2017 Global Digital Health Innovation Trends in Oncology Report with Case Studies of the Top 5 U.S. Cancer Hospitals

“Tumors,” whether for the general public or physicians, remain a deeply sensitive and intractable challenge of our time. Often described as “an ancient and mysterious disease,” humanity has been battling it for 4,000 years.

For centuries, patients suffering from this disease have become the subjects of almost every conceivable experiment. In the quest for some effective remedy to treat this intractable illness, no stone was left unturned—from fields and forests to pharmacies and temples. Nearly all animals were conscripted into service, contributing everything from hair and skin to teeth and nails, thymus and thyroid glands, liver and spleen. — The Emperor of All Maladies: A Biography of Cancer

With the evolution of the times and advancements in medical research, public understanding of cancer has continuously improved, and significant progress has been made in diagnostic and therapeutic approaches. Examples include the continuous launch of new oncology drugs, innovative breakthroughs in cancer diagnostic technologies, and advances in personalized cancer treatment. Consequently, there is an expanding array of options for cancer therapies and diagnostic techniques.

In recent years, with improvements in economic living standards, a shift in user perspectives on health needs, and the gradual maturation of emerging technologies such as biosensors, artificial intelligence, and 3D printing, the traditional oncology industry has been undergoing continuous innovation and transformation, giving rise to a new industrial paradigm.

VCBeat aims to review the entire oncology innovation industry chain, using innovative technologies and business models as entry points for analysis and discussion, to provide new perspectives for professionals in the oncology-related industries.

The core discussion of this report will center on “oncology innovation,” referring to innovative products, models, and trends emerging from the integration of oncology with emerging technologies such as gene sequencing, artificial intelligence, and biosensors. The content is primarily divided into six sections: an overview of the overall oncology market; analysis of the digital innovation industry chain in oncology; commercial opportunities for digital innovation in the oncology industry; trends in digital innovation among industry giants in oncology; investment and financing analysis of China’s oncology digital innovation industry; and case studies of the Top 5 cancer specialties at the best hospitals in the United States.

The main contents of the report are as follows:

1. Overview of the Overall Market in the Oncology Industry

1.1 Current Status of the Oncology Industry

1.2 Needs from Key Stakeholders in Oncology Healthcare Services

1.3 Favorable Policy Environment

1.4 Innovation Opportunities Brought by Digital Technology

2. Industry Chain Relationships in the Digital Oncology Innovation Market

2.1 Oncology Industry Chain Relationship Diagram

2.2 21 Areas of Integration Between Digital Technologies and the Five Stages of Oncology Diagnosis and Treatment

2.3 Technical/Market Architecture of the Oncology Innovation Industry

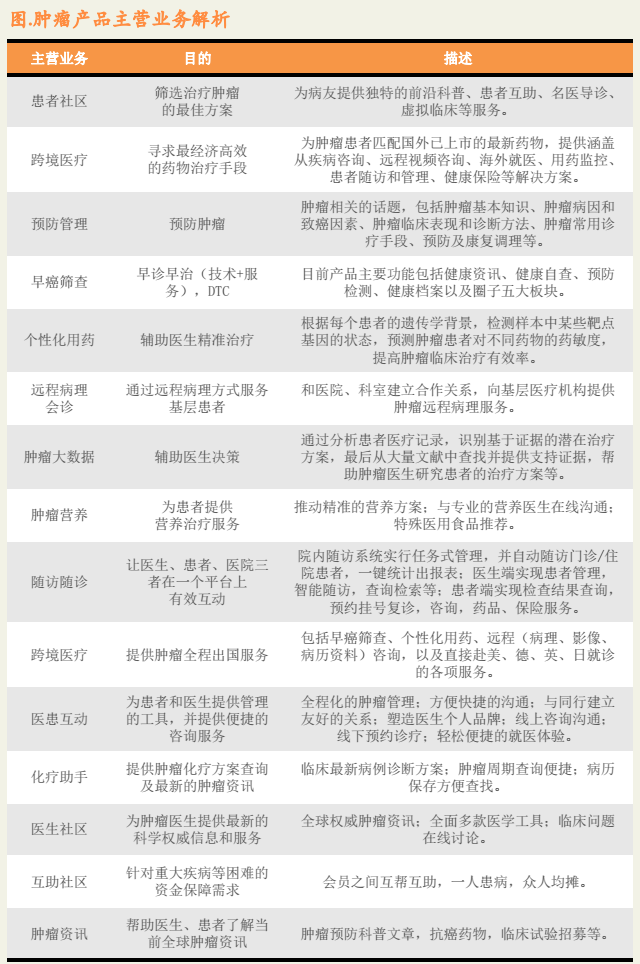

2.4 Analysis of Core Business in Oncology Products

3. Business Opportunities in Digital Innovation for the Oncology Industry

3.1 Opportunity 1: Early Cancer Screening

3.2 Opportunity 2: New Technologies Facilitating Early Diagnosis

3.3 Opportunity 3: Breakthroughs in Personalized Treatment Modalities

3.4 Opportunity 4: Nutritional Therapy for Oncology Rehabilitation

4. Trends in Digital Innovation in Oncology Among Industry Giants

5. Investment and Financing Analysis of China’s Digital Innovation Industry in Oncology

5.1 Analysis of the Entrepreneurial Market for Digital Innovation in China’s Oncology Industry

5.2 Analysis of the Financing Market for China’s Digital Innovation Industry in Oncology

6. Appendix: Top 5 Hospitals for Cancer Care in the United States, 2016–2017

This article excerpts Parts I, II, and V of the report; case studies of domestic and international enterprises are presented in Parts III, IV, and VI. Scan the QR code at the end of the article to become a member and gain access to the full report.

Overview of the Overall Market in the Oncology Industry

Characteristics of the Oncology Industry

Current Status of the Patient Side in Oncology

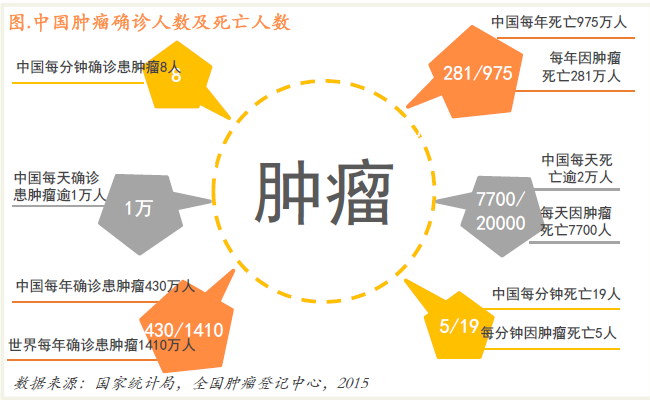

In recent years, malignant tumors have become the leading cause of death worldwide, evoking widespread fear and anxiety. This apprehension stems not only from a lack of professional knowledge but also from the high incidence, low survival rates, and high mortality associated with cancer. According to an analysis of 2015 cancer statistics in China, jointly published by Professor Chen Wanqing, Director of the National Central Cancer Registry, and colleagues in *CA: A Cancer Journal for Clinicians* (impact factor: 144.8), there were approximately 4.292 million new cancer cases and over 2.814 million cancer-related deaths in China in 2015. This translates to an average of eight new cancer diagnoses and five cancer-related deaths every minute.

If this trend continues, with the accelerating pace of population aging, the number of cancer patients will increase year by year. Relevant research and analysis indicate a positive correlation, meaning that the trend in population aging aligns with changes in cancer incidence rates. Furthermore, the age group of 30–44 years is a critical period during which many diseases undergo an order-of-magnitude change; for instance, the incidence rate of colorectal cancer has increased tenfold. Meanwhile, individuals aged 65 and older account for the largest proportion of cancer cases, at approximately 55.36%.

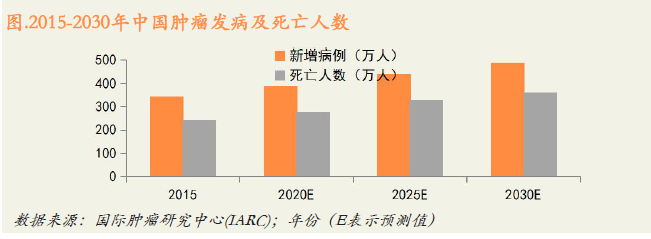

The 2016 report from the American Society of Clinical Oncology (ASCO) projected that the number of cancer patients diagnosed globally would reach 22 million by 2030. Given China’s large aging population and exposure to risk factors such as air pollution and food safety issues, its cancer incidence rate is expected to be even higher. According to estimates from a report by the International Agency for Research on Cancer (IARC), China is projected to have 4.87 million new cancer cases and 3.6 million cancer-related deaths in 2030. However, based on surveys conducted by Professor Chen Wanqing and colleagues, the future demand for cancer diagnosis and treatment services in China will far exceed this projected growth.

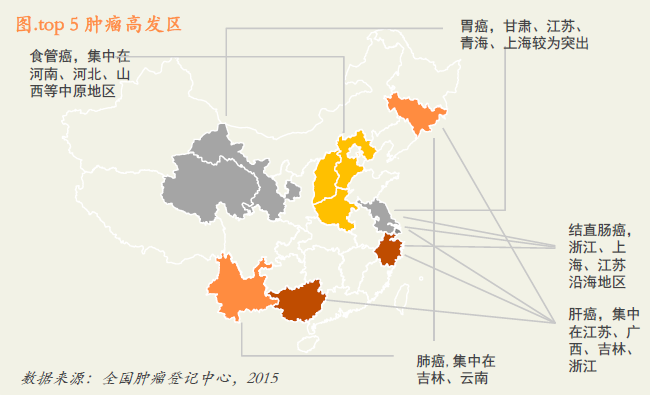

Among these, lung cancer is the most prevalent malignancy and the leading cause of cancer-related mortality. Gastric cancer, esophageal cancer, liver cancer, and colorectal cancer are common malignancies in China with high incidence and mortality rates, closely following lung cancer. Analyses have revealed that cancer is closely associated with geographic region, environment, and diet. For instance, in the Central Plains regions such as Henan, Hebei, and Shanxi provinces, long-term consumption of food that is eaten too quickly, is overly coarse, excessively hot, or highly salty leads to damage of the esophageal mucosa, thereby increasing the risk of esophageal cancer. In coastal areas, susceptibility to viral hepatitis infections, combined with a humid and hot climate that favors the proliferation of aflatoxins, contributes to a higher incidence of liver cancer.

Current Status of Oncology Medical Services

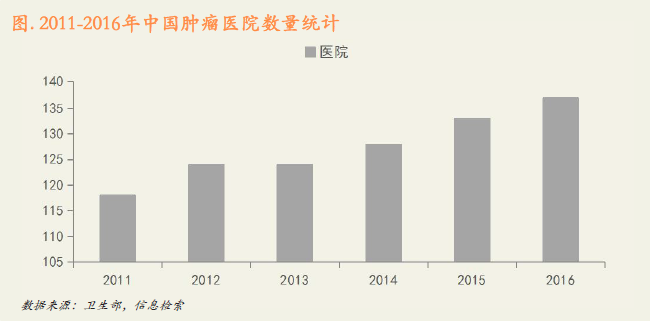

As of the end of 2016, according to data from the National Health and Family Planning Commission and publicly available information, there were 137 oncology hospitals in China, with over 20,000 oncology specialists. In contrast, there were more than 4 million new cancer cases annually. The supply of oncologists was far insufficient to meet patient demand, resulting in significant difficulties in accessing medical care and hospital admission.

In terms of market size, given that China sees 4 million new cancer cases annually, with an average hospitalization cost of RMB 24,018 per patient, and considering that patients typically require multiple hospitalizations during treatment—resulting in total costs of approximately RMB 60,000–80,000—the conservative estimate for cancer treatment expenses rises to around RMB 100,000 when maintenance therapy costs are included. Consequently, the overall market size for oncology care in China has exceeded RMB 400 billion.

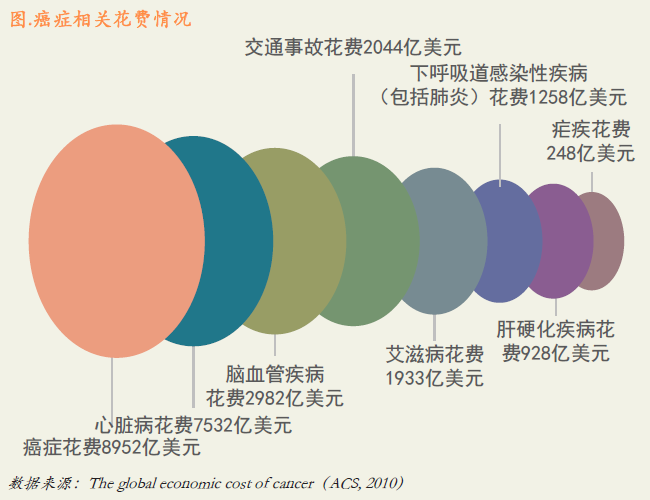

According to the American Cancer Society’s 2010 survey on cancer-related expenditures, annual losses attributable to cancer—including medical costs, disability, and mortality—resulted in cancer-related expenses far exceeding those of all other health conditions combined, reaching $895.2 billion. This implies that the domestic market size in China is already approaching half of this figure.

Needs from Key Stakeholders in Oncology Healthcare Services

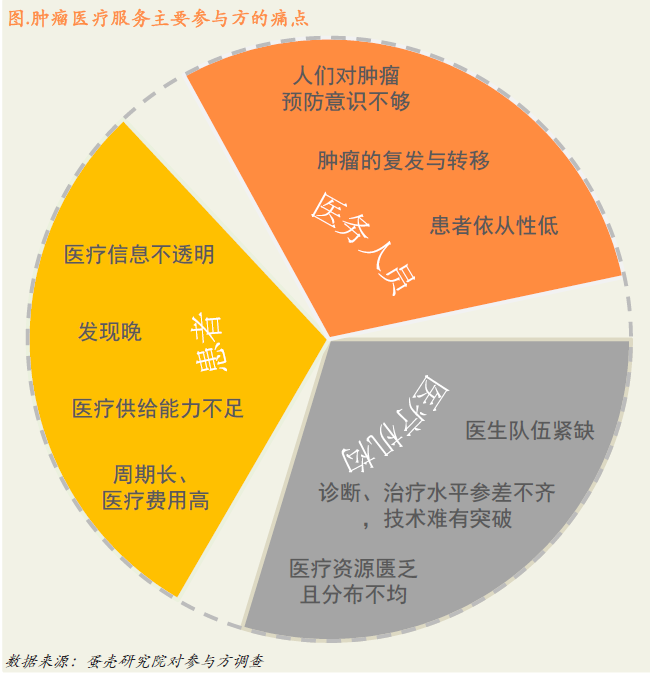

The most critical segment of the oncology industry is medical services, while other sectors such as pharmaceuticals and medical devices primarily serve to facilitate the efficient, high-quality, and convenient delivery of these services. The key stakeholders involved in medical services include healthcare institutions, medical professionals, and patients. Their prominent pain points are manifested in insufficient medical supply capacity and the “three difficulties” faced by patients. For instance, specialized oncology hospitals in China are predominantly concentrated in first-tier cities across provinces such as Hebei, Henan, Shandong, Jiangsu, and Sichuan. This distribution is uneven, with more facilities in the north than in the south, and a higher concentration in economically developed cities. The quality of care at oncology hospitals varies significantly; the majority are public institutions, with only a few being private. While medical professionals generally aspire to see a reduction in cancer incidence and an improvement in patients’ five-year survival rates, these goals are often thwarted by broader environmental factors. From the patient’s perspective, the primary desire is to avoid developing cancer altogether; if it does occur, the hope is for timely detection, treatment, and recovery. According to surveys and interviews conducted by VCBeat with various stakeholders, the main needs are as follows:

Favorable Policy Environment

In recent years, with the rapid development of technologies such as “Healthcare + Internet,” the Chinese government has continuously introduced favorable policies to vigorously promote industrial innovation. As one of the major diseases, oncology is undoubtedly advancing rapidly under the guidance of a series of policies. Below, we primarily analyze this trend from three policy perspectives:

Commercial Health Insurance Is Poised to Take Center Stage

The Chinese government has successively introduced a series of relevant policies to maximize the development of commercial health insurance. Since September 2013, the State Council has issued the “Several Opinions of the State Council on Promoting the Development of the Health Service Industry” and the “Several Opinions of the State Council on Accelerating the Development of the Modern Insurance Service Industry,” both of which explicitly include support for the development of commercial health insurance. Subsequently, the “Several Opinions on Accelerating the Development of Commercial Health Insurance” was released. The growth of commercial health insurance will facilitate the expansion of insurance coverage for major diseases such as cancer.

If commercial health insurance participates in basic medical insurance according to market competition rules, it will help resolve three major challenges: the lack of separation between management and operation of medical insurance funds, the increasing fiscal pressure caused by rising medical costs, and the misuse of medical insurance funds.

Some institutions predict that by 2020, China's commercial health insurance premiums are expected to reach RMB 500 billion to RMB 700 billion, making it one of the three major business segments alongside property and casualty insurance and life insurance.

Tiered Diagnosis and Treatment Promotes the Gradual Decentralization of Oncology Care Resources

In September 2015, the General Office of the State Council released the “Guiding Opinions on Promoting the Construction of a Tiered Diagnosis and Treatment System” to the public. It proposed that by 2017, the proportion of diagnoses and treatments conducted at primary healthcare institutions would increase significantly within the total volume of medical services, resulting in a more rational and standardized order for seeking medical care; by 2020, a tiered diagnosis and treatment model characterized by “initial consultation at primary care facilities, two-way referrals, separate management of acute and chronic conditions, and coordination between upper- and lower-level institutions” would be gradually established. The Guiding Opinions required that chronic diseases such as hypertension, diabetes, cancer, and cardiovascular and cerebrovascular diseases serve as breakthrough points to clarify and implement the diagnostic and therapeutic service functions of medical institutions at all levels, improve the service chain encompassing treatment, rehabilitation, and long-term care, and provide patients with scientific, appropriate, and continuous diagnostic and therapeutic services.

Under policy guidance, many provinces and cities have explored the implementation of tiered diagnosis and treatment within urban areas, designating pilot programs and including chronic diseases such as hypertension, diabetes, cancer, respiratory diseases, and cerebrovascular diseases in the tiered diagnosis and treatment framework. For instance, in March 2016, the Health and Family Planning Commission of Hexi District, Tianjin, explored the establishment of a medical consortium for cancer prevention and treatment between the District Traditional Chinese Medicine Hospital and the Municipal Cancer Hospital. Over the following six months, the number of outpatient cancer patients at the Traditional Chinese Medicine Hospital increased from 220 to 597, a year-on-year increase of 34%, while hospitalized cancer patients rose by 25%. This initiative achieved comprehensive, full-cycle services for cancer prevention, treatment, and rehabilitation, enabling patients to access cancer rehabilitation care within their communities.

It is foreseeable that, guided by national policy trends promoting tiered diagnosis and treatment, telemedicine, and the enhancement of primary healthcare capabilities, the gradual decentralization of oncology treatment resources is an inevitable trend. Considering the current state of China’s oncology medical services market, large public specialized hospitals hold the highest level of technical expertise and physician resources within the entire system, while oncology departments in lower-tier hospitals and privateSpecialized oncology hospitals have relatively limited resources; therefore, we believe that healthcare information systems centered on remote consultations and tiered diagnosis and treatment will facilitate the decentralization of high-quality medical resources and expand their reach.

Gradual Liberalization of Gene Sequencing

Industry policies have evolved from the joint moratorium imposed by the National Health and Family Planning Commission (NHFPC) and the China Food and Drug Administration (CFDA) in 2014, to the approval of sequencing products from companies such as BGI Genomics and Daan Gene, the designation of pilot units for personalized medical testing, and the issuance of industry standards for personalized tumor medication. These developments signal that gene sequencing applications in tumor screening and personalized treatment are poised for rapid growth.

Industrial Application Innovation Opportunities Brought by Digital Technologies Such as Artificial Intelligence

As new-generation digital technologies, represented by artificial intelligence, cloud computing, and big data, converge with oncology, the cancer care industry is entering an era of technological integration. The industry will become increasingly digitalized, with applications gradually covering the entire spectrum of cancer diagnosis and treatment services, thereby unlocking immense potential for innovation. Companies possessing proprietary technologies are poised to lead this transformative wave.

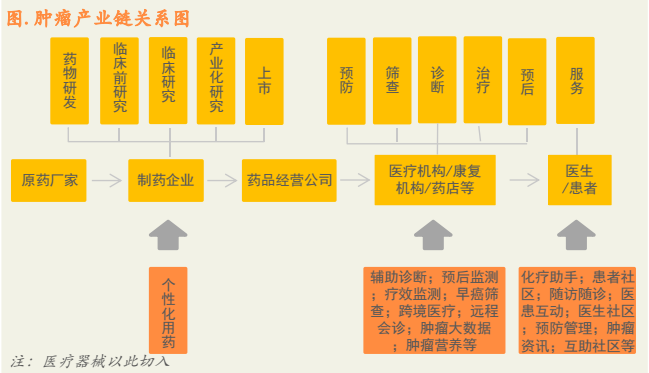

Industrial Chain Relationships in the Oncology Digital Innovation Market

Based on the entire workflow of oncology diagnosis and treatment services, we categorize the cancer industry into five stages: prevention, screening, diagnosis, treatment, and prognosis. Driven by new technologies, these five stages have given rise to innovative models distinct from traditional approaches, aiming to promote innovation in the cancer industry from various perspectives.

The industrial chain of the traditional oncology sector has become increasingly mature, evolving into a scaled, economically efficient value chain that spans from upstream active pharmaceutical ingredient (API) and raw material manufacturers to pharmaceutical and medical device companies, and finally to end-point service providers. Driven by emerging technologies, market demand, and capital investment, innovation in both industry value chains and business models has become more vibrant, disrupting traditional paradigms and integrating novel approaches across various entry points.

According to statistics from VCBeat, there are currently over one hundred companies of varying sizes in China’s innovative oncology industry. These entities primarily enter the market through pharmaceutical manufacturers, enterprises, medical institutions/rehabilitation centers/pharmacies, and service providers or stakeholders such as patients and physicians, leveraging technological innovations to optimize oncology diagnosis and treatment workflows.

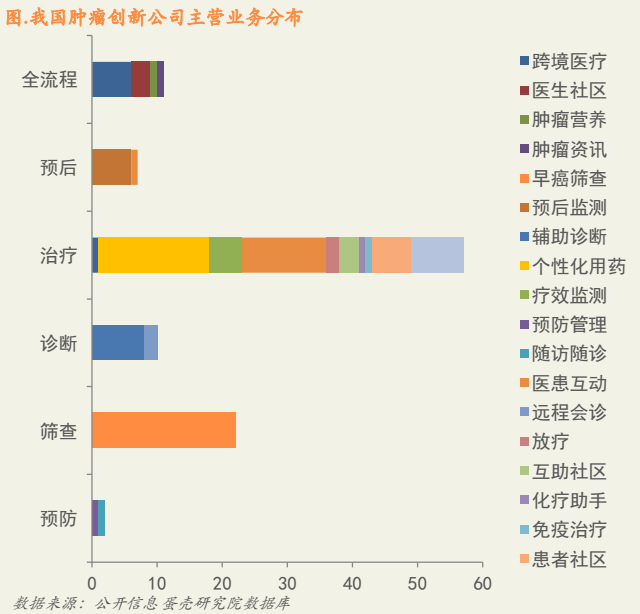

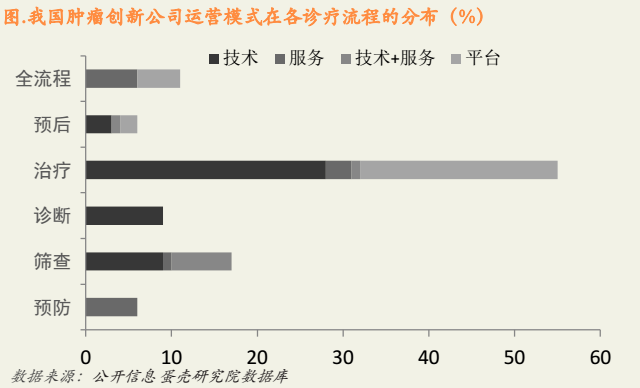

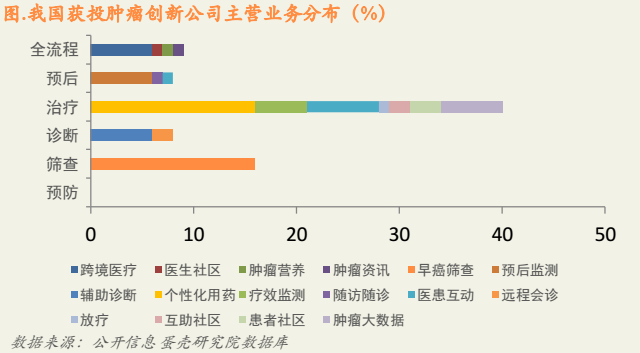

Across the five major service stages—prevention, screening, diagnosis, treatment, and prognosis—the drive of new technologies has given rise to innovative models unlike any before, leading the continuous upgrading of industrial structure under the new normal. According to statistical analysis by VCBeat Research Institute, core businesses are distributed across 21 fields, with a focus on early cancer screening, doctor-patient interaction, and personalized medication. Moreover, innovation models originating from the treatment stage are the most diverse, while those in other service stages appear relatively singular and homogeneous.

The oncology industry is a sector that requires the integration and cross-pollination of cutting-edge technologies (such as gene sequencing, bioinformatics, and nanotechnology) with foundational technologies (such as network and communication technologies). Cutting-edge technologies enhance the precision of oncology diagnosis and treatment services, while foundational technologies serve as the underlying infrastructure, ensuring the orderly operation of the entire new industrial chain.

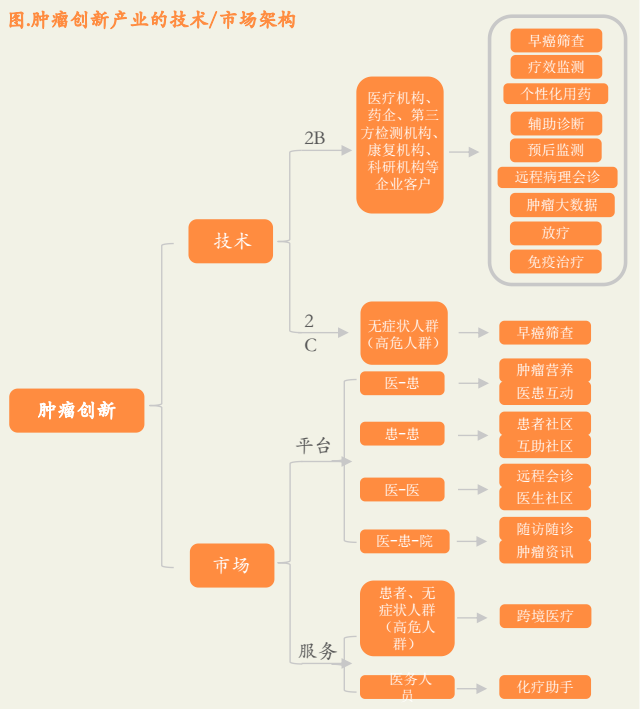

From the perspectives of technology and market, respectively: On the technology front, there are pure technology supplies targeted at B-side enterprises, such as innovative products like personalized medication and system software like remote pathology consultation. Technologies aimed at C-side users primarily involve innovative models directly facing consumers, focusing on making products more convenient and efficient, such as early cancer screening. In terms of the market, it is mainly divided into two categories: platforms and services. Platforms include four types: doctor-patient, doctor-doctor, patient-patient, and doctor-patient-hospital, facilitating interactive communication among two or more groups. Examples include remote consultations and physician communities on doctor-doctor platforms, as well as patient communities and mutual aid communities on patient-patient platforms. Services mainly provide cross-border healthcare, physician tools, and other offerings to C-side patients, asymptomatic individuals (high-risk groups), and medical personnel. This also includes leveraging third-party technologies to deliver services to asymptomatic individuals and others, even if the service provider does not possess its own proprietary technology.

According to VBInsight’s assessment of all innovative oncology products, early cancer screening solutions account for the largest share, followed by personalized medication and doctor-patient interaction products. Light-touch preventive management and oncology information services represent a smaller proportion. The analysis suggests that, as oncology is a critical disease area with a complex landscape of served and participating populations due to disease heterogeneity, light-touch models struggle to generate cash flow and exhibit weak user stickiness. Therefore, it is more appropriate to integrate the characteristic features of light-touch models into heavy-touch product offerings.

Analysis of Investment and Financing in China's Innovative Oncology Industry

Overview of Venture Capital

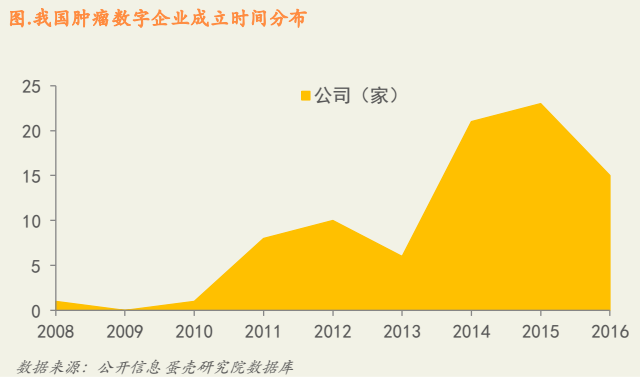

As of December 2016, VCBeat conducted statistics and analysis on 85 innovative oncology companies established across China. Among them, 62 companies had publicly disclosed financing information. The venture capital analysis is as follows:

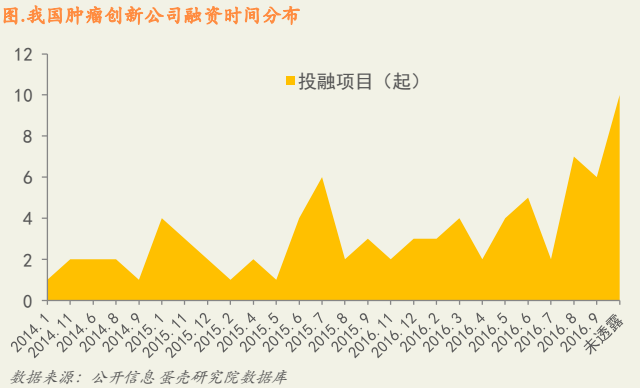

2014 and 2015 were the two peak years for project establishment;

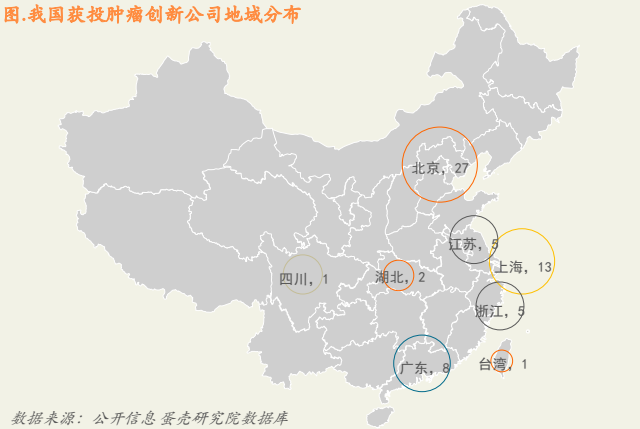

Innovative projects are led by Beijing and distributed across 10 provinces (municipalities);

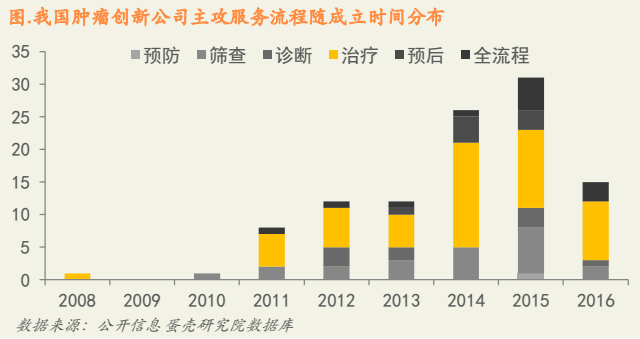

The primary entry point for innovation is the treatment phase, with key focus areas including adjuvant therapy, personalized medication, doctor-patient interaction, remote consultation, oncology big data, and medical imaging;

The startup project primarily targets medical institutions, followed by platform-based users (patients and healthcare professionals) and individual patient clients.

The peak financing periods were concentrated in the middle to late parts of 2015 and 2016;

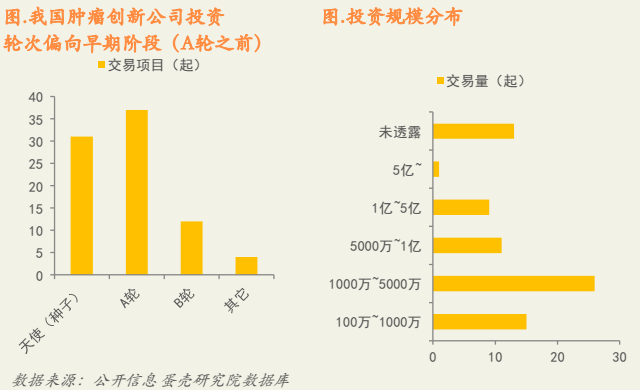

Projects tend to be at the pre-Series A stage, with transaction volumes concentrated between RMB 10 million and RMB 50 million;

The treatment phase accounts for the highest proportion of startup financing, while patient tools, physician tools, and medical expenses account for the lowest proportions.

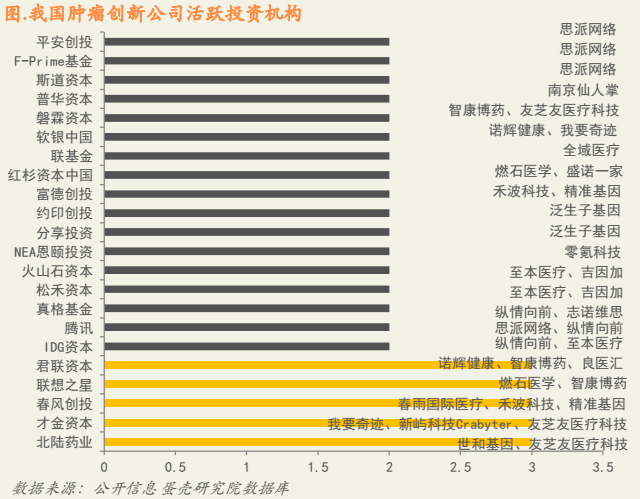

Twenty-two institutions have participated in two or more investment and financing transactions for innovative oncology projects. Active institutions include Beilu Pharmaceutical, Caijin Capital, Chunfeng Venture Capital, Legend Star, and Junlian Capital;

Startup Market

1) Over the past three years, China’s oncology innovation companies have experienced explosive growth. Prior to 2013, fewer than 10 new oncology innovation companies were established annually. With the application of digital technologies such as the internet and big data, oncology innovations have gradually been adopted in the market. In 2014, 21 oncology innovation enterprises were founded, marking the inaugural year of digital innovation in oncology. This growth was significantly propelled by President Obama’s “Precision Medicine” initiative announced in early 2015 and the establishment of China’s National Expert Committee on Precision Medicine Strategy.

2) The market for innovative oncology applications has primarily undergone two stages of development: the surge in therapeutic products in 2014, and the emergence of therapeutic, screening, and end-to-end workflow products in 2015. Notably, the pace of entrepreneurial activity in therapeutic projects slowed down in 2015.

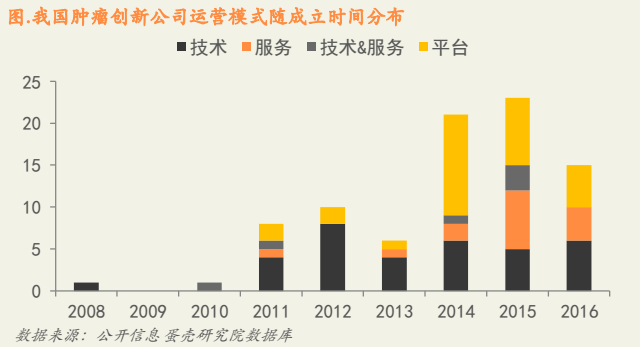

3) Technological products have exhibited limited volatility, maintaining relatively stable growth in recent years after peaking in 2012. With the development of underlying technologies such as the internet, service- and platform-based products have gradually become popular vehicles for startups since 2014.

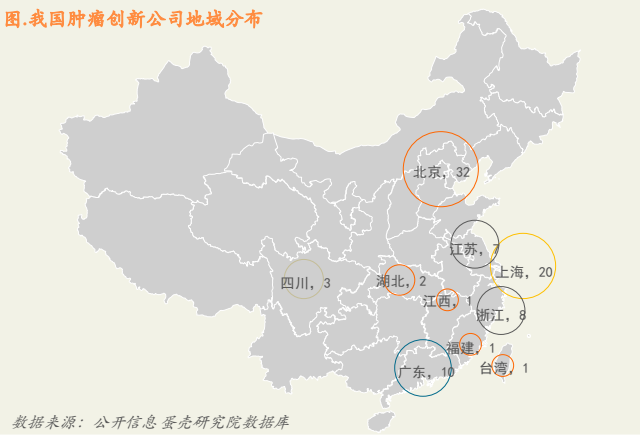

4) China’s innovative oncology companies are primarily concentrated in Beijing and distributed across ten major provinces, municipalities, and autonomous regions. The top three locations are Beijing (32 companies), Shanghai (20 companies), and Guangdong Province (10 companies). These hubs are predominantly resource-rich coastal cities that drive development in inland regions. The scope of entrepreneurship is expected to expand rapidly in the coming years. In addition to technological and economic considerations, areas with high cancer incidence will become a key factor in location decisions.

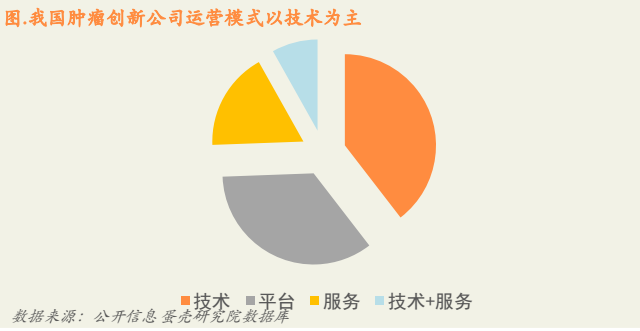

5) Operational models are primarily categorized into four types. The technology-driven model focuses on providing technical support to large entities such as medical institutions, research organizations, and third-party testing laboratories. The service-oriented model mainly leverages (mobile) internet services to cater to specific groups, such as patients and healthcare professionals, and also involves collaborations with third-party technology providers to deliver technologies directly to end consumers. The platform-based model facilitates interactions among two or more parties; in the context of innovative oncology care, this is primarily manifested as patient-physician interaction platforms. The “Technology + Service” model utilizes the company’s proprietary technologies to serve both B-end enterprises and C-end individual users.

6) Oncology innovators are most active in therapeutic initiatives and least engaged in prevention. Their primary entry points include early cancer screening within screening services, personalized medication during treatment, and doctor-patient interaction, with relatively fewer ventures focused on prevention and prognosis. This distribution correlates with the fact that public awareness of oncological health is still in its nascent stage. In the long term, however, an increasing number of innovative companies are expected to emerge in these two areas.

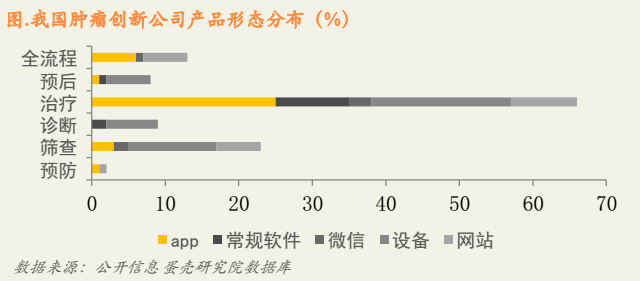

7) Product forms are categorized into five types: mobile apps, conventional software, WeChat (providing services exclusively through the WeChat channel), devices, and websites. As the number of innovative projects increases, the volume of conventional software, WeChat-based, and device-related products will grow, while the proportions of mobile apps and websites will tend to stabilize.

8) Technologies are primarily focused on the screening, diagnosis, and treatment service workflows; services encompass the entire care continuum and prevention; the “technology + service” lightweight and convenient model is centered on screening, while platforms are focused on treatment.

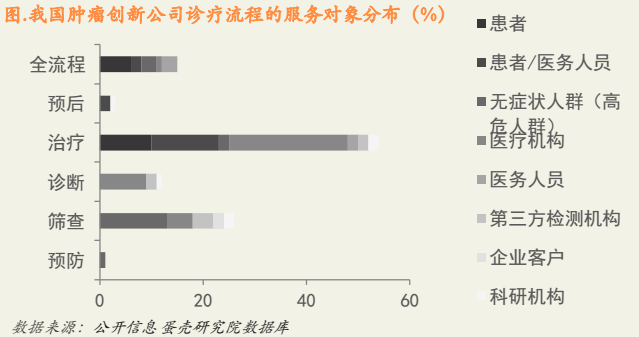

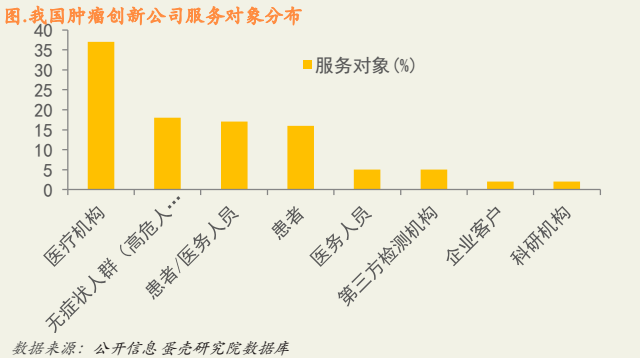

9) The users are mainly divided into eight categories, including single-group users such as patients, healthcare professionals, and asymptomatic individuals (high-risk groups), as well as platform-based users comprising patients and healthcare professionals, along with large enterprise entities such as medical institutions and third-party testing agencies.

10) The target population primarily comprises eight categories, with the top three being medical institutions, asymptomatic individuals (high-risk groups), and patients/healthcare workers.

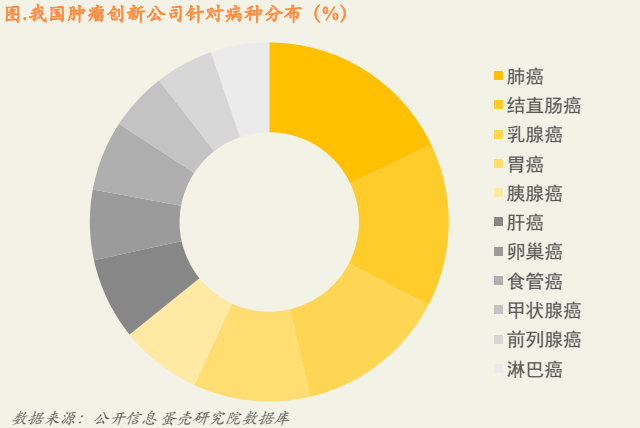

11) The top five cancer types with the highest concentration of startups are lung cancer, colorectal cancer, breast cancer, gastric cancer, and pancreatic cancer. Compared to the top five cancers in China by incidence and mortality rates, esophageal cancer and liver cancer are less represented.

Financing Market

1) As of December 2016, a total of 62 innovative oncology projects across China had secured financing, involving 84 funding transactions with a total amount exceeding RMB 3 billion. The earliest publicly recorded transaction dates back to January 2014, with financing peaks concentrated in the mid-to-late periods of 2015 and 2016, averaging four transactions per period. Overall, financing activities have progressed steadily.

2) To date, the overall oncology innovation market remains in its early stages, with most projects at early-stage funding rounds (Angel to Series A). Series A rounds were the most frequent, with 37 deals completed (including four Series A+ transactions); there were 31 Angel-round deals (including four Pre-A deals). The number of mid-stage deals is expected to increase next year. Furthermore, deal sizes were concentrated between RMB 10 million and RMB 50 million, accounting for 26 transactions.

3) Early cancer screening and personalized medication projects have attracted the most attention from capital.

4) Funded projects are distributed across eight provinces, municipalities, and autonomous regions, with Shanghai having the lowest funding rate at 65%.

5) A total of 73 investment institutions participated in financing transactions for innovative oncology projects, among which 22 institutions were involved in two or more deals. The most active institutions included Beilu Pharmaceutical, Caijin Capital, Chunfeng Venture Capital, Legend Star, and Junlian Capital.

Appendix: Top 5 U.S. Hospitals for Oncology, 2016–2017

Case 1. The University of Texas MD Anderson Cancer Center

Case 2. Memorial Sloan Kettering Cancer Center

Case 3. Mayo Clinic

Case 4. Dana-Farber/Brigham and Women’s Cancer Center

Case 5. UCLA Medical Center

Scan the QR code below to becomeVCBeat Official Member, can obtainFull Version“Report on Trends in Digital Health Innovation in the Oncology Sector, Domestic and International”. The full report also includes introductions to digital innovation cases in the overseas oncology industry; trends in digital innovation among industry giants in oncology; and case analyses of the Top 5 cancer specialties at the best hospitals in the United States. Meanwhile, over the coming year, you will have unrestricted access to the completeIndustry Trend Report, promptly grasp the latest globalInvestment and Financing Information, with a comprehensive range ofHealthcare Enterprise Database, andMassive Resource Matching。

Scan the code to become a VCBeat member,

Beta Trial Price: 365 CNY/year.