State Council Announces DRG Payment Pilot: Will DRG-Based Cost Control Market Heat Up?

On June 28, under the directive of Premier Li Keqiang, the State Council issued what is regarded as the most significant healthcare insurance policy of 2017: the “Guiding Opinions of the General Office of the State Council on Further Deepening the Reform of Basic Medical Insurance Payment Methods.” The issuance of these Opinions will undoubtedly accelerate the reform process of medical insurance payment.

The "Opinions" clearly highlight five key points:

I. Implementation of a diversified, composite health insurance payment method;

II. Vigorously promote diagnosis-related group (DRG) payment;

III. Launch pilot programs for Diagnosis-Related Groups (DRG)-based payment;

IV. Improve payment methods such as capitation and per-diem payments;

V. Strengthen the supervision of medical practices by health insurance.

Five Requirements, Each Hitting the Mark.

For inpatient medical services, payment shall be primarily based on disease types and Diagnosis-Related Groups (DRGs); long-term and chronic inpatient care may be reimbursed on a per-diem basis. For primary healthcare services, capitation payments may be adopted, with active exploration of integrating capitation with chronic disease management. For complex cases and outpatient expenses unsuitable for bundled payments, fee-for-service reimbursement may be applied. Payment mechanisms tailored to the characteristics of Traditional Chinese Medicine (TCM) services shall be explored. Supervision by medical insurance over medical practices must be strengthened, shifting the regulatory focus from merely controlling medical costs to dual control of both medical costs and quality of care.

In fact, the State Council’s recent push is also evident from the series of policies issued in recent months and the operational developments of departments such as the National Health and Family Planning Commission.

Since 2016, a series of policies related to the reform of healthcare insurance payment methods have been successively introduced. On June 2, 2017, the National Health and Family Planning Commission held a launch meeting for the pilot program on Diagnosis-Related Group (DRG)-based payment and charging reforms in Shenzhen.

Policies Related to Healthcare Payment Reform

Changes in payment methods, apart from directly benefiting the general public, will also bring about a new round of reforms in healthcare insurance cost containment, which is closely linked to these changes. Before proceeding, let us review the several stages in the development of healthcare insurance payment systems and gain an understanding of the current status of healthcare insurance cost containment.

The Informatization of Medical Insurance Has Undergone Three Stages

The First Stage of the Development of Medical Insurance Payment, from 1998 to 2003. During this period, various regions across China began to gradually establish their own medical insurance systems in accordance with the urban employee medical insurance policy, completing the initial framework of the medical insurance system in terms of organizational structure and fund pooling. Starting from 2000, due to strong government support, social security informatization was rapidly implemented nationwide.

By the end of 2000, among the 349 prefecture-level and above pooling areas nationwide in China, 320 had introduced medical insurance system reform plans, accounting for 92% of the total; 284 pooling areas had implemented these reforms, representing 81% of the total, covering 43.32 million people. Throughout the year, the basic medical insurance fund recorded revenues of RMB 17 billion and expenditures of RMB 12.4 billion, with a cumulative balance of RMB 8.9 billion.

The Second Phase of Medical Insurance Payment Development, marking the construction phase of the Golden Social Security Project. From 2003 to 2007, with the establishment of social security systems across various regions in China, there was a managerial need for a top-down informatization management system.

In August 2003, the State Council officially approved the establishment of the Golden Social Security Project, a nationwide unified e-government initiative for labor and social security. Relying on a three-tier network infrastructure at the central, provincial, and municipal levels, and extending to grassroots institutions such as counties and townships, the project supports core applications including labor and social security business operations, public services, fund supervision, and macro-level decision-making.

Phase III,From 2007 to 2012. During this period, with the advancement of the “New Healthcare Reform” and the gradual improvement in health insurance coverage rates and payment standards, health insurance gradually assumed a critical role as a major payer in China’s healthcare system.

Throughout these three phases, fee-for-service has remained the primary method for hospital billing and health insurance reimbursement in China. Currently, fiscal subsidies from all levels of government account for only 8.22% of the actual operational expenditures of public hospitals at the county level and above. The remainder of hospital compensation is primarily derived from revenue generated through medical service activities.

Furthermore, public hospitals are subject to strict government pricing for medical services, with fee levels set far below the actual cost of care. This pricing structure fails to reflect the professional value of healthcare workers’ labor and is insufficient to cover the operational costs of hospital management.

Meanwhile, the absence of a clear application management mechanism for pharmaceuticals and medical consumables has led to revenue from these items becoming the primary means of hospital compensation. This is the fundamental reason behind the formation of the “drug-revenue-subsidized healthcare” compensation mechanism.

Under this compensation mechanism, healthcare institutions induce patient consumption through a fee-for-service payment model. The prescription of excessive medications, the misuse of high-value consumables, and the overuse of diagnostic tests have become the predominant manifestations of profit-driven behavior in hospitals, with these trends intensifying over time.

These mechanisms and tendencies have led to an increase in the sales volume of pharmaceuticals and medical consumables, as well as a rise in the utilization of diagnostic and laboratory tests, driving a rapid surge in healthcare costs. This has placed an unsustainable burden on medical insurance funds and increasingly exacerbated the financial burden of medical expenses for residents.

Cost containment in medical insurance has become an imperative policy decision for the state. Consequently, since 2011, the government has successively introduced relevant policies aimed at alleviating the financial burden on medical insurance funds through measures such as payment method reforms.

Against the backdrop of a government-led roadmap for healthcare system reform that leverages medical insurance cost containment as a financial tool and promotes the coordinated development of healthcare, medical insurance, and pharmaceutical sectors, new industrial forces have emerged. A cohort of healthcare IT companies equipped with core cost-containment technologies is now stepping into the spotlight.

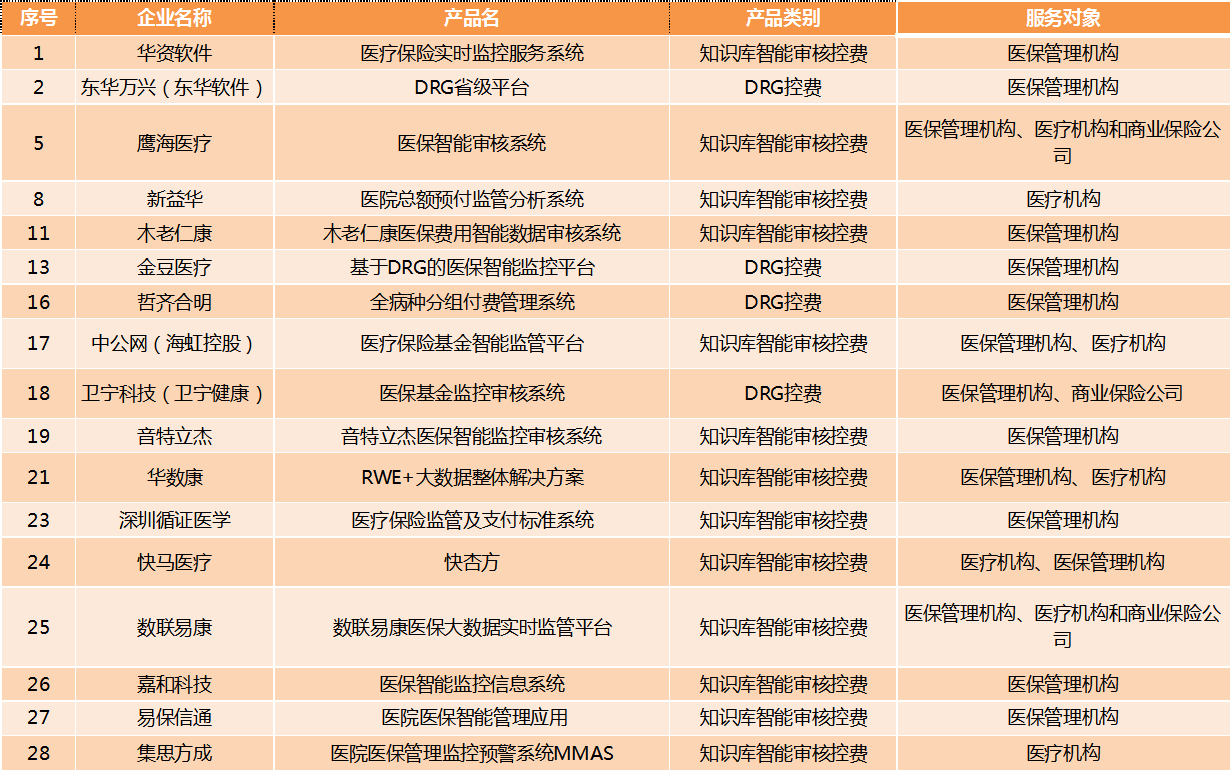

Information Technology Enterprises in the Medical Insurance Cost Control Market

VCBeat (WeChat ID: vcbeat) has compiled the domestic17 companiesIT Enterprises Related to Medical Insurance Cost Control (Excluding Listed Companies): The Following is an Overview of the Enterprises:

From the perspective of timing for cost-control interventions, medical insurance cost control is categorized into prospective control, concurrent control, and retrospective control.

1. Pre-event control refers to providing physicians with decision support and intelligent alerts for medication and prescription practices based on clinical pathway rules, thereby promoting more rational medical behavior;

2. In-process control refers to the timely detection of non-compliant data during the patient settlement process, preventing such data from being included in the settlement; this requires real-time interaction with the social insurance settlement system;

3. Post-event control is currently the primary approach, involving in-depth audits of settlement data and invoices to identify non-compliant transactions, followed by penalties imposed on healthcare institutions and insured individuals.

Specifically, the development of post-event control systems is primarily concentrated on the backend, such as within social security bureaus and commercial insurance providers, whereas pre-event control requires integration at the frontend with hospital information systems. Given the numerous stakeholders and business systems involved in cost containment, various enterprises can enter the medical insurance cost control market through different entry points.

From the perspective of cost containment categories, they are mainly divided into the following three types:

1. Intelligent Audit and Cost Control Based on Knowledge Base;

2. PBM Cost Control;

3. DRG Cost Control.

The “Three-Medical” linkage reform, driven by medical insurance cost containment as a lever, will inevitably lead to a restructuring of industrial value among service providers (hospitals and the pharmaceutical industry), demand-side participants (patients), and payers.

Amid increasing policy pressure, payers are gaining greater industry influence, and the technology, data, and service support provided by third-party medical cost-containment companies will become an indispensable backbone behind them.

Global Budget Payment System

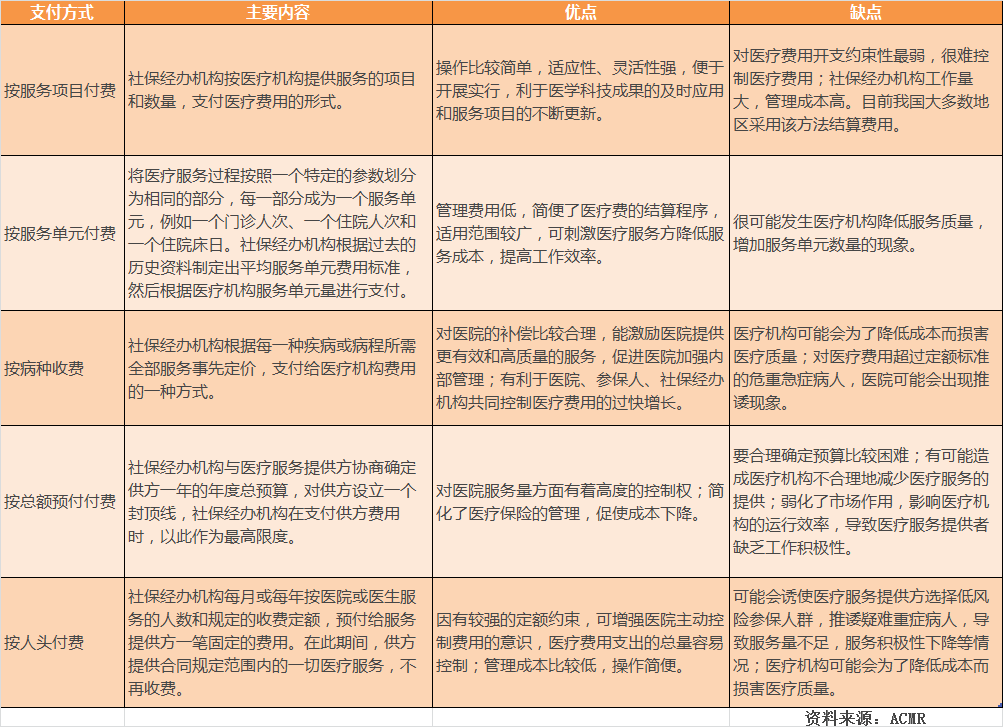

Reform of Medical Insurance Cost Control: A Key Component Is the Reform of Payment MethodsA crucial aspect of medical insurance cost-control reforms is the transformation of payment mechanisms. This involves gradually transitioning from fee-for-service models to alternative approaches such as capitation, diagnosis-related group (DRG) payments, and global budgeting. Practical implementations across various regions in China have predominantly adopted global prospective payment systems as the primary method, supplemented by other payment modalities.

Pros and Cons of Various Payment Methods

Global Budgeting: A payment method in which government departments or insurance agencies, after comprehensively evaluating and calculating hospital service performance, negotiate with hospitals to establish an annual total budget as the maximum payment limit.

Global Budgeting is a highly straightforward health insurance cost-containment mechanism: based on the fund utilization in the previous year, plus a reasonable growth rate, it establishes the total annual reimbursement cap for healthcare institutions, thereby setting an upper limit on health insurance expenditures.

The advantages of the global budget system lie in eliminating the economic incentive for healthcare providers to deliver excessive medical services, thereby effectively controlling the unreasonable growth of medical expenses. Since costs under a global budget are fixed, hospitals can proactively plan in advance and utilize healthcare resources rationally. Furthermore, this payment settlement method is straightforward, helping to reduce administrative costs.

However, there are also drawbacks. Under the “hard constraint” of a fixed global prepaid budget, healthcare providers may underprovide services and experience a decline in quality of care. Moreover, given the numerous uncertain factors affecting the global budget and the substantial room for rent-seeking, determining hospitals’ annual global budgets is extremely difficult. Once budget caps become tight, shifting patients away becomes the easiest recourse. The “Qinling dilemma” that erupted in Shanghai in the second half of 2012 serves as a pertinent example.

Global budgeting schemes simplify the overall management of health insurance funds, but fail to incentivize healthcare institutions’ intrinsic motivation for cost containment.

In the “Opinions” issued by the State Council, certain improvements have been made to the global budgeting system:

● For medical institutions that reasonably increase their workload beyond the total budget control indicators, compensation may be provided in accordance with the agreement based on performance assessments.

● Total expenditure control targets should be appropriately tilted toward primary healthcare institutions, pediatric medical institutions, and others; the formulation process shall be disclosed to medical institutions, relevant departments, and the public in accordance with regulations.

● Regions with the necessary conditions should actively explore integrating the point-based payment method with global budget management and diagnosis-related group (DRG) payment, gradually replacing institution-specific global budget controls with regional (or defined-scope) global caps on medical insurance funds.

To better incentivize medical institutions to proactively control costs, it is necessary to adopt a composite payment model that combines global budgeting with capitation, case-based payment, and DRG-based cost containment.

Among the 17 companies profiled by VCBeat, the vast majority are enterprises that leverage knowledge bases for intelligent claims review and cost control. However, with the diversification of payment methods and the development of commercial insurance, these companies are gradually transitioning toward two directions: Pharmacy Benefit Management (PBM) and Diagnosis-Related Groups (DRG).

PBM Cost Containment: Repeated Setbacks

Pharmacy Benefit Management (PBM) is a specialized third-party service that acts as an administrative coordinator among insurance providers, pharmaceutical manufacturers, hospitals, and pharmacies. Its primary objective is to effectively manage healthcare costs, reduce expenditures, and enhance the value of pharmaceutical care.

PBMs enter into contracts with pharmaceutical companies, healthcare providers, insurance companies, or hospitals to influence the prescribing behaviors of physicians and pharmacists, thereby controlling the growth of drug costs without compromising the quality of medical services. The core objective of PBMs is to enhance the efficiency of health insurance fund utilization, and their revenue model involves charging management fees to the institutions they represent and to pharmaceutical manufacturers.

The success of ESI, a renowned PBM company abroad, is largely attributed to its robust support from clinical medicine and prescription standard databases. However, for Chinese enterprises, several hurdles must be overcome to truly implement PBM.

In China, social insurance accounts for a substantial proportion of healthcare expenditures. The pressure to control costs falls primarily on medical insurance administrative authorities, which rely mainly on administrative measures rather than market-based mechanisms. Consequently, the role of third-party cost-control platforms has not been effectively leveraged.

Part of the reason for the difficulties encountered by Pharmacy Benefit Managers (PBMs) in China lies in the entrenched interests tied to prescriptions. Although policies now mandate the separation of prescribing from dispensing, hospitals continue to derive substantial benefits from the prescription circulation process. The core function of a PBM is the review and modification of prescriptions; thus, it is challenging to persuade hospitals to relinquish this authority in the short term.

Another core component of PBM is the formulary. However, as medical insurance formularies across different regions in China have yet to be unified, developing a nationwide solution remains impractical. Furthermore, the authority to formulate these formularies currently resides with government medical insurance administrative departments. Unless this authority is delegated or distributed to commercial insurance companies, PBM development will inevitably remain limited to a small scale.

Although the development of Pharmacy Benefit Managers (PBMs) has faced numerous obstacles, it is not without a way forward; the rise of commercial insurance has presented PBMs with new opportunities.

Commercial insurance companies often require data support when designing products. For instance, data on the number of individuals in high-risk groups for complications can underpin the development of innovative insurance products. Only with such data can insurers more accurately target local populations, thereby ensuring their products better align with local needs.

Therefore, collaboration between commercial insurance companies and healthcare cost-control enterprises can enable them to develop products that better align with actual market needs.

Since commercial insurers administer the government’s critical illness insurance program, regulatory measures are equally necessary in this domain to identify fraud and abuse, medical waste, and overtreatment. Establishing a risk management system is essential to reduce premium costs.

Once healthcare cost-containment companies obtain prescriptions outside the scope of basic medical insurance, they gain greater leverage in negotiations with pharmaceutical distributors, thereby securing medications at lower prices. Taking Express Scripts, Inc. (ESI) as an example, its annual revenue in 2013 amounted to $104.1 billion, of which only $1.231 billion came from service fees, while the remaining $102.8 billion was generated from drug distribution activities.

Furthermore, medical insurance cost-control companies can also assist hospitals in providing services such as health management, helping patients with disease prevention and control, thereby reducing medical expenses.

DRG Cost Control: Managing Costs Through Payment Methods

DRG stands for "Diagnosis-Related Groups." It classifies patients into several "Diagnosis-Related Groups" based on factors such as the severity of the inpatient's condition, the complexity of treatment methods, the level of resource consumption (cost) for diagnosis and treatment, as well as comorbidities, complications, age, and hospital discharge outcomes. Prices, charges, and health insurance payment standards are determined on a bundled basis per group.

Under this bundled payment model, medications, medical consumables, and diagnostic tests used by patients become costs of care delivery rather than sources of revenue for hospitals.

Following the implementation of the Diagnosis-Related Groups (DRG) payment system, it not only serves as an effective guide for standardizing medical practices but also acts as a strategic directive for hospital operations. DRG plays a significant role in fostering cost-awareness among healthcare professionals, preventing overdiagnosis, excessive testing, and overprescribing, thereby promoting greater operational efficiency within hospitals.

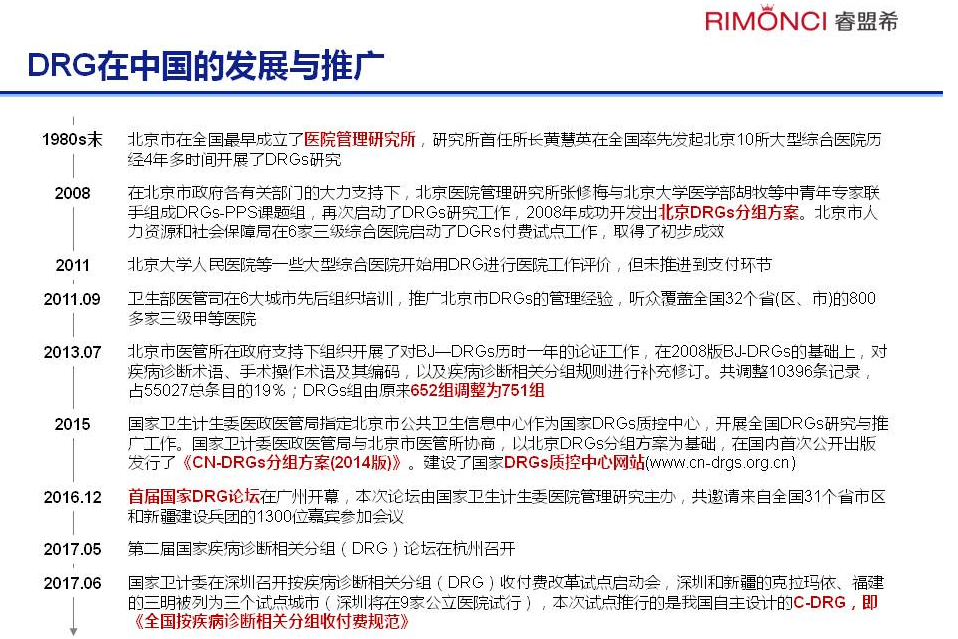

A review of the history of DRG development reveals that there is no single DRG system in China. Multiple variants exist, including BJ-DRGs, CN-DRGs, and C-DRG.

Currently, only a handful of companies in China, such as Jindou Medical, have adopted DRG-based cost containment. Although the number is relatively small, with the frequent introduction of national policies, it is expected that more healthcare cost-containment enterprises will enter the DRG market in the future.

From a timeline perspective,It is already 2017, and the distance fromIn 2020, with less than three years remaining. To achieveWith the reform of health insurance payment methods covering all medical institutions and services, aiming for a significant reduction in the proportion of fee-for-service payments, the State Council has also had to step up its efforts.

The issuance of these “Opinions” is likely to play a crucial role in the coming years.