Anlong Fund: How It Identified Hidden Gems in Healthcare, Doubling Portfolio Valuations After Investing in 13 Companies Within Two Years

In the first quarter of 2017, the top three “hotspots” for domestic healthcare investment and financing were undoubtedly companies in the big health, consumer healthcare, and healthcare informatization sectors. Pharmaceuticals and medical devices, as the pillar industries of traditional healthcare, appeared to have been somewhat neglected by capital.

Investors’ wait-and-see stance reflects, on the one hand, the high barriers to entry for investing in these two sectors, and on the other, the considerable difficulty of identifying distinctive investment targets in an absolutely mature market.

Professionalism is particularly important.

Anlong Fund, established in 2015, focuses on the pharmaceuticals, medical devices, healthcare services (informatization), and life sciences sectors. Prominently displayed on its official websiteOverseas-educated, Global Perspective, Senior, BackgroundThese nine words aptly summarize the professional backgrounds of the three co-founders.

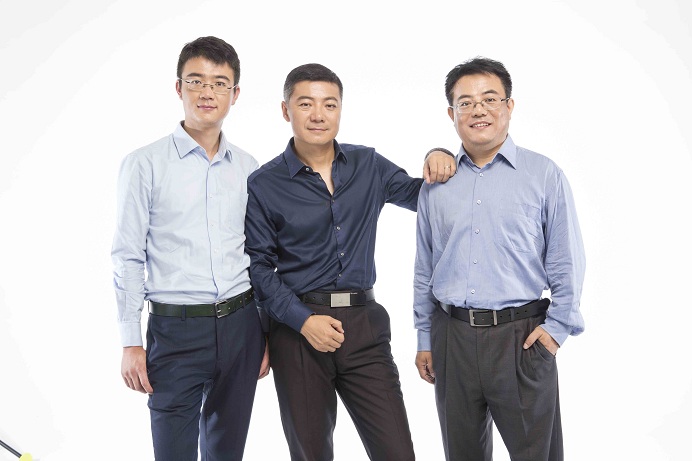

Anlong Fund’s three investors, from left to right: Gong Mengchun, Zhao Chunlin, and Wu Yuepeng

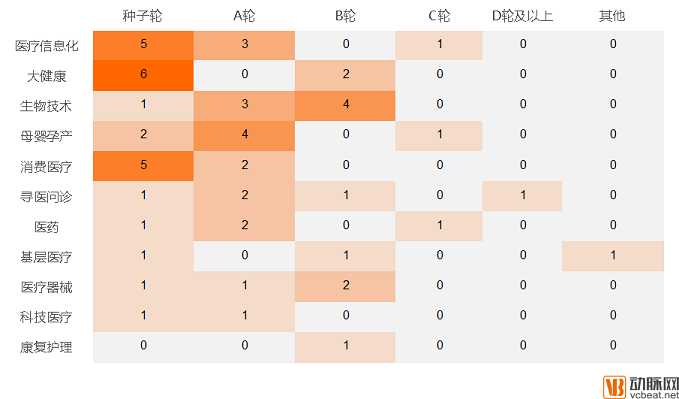

Over the past two years, Anlong Fund has leveraged its investors' discerning eye toPharmaceuticals, Medical Devices, among other areas, including3Including enterprises co-founded, the total investment amounted to13 companies, with its post-investment valuation doubling repeatedly.

Anlong Fund’s “Peach Garden Oath”

Zhao Chunlin was the first to propose the idea of establishing a fund. As a returnee from overseas, he previously spearheaded global market expansion at Pfizer in the United States.

After returning to China, Zhao Chunlin founded Beijing Longmaide Biotechnology Co., Ltd., which served as the distributor for foreign life science products and medical devices. Five years later, the company was sold to Cold Spring Harbor Taiwan, enabling Zhao Chunlin to earn his first significant fortune.

In 2011, Zhao Chunlin entered the field of life sciences and healthcare investment, successively working at CAS Star Capital and C-Bridge Capital.

During this period, Zhao Chunlin invested in14 projects, led 8 of them, among which one project increased in value by 4 times over 2 years and has already been exited. Additionally, 2 projects received follow-on investments, with the investment value increasing by 8 times over two years.。

For Anlong’s management team, Zhao Chunlin has always maintained stringent criteria for candidate selection. Only senior experts with advanced degrees and years of experience in the industry are granted entry into Anlong Fund.

Wu Yuepeng, Investment Director at Anlong Fund, holds an MBA from the School of Economics and Management at Tsinghua University. He has been engaged in venture capital since 2011, previously working in equity investment at CAS Orient Instrument Group and 55 Oriental Ruitai Venture Capital. He has achieved notable accomplishments in the TMT, healthcare, and biopharmaceutical sectors.

Previous investment cases include: Winner Microelectronics, Zhongyuan Heju, Guoke Hengtai Medical Technology, CAS Cloud Spectrum, Xipu Education, Huatai Chenguang Pharmaceutical, Tianxinhe Biotechnology, Lianxin Medical, Langsheng Technology, and Conatus Pharmaceuticals.

In 2012, Wu Yuepeng joined Orient Scientific Instrument Group, a company engaged in the sales of scientific research instruments and equipment.

At Orient Scientific Instrument Group, Wu Yuepeng also engaged in investment activities, establishing a venture capital firm named 55 Orient Ruitai Venture Capital. As the cornerstone investor, Orient Scientific Instrument Group guided the firm’s primary focus and investment direction toward high-tech instruments and equipment, advanced manufacturing, and medical devices.

As both were equity investment funds under the Chinese Academy of Sciences system, Wu Yuepeng got to know Zhao Chunlin during that period. The two frequently exchanged views on investments and jointly participated in numerous projects.

Although the two later joined different platforms, they reunited at Anlong Fund two years later. In 2016, in addition to Wu Yuepeng, Zhao Chunlin welcomed another key addition to the management team—Dr. Gong Mengchun.

Gong Mengchun, Investment Director at Anlong Fund, holds a Doctor of Medicine degree from Peking Union Medical College. He served as a resident physician in the Department of Internal Medicine at Peking Union Medical College Hospital, where he conducted research in pediatric nephrology and visited the University of California, San Francisco (UCSF) as a visiting scholar. In early 2015, he joined InterSystems as Executive Physician, overseeing market expansion, product design and planning, clinical support, and user training, thereby fostering positive interaction and efficient collaboration between InterSystems and healthcare professionals.

As the only one among the three with a medical background, Gong Mengchun primarily focuses on precision medicine and healthcare informatization at Anlong Fund. Together with Zhao Chunlin, who oversees pharmaceuticals, and Wu Yuepeng, who is responsible for medical devices, they formed a well-defined and unbreakable “trident” team.

Zhao Chunlin’s Pharmaceuticals: Overseas Endorsements Are Essential

Current Opportunities in the Pharmaceutical and Healthcare Sector Lie in"New Drug Development",Zhao Chunlin's overseas work experience has always convinced him of one thing:The product must be endorsed by multinational pharmaceutical companies.。The Meaning of Quotation Marks, Based onZhao Chunlin explained that domestic new drug development is still in the imitation stage.

“It is difficult for new drugs from our country to achieve the recognition and standards of European and American markets.”

Based on this philosophy, Anlong Fund, leveraging the foundation of the Chinese Academy of Sciences and in partnership with Pfizer, jointly established Kehui Innovation. This enterprise incubator, featuring management participation from a multinational corporation and focusing on the Chinese market, is eligible for government policy support.

Currently, Kehui Innovation has established its first new drug R&D enterprise in Chengdu, which is also a company co-founded by Anlong.

“Anlong Fund currently refrains from investing in domestic innovative products, particularly those billed as “globally leading” or “the world’s only.””

According to Zhao Chunlin, these products and technologies have obtained approvals and certificates from China’s National Medical Products Administration (NMPA) through various means, clearing hurdles such as bidding processes and pricing reviews. If a product or technology lacks supporting literature from renowned foreign academic institutions and clinical organizations, or endorsement from well-funded multinational corporations, most domestic clinicians will remain skeptical. In the short term, these products may fail to gain acceptance in the clinical market, and in some cases, may never be accepted.

“This is the dire consequence of the widespread skepticism and rejection among doctors in China, resulting from years of deception by domestic companies,” said Zhao Chunlin.

Take cancer as an example. If Chinese entrepreneurs suddenly propose a target that has not been proven and is absent from scientific literature, beyond the important targets already recognized internationally, it can be said that such entrepreneurs have basically “bid farewell” to Anlong Fund.

In 2016, Anlong Fund invested RMB 10 million in Conatus Pharmaceuticals to support new drug development. This biopharmaceutical company, with products in the clinical (research) stage, is dedicated to developing innovative therapies for autoimmune and allergic diseases. Its lead candidate, CBP-307, is a second-generation immunomodulator targeting S1P1 (a GPCR), intended for the treatment of various autoimmune conditions, including multiple sclerosis, inflammatory bowel disease, and psoriasis.

In January this year, Kangnaide secured a $20 million premium financing round led by Qiming Venture Partners.

Regarding the rationale behind investing in Connexin, Zhao Chunlin told VCBeat: “Internationally, there are already mature products targeting S1P1, with annual sales reaching $700 million. However, these foreign products have not entered the Chinese market, and they suffer from insufficient specificity and sensitivity, necessitating higher dosages and resulting in more significant side effects. In contrast, Connexin’s product offers higher specificity and sensitivity, which allows for lower dosages and reduced side effects, thereby presenting substantial market potential.”

Wu Yuepeng's Devices: Import Substitution Is the Core

Unlike the high volatility characteristic of internet companies, the medical device industry is relatively stable. This isWu Yuepeng's Assessment of This Field。

“The medical device industry is a showcase for hard technology. If a company has distinct advantages in terms of medical applications, target customer segments, and marketing strategies, it is considered relatively reliable.。”

At present, many key large-scale medical devices and consumables remain under the control of certain foreign companies. Meanwhile, the trend and background of domestic substitution in China have become irreversible.

The import substitution of medical devices, particularly high-end consumables, has consistently received government support. The policy dividends for high-end substitution lie not only in the regulatory leniency regarding product patents, clinical trials, and approval processes, but also in the preferential policies governing hospital tendering and procurement.

“The ideal founders for such projects are distributors of multinational corporations’ products. These individuals often have a background in clinical medicine; they ventured into the business world early on, serving as pharmaceutical or medical device sales representatives for multinational companies. After a few years, they became distributors, and after more than a decade of navigating the medical distribution industry, they have firmly secured healthcare sales channels and possess deep familiarity with their focused markets,” Wu Yuepeng told VCBeat.

As competition intensifies, with market share and profit margins being continuously squeezed, this group seeks to transform into manufacturers with research and development capabilities.

“They are well-versed in the market, have mastered distribution channels, and collaborate with domestic research institutions to develop medical devices tailored to China’s specific conditions.Leverage government policy preferences in approval, tendering, and procurement to replace imported products through proprietary channels or extend distribution networks to county- and township-level hospitals, thereby rapidly capturing the domestic medical market.“said Wu Yuepeng.

Anlong Fund Investmentof Handheld Ultrasound and 4D Xiangtai, are all such representative enterprises.

Why Invest in Handheld Ultrasound (Langsheng Technology): Wu Yuepeng’s Three Considerations:

1. Technological factors.Langsheng Technology’s co-founder, Wu Zhe, earned his Ph.D. in Ultrasound and Imaging from the University of Rochester in the United States. With 13 years of dedicated research in ultrasound imaging, he is a renowned expert in the field. The other co-founder, Gong Ren, graduated with a degree in Electrical Engineering from the Georgia Institute of Technology in the United States and brings extensive experience in handheld device computing. Together, they form an ideal partnership.

Additionally, Langsheng Technology’s smart handheld ultrasound device has obtained medical device product registration certification from Sichuan Province, making it one of the very few such products authorized for market sale.

2. Market Demand.Conventional medical ultrasound imaging equipment is bulky and immobile, making it inconvenient to carry. For primary healthcare institutions, transporting these machines during outreach programs to lower-tier facilities or communities becomes a significant challenge.

In addition to primary care institutions, various departments in large hospitals also have significant demand: such as anesthesiology, pain management, urology, general surgery, gynecology, pulmonology, hematology, and oncology. These departments frequently utilize ultrasound equipment during routine diagnostic procedures. This has led to an exceptionally heavy workload for the radiology/ultrasound departments in large hospitals, making it difficult to fully meet the needs of all other clinical departments.

Ultrasound equipment is expensive, and the cost of independent procurement by each department is prohibitively high. Moreover, large-scale ultrasound devices are complex to operate, making operator training a long-term endeavor. Therefore, an intelligent handheld ultrasound device that meets clinical needs, is portable, and is reasonably priced has become an essential requirement for large hospitals.

3. Marketing Level.Wu Yuepeng previously communicated with two senior marketing executives at Langsheng Technology. Both are seasoned marketing experts with many years of industry experience who left large corporations to join this startup, driven by their optimism about the product’s market prospects. They also brought to Langsheng Technology the extensive market resources they had accumulated over the years.

Gong Mengchun: Clinical Data Is Key to Precision Medicine

Regarding the development of the healthcare informatization industry, Gong Mengchun offered VCBeat a Dickensian response: “It was the worst of times, it was also the best of times.”

The so-called "worst of times" refers to the fact that years of development have led the entire industry into a situation of low-price competition, with manufacturers making minimal profits on projects. During this period, not only have substantial labor costs been incurred, but no major technological breakthroughs have emerged either.

Gong Mengchun believes that after a period of stagnation, new demands have gradually emerged in the industry. For companies with technological innovation capabilities, now is an excellent time to enter the market.Particularly in the following areas:

First,Companies engaged in phenotypic exploration of clinical data will have very broad future prospects.Phenotyping of clinical data includes standardization of clinical data, construction of phenome groups, etc. In simple terms, it is the process of transforming data generated by real-world clinical systems into analyzable data.

Given the difficulty in analyzing EMR data, transforming these clinical records into analyzable datasets constitutes a vast technical framework.

Second,Next-generation hospital information systems, or enterprise-wide, integrated informatics solutions, will present significant growth opportunities.。

The so-called next generation refers to how genomic data or other omics data are integrated with clinical data in the era of precision medicine.

Once hospitals have established robust health informatics capabilities, they can capture the value and benefits to which they are entitled across the entire precision medicine industry. This also serves as the driving force for hospitals to create new service models and build new value systems.

Third,Next-Generation Electronic Medical Record (EMR) Products。

Gong Mengchun’s experience at InterSystems has given him a clear understanding that the integration of electronic medical records (EMR) with clinical decision support systems in China still has significant room for growth compared to international products. Therefore, this direction presents substantial opportunities for the entire healthcare informatics industry.

Previously, VCBeat reported on Weishuo Medicine and Hetao Medical, whose investor was Gong Mengchun.

At the core of Shuo Medicine is a typical project that integrates healthcare informatics with precision medicine, with its primary product being a knowledge base for precision medicine.

The entire gene sequencing process, from the generation of sequencing results and bioinformatics analysis to the creation of VCF files and the subsequent generation of clinical reports, requires extensive utilization of knowledge base content.

However, the quality of knowledge bases referenced by various hospitals during gene analysis and interpretation varies significantly, leading to substantial disparities in the quality of clinical reports. Consequently, physicians are often unable to freely utilize the results of genetic analysis in clinical practice due to various concerns.

What we are doing for Shuo Medicine is to establish a standardized knowledge base platform.

Gong Mengchun favors Weishuo Medicine, primarily for the following reasons:

First, Weishuo addresses rigid demand. Currently, precision medicine in China is gradually transitioning from a disordered and chaotic state to a standardized and regulated system. Weishuo Medicine has seized the core opportunities and made proactive strategic arrangements.

Second, Weishuo’s business aligns with the direction of national healthcare development and responds to national policies. In the 2016 National Key R&D Program for Precision Medicine, a major project was the establishment of a precision medicine knowledge base. This further validates that Weishuo Medical has chosen the right path.

In addition, Anlong Fund has also helped introduce numerous strategic resources to Weishuo Medicine. Leveraging Gong Mengchun’s strong reputation in the field of precision medicine, the fund facilitated connections between Weishuo Medicine and hospitals, creating a win-win situation for all parties involved.

Invest in Reliable People, Do Reliable Things

After concluding the interviews with two other investors, Zhao Chunlin could not contain himself and added a further statement. The reporter had initially intended to integrate it with the preceding text and make slight edits, but after careful consideration, decided to present it to readers in its original, unedited form:

I typically begin by exploring the founder’s background, listening attentively to their story: their parents, family, and university years. I trace their journey from their first job to their most recent one, examining their thoughts, uncertainties, and actions, all the way through to the genesis of their entrepreneurial idea and its concrete execution. A thirty- to sixty-minute conversation is sufficient to gain a comprehensive understanding of an individual’s professional experience and to assess whether their venture is truly a lifelong commitment, as they claim.

A qualified entrepreneur should possess a highly relevant professional background, have experience in marketing and sales, have attempted similar ventures—whether successful or not—and have gained firsthand experience and deep insights from these endeavors.

Such individuals are extremely rare to find; they represent both the trials and joys for investors, as well as the barrier to entry in our investment sector. The Anlong Fund team comprises professionals with successful entrepreneurial experience, who provided the most significant support during the company’s early stages. This is also why we have been able to invest in numerous early-stage projects.

"Startup Project's "HumanThe authenticity of both “facts” and “matters” must be verified, which requires investors to draw on years of specialized knowledge and professional networks—a key factor behind the success of the Anlong Fund team.

Invest in trustworthy people, do trustworthy things; this is the core insight I have gained from years of investing in the healthcare sector.

Further Reading:

A Single CD-ROM: How Did This Company Spot a Business Opportunity in Hospital Medical Records?