Pioneering Independent Hemodialysis Centers in China: Industry Insights and Firsthand Perspectives from Early Entrants

In the "Report on the Private Independent Hemodialysis Center Industry," recently released by VCBeat and Eggshell Research Institute, we analyze the industrial landscape of the hemodialysis market from both policy and market perspectives. Additionally, we provide investment directions for the hemodialysis market, offering a channel for industry insiders and outsiders to understand this sector.

VCBeat · Eggshell Research Institute reviewed domestic and international industry data and interviewed the heads of several leading private independent hemodialysis service providers in China., gained first-hand information on independent hemodialysis centers in China.Based on two months of interviews and data compilation, VCBeat has completed this report. This article distills insights from industry experts and summarizes key considerations for establishing independent hemodialysis centers.

1.According to CNRDS statistics, the number of hemodialysis patients in China has increased significantly in recent years, reaching 447,000 in 2016.

2.According to CNRDS registration, there were 4,089 hemodialysis centers and approximately 1,100 peritoneal dialysis centers in China in 2016. Based on expert projections, as the dialysis penetration rate continues to rise, China will require approximately 10,000 hemodialysis centers.

3. The budget for an independent hemodialysis center with a minimum configuration of 20 machines is approximately RMB 4–5 million.

4. Independent hemodialysis centers can adopt a co-construction model with hemodialysis machine manufacturers to significantly reduce upfront capital investment.

5. Independent hemodialysis centers, though small in scale, are fully equipped. Their construction should take into account various medical and non-medical factors, including environmental protection, infection prevention and control, and clinical facility configuration.

6. For independent hemodialysis centers to achieve long-term development, they must consider integrating with nephrology medical services.

Special thanks to the following industry professionals for their support of VCBeat.

Chen Shaobo, Chairman of Beijing Dakang Medical Investment Co., Ltd.

Aishen Medical COO Zhang Yongqiang

Cheng Shaokai, Executive Director of Beijing Huansheng Medical Investment Co., Ltd.

Chen Shi, VP of Shengrenkang Medical Group

Chongqing Aokailong Medical Technology Co., Ltd. General Manager and Board Secretary Jia Bei

Wang Wei, CEO of Beijing Infomed Information Technology Co., Ltd.

Guangdong Weigao Blood Purification Medical Technology Co., Ltd. Executive Director Su Yuanbin

Below is an excerpt from the report, featuring interviews with pioneers in China’s private independent hemodialysis industry. To access the full report, please become a VCBeat member and download it.

Case Study Interviews on Independent Hemodialysis Centers in China

Currently, there are approximately 4,000 registered hemodialysis centers in China, while only about 20 companies and institutions are piloting independent or chain-based hemodialysis services.

Pioneering enterprises in this field, after a period of development, have gained crucial insights and perspectives on the industry. VCBeat interviewed the leaders and senior executives of several companies that were among the early players in China’s independent hemodialysis center sector, to discuss their experiences, lessons learned, and challenges encountered as private enterprises operating in this field.Therefore, this chapter also represents the essence of this report.

Based on interviews, the case analyses presented in this report by VCBeat are as follows:

Bethune Blood Purification Center

In 2010, the Ministry of Health authorized the Bethune Foundation to launch a pilot program for establishing non-profit chain hemodialysis medical services in communities and at the grassroots level. Beijing Dakang Medical Investment Co., Ltd. actively undertook the investment, operation, and management of the project. Dakang Medical established the non-profit chain “Bethune Blood Purification Centers,” and has invested in and built more than 50 hemodialysis service centers in central regions such as Henan, Hebei, Shandong, and Jiangxi provinces.

In 2010, the Ministry of Health authorized the Bethune Foundation to launch a pilot program for establishing non-profit chain hemodialysis medical services in communities and at the grassroots level. Beijing Dakang Medical Investment Co., Ltd. actively undertook the investment, operation, and management of the project. Dakang Medical established the non-profit chain “Bethune Blood Purification Centers,” and has invested in and built more than 50 hemodialysis service centers in central regions such as Henan, Hebei, Shandong, and Jiangxi provinces.

Chen Shaobo, Chairman of Beijing Dakang Medical Investment Co., Ltd.

Vice Chairman of the Bethune Public Welfare Foundation, Vice Chairman of the Nephrology and Dialysis Professional Committee of the China Non-Public Medical Institutions Association, Chairman of Beijing Dakang Medical Investment Co., Ltd., and Founder of Independent Chain Hemodialysis Centers.

The First to Launch the Independent Hemodialysis Center Project

In 2010, in accordance with the principles of healthcare system reform, the then Ministry of Health commissioned the “Bethune Fund Management Committee” to launch pilot programs for non-profit chain hemodialysis medical services in selected provinces and municipalities across China, with a particular focus on the central and western regions, bringing services into communities and grassroots levels. Beijing Dakang Medical Investment Co., Ltd. actively undertook this initiative.investment, operation, and management of the project.

In June 2011, Dakang’s Bethune Hemodialysis Center was established in Shandong Province. At that time, the Ministry of Health approved six private hemodialysis centers in Shandong, with three established by Dakang in the Jiaodong Peninsula and three by Weigao, a publicly listed company, in Weihai. Subsequently, Dakang successively set up dozens of hemodialysis centers in Jiangxi, Shanxi, Hebei, Fujian, Hubei, and Guangdong provinces.

Analysis of the Hemodialysis Market

At the time Dakang Company launched its project, it conducted a nationwide survey of the hemodialysis market in China, estimating the number of dialysis patients at 160,000. In recent years, due to increased government attention to critically ill patients and the promotion of major disease medical insurance policies, a significant portion of dialysis costs has become reimbursable under medical insurance. As a result, by the end of 2016, the number of patients receiving blood purification therapy had exceeded 500,000. Given the variation in charging standards across different regions in China, the annual cost of hemodialysis for patients with end-stage renal disease ranges from RMB 70,000 to RMB 100,000. Multiplying this by the 500,000 hemodialysis patients yields an existing market size estimated at RMB 35 billion to RMB 50 billion.

Based on the dialysis prevalence rates in Japan and Taiwan, China should have two to three million dialysis patients. However, due to the uneven distribution of dialysis resources, less comprehensive health insurance policies, and patients’ limited ability to pay, the proportion of patients receiving continuous dialysis services has not yet reached the high levels seen in Japan and Taiwan. Nevertheless, with advancements in medical technology, the expansion of hemodialysis centers into lower-tier markets, and improvements in health insurance coverage, the proportion of end-stage renal disease (ESRD) patients undergoing hemodialysis is expected to continue rising, leading to a sustained increase in the number of hemodialysis patients in China.

Issues Prior to Policy Liberalization

Chen Shaobo explained that prior to the introduction of policies establishing standards for independent hemodialysis centers, the primary obstacle constraining the development of private enterprises was qualification requirements. Each dialysis center was required to obtain an independent license as a nephrology hospital. Furthermore, every newly established hemodialysis service site needed to secure two additional qualifications: medical and nursing practice licenses, and designated provider status for both Urban Employee Basic Medical Insurance and the New Rural Cooperative Medical Scheme. Obtaining these qualifications required approval from local health administrative authorities.

Chen Shaobo stated that under the original policies of the health authorities, medical institutions were required to operate for more than one year before applying for designated status under the Urban Resident Basic Medical Insurance and the New Rural Cooperative Medical Scheme. Since patients seeking reimbursement would inevitably choose institutions with such designated status, private hemodialysis centers had to remain operational without this designation for a year before becoming eligible to apply.

Dakang hopes to gain the understanding and support of health authorities and medical insurance departments, so that a special approval can be granted to resolve the issue. Currently, DakangOf the 50 chain medical service centers operated by Kang Medical, more than two-thirds have already been designated as approved providers under China’s basic medical insurance scheme. “This is a pilot initiative promoted by the Ministry of Health to address the difficulties and high costs faced by grassroots patients in accessing dialysis services. During the pilot phase, we encountered numerous challenges, including conflicts with existing policies and regulations, all of which required continuous efforts to overcome and resolve,” said Chen Shaobo.

Participated in the Development of Standards for Independent Hemodialysis Centers in China

Whether private or public, whether chain-operated or independent, hemodialysis centers all serve the purpose of healthcare delivery, aiming to address the inconvenience faced by patients with end-stage renal disease (ESRD) in remote areas when accessing dialysis services. Therefore, from a policy perspective, market access for private capital in the hemodialysis industry will continue to become increasingly open. Dakang Company was the first enterprise to participate in establishing chain hemodialysis centers through private investment and contributed to the formulation of both provincial standards in four provinces and national standards for independent hemodialysis centers, giving it the greatest authority in commenting on the evolution of relevant policies.

In 2010, Dakang Company began piloting the establishment of independent hemodialysis centers. At that time, each center required approval through a four-tier process, ultimately reaching the Ministry of Health. Currently, the establishment of hemodialysis centers only requires approval from the provincial Health and Family Planning Commission, reflecting a continuous liberalization of policy. However, while introducing these policy changes to VCBeat, Chen Shaobo also discussed the limitations of this regulatory relaxation. At the end of last year, the National Health and Family Planning Commission issued regulations for four types of independently established medical institutions. The approval authority for clinical laboratory centers, pathology centers, and medical imaging centers lies at the county or municipal level, whereas the approval authority for hemodialysis centers remains at the provincial level. What is the reason for this distinction?

Because the first three types of institutions primarily serve business-to-business (B-end) clients, only hemodialysis centers directly cater to patients. Hemodialysis is a service prone to medical risks; patients’ conditions can change rapidly during treatment, and infection control requirements are stringent—exceeding those in dentistry, orthopedics, and ophthalmology. Therefore, national policies aim to open up the industry while simultaneously implementing controls to ensure medical safety.

In the industry standards for hemodialysis centers, the national government has established two requirements. The first requires approval by the provincial Health and Family Planning Commission. The second encourages the establishment of chain-based and group-operated dialysis centers, while discouraging individually operated facilities, as individual dialysis service points have poor risk resilience and weak management capabilities.

When Dakang was preparing the provincial standards for hemodialysis centers, it included treatment agreements with hospitals at Level II and above, as well as two-way referral green channel agreements with tertiary hospitals; these provisions were also retained in the national standards. Chen Shaobo believes that the public welfare nature of public hospitals requires them to provide services to patients. China’s three-tier pre-hospital emergency care system also mandates that public hospitals, along with all medical institutions, must not turn away patients.

Therefore, public hospitals cannot refuse to enter into cooperation agreements with hemodialysis centers. However, Chen Shaobo also acknowledged that issues may arise during implementation. When private medical institutions compete with public ones in a market-driven environment, certain unspoken obstacles may emerge.

Currently, there are two models for private hemodialysis centers. The first is a hospital-based model, where nephrology hospitals serve as the primary entity and hemodialysis centers play a supporting role. This approach was adopted because these institutions were previously unable to participate in pilot programs for independent hemodialysis centers, leaving them with no choice but to combine nephrology services with hemodialysis. The second model consists of independent hemodialysis centers, such as Dakang. Chen Shaobo believes that when private capital enters this industry, if investors lack experience in the relevant industrial chain, it is advisable to initially adopt the combined nephrology hospital and hemodialysis center model. Standalone hemodialysis centers entail higher management requirements and greater operational complexity, offer limited profit margins, and yield slower returns on investment.

iKidney Medical

AiShen (Hainan) Medical Technology Co., Ltd. is a venture co-founded by Jie Renxiang, former Vice General Manager of Weigao Blood Purification Group, along with Gao Xing and Zhang Yongqiang. Jie Renxiang serves as CEO, Gao Xing as CFO, and COO Zhang Yongqiang oversees the construction and operation of offline dialysis centers. In addition to AiShen Wang, which focuses on chronic kidney disease management, AiShen Medical has applied for licenses for three nephrology hospitals and three dialysis centers in Hainan, Yunnan, and Guangdong provinces. Among these, two nephrology hospitals and one dialysis center have already received approval, with the first specialized kidney hospital expected to officially open in August.

Zhang Yongqiang, COO of Aishen Medical

In December 2010, the former Ministry of Health approved WEGO Group and the Bethune Foundation Management Committee to launch a pilot program for independent blood purification centers in Shandong Province. At that time, Zhang Yongqiang of Aishen Medical personally witnessed and participated in the development of this hemodialysis center from its inception to full operation. Currently, Zhang Yongqiang is responsible for the construction and operational management of hemodialysis centers at Aishen Medical.

Although Zhang Yongqiang has witnessed the establishment of hemodialysis centers in China from scratch, there is still a need to continuously draw on the experience of more advanced regions. Taiwan currently has the highest proportion of hemodialysis patients worldwide, and the Ai Shen Medical team maintains close ties with hemodialysis centers in Taiwan. According to 2015 statistics, there were over 73,000 patients undergoing hemodialysis treatment in Taiwan, with more than 3,000 dialysis patients per million population.

In 2000, there were only slightly over 30,000 hemodialysis patients in Taiwan, a figure that nearly doubled over the next decade and more. Currently, mainland China has fewer than 450,000 hemodialysis patients, with an average prevalence of less than 400 per million population. In May 2017, Academician Chen Xiangmei released a set of data: according to the 2016 registration from the Chinese National Renal Data System (CNRDS), there were 4,089 hemodialysis centers nationwide, serving 447,435 patients on dialysis, with new cases75,831 cases.

Therefore, Zhang Yongqiang believes that there is still significant room for growth in China’s hemodialysis market. Based on this ratio, the number of hemodialysis patients in mainland China will certainly exceed 2 million in the future, likely reaching 3 to 4 million, and the number of hemodialysis centers should at least double, reaching approximately 10,000.

The rapid development of the hemodialysis market in the Taiwan region can be attributed to three factors. The first factor is health insurance; economic considerations are a primary concern in the field of hemodialysis worldwide. In recent years, Taiwan has implemented National Health Insurance, resulting in a very high proportion of the population receiving hemodialysis. In the 1970s, because health insurance did not cover hemodialysis treatment, the mortality rate among patients with end-stage renal disease (ESRD) was also very high. Following medical system reforms and the implementation of National Health Insurance, coupled with a decline in the cost of hemodialysis, the number of hemodialysis patients experienced rapid growth.

Second, the overall healthcare environment in the Taiwan region, including medical quality, ranks among the top in Asia and even globally, with a large number of community dialysis centers. Zhang Yongqiang provided an example: there are approximately 600 to 700 kidney dialysis centers (i.e., various hemodialysis institutions as we refer to them) across Taiwan. One chain hemodialysis provider, operating around 100 centers, was acquired by an international dialysis chain and subsequently ranked first in dialysis quality within that global network. This demonstrates that the medical quality in the Taiwan region is quite outstanding, particularly in areas such as clinical pathways, patient management, and nutritional guidance.

Third, patient compliance in Taiwan is relatively high. Since dialysis patients spend a significant amount of time outside the hospital, they need to control their fluid intake after dialysis and maintain a low-phosphorus, low-potassium diet. Poor patient compliance would result in a shorter life expectancy. Therefore, these three factors combined have led to Taiwan having the highest dialysis treatment rate globally.

Industry development is heavily influenced by policy.

Independent hemodialysis centers in mainland China are still in their nascent stage. Prior to 2016, approvals for independent hemodialysis centers were granted only sporadically across various provinces. It was not until the official release of national policy documents at the end of 2016 that substantive implementation began. To date, more than 20 enterprises registered with industrial and commercial authorities as being related to hemodialysis centers or hemodialysis clinics can be identified. However, these figures merely reflect business registration; the number of independent hemodialysis centers that have actually obtained practice licenses and signed agreements with medical insurance programs to admit patients remains limited. It is estimated that by the end of this year, more than ten newly established independent hemodialysis centers will commence actual operations.

In 2016, the national government shifted the regulatory framework for designated medical institutions under social health insurance from an approval-based system to a filing-based system. However, it remains difficult to predict the timeline and intensity of policy implementation as it cascades from the central government to local authorities. Currently, execution methods vary across regions; some areas have already begun implementing the central government’s policies, allowing private medical institutions to proceedApplication for inclusion in the national medical insurance scheme. In some regions, local policies have been implemented, whereby newly established medical institutions are granted only a few application windows per year, during which they may submit their applications. Some more conservative provinces continue to adhere to the original approval-based system, which generally requires medical institutions to have been in operation for at least one year and to submit various documentation; inclusion in the medical insurance scheme is then determined based on medical insurance indicators and market share. Given the strong correlation between hemodialysis centers and medical insurance coverage, enterprises would face significant operational pressure if their services were not covered by medical insurance.

Establishing Center Experience Is Crucial

Zhang Yongqiang noted that the minimum configuration for a hemodialysis center currently requires 20 hemodialysis machines. When factoring in rent, renovation, basic medical equipment, specialized hemodialysis equipment, and working capital, the total investment needed is approximately RMB 6 million.However, the minimum investment in just 20 hemodialysis machines may not necessarily yield profitability.

Zhang Yongqiang believes that as private capital has only just entered this field, the biggest barrier lies in the lack of professional medical operations teams and operational experience, including the setup of both clinical and non-clinical departments. Most investment and operation teams for independent hemodialysis centers have transitioned from backgrounds in hospital department contracting or equipment placement, meaning the establishment of such centers is still in an exploratory phase. There is a significant difference between independent operation and departmental contracting. Within a hospital, considerations such as department design, infection control, and environmental protection are not required. However, although independent hemodialysis centers are small in scale, they must be fully comprehensive; strict compliance with laws and regulations in all aspects is essential to ensure risk-free operations.

For example, an independent hemodialysis center was once established on the fourth floor of a mixed-use commercial and residential building, posing significant safety hazards. First, elevator access was not adequately considered. The shopping mall only had standard sightseeing elevators, lacking medical-grade elevators. Since acute critical conditions can readily occur during hemodialysis sessions, the absence of medical elevators precludes the use of stretchers for emergency transport. Furthermore, hemodialysis generates substantial volumes of wastewater, making it impossible to pass the environmental impact assessment for sewage treatment facilities. Additionally, issues such as internal workflow design related to medical care, infection control, and patient safety are far more complex. A shortage of operational talent represents a critical challenge in the hemodialysis sector.

Medical services and hemodialysis services must be provided together.

Once an independent hemodialysis center is established, patient acquisition becomes a critical issue. Therefore, such centers should not pursue large-scale expansion; instead, they must carefully select their patient population. Based on experiences from Taiwan and Singapore, community-based hemodialysis centers typically operate with 20–30 dialysis machines. This scale allows centers to prioritize stable patients, while critically ill individuals and those requiring surgical interventions are referred to hospitals. Centers must avoid accepting all patients solely for profit motives; strategic selectivity is essential to mitigate medical risks.

In his article titled “In-Depth Analysis: The Liberalization of Policies for Hemodialysis Centers in China,” published on VCBeat, Zhang Yongqiang noted that policy management requires independent hemodialysis centers to enter into medical service agreements with general hospitals at Level II or above for the treatment of patients with acute complications of hemodialysis, and to establish two-way referral channels for the diagnosis and treatment of chronic complications of hemodialysis through medical service agreements with tertiary general hospitals within the same region. These two types of agreements have significant implications for independently established hemodialysis centers.It is relatively difficult from the perspective of the heart, as there is a competitive relationship between hemodialysis rooms in public hospitals and independent dialysis centers, making it challenging to finalize agreement signings, or requiring extensive communication and coordination efforts to achieve completion.

Such issues do not exist in hemodialysis centers in Singapore and the United States. In these countries, large public hospitals are responsible only for the first and second dialysis sessions; subsequent treatments are provided in community settings, with patients returning to hospitals only if complications arise. Physicians from public hospitals regularly conduct patient reviews at various private hemodialysis institutions, either proactively or upon invitation. However, such a model is unlikely to be implemented in China within the next five to ten years.

Experience of Aishen Medical

Aishen Medical is primarily composed of former members of the Weigao Renal Disease Industry Team, with a focus on establishing hemodialysis centers and specialized nephrology hospitals that integrate online and offline services. In 2017, its operations were launched in Hainan Province, and in 2018, Aishen Medical plans to expand its proven model to other key provinces across China.

Aishen Medical’s strategic focus on Hainan is driven by two key considerations: first, to develop tourism-oriented dialysis services; and second, to leverage Hainan’s interconnected medical insurance system with 25 other provinces and municipalities across China, which supports cross-regional direct settlement—a competitive advantage unmatched by other regions. Currently, Aishen Medical has applied to establish two nephrology hospitals and one dialysis center in cities such as Haikou and Sanya, with its first nephrology hospital scheduled to officially open in August. The company will provide comprehensive blood purification treatments covering the entire Hainan Province for both local and non-local dialysis patients. In particular, tourists and “snowbird” patients can seamlessly access dialysis services across the island within the Aishen Medical network, eliminating concerns related to referrals, appointments, and cross-regional medical insurance reimbursement.

Zhang Yongqiang believes that to develop in the hemodialysis industry, a long-term competitive mechanism is essential. In 5 to 10 years, as patients age and experience an increase in complications, having a broader range of related medical specialties will provide a distinct advantage. Relying solely on hemodialysis services is technically unsustainable in the long run.

During prolonged hemodialysis, the physical condition of patients may change, potentially leading to complications such as vascular calcification or thrombosis. In such cases, timely intervention by experienced physicians and nurses from multiple disciplines is required, including prompt thrombolysis and surgical procedures, which places high demands on the healthcare team.

Data from the English white paper released by Academician Liu Zhihong in 2015 showed that there were only about 10,000 nephrologists in China, and it was estimated that at least 5,000 additional hemodialysis centers would be needed in the future. According to the “Basic Standards for Hemodialysis Centers (Trial),” a hemodialysis center must have at least two physicians, one of whom must be a nephrologist permanently registered with the institution, while the other may be a physician practicing at multiple sites. Therefore, at least an additional5,000 to 6,000 physicians, half of whom should hold intermediate or senior professional titles.

When establishing independent hemodialysis centers, Aishen Medical adopts an integrated model combining specialized nephrology hospitals with independent hemodialysis centers to deliver comprehensive “whole-kidney disease” medical services. This approach addresses the majority of healthcare needs for patients with kidney disease and those undergoing dialysis, while progressively establishing technical support collaborations with leading academic medical centers across various regions. “Prioritizing patient safety and continuously improving healthcare quality” is Aishen Medical’s primary objective. The company provides systematic, long-term diagnostic and therapeutic services. In addition to basic dialysis care, it offers vascular access creation and maintenance, diagnosis and treatment of complications (such as hypertension, diabetes, and cardiovascular and cerebrovascular conditions), out-of-hospital patient management, and rehabilitation services.

Healthcare is inherently a systematic engineering endeavor that requires multidisciplinary and multi-party collaboration to be successfully implemented. It is believed that in the future, China will establish a healthcare system for blood purification therapy in which public hospitals serve as the mainstay—referring primarily to their leadership in medical technology rather than sheer volume—coexisting and collaborating with privately operated hemodialysis institutions, thereby providing patients with convenient and safe medical services.

Shengrenkang Medical Group

In the 1990s, the founder of Shengrenkang Medical Group (Chengdu Kangyi Mingren Medical Investment Management Co., Ltd.) started with two hemodialysis machines in Nanchong, Sichuan. After more than a decade of development, the group began to expand its layout after receiving investment from international capital such as OrbiMed in 2016. Currently, it holds controlling stakes in 12 primary and secondary hospitals, with main medical services focusing on the treatment of kidney diseases and hemodialysis.

These 12 hospitals are primarily located in Sichuan Province, with a strategic presence across Southwest and Northwest China, collectively operating more than 400 dialysis machines. The flagship facility, Chengdu Gaoxin Boli Hospital, covers an area of over 6,000 square meters and is equipped with 73 hemodialysis machines. Following the relaxation of regulatory policies, Shengrenkang plans to establish several independent hemodialysis centers in regions such as Sichuan, Xi’an, and Wuhan. These centers will be developed around hub hospitals like Boli Hospital, extending services into areas with limited medical resources. The independent hemodialysis centers will provide dialysis treatments, while the hub hospitals will deliver comprehensive medical services. Furthermore, Shengrenkang Group places significant emphasis on technological advancement and cutting-edge innovation. It has identified genetic engineering as the ultimate long-term solution for hemodialysis and will pursue further frontier developments in smart healthcare and gene technologies.

Sheng Renkang Medical Group, VP Chen Shi

Development of the Domestic Hemodialysis Market

Chen Shi believes that the current market size for hemodialysis services in China is approximately RMB 50 billion, and it has already entered a highly competitive "red ocean" stage. The domestic hemodialysis market has undergone three development stages: the first stage was tertiary hospitalsHospitals and public hospitals provide hemodialysis services; the second stage is when private hospitals began to enter the hemodialysis service market; the third stage is the opening of independent hemodialysis centers.

Compared with the "Management Specifications for Independent Hemodialysis Centers" promulgated in 2014, the standards introduced at the end of 2016 actually lowered the entry threshold for hemodialysis centers. Previously, only secondary or higher-level hospitals with a nephrology department were permitted to establish dialysis centers. Subsequently, independent hemodialysis centers could be established by securing contracts with secondary or higher-level general hospitals within a ten-kilometer radius and signing agreements with tertiary Grade A hospitals to guarantee green channels for patient referrals.

Therefore, under such policies at the time, it was difficult to apply for and operate independent hemodialysis centers. For private capital to establish a hemodialysis center, it had to either become an affiliate of a relevant Grade A tertiary or secondary hospital, or rely on opaque connections, to ensure that the center met regulatory standards. Previously, Shengrenkang’s internal calculations showed that the cost and effort required to apply for an independent hemodialysis center were comparable to those for establishing a small general hospital, and it also had to sign unequal agreements with other hospitals. In light of this, Shengrenkang Medical Group chose to directly apply for the establishment of a private hospital. Although referral and consultation agreements are still required after the relaxation of policies, the terms now differ fundamentally from those in the past.

Sheng Renkang’s previous strategy focused on building comprehensive private hospitals at the primary and secondary levels, incorporating hemodialysis centers under a model described as “small general, large specialty.” Currently, the time, effort, and costs required to apply for independent hemodialysis centers have been significantly reduced. Moving forward, Sheng Renkang will leverage its existing general hospitals as a foundation to apply for independent hemodialysis centers as branch facilities. This reduction in expansion costs will make it easier for hemodialysis centers to extend their reach to grassroots-level healthcare settings.

Hemodialysis Services Are an Industrialized Medical Service

In Chen Shi’s view, the mature hemodialysis industry exhibits the characteristics of instrument-based and industrialized healthcare, enabling assembly-line operations. Therefore, the Chinese government has currently classified hemodialysis centers as independently establishable medical institutions and opened them to private capital.

Treatment protocols and clinical workflows in hemodialysis centers have become mature and standardized. With the growing number of dialysis patients, costs have decreased significantly on a large scale. Therefore, for these reasons, the assembly-line operation of hemodialysis services is easier to implement than other medical services, thereby enabling the emergence of an independent hemodialysis center industry.

Patients who choose private hospitals or independent hemodialysis centers typically have two objectives. First, the costs are lower. Second, the standardization of hemodialysis has enabled low-risk medical services that are fully trustworthy.A More Convenient Private Hemodialysis Center.

The primary barriers to entry for hemodialysis centers lie in the scarcity of management expertise and qualified physicians. Given that hemodialysis services have achieved industrialization, a comparison with manufacturing facilities is apt. A factory’s competitiveness stems from effective production control, enhanced efficiency on assembly lines, and the advanced technical skills of process engineers (PE). In this analogy, production control corresponds to hospital management, assembly-line workers correspond to nurses in hemodialysis centers, and physicians correspond to process engineers. With robust management capabilities and highly skilled physicians and nurses, hemodialysis centers can continuously refine their “processes,” thereby enhancing their competitiveness. Currently, the most critical shortage is that of experienced physicians.

Although hemodialysis services have largely become industrialized, they still require healthcare professionals to provide personalized treatment and adjustments for individual patients. Strong capabilities in managing complications have thus become the core competitive advantage of private hemodialysis centers. In this context, Sheng Ren Kang’s nephrology hospitals place significant emphasis on personalized patient care and possess the expertise to manage complex complications associated with kidney disease, including procedures such as arteriovenous fistula creation, angioplasty, and parathyroidectomy (PTX), thereby enhancing their competitiveness.

Chongqing Aokailong

Chongqing Aikailong primarily serves the blood purification sector, offering a comprehensive portfolio that includes hemodialysis machines, water treatment systems for hemodialysis, hemodialysis consumables, and continuous renal replacement therapy (CRRT) systems. The company integrates research and development, production and sales, medical services, and healthcare informatics. Aikailong’s main products include: hemodialysis machines, hemodiafiltration machines, CRRT systems, and hemoperfusion machines; water treatment systems for hemodialysis, pure water equipment for sterile supply departments, pure water equipment for clinical laboratories, and central medical pure water systems; as well as laboratory ultrapure water systems. In recent years, Aikailong has expanded into the hemodialysis medical services sector, currently operating and preparing 16 hemodialysis service centers.

Chongqing Aokailong Medical Technology Co., Ltd. General Manager and Board Secretary Jia Bei

As a domestic manufacturer of dialysis machines, Aukailong’s business model has long extended beyond the mere sale of hemodialysis equipment. Instead, it employs a multi-pronged strategy—combining product sales, co-construction partnerships, solution support, and self-operated services—to increase its market share in the hemodialysis equipment sector.

In traditional sales, the main competitors of domestic brands are European, American, and Japanese brands. Aokailong's hemodialysis equipment has captured a portion of the market share and entered large hospitals such as Grade III Class A and Grade II Class A hospitals.

Public tertiary hospitals predominantly have a demand for direct procurement of equipment, while public secondary hospitals and non-public hospitals haveMost demands are for cooperative joint construction. Collaborating with small medical institutions to jointly establish hemodialysis centers is another way to increase the market share of hemodialysis machines.

For the independently operated dialysis service market, which has been gradually expanding in recent years, Aikailong offers comprehensive solutions and support, including standardized configurations for hemodialysis centers, clinical medical support from healthcare professionals, equipment maintenance and operational training, patient acquisition and promotion strategies, and an operational performance management system.

Meanwhile, Aokal has also established its own hemodialysis service institutions, creating a for-profit chain of blood purification centers under the brand “Aokal Dialysis Home.” Tailoring its services to different regions, cultural contexts, and patient preferences, Aokal has developed distinctive single-site medical service offerings, such as scheduled dialysis, travel dialysis, dedicated-physician dialysis, charitable dialysis, self-service dialysis, mutual-assistance dialysis, crowdfunding-supported dialysis, and visualized dialysis.

Aokailong’s future strategic goal is to build an integrated ecosystem of “hemodialysis products + hemodialysis services + a community for kidney patients.” This strategy is anchored by three pillars: “Aokailong Medical,” focusing on hemodialysis products; “Aokailong Dialysis Home,” dedicated to hemodialysis medical services; and “Aokailong Kidney Friends Club,” centered on the patient community and ecosystem. By leveraging internet-plus-healthcare platforms such as the “Kidney Aid” information platform and the “HCIS Online Hemodialysis Service Platform,” Aokailong aims to establish a comprehensive hemodialysis data platform. In summary, the company seeks to drive front-end sales and production of hemodialysis equipment and extend into the post-dialysis service market by investing in and operating (or exporting) hemodialysis centers, with hemodialysis medical services as the core foundation.

Hemodialysis Center Layout Across Regions

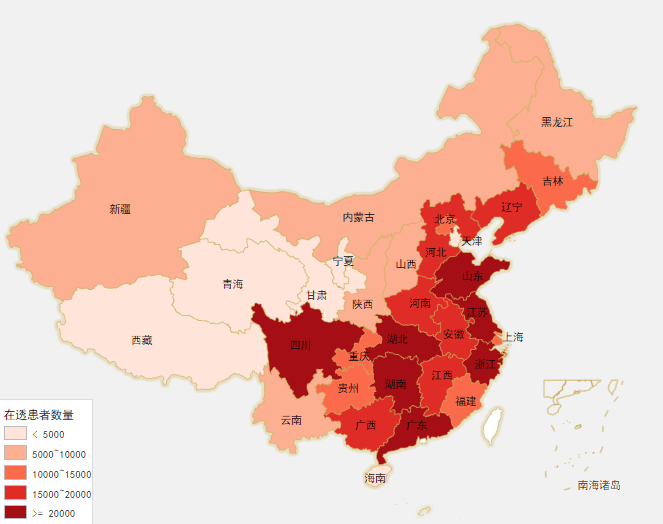

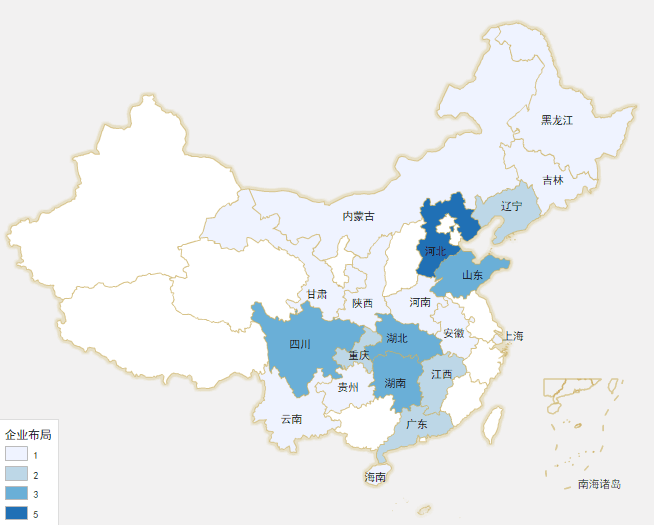

Based on the distribution map of hemodialysis patients across China, as compiled by CNRDS in the “Industry Report on Private Independent Hemodialysis Centers,” we can determine which provinces should be prioritized when planning the establishment of hemodialysis centers, taking into account patient volumes in each region. Of course, it is also necessary to consider various other factors, such as local approval policies, medical insurance policies, and the availability of upstream and downstream supporting services. Meanwhile,VCBeat’s statistics on independent hemodialysis center enterprises also describe their geographic distribution, which can be compared with the map of hemodialysis patient distribution.

National Distribution of Hemodialysis Patients, Data Source: CNRDS

Hemodialysis service providers have already established their presence; data collected by VCBeat.

Scan the QR code below to become an official VCBeat member and gain access to the full version.《"Report on the Private Independent Hemodialysis Center Industry". Furthermore, in the coming year, you will have unlimited access to the completeIndustry Trend Report, promptly grasp the latest globalInvestment and Financing Information, boasting a comprehensiveMedical Enterprise Database, andMassive Resource Matchmaking。

Related Links:

450,000 Hemodialysis Patients, a RMB 33.5 Billion Market: Will You Take Your Share?