Policy and Medical Insurance Are Decisive Factors for the Development of Primary Care SaaS Enterprises

Traditional HIS and cloud-based HIS in the SaaS model target entirely different customer segments. The former is widely adopted by large and medium-sized medical institutions, while the latter is better suited for primary care facilities.

Large and medium-sized medical institutions are characterized by ample funding and well-staffed information technology departments.Meanwhile, their operations are complex and encompass numerous departments.

Over the past two decades, large and medium-sized medical institutions in China have invested heavily in building in-house IT teams, procuring information systems through tendering processes, and establishing hospital IT infrastructure. To date, China’s traditional HIS market has become quite mature.

Administrators of Chinese healthcare institutions maintain a conservative stance toward data, citing concerns over patient data privacy breaches and cybersecurity. Although policies encourage data interoperability and the development of medical big data, the informatization initiatives of large and medium-sized healthcare institutions are expected to remain dominated by products from traditional HIS vendors in the coming years.

Why Are Primary Healthcare Institutions More Suited for the SaaS Cloud Model Than Large Hospitals?

1. As tiered diagnosis and treatment has entered a substantive implementation phase, primary healthcare institutions face an increasingly urgent—almost essential—need to integrate with medical insurance systems, enhance clinical capabilities, and improve revenue generation. This demand has spurred the emergence of companies offering cloud-based Hospital Information Systems (HIS) and cloud clinic solutions tailored for primary care settings;

2. Medical SaaS products are standardized services, primarily targeting the market of primary care and private medical institutions. These types of healthcare providers cannot afford to invest heavily in IT infrastructure or build in-house information technology teams like large hospitals do, nor can they sustain ongoing expenditures for subsequent system maintenance.Precisely because of its cost advantage, cloud-based HIS is more attractive to primary healthcare institutions than traditional HIS systems, which come with a hefty price tag.

At present, there are quite a few enterprises in China engaged in cloud-based HIS and cloud clinic solutions for primary healthcare.What is their current development status? What are the business models? Where do the core demands of primary healthcare institutions lie?What Are the Key Challenges in Implementing Enterprise Services?In response to these issues, VCBeat (WeChat Official Account: vcbeat) has compiled a list of domestic29 companiesMedical SaaS-related companies, with interviews and analyses of typical cases.

Through this report, you will learn:

I. Cloud-based HIS and cloud clinic markets in primary healthcare: both listed companies and startups are entering the fray;

II. The key to the business models of cloud-based Hospital Information Systems (HIS) and cloud clinics in primary healthcare lies in providing value-added services that meet core needs;

III. The main challenges in implementing SaaS services for primary healthcare institutions lie in localization and customization requirements.

1. Cloud-based HIS and Cloud Clinic Markets in Primary Healthcare: Both Listed Companies and Startups Enter the Arena

The latest data from the Statistical Information Center of the National Health and Family Planning Commission shows that,As of the end of April 2017, there were a total of 930,000 primary healthcare institutions across China, including: 35,000 community health service centers (and stations), 37,000 township health centers, 638,000 village clinics, and 205,000 outpatient clinics (infirmaries). This set of data corresponds to the theoretical market size for domestic primary healthcare informatization.

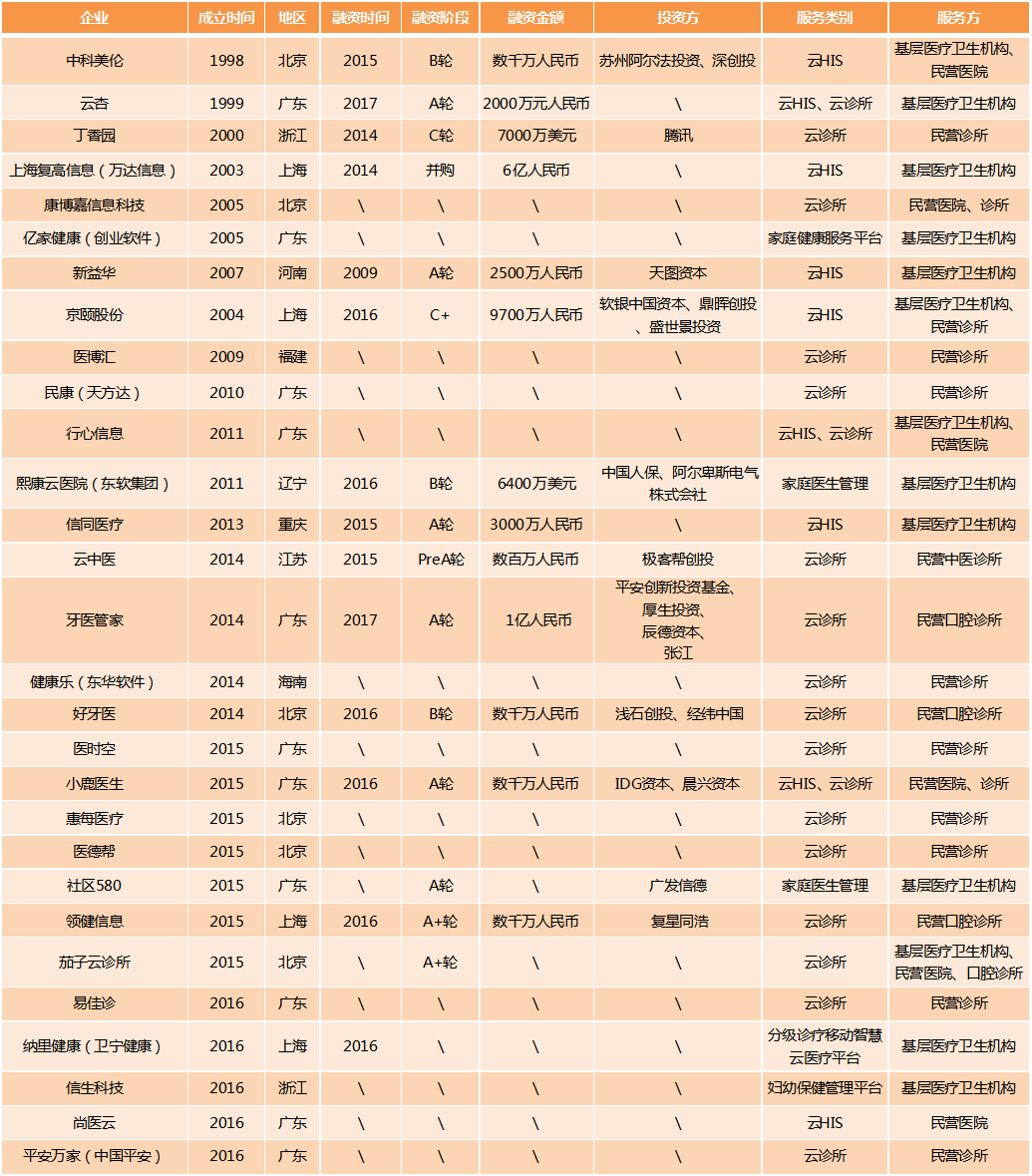

29 Chinese Companies Engaged in Primary Healthcare Informatics:

Data Source: VCBeat Knowledge Base

Company information presented in the charts can be queried through the VCBeat database. Scan the QR code at the end of this article to become a VCBeat member, granting you access to the VCBeat mini-program or official website to search for relevant company details using the database.

By analyzing the data in the table, VCBeat has identified two types of participants among cloud HIS and cloud clinic enterprises: one type comprises traditional HIS companies that also place significant emphasis on the market for primary care informatization. This category includes Yijia Health (under Chuangye Software), Fugao Information (under Wanda Information), Xikang Cloud Hospital (under Neusoft), Jiankangle (under DHC Software), and Nali Health (under Winning Health).

Another category consists of emerging healthcare IT companies. Although these enterprises missed the first wave of traditional Hospital Information System (HIS) development, they have entered the competitive landscape in this field due to their possession of certain resources within regional markets.

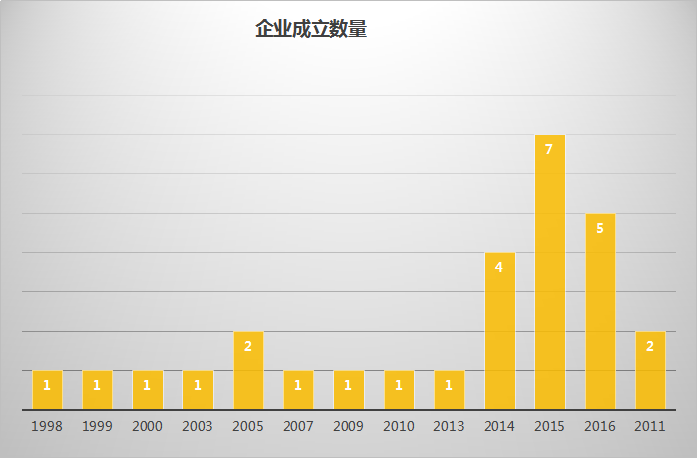

As can be seen from the establishment dates, the founding of these 29 companies was mainly concentrated in 2015 and 2016, during which a total of 12 companies were established successively.

From a policy perspective, the State Council successively issued the Guiding Opinions on Actively Promoting the “Internet Plus” Action and the Guiding Opinions on Promoting and Regulating the Application and Development of Health and Medical Big Data in 2015 and 2016.

The two “Opinions” call for supporting third-party institutions in establishing information-sharing service platforms for medical imaging, health records, laboratory test reports, and electronic medical records, and for building a safeguard system for healthcare big data. In light of this, many companies have seized the opportunity to invest in the development of new-generation healthcare IT platforms.

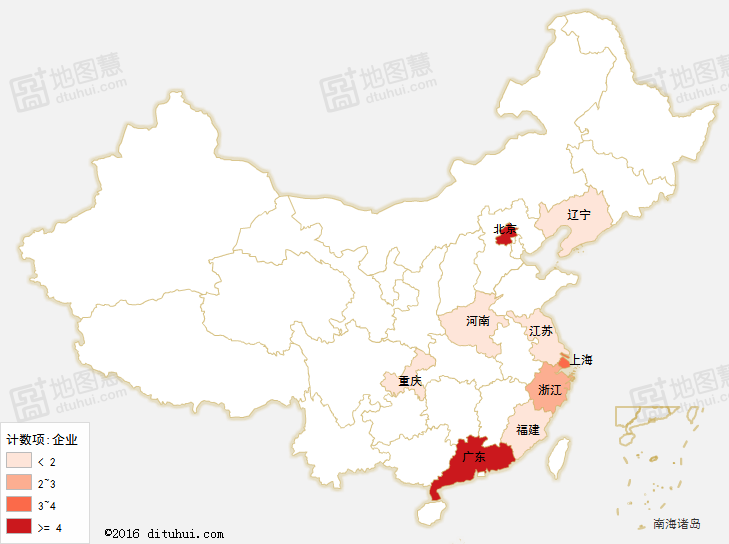

Geographically, these enterprises are primarily concentrated in regions with relatively abundant medical resources, such as Beijing, Shanghai, Guangzhou, and the Jiangsu-Zhejiang area.

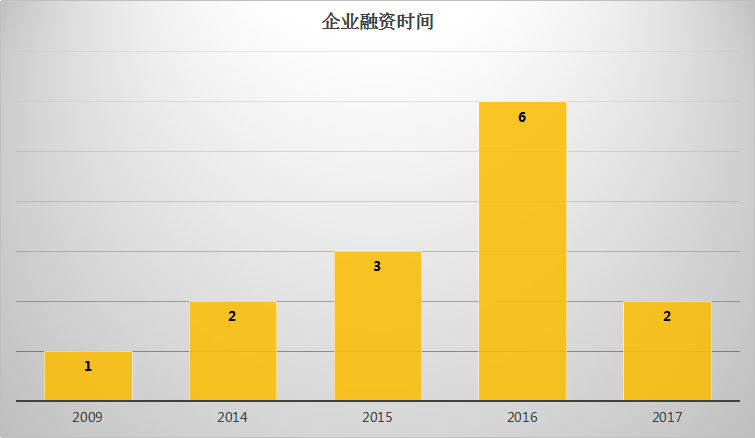

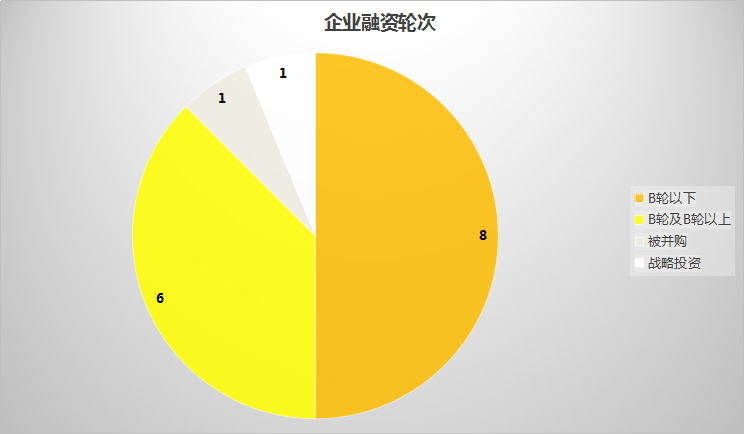

From a financing perspective, among companies with publicly disclosed funding information, the latest rounds of financing occurred primarily in 2015 and 2016. Considering both the financing stages and amounts, capital investment enthusiasm for cloud-based HIS (Hospital Information System) companies was relatively high between 2015 and 2016. Furthermore, among companies with publicly available financing data, the number of enterprises below Series B and those at or above Series B were roughly equal.

Given that more than half of the companies were established before 2015, we infer that investors do not place significant emphasis on a company’s age; rather, they base their investment decisions primarily on the business model. Consequently, earlier-established companies do not enjoy a distinct advantage in fundraising compared to newly founded ones.

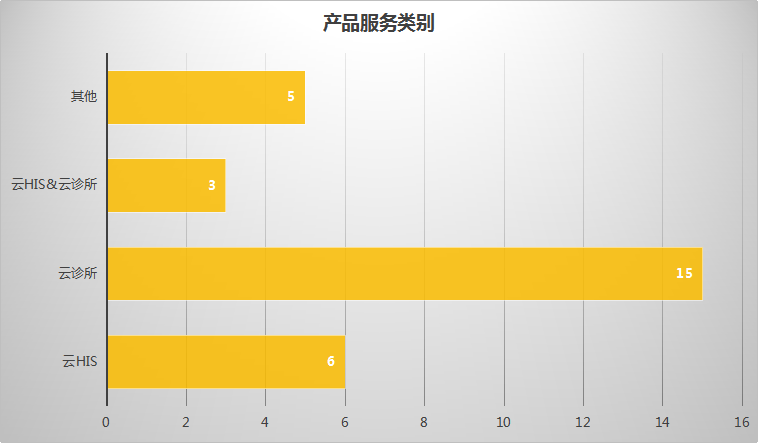

As can be seen from the product categories, cloud clinics and cloud HIS are the core products for the informatization needs of primary healthcare institutions. The vast majority of enterprises involved are24 CompaniesAmong them, Yunxing, Xingxin Information, and Xiaolu Doctor offer the broadest product portfolios, encompassing not only cloud-based Hospital Information System (HIS) solutions tailored for primary healthcare institutions but also cloud clinic products designed for private practices.

It is worth mentioning the sub-sectors,Stomatology, Traditional Chinese Medicine, and Western Medicine, forming the three major categories of cloud clinics currently.

II. The key to the business model of cloud-based HIS for primary healthcare and cloud clinics lies in providing value-added services that meet core needs

Keywords: Rapidly providing value-added services to community health service centers through the "Capability Cloud."

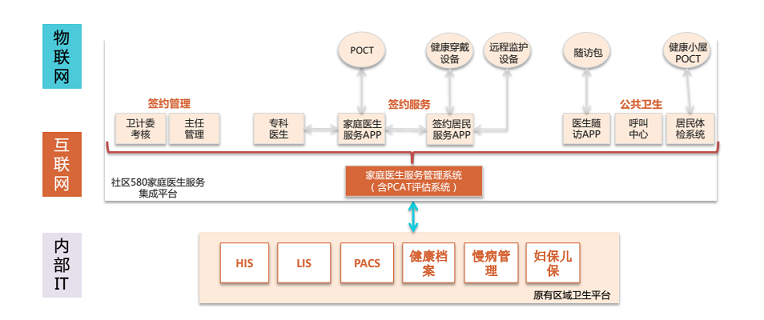

The entire product framework of Shequ 580 is built on the premise of serving primary healthcare.

First is the family doctor contract service. As a brand-new B2B2C service model, Community 580 signs contracts with hospitals and leverages SaaS cloud platforms, hospital information, and service workflows to enable rapid deployment, thereby extending community medical services to the internet.

Currently, the Community 580 product suite includes the Mobile Family Doctor APP, Mobile Follow-up APP, Two-way Referral Platform, Integrated Communication System for Community Hospitals, Chronic Disease Management and Assessment System, and Family Doctor Performance Management Platform. By integrating with existing Hospital Information Systems (HIS), Laboratory Information Systems (LIS), Picture Archiving and Communication Systems (PACS), and electronic health records from regional public health platforms, it forms a comprehensive internet-based tiered diagnosis and treatment solution.

Community 580 brands its comprehensive suite of self-provided services as the “Capability Cloud.” In addition to information technology services, the “Capability Cloud” integrates multiple medical services, including intelligent diagnosis, pharmaceutical delivery, and laboratory testing. Once these third-party services are integrated into the Community 580 platform, they can rapidly empower community hospitals and family doctors. Furthermore, various medical data from healthcare institutions can be quickly made available to physicians and residents through integration with the Community 580 platform, thereby generating substantial value.

For many community hospitals, building their own systems to integrate various services is often hindered by insufficient funding and maintenance capabilities. Through the “Capability Cloud” platform of Community 580, services such as patient enrollment, health management, medication delivery, and remote consultation can be provided to community hospitals within one to two weeks. This tightly connects patients, medical data, healthcare services, and the Internet of Things (IoT).

In terms of its business model, Community 580 collaborates with community hospitals to establish offline Family Doctor Contract Service Centers, akin to creating VIP lounges in banks. These centers offer residents a range of differentiated services, including premium interior design, identity verification, green-channel access, health kiosks, free screenings, and discounted consultation and treatment fees. Such measures significantly enhance residents’ willingness to sign up for family doctor contracts.

Furthermore, the Family Doctor Contract Service Center offers various customized service packages tailored to specific populations, such as the elderly and individuals with chronic diseases or a history of stroke. By integrating insurance, pharmaceuticals, caregiving, and chronic disease management services, Community 580 has developed a series of comprehensive service packages available for purchase on its platform. All these service packages are integrated into the Community 580 mobile app, allowing end-users to make direct purchases, akin to personalized value-added services.

Keywords: Targeting primary hospitals in prefecture-level cities, with a strong focus on services.

Jingyi Share’s cloud-based Hospital Information System (HIS) is implemented at the prefecture-level city level. Currently, the majority of primary healthcare institutions across China’s 293 prefecture-level cities are motivated to address their informatization needs through cloud-based models such as cloud HIS and cloud Picture Archiving and Communication Systems (PACS). Bozhou City in Anhui Province serves as a representative example.

Bozhou City has a population of approximately 6.5 million. There are a total of 13 hospitals at the secondary level or above, including one tertiary hospital. The city also has 1,520 primary healthcare facilities and around 50 private medical institutions.

Currently, all primary healthcare institutions across the two counties and one district of Bozhou City—including public medical institutions, private hospitals, and clinics—have adopted Jingyi Cloud HIS. (Secondary and tertiary hospitals retain their own HIS systems and engage in bidirectional data exchange with Bozhou Cloud HIS through the Bozhou Regional Health Information Platform.)

As of June 10, 2017, 978 medical institutions in Bozhou City had achieved real-time information sharing through Kyee’s Cloud HIS. Building on this foundation, the Bozhou Population Health Information Platform rapidly facilitated interconnectivity among more than 1,500 medical institutions via the Cloud HIS, accumulating 380 million clinical records and providing massive data support for the construction of a tiered diagnosis and treatment system. The Bozhou tiered diagnosis and treatment system covers one tertiary hospital, eight secondary hospitals, and all local primary healthcare institutions using the Cloud HIS. To date, the system has processed 1,780 upward referrals and 3,239 downward referrals.

Given current market conditions, the cost of even the most basic Hospital Information System (HIS) is no less than RMB 200,000. Kyee Cloud HIS can help governments and primary healthcare institutions reduce these costs by 90%. A primary healthcare institution needs to invest only RMB 5,000 annually to meet its routine informatization needs, and just RMB 20,000 to comprehensively support all its daily informatization applications.

Implementing cloud-based Hospital Information Systems (HIS) at the prefecture-level city level requires substantial investment in both capital and human resources. Deploying a cloud HIS system in a single prefecture-level city may demand the full-time efforts of 30 to 50 staff members for research, development, and implementation over a period exceeding six months before yielding tangible results. This places significant financial and labor cost pressures on smaller cloud HIS vendors.

Kyee Group has invested substantial human and financial resources in the development of its cloud-based Hospital Information System (HIS) to meet the personalized informatization needs of local governments and healthcare institutions, helping them transition from legacy workflows and become adept at using cloud-based medical information systems. Meanwhile, Kyee Group also bears the critical responsibility of securely migrating historical data from legacy systems to the new platform.

The entire implementation and delivery of Jingyi Cloud HIS is divided into three phases:

Phase I is the product implementation phase. During this phase, Kyee Group deploys a team of 50 to 60 personnel to carry out customized development over a period of 4 to 6 months, based on the actual informatization needs of local governments and healthcare institutions.

The second phase is the training phase. Kyee Group will dispatch a professional team to conduct training for local primary healthcare institutions over a period of four to six months;

Phase III is the ongoing maintenance phase. Jingyi Co., Ltd. deploys a team of approximately 10 personnel to maintain a permanent on-site presence in cities where the cloud-based HIS has been implemented, providing long-term services to local governments and healthcare institutions.

Thus, it appears that Jingyi Cloud HIS is not as “lightweight” as one might imagine.

Keywords: Centered on informatization, facilitating deep integration of primary care clinics with medical insurance, medical-nursing combined care, and elderly care services.

Minkang, established in 1996, is a wholly-owned subsidiary of Tianfangda. Prior to 2013, Minkang was dedicated to the informatization of public health services at the primary care level, achieving remarkable performance. Its years of deep engagement in the primary healthcare sector have earned Minkang a solid brand reputation within the industry.

After 2013, Minkang entered a transition period and began to focus on the private clinic market.

Minkang Clinic Management Software, delivered as a SaaS solution, integrates healthcare-related industries to provide primary care institutions with one-stop medical services—including electronic prescriptions, electronic medical records, patient management, and financial management—that span the pre-consultation, consultation, and post-consultation phases.

Currently, the number of paying users of Minkang Clinic Cloud has exceeded 18,000. It covers high-end chain clinics and scattered grassroots clinics. Among these 18,000 clinics, the ratio of non-public to public institutions is approximately 5:1.

After years of exploration, Minkang has formulated a new strategic initiative called the “One Body, Three Wings Strategic Empowerment Plan,” building upon its clinic cloud platform, Minkang Academy, and new media marketing services.

“One Body, Three Wings” Plan: “One Body” refers to the SaaS Outpatient Cloud (comprising twelve major modules, such as electronic medical records, remote consultations, and mobile payments); “Three Wings” refer to medical insurance, pharmaceuticals, and the integration of medical care with elderly care, thereby establishing R&D centers and marketing centers.

In this strategy, Minkang leverages information technology as a vehicle, integrating medical insurance (including commercial insurance), pharmaceuticals, and elderly care to truly extend clinic services to surrounding residents, particularly the elderly, the weak, the sick, and the disabled.

Medical Insurance and Commercial Insurance:

Currently, Minkang’s pricing for social security informatization, interface integration, and a series of agency services for its clinics in Shenzhen is set at three tiers: RMB 12,000, RMB 14,000, and RMB 18,000 per clinic. In other cities across China, the prices are relatively higher, averaging approximately RMB 80,000 per clinic.

In addition to medical insurance, Minkang has also partnered with large-scale or distinctive commercial insurance companies in China, such as Ping An Insurance, PICC, and Hua An Insurance.

On one hand, Minkang can partner with insurance companies to provide medical liability coverage for doctors or practitioners at clinics, thereby reducing their professional risks.

On the other hand, clinics can also act as agents for the sale of commercial insurance products—including health, disease, accident, and even dividend-type policies—to existing patients. By providing high-quality health and critical illness insurance services, clinics can help alleviate patients’ financial concerns regarding medical treatments not covered by basic medical insurance.

Furthermore, Minkang collaborates with commercial insurance companies by designating selected high-quality primary care clinics as designated primary healthcare providers for these insurers, thereby enhancing its brand reputation.

Pharmaceuticals:

Minkang has established the “Yaozhigong” B2B trading platform and actively collaborates with numerous well-known domestic pharmaceutical companies, including Kangmei Pharmaceutical, Luye Pharma, and Xiuzheng Pharmaceutical, to explore payment models such as online payment, offline payment, and credit-term payment. Furthermore, Minkang plans to introduce third-party supply chain finance companies to address the funding challenges faced by primary healthcare institutions.

Since Minkang Cloud Clinic serves 18,000 primary care clinics, the Minkang Outpatient Cloud Platform leverages this large network to conduct centralized online procurement and collective bidding, thereby securing lower drug purchase prices for these clinics.

This approach not only directly benefits clinics but also enables the general public to purchase affordable medications.

Integration of Medical and Elderly Care:

Since the vast majority of national medical insurance funds are allocated to the elderly population, and supporting policies related to integrated medical and elderly care have been significantly liberalized across China.

Therefore, Minkang has chosen to collaborate with major domestic elderly care institution service providers to help these institutions enhance their integrated services for information technology and supporting hardware, up toIntegration with medical insurance.

III. Primary Healthcare InstitutionsSaaS ServicesThe main challenge in implementation lies in localization and customization requirements.

Keywords: localized customization of reports, electronic medical records (EMR), and refund processes.

To facilitate the familiarization of healthcare professionals in Bozhou with the Cloud HIS, Kyee Group assigned an administrator to each hospital in Bozhou during the implementation and go-live process, enabling these administrators to configure customized functionalities tailored to each hospital’s needs.

These medical institutions’ customized solutions primarily consist of two components, one of which is reporting and statistics; the Weigang Central Health Center in Qiaocheng District serves as a representative example.

In 2016, after implementing Kyee’s cloud-based Hospital Information System (HIS), Weigang Central Health Center devoted significant effort to report processing. Kyee’s R&D engineers conducted multiple rounds of on-site investigations and, addressing the needs of directors from multiple community health centers in Bozhou City, carried out customized reporting and tiered statistical analysis. Furthermore, Kyee performed localized customization for Bozhou City’s existing electronic medical records (EMR) and refund processes.

When Bozhou City first began promoting Jingyi Cloud HIS, it encountered numerous challenges. These included inconsistent usage habits among physicians, varying levels and metrics for report statistics, and the need to implement statistical analyses by department, by physician, and across other specialized dimensions. Given the urgent demand from medical institutions for these functionalities, Jingyi deployed a professional team to actively collaborate and carry out customized development.

After months of development and debugging, Kingyee has enhanced the reporting and statistical capabilities of its Cloud HIS, further refining the system to enable healthcare administrators and physicians in Bozhou’s medical institutions to truly experience the convenience brought by the new platform.

Keywords: Under policy guidance, there is a need for rapid product customization and iteration capabilities.

Prior to adopting Community 580’s products, the Qingshan District Community Health Service Center in Wuhan lagged behind in informatization, with most of its information systems still being standalone versions based on C/S architecture.

The plan at the time was threefold: first, to align Qingshan District with the medical insurance system; second, to create electronic records for family doctor contracts and other tasks performed by medical personnel, upload them to the cloud, and establish an integrated platform and system for management; and finally, to replace previous manual operations with a new information system.

The family doctor service platform provided by Community 580 delivers services via the cloud. Internally, it integrates information systems for basic medical care and basic public health services, thereby breaking down information silos. Externally, it offers residents services such as contract signing, interaction, appointment scheduling, personal health records, chronic disease management, remote diagnosis and treatment, and online payment, thus bridging the “last mile” gap in healthcare access. These services align with the direction of China’s healthcare reform.

Given the broad scope of services provided by community health centers, informatization initiatives must be policy-driven. Rather than prioritizing corporate brand recognition or market share, the Qingshan District Health and Family Planning Commission places greater emphasis on an IT enterprise’s ability to rapidly iterate and sustain long-term development. The Community 580 product can swiftly adapt to evolving needs at primary healthcare institutions. Minor requirement changes for typical community health centers can be implemented within ten days to two weeks, while more systematic functional updates can be delivered in approximately one month.

Regarding payment, community health service centers pay on an annual service-purchase basis.

IV. Summary and Analysis

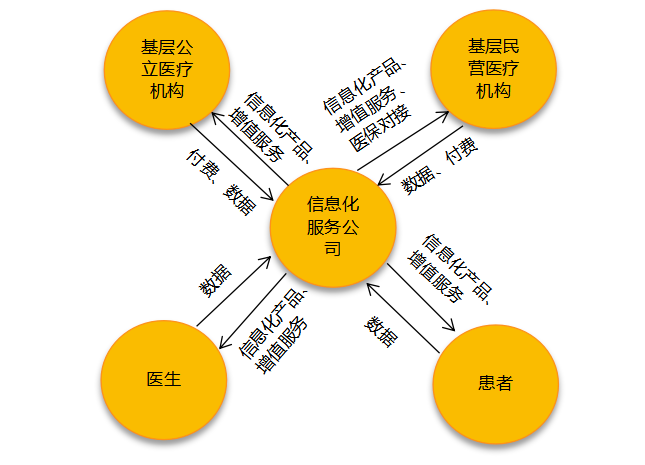

If the roles involved in the informatization of primary healthcare are simply categorized:Primary-level public medical institutions, primary-level private medical institutions, health IT service companies, physicians, and patients.We can derive the following supply-demand relationship:

1. As primary-level public medical institutions are significantly influenced by policies and are required to implement tiered diagnosis and treatment as well as family doctor contracting services, they exhibit strong demand for new information technology products and a high willingness to pay. Furthermore, since enterprises serving these primary-level public medical institutions are also heavily impacted by policy dynamics, companies seeking to capture this market segment must possess not only robust resource backgrounds but also strong capabilities in product customization and localization.

2. Grassroots private medical institutions have less demand for information technology (IT) products than grassroots public medical institutions. However, private clinics often have a rigid demand for health insurance payment services. Given the interdependent relationship between health insurance payments and IT systems, IT companies can transition toward health insurance payment solutions or integrated medical and elderly care services. This strategy can generate strong willingness to pay among a subset of clinics and may also help direct elderly care funding toward the clinic sector.

3. Although doctors and patients have certain informatization needs regarding family doctor services, it is currently difficult to persuade them to pay for these services. However, some enterprises are beginning to encourage patients to pay through health management and service upgrades, but the business model still requires exploration, and market acceptance remains to be tested.

4. As can be seen from the figure, nearly every loop generates data flow, making medical big data services possible. In terms of data value, since private medical institutions currently have low market coverage and low system utilization rates, the volume of data obtained, such as electronic prescriptions, is not significant. Furthermore, due to legal issues concerning data ownership, it is difficult to achieve data application at this stage.

Currently, the core competitive factor for enterprises providing health IT solutions to public primary care institutions is resources. From the perspective of payers, the government remains the largest paying group in this market; therefore, companies with strong government resource backgrounds can access a larger market share.

In the future, competition among these enterprises in public medical institutions will largely unfold at the prefecture-level city level. Drawing on the market landscape of traditional healthcare IT companies, the informatization market for primary care institutions is likely to remain fragmented, with different players dominating their respective regions.

In the informatics market for grassroots private medical institutions, product differentiation among various systems is not significant, and marketing exerts a strong influence, making price wars more likely. Influenced by the varying stringency of local medical insurance policies, enterprises seeking to acquire customers with more precise needs will increasingly focus their competitive efforts in cities where medical insurance policies are more open.

References:

Donghai Securities Report “Latest Industry Tracking Report: Healthcare Informatics, the Cloud Era Has Arrived》Author/Liu Chenchen

Special Acknowledgments:

Mr. Cheng Ming, Deputy Director of the Health and Family Planning Commission of Qingshan District, Wuhan City

Mr. Zhang Jie, Chief of the Publicity and Information Section, Bozhou Municipal Health and Family Planning Commission

Mr. Liu Bo, CEO of Shequ 580

Mr. Li Zhi, Chairman of Jingyi Group

Mr. Yan Biao, General Manager of Minkang

Scan the QR code below to become an official VCBeat member, and you can log in to the VCBeat mini-program/official website to use the database to query relevant company information. In the coming year, you will have unlimited access to the completeIndustry Trends Report, timely grasp the latest globalInvestment and Financing Information, boasting a comprehensiveHealthcare Enterprise Database, and alsoMassive Resource Matching。

Scan the code to become a VCBeat member,

Beta Version Trial Price: ¥365/year.