower total expenses and demonstrates greater socio-economic benefit. The choice of treatment modality for patients is largely determined by health insurance policies. For instance, over the 50-year history of dialysis in the United States, the ratio of patients undergoing hemodialysis versus peritoneal dialysis has fluctuated significantly, primarily due to differences in reimbursement mechanisms and coverage rates. Therefore, the selection of dialysis modality is heavily influenced by policy factors.

1.3 Global Market Share of Hemodialysis and Peritoneal Dialysis

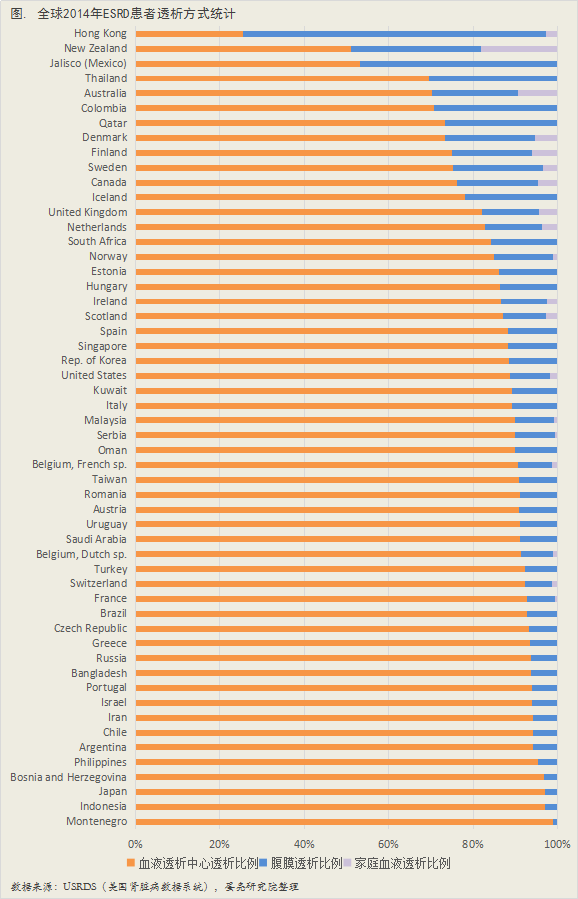

Currently, the majority of patients with end-stage renal disease (ESRD) in most countries worldwide primarily undergo hemodialysis, with the ratio of hemodialysis to peritoneal dialysis patients being approximately 9:1. According to 2014 data published by the United States Renal Data System (USRDS), a small number of countries and regions, including Mexico, Hong Kong, New Zealand, and Thailand, predominantly utilize peritoneal dialysis. This is because these regions guide patients’ choice of dialysis modality through insurance reimbursement policies after comprehensively considering economic costs. For instance, Hong Kong implements a “peritoneal dialysis first” policy; unless contraindications necessitate hemodialysis, patients must initially choose peritoneal dialysis; otherwise, the treatment will not be covered by medical insurance.

II. The Market Potential in the Hemodialysis Service Sector Is Substantial

How Large Is the Hemodialysis Market? In a previous article, VCBeat pointed out that there are approximately 2 million patients with end-stage renal disease (ESRD) in China, and the theoretical market size for hemodialysis is around RMB 150 billion.

2.1 Estimation Method for ESRD Patient Data in China

Currently, there are no accurate statistical data on ESRD patients in China. In all reports related to hemodialysis services,Estimates of the number of patients with end-stage renal disease (ESRD) in China are all derived from data published in the 2012 Lancet article “Prevalence of chronic kidney disease in China: a cross-sectional survey” by scholars including Zhang Luxia and Wang Haiyan.

This project was a nationwide cross-sectional study on the prevalence of chronic kidney disease, involving 13 provinces, municipalities, and autonomous regions across China, and funded by the National Key Technology R&D Program of the Ministry of Science and Technology during the 11th Five-Year Plan period.

This study, conducted over a four-year period from January 2007 to October 2010, surveyed 50,550 adult residents aged 18 and above across China for chronic kidney disease (CKD). The final conclusion indicated that the prevalence of CKD among Chinese adults was 10.8%, affecting a total of up to 120 million people, which means that on average, one in every ten adults suffers from chronic kidney disease. However, the awareness rate was only 12.5%, making it highly susceptible to deterioration.

The aforementioned study determined the prevalence and absolute number of chronic kidney disease (CKD) patients among Chinese adults. In contrast, the number of patients with end-stage renal disease (ESRD) was estimated based on survey statistics from the United States. According to ESRD statistical data from the United States Renal Data System (USRDS), 1.5% of chronic kidney disease cases progress to end-stage renal disease.Therefore, current market research reports on hemodialysis services in China all use this data and ratio to estimate that the number of ESRD patients in China approached 2 million in 2014 and will reach 3.15 million by 2030.

2.2 Market Size Is Closely Linked to Treatment Rates

VCBeat estimates the hemodialysis market to be worth RMB 150 billion, assuming that all 2 million patients with end-stage renal disease (ESRD) undergo hemodialysis.Treatment, derived from data indicating an annual treatment cost of RMB 75,000. However, in reality, the treatment rate for patients with end-stage renal disease (ESRD) does not reach 100%.China’s average dialysis treatment rate is less than 20%, significantly lower than that of other countries and regions. The global average dialysis treatment rate stands at 37%, while in developed countries and regions such as Europe and the United States, the rate has reached 90%.

The size of the hemodialysis market is closely tied to the hemodialysis treatment rate.

China has a very low treatment rate for end-stage renal disease (ESRD), with patients having an average survival period of only 2.5 years, significantly lower than the 7-year survival rate achieved with standardized treatment. However, as residents' paying capacity increases and health insurance coverage expands, China's hemodialysis treatment rate is rising substantially, with a rapid increase in the number of patients receiving hemodialysis, indicating considerable room for growth.

2.3 Data on Dialysis Patients in China

In China, although the number of patients with end-stage renal disease (ESRD) is estimated, there are accurate statistics on the number of individuals undergoing hemodialysis treatment.

Since May 1, 2010, the Ministry of Health has required all medical institutions to log into the “China National Renal Data System” (CNRDS)—established under the leadership of Academician Chen Xiangmei, Chair of the Chinese Society of Nephrology—to submit case information within three days after completing each hemodialysis treatment. The implementation of this system not only facilitates refined and informatized management of hemodialysis and promotes quality improvement in hemodialysis care, but also provides substantial data support for nephrology research and the formulation of medical insurance policies in China.

According to CNRDS statistics, the number of hemodialysis patients in China has increased significantly in recent years, reaching 447,000 in 2016.The growth potential in the hemodialysis market primarily stems from two aspects. First, an increase in the proportion of dialysis patients (expansion of the existing market), and second, a year-on-year rise in the number of end-stage renal disease (ESRD) patients (growth of the incremental market).Based on this calculation, China's hemodialysis market reached RMB 33.5 billion in 2016 and is projected to exceed RMB 35 billion in 2017.

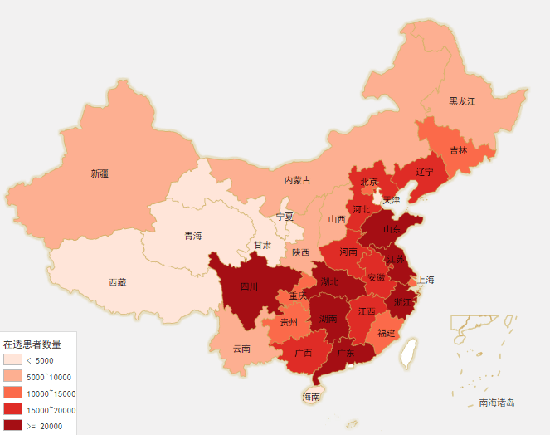

Hemodialysis patients in China are distributed across all provinces and municipalities (excluding Hong Kong, Macao, and Taiwan). The four provinces with the highest patient numbers—Zhejiang, Jiangsu, Guangdong, and Hunan—each have more than 30,000 patients, while Tibet has the lowest number, with only 49 patients. Other provinces with more than 20,000 patients include Shandong, Anhui, Hubei, and Sichuan. This map can serve as a reference for determining which provinces should prioritize the establishment of future hemodialysis centers.

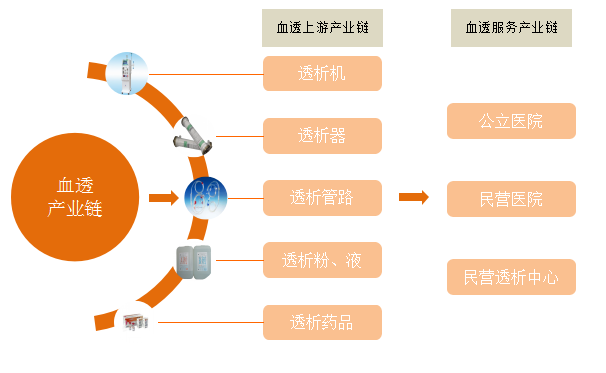

III. Hemodialysis Industry Chain

3.1 Hemodialysis Industry Chain

The hemodialysis-related industry chain is divided into three segments: (1) dialysis equipment and consumables, (2) dialysis pharmaceuticals, and (3) dialysis services. These three segments account for 45%, 25%, and 30% of total costs, respectively.

Dialysis EquipmentEquipment and consumables include dialysis machines, dialyzers, and dialysis tubing. Dialysis machines represent an upfront one-time investment; the market is dominated by foreign brands, with domestically produced products accounting for approximately 15% of the market share, and import substitution is accelerating continuously. As a core consumable, dialyzers have the highest technical barriers, with major brands being imported and holding a 70% market share. However, some domestic companies, such as Weigao and Langsheng, are gradually breaking through these technical barriers and expanding production capacity, further accelerating the pace of import substitution.

Hemodialysis medications consist of erythropoietin (EPO) and heparin, while dialysate solutions and powders are also regulated as pharmaceutical products. EPO is used during dialysis to stimulate red blood cell production and address anemia. Heparin, an anticoagulant, prevents blood coagulation that may occur extracorporeally during dialysis. Currently, hemodialysis medications have largely achieved domestic production in China.

Dialysis service fees cover the costs of hemodialysis services, including not only the cost and depreciation of dialysis equipment and consumables, but also bed charges and medical personnel labor costs. Currently, there are still many untapped market segments in China’s dialysis service sector, with the industry in a phase of rapid expansion and market share acquisition.

3.2 Hemodialysis Manufacturing Process

3.2.1 Dialysis Machine

Hemodialysis machines are the most widely used therapeutic devices in blood purification therapy. They are relatively complex electromechanical systems, consisting of a dialysate supply and monitoring unit and an extracorporeal circuit monitoring unit.

3.2.2 Dialyzer

Dialyzers, also known as “artificial kidneys,” are composed of hollow fibers made from chemical materials, with countless microscopic pores distributed along each fiber. During dialysis, small-molecule solutes and water in the blood and dialysate exchange across these pores in the hollow fibers.

3.2.3 Dialysis Tubing

Dialysis tubing refers to the extracorporeal circuit tubing connected to the hemodialyzer, consisting of a set of arterial lines and a set of venous lines; the red connector indicates the arterial end, and the blue indicates the venous end. It is manufactured from medical-grade materials such as PVC, PP, and flame-retardant PE.

3.2.4 Dialysate/Powder

Dialysate is prepared by diluting a dialysis concentrate containing electrolytes and buffer agents with reverse osmosis water in a specified ratio, ultimately forming a solution with electrolyte concentrations similar to those of blood. This helps maintain normal electrolyte levels while providing buffer bases to the body through a higher buffer concentration, thereby correcting acidosis in patients. The primary buffer agent used in dialysate is bicarbonate, with a small amount of acetate also included.

3.2.5 Water Treatment System

During a single dialysis session, the patient’s blood is exposed to a large volume of dialysate (120 L) across the dialysis membrane. Since municipal tap water contains various trace elements, particularly heavy metals, as well as disinfectants and bacteria, direct contact with blood would allow these substances to enter the body. Therefore, tap water must undergo sequential treatment processes, including filtration, iron removal, softening, activated carbon adsorption, and reverse osmosis. Only reverse osmosis (RO) water is suitable for diluting concentrated dialysate.

3.2.6 Dialysis Drugs

Medications for hemodialysis primarily include erythropoietin (EPO) and heparin, as well as vitamin D, antihypertensive agents, and antidiabetic drugs.

3.3 Hemodialysis Service Process

3.3.1 The Hemodialysis Services Market Offers Substantial Growth Potential

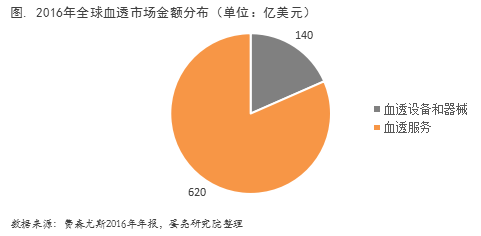

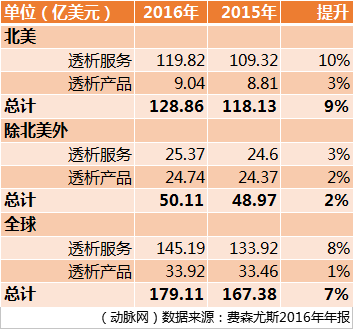

According to data from Fresenius’ 2016 annual report, the market size for dialysis equipment is limited.In 2016, the global dialysis services market (including hemodialysis drugs) was valued at approximately $62 billion, and it is projected to reach $95 billion by 2030. The total market value of dialysis products, such as dialysis machines, was around $14 billion in 2016. The market for hemodialysis services is significantly larger than that for hemodialysis products.

In regions with well-developed dialysis services, such as North America and Europe, the market for dialysis equipment sales has become saturated, with the primary growth market now located in Asia. According to Fresenius's annual report, Fresenius Medical Care (FMC), the company responsible for hemodialysis products and services, generated only $904 million in revenue from dialysis equipment and supplies in the North American market in 2016, while its dialysis service revenue reached $11.982 billion.Globally, FMC’s dialysis services revenue accounted for 81% of the company’s total revenue.It also demonstrates that the market for hemodialysis services is significantly larger than that for hemodialysis products.

3.3.2 There is still a significant shortage of dialysis centers in China

According to the current registration data from CNRDS, there were 4,089 hemodialysis centers and approximately 1,100 peritoneal dialysis centers in China in 2016.And according to expert predictions,As the dialysis penetration rate in China continues to rise, there will be a need for approximately 10,000 hemodialysis centers, indicating substantial market growth potential.

Currently, hemodialysis centers in China are categorized into three types.

First, there are hemodialysis centers established within hospitals. This is currently the mainstream model for hemodialysis centers in China, encompassing both public and private hospitals, and accounting for over 97% of the total. These centers primarily cater to the needs of patients with acute conditions, critical illnesses, and those requiring hospitalization.

Second is the chain hemodialysis center model. This is the model for hemodialysis center development that needs to be vigorously promoted in the future, and it is also the mainstream model in North America and Europe. Chain hemodialysis centers are established near communities to meet the dialysis service needs of the vast majority of patients with end-stage renal disease (ESRD), facilitating convenient access to nearby dialysis and helping patients reintegrate into society.

Third, independent hemodialysis centers separate from hospitals. In essence, this type of hemodialysis center operates under the same model as chain hemodialysis centers, except that it has not yet achieved chain-scale operations.

VCBeat Research Institute has learned that the budget for an independent hemodialysis center with a minimum configuration of 20 units is approximately RMB 4–5 million. The detailed breakdown includes: an investment of about RMB 2.5 million for 20 hemodialysis machines and one water treatment system; renovation costs of RMB 0.5–1 million (calculated at a construction cost of RMB 1,000 per square meter for a center spanning 500–1,000 square meters); approximately RMB 300,000 for auxiliary medical facilities, furniture, and appliances; around RMB 200,000 for emergency vehicles; and roughly RMB 500,000 for other expenses, including the procurement of medical consumables, personnel, medical waste disposal, hygiene, safety, and fire protection.

IV. China Vigorously Relaxes Policies Related to Hemodialysis Centers

4.1 High-Reimbursement Coverage for Dialysis Costs under Medical Insurance

In August 2012, six ministries and commissions jointly issued the “Guiding Opinions on Launching Critical Illness Insurance for Urban and Rural Residents,” introducing critical illness insurance to further improve the medical security system for urban and rural residents, establish a multi-tiered medical security framework, and address the problems of poverty caused or exacerbated by illness. Rather than simply defining critical illnesses by specific disease types, the document determines eligibility based on a comparison between the high medical expenses incurred from critical illnesses and the economic burden-bearing capacity of urban and rural residents. In principle, the higher the expenses, the higher the reimbursement rate. The “Guiding Opinions” explicitly include end-stage renal disease (uremia) in the critical illness insurance compensation policy, with a reimbursement rate of no less than 50% for the actual out-of-pocket portion.

In February 2014, the Office of the State Council Leading Group for Healthcare Reform issued a notice on accelerating the implementation of critical illness insurance for urban and rural residents, to implement the requirements of the "Guiding Opinions on Launching Critical Illness Insurance for Urban and Rural Residents," and fully launched pilot programs for critical illness insurance for urban and rural residents in 2014. After being included in the critical illness coverage system, the reimbursement rate for end-stage renal disease reached 90%, which helps significantly reduce the financial burden and extend patients' survival periods. Meanwhile, the demand for dialysis will be rapidly unleashed, indicating huge market growth potential.

4.2 Gradual Deregulation of Hemodialysis Centers

As the financial burden on hemodialysis patients continues to decrease, the demand for hemodialysis treatment is being rapidly unleashed. Since 2014, the government has been gradually lowering the requirements for establishing independent hemodialysis centers, encouraging social capital to enter the field of hemodialysis centers and promoting their development toward chain-based and group-oriented models.

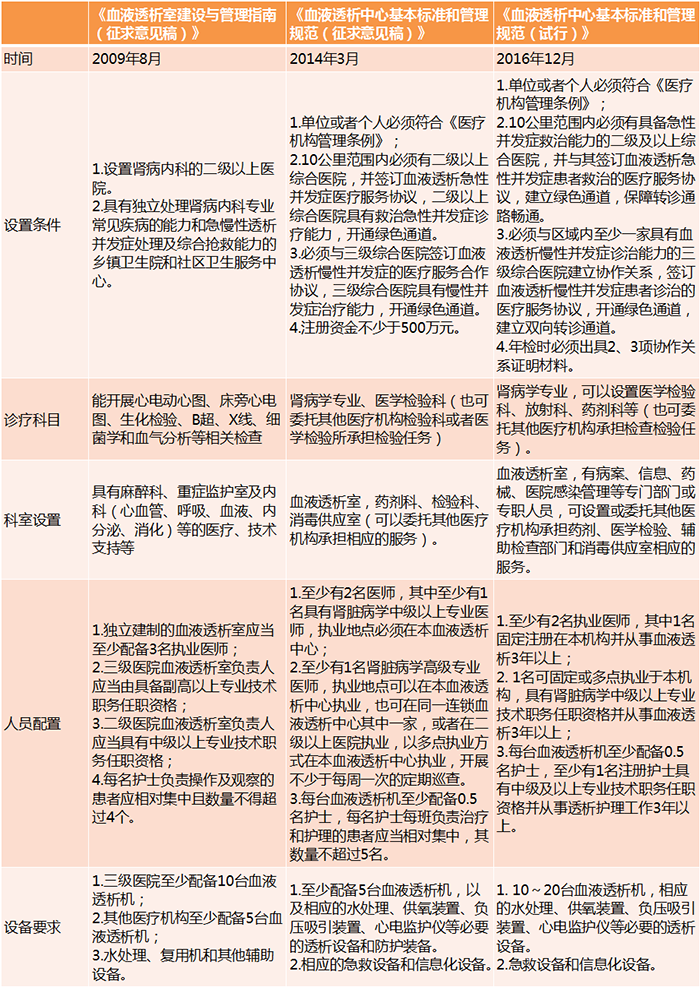

In August 2009, the Department of Medical Administration of the Ministry of Health released the “Guidelines for the Establishment and Management of Hemodialysis Centers (Draft for Comments)” to guide and strengthen the standardized construction and management of hemodialysis centers in medical institutions.

In March 2014, the Medical Administration Bureau of the National Health and Family Planning Commission issued the “Letter on Soliciting Opinions on the Basic Standards and Management Specifications for Hemodialysis Centers,” drafting the standards and management specifications for the establishment of hemodialysis centers. Subsequently, several provinces successively released policies to encourage the development of independent hemodialysis centers.

In November 2016, the National Health and Family Planning Commission issued the “Decision on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions (Draft for Comments),” which already listed “hemodialysis centers” as a routine category of medical institutions under Article 3, Item (10).

In December 2016, the National Health and Family Planning Commission issued the "Basic Standards and Management Specifications for Hemodialysis Centers (Trial)," which stipulates that a hemodialysis center must be equipped with at least 10 to 20 hemodialysis machines and have at least two licensed physicians.

V. Case Study of a North American Chain of Hemodialysis Centers

The business model of chain hemodialysis centers has long been validated abroad. Currently, the two largest global chains in hemodialysis services are Fresenius and DaVita, which together account for 75% of the U.S. hemodialysis services market. Fresenius is the leading global brand in hemodialysis equipment, with a very high market share for its dialysis machines and consumables. In addition to its dominant position across the hemodialysis industry chain, Fresenius also holds a substantial share of the hemodialysis services market in Europe and the United States. DaVita, by contrast, provides only hemodialysis services; it is a company that captures a significant share of the North American hemodialysis services market despite having no proprietary line of hemodialysis products.

5.1 Fresenius

FeeFresenius Group was founded in 1912 and is headquartered in Bad Homburg, Germany. The Fresenius Group comprises several major subsidiaries, including Fresenius Medical Care (commonly referred to as FMC), a healthcare company that provides dialysis products and services, medical care, and home healthcare for patients. In addition to manufacturing a full range of dialysis equipment and consumables, Fresenius owns and operates a chain of dialysis centers worldwide. This vertical integration grants Fresenius a cost advantage in operating outpatient dialysis centers, as its equipment and consumables are produced in-house.

In Fresenius Group’s annual report, FMC’s total revenue in 2016 amounted to $17.911 billion; after excluding sales revenue from dialysis products, its dialysis services revenue was $14.519 billion, comparable to DaVita, a company engaged solely in dialysis services.The turnover figures are quite close. In North America, sales of dialysis machines and other dialysis products are very low, amounting to only $904 million—a mere fraction of dialysis service revenue—due to market saturation of dialysis centers. In markets outside North America, however, revenues from dialysis products and dialysis services are comparable. Globally, FMC’s dialysis service revenue far exceeds its sales of dialysis products, which explains why medical device manufacturers leverage their technological and cost advantages to enter the hemodialysis healthcare services sector.

FMC operates 3,624 clinics across 45 countries worldwide, with a strategic focus on the North American market. Among these, there are 2,306 dialysis centers in the United States, 711 in Europe, the Middle East, and Africa (EMEA), 233 in Latin America, and 374 in the Asia-Pacific region, representing a 6% increase in the number of centers compared to 2015. In 2016, FMC held a 38% market share in the United States, providing dialysis services to approximately 185,000 patients with end-stage renal disease (ESRD). Together with DaVita, they accounted for 75% of the U.S. market (note: this figure slightly differs from DaVita’s annual report, which states that DaVita and FMC each held a 36% share, totaling 72%).

5.2 DaVita

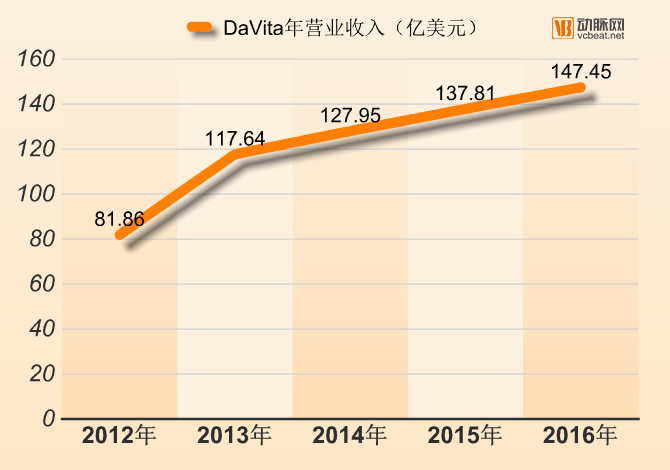

DaVita Inc. is a U.S.-based company that provides dialysis and related laboratory services to patients with end-stage renal disease (ESRD). As of December 31, 2016, DaVita operated 2,350 affiliated dialysis centers in the United States. In addition to its U.S. operations, DaVita had 154 dialysis centers worldwide, primarily located in Southeast Asia, with Malaysia having the largest number, totaling 38 facilities.

Source: DaVita 2016 Annual Report

In 2016, DaVita’s total revenue comprised $9.138 billion from dialysis and related laboratory services, $4.114 billion from DMG healthcare services, and $1.621 billion from other ancillary services and strategic initiatives. After deducting negative segment revenues, the consolidated net revenue amounted to $14.745 billion.

Data from DaVita indicates that the average cost to establish a new chain hemodialysis center is $2.8 million, with upfront costs covering leasing, renovation, equipment, and one year of operating capital. These centers typically open within one year of signing the property lease agreement, achieve profitability in the second year following Medicare certification, and recoup their investment within three to five years.

VI. Case Studies of Independent Hemodialysis Centers in China

Currently, there are approximately 4,000 registered hemodialysis centers in China, while only about 20 companies and institutions offering independent or chain-based hemodialysis services are currently in the pilot phase.

The pioneers that first ventured into this field have developed crucial insights and perspectives on the industry after a period of growth. VCBeat interviewed the heads and senior executives of several companies that were early entrants in China’s independent hemodialysis center sector, capturing their views on the experiences, lessons learned, and challenges faced by private enterprises in this space. Therefore, this chapter represents the core essence of this report.

VCBeat Institute, through interviews, presents the following case studies in this report:

6.1 Bethune Blood Purification Center

In 2010, the Ministry of Health authorized the Bethune Foundation to launch a pilot program for establishing non-profit chain hemodialysis medical services in communities and at the grassroots level. Beijing Dakang Medical Investment Co., Ltd. actively undertook the investment, operation, and management of the project. Dakang Medical established the non-profit chain “Bethune Blood Purification Centers,” and has invested in and constructed more than 50 hemodialysis service centers in central regions, including Henan, Hebei, Shandong, and Jiangxi provinces.

6.2 AiShen Medical

Aishen (Hainan) Medical Technology Co., Ltd. is a venture co-founded by Jie Renxiang, former Vice General Manager of Weigao Blood Purification Group, along with Gao Xing and Zhang Yongqiang. Jie Renxiang serves as CEO, Gao Xing as CFO, and COO Zhang Yongqiang oversees the construction and operation of offline dialysis centers. In addition to Aishen.com, which focuses on chronic kidney disease management, Aishen Medical has applied for licenses for three nephrology hospitals and three dialysis centers in Hainan, Yunnan, and Guangdong provinces. Among these, two nephrology hospitals and one dialysis center have already been approved. The first specialized nephrology hospital is expected to officially open in August.

6.3 Shengrenkang Medical Group

In the 1990s, the founder of Shengrenkang Medical Group (Chengdu Kangyi Mingren Medical Investment Management Co., Ltd.) started out in Nanchong, Sichuan, with just two hemodialysis machines. After more than a decade of development, the company began to expand its layout after receiving investment from international capital such as OrbiMed in 2016. Currently, it holds controlling stakes in 12 primary and secondary hospitals, with its main medical services focusing on the treatment of kidney diseases and hemodialysis.

These 12 hospitals are primarily located in Sichuan Province, with a strategic presence across Southwest and Northwest China, collectively operating more than 400 dialysis machines. The flagship facility, Chengdu Gaoxin Boli Hospital, covers an area of over 6,000 square meters and is equipped with 73 hemodialysis machines. Following the relaxation of regulatory policies, Shengrenkang will establish several independent hemodialysis centers in regions such as Sichuan, Xi’an, and Wuhan, centered around hub hospitals like Boli Hospital, to penetrate areas with inadequate medical services. These independent hemodialysis centers will provide dialysis treatments, while the hub hospitals will deliver comprehensive medical care. Furthermore, Shengrenkang Group places greater emphasis on technological advancement and cutting-edge innovation, targeting genetic engineering as the ultimate solution for hemodialysis in the future. The group will also pursue further advanced development in smart healthcare and genetic technologies.

6.4 Chongqing Aokailong

Chongqing Aikailong primarily serves the blood purification sector, offering a comprehensive portfolio that includes hemodialysis machines, water treatment systems for hemodialysis, hemodialysis consumables, and continuous renal replacement therapy (CRRT) systems. The company integrates research and development, production and sales, medical services, and healthcare informatics. Aikailong’s core products include: hemodialysis machines, hemodiafiltration machines, CRRT systems, and hemoperfusion machines; water treatment systems for hemodialysis, pure water equipment for sterile supply departments, pure water equipment for clinical laboratories, and centralized medical pure water systems; as well as laboratory ultrapure water systems. In recent years, Aikailong has expanded into the hemodialysis medical services sector, with 16 hemodialysis service centers already in operation or under preparation.

6.5 Xiao Jing Dialysis Beijing Huansheng Medical Investment Co., Ltd.

Xiaojing Dialysis was established by Beijing Huansheng Medical Investment Co., Ltd., which evolved from the medical division of Shenyang Sunshine Pharmaceutical. Huansheng Medical currently operates ten hemodialysis centers, primarily located in second- and third-tier cities across Hebei, Liaoning, Hunan, and Hubei provinces. On one hand, it has built independent hemodialysis centers equipped with approximately 20 dialysis machines and basic nephrology departments. On the other hand, it has developed secondary hospitals adopting a “specialized-focused, general-support” model, with nephrology specialty hospitals and hemodialysis centers as their core services.

In addition to the above cases, VCBeat Research has also compiled information on private independent hemodialysis centers established by the following companies based on publicly available data:

>>>>

6.6 Shandong Weigao Group

6.7 Chongqing Sunway Blood Purification Technology Co., Ltd.

6.8 Shandong Xinhua Medical Instrument Co., Ltd.

6.9 Hebei Changshan Biochemical Pharmaceutical Co., Ltd.

6.10 Guangdong Biolight Meditech Co., Ltd.

6.11 Ningbo Changsheng Medical Investment Management Co., Ltd.

6.12 Shanghai Deheng Hospital Investment Management Co., Ltd.

6.13 Other Opportunities in the Dialysis Industry Chain

Management Software

Dialysis centers require a hemodialysis management system, a peritoneal dialysis management system, and a nephrology medical record database management system to achieve patient operations management, comprehensive tracking of the dialysis process, healthcare staff management, and pharmaceutical and consumable inventory management.Patient operations management, comprehensive tracking of the dialysis process, medical staff management, inventory management of pharmaceuticals and consumables, and big data analytics. Hospitals with such needs can also integrate with hardware devices at hemodialysis centers—including hemodialysis machines, scales, blood pressure monitors, and water treatment systems—as well as with information systems such as HIS, LIS, PACS, and EMR, to enable more efficient management.

Representative Companies:

Beijing Infome Information Technology Co., Ltd. offers i-DiaPro Hemodialysis Electronic Medical Records and i-DiaPro Blood Purification Quality Control System.

Shenzhen Jingyunsu Information Technology Co., Ltd. The product is the Yunjing System.

Chronic Disease Management

Chronic kidney disease (CKD) is a highly significant condition among chronic diseases, featuring dedicated chronic disease management platforms and patient education communities, similar to those for diabetes and hypertension. By leveraging mobile internet technology and integrating CKD patients’ living environments with clinical data, precise and humanized full-cycle services are provided to patients with chronic kidney disease. Hemodialysis patients, who undergo long-term dialysis treatment, also utilize specialized management software to monitor various health indicators.

Representative Companies:

Beijing Yingfumei Information Technology Co., Ltd. The product is the nephrology follow-up system, Cashew Doctor.

Shanghai Ailipi Information Technology Co., Ltd. (iKidney Medical), with its product being iKidney Network.

Chengdu Shengrenkang Network Technology Co., Ltd., with its product being Xiaoyu.

References:

"Blood Purification Industry: In-Depth Report - Dialysis Service Policies Gradually Liberalized, Ushering in the Golden Age of Blood Purification", Guohai Securities

"Dialysis Industry: Special Research – 'Kidney' Beyond Control, Boundless Purification", Guosen Securities

《In-Depth Research Report Series on “Hemodialysis”》, Heda Capital

This industry report on the hemodialysis sector, titled “Report on the Private Independent Hemodialysis Center Industry,” constructs an industrial landscape of the hemodialysis market from both policy and market perspectives. It also provides investment directions for the hemodialysis market, offering a channel for professionals within and outside the industry to gain insights into the hemodialysis market and inviting all stakeholders to explore the various possibilities for the future development of the hemodialysis industry.

Scan the QR code below to become an official VCBeat member and gain access to the full version.《"Report on the Private Independent Hemodialysis Center Industry". Furthermore, over the coming year, you will have unlimited access to the completeIndustry Trend Report, timely grasp the latest globalInvestment and Financing Information, boasting a comprehensiveMedical Enterprise Database, andMassive Resource Integration。

Scan the QR code to become a VCBeat member,

Beta Version Trial Price: 365 Yuan/Year.