Blood Products Industry Scan: A RMB 40 Billion Niche Market in Pharmaceuticals

Recently, the domestic blood products market has seen a succession of high-profile developments, such as Humanwell Healthcare transferring its blood products subsidiary for over RMB 2 billion, Weiguang Bio, a blood products R&D and manufacturing enterprise, going public, and Tsinghua Tongfang investing more than RMB 30 billion to acquire a stake in Shanghai RAAS.

Amid sustained industry interest, VCBeat (WeChat ID: vcbeat) has compiled relevant data on China’s blood products sector to provide insights into the overall operational landscape and the key product portfolios and business layouts of leading enterprises.

Fundamentals of Blood Products

Blood products fall within the category of biological products and primarily refer to biologically active preparations derived from healthy human plasma, manufactured using biological processes or separation and purification technologies.

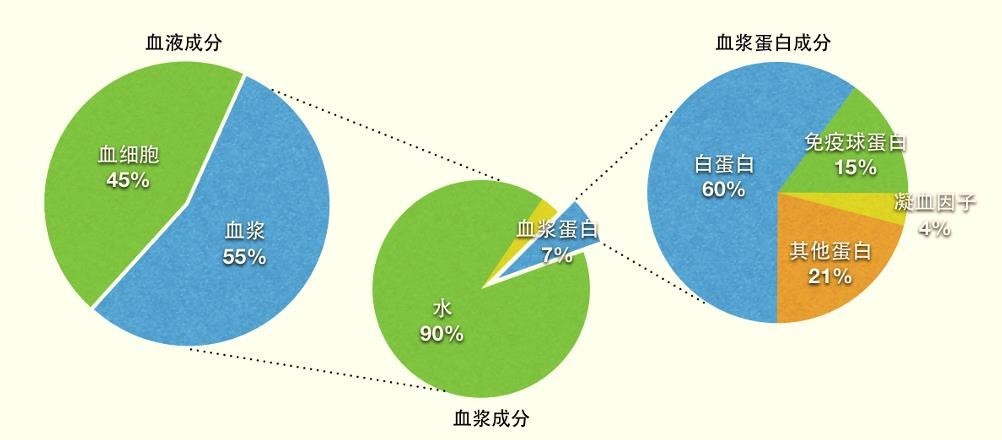

Human blood is composed of plasma, red blood cells, white blood cells, and platelets. Plasma accounts for approximately 55% of blood volume, while blood cells account for approximately 45%. Human plasma consists of about 90% water and only about 7% protein. Of the proteins, approximately 60% are albumin, 15% are immunoglobulins, 4% are coagulation factors, and 21% are other protein components.

Schematic Diagram of Blood, Plasma, and Plasma Proteins

Blood products are various preparations derived from the separation of different protein components in blood, used for patients with specific conditions. Blood products mainly fall into three major categories:Human Albumin, Human Immunoglobulins, and Coagulation Factors, among which coagulation factor products have the widest variety.

Human albumin is primarily used to regulate plasma colloid osmotic pressure and expand blood volume, and to treat traumatic and hemorrhagic shock, severe burns, and hypoproteinemia. It is widely applied in the management of common conditions such as stroke, liver cirrhosis, and kidney disease.

Human immunoglobulin products are primarily used for the prevention and treatment of immunoglobulin deficiency disorders, autoimmune diseases, and various infectious diseases. When used in combination with antibiotics or antiviral agents, they can enhance the therapeutic efficacy against certain severe bacterial or viral infections.

Coagulation factor products are used to treat various coagulation disorders and are also widely applied in surgical hemostasis. These products contain numerous components, each with distinct indications, making them a key focus for future new product development.

Internationally, source plasma used in the production of blood products is typically categorized into two types: recovered plasma and plasmapheresis plasma. Recovered plasma is primarily the plasma remaining after hospitals extract blood cells from whole blood; plasmapheresis plasma is plasma collected from human donors through plasmapheresis technology.

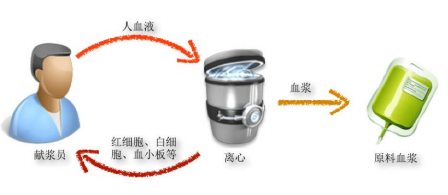

In China, the recycling of plasma for the production of blood products is prohibited; source plasma must be collected exclusively through plasmapheresis. Plasmapheresis refers to a procedure that uses physical methods to separate plasma from cellular components in whole blood and reinfuse all components except plasma back into the plasma donor. The collection process is illustrated in the figure below: blood (whole blood) is first drawn from the plasma donor, after which plasma is separated from other components, including red blood cells, white blood cells, and platelets. The isolated plasma is used for industrial production, while the remaining components—such as red blood cells, white blood cells, and platelets—are reinfused into the plasma donor.

Plasma Collection Flowchart

The collection and management system for source plasma is highly stringent. The collection and supply of source plasma must be conducted exclusively by plasmapheresis stations established with legal approval; no other entities or individuals are permitted to engage in plasmapheresis activities. Furthermore, China’s regulations on plasma collection are more rigorous than those in European and American countries.

The raw material for blood products is plasma, which is collected from healthy registered residents (plasma donors) within the catchment areas of plasmapheresis stations. These stations are operated and controlled by the manufacturing company itself. The entire process, from plasma collection to product manufacturing, is conducted internally within the production enterprise. After batch release certification, the products are sold directly to pharmaceutical distributors and healthcare institutions, and are ultimately provided to patients by hospitals, centers for disease control and prevention, and other medical facilities.

The industry is significantly influenced by policy.

The blood products industry is subject to strict regulatory oversight under national laws and regulations across numerous stages, including source plasma collection, production, sales, and importation. The competent authorities include the National Health and Family Planning Commission, the China Food and Drug Administration, and their corresponding local counterparts.

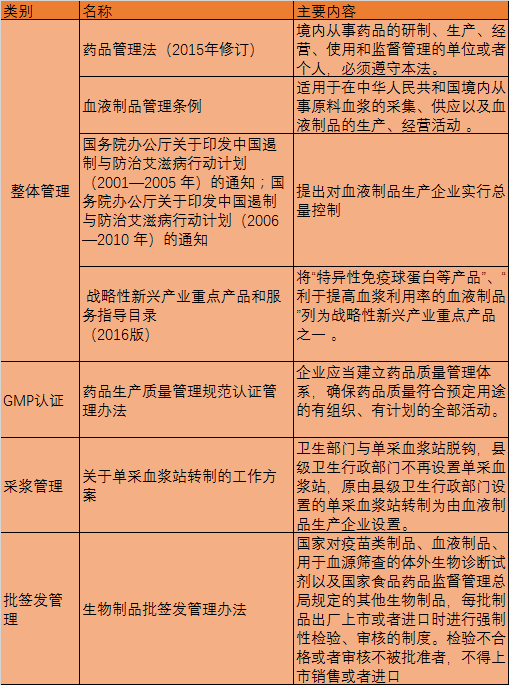

Major Laws, Regulations, Rules, and Normative Documents in the Blood Products Industry

The aforementioned regulations constitute the norms established by relevant regulatory authorities for the collection, production, sales, and distribution of blood products. This discussion focuses on two key aspects: first, the aggregate volume control within the blood products industry, and second, the administrative measures for lot release.

The blood products industry is characterized by high barriers to entry. To implement aggregate control over the number of blood product manufacturers, the state has not approved any new blood product production enterprises since 2001. This has resulted in a closed industry structure, thereby providing incumbent companies with a relatively less competitive environment.

Lot Release Management of Blood Products refers to the mandatory testing and review required for each batch of blood products prior to ex-factory release or import, in accordance with the Measures for the Administration of Lot Release of Biological Products. Batches that fail testing or do not pass review are prohibited from being marketed or imported.

Blood product manufacturers generally apply for lot release to the national drug testing authorities after qualified products are warehoused. Upon obtaining lot release approval, the Qualified Person issues a notice authorizing product sale. Therefore, industry insiders can typically estimate sales volume based on the lot release quantity of specific products, as the lot release volume serves as a proxy for sales to a certain extent.

Major Regulatory Frameworks Governing Plasmapheresis Stations

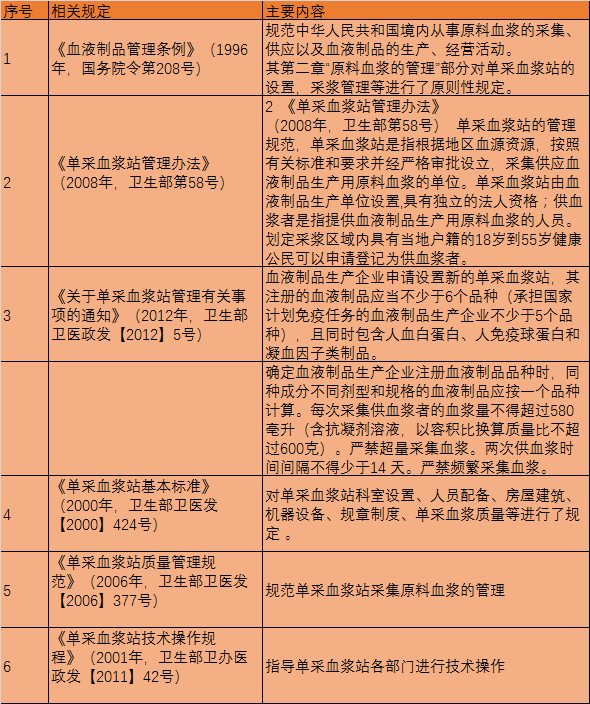

The primary regulatory framework governing plasmapheresis centers in China and its key provisions are as follows:

The Regulations on the Administration of Blood Products serve as the primary legal framework for the blood products industry, with a dedicated chapter regulating plasma collection management. The Measures for the Administration of Plasmapheresis Stations are departmental rules that provide more detailed provisions for plasmapheresis stations.

“Notice on Matters Concerning the Administration of Plasmapheresis Stations” raises and standardizes the requirements for establishing new plasmapheresis stations, specifically stipulating that blood product manufacturers applying to set up new plasmapheresis stations must have registered products that “simultaneously include human albumin, human immunoglobulin, and coagulation factor products.”

Relevant regulations stipulate the conditions that newly established plasmapheresis stations must meet, as well as the eligibility criteria for plasma donors. Article 8 of the Measures for the Administration of Plasmapheresis Stations provides: “The health administrative departments of the people’s governments of provinces, autonomous regions, and municipalities directly under the Central Government shall delineate plasma collection areas for plasmapheresis stations based on actual circumstances. The selection of plasma collection areas shall ensure a sufficient number of plasma donors to meet an annual raw plasma collection volume of no less than 30 tons. Newly built plasmapheresis stations shall achieve an annual collection volume of no less than 30 tons within three years.” The aforementioned provisions serve as considerations for provincial-level health administrative departments when delineating plasma collection areas, rather than prescribing specific requirements for the actual number of plasma donations or collection volumes at individual plasmapheresis stations.

Overview of the Current State of the Industry in China and Abroad

Data from the MRB, an affiliate of the Plasma Protein Therapeutics Association (PPTA), indicate that the global blood products industry initially comprised 102 companies. Following a series of blood product safety incidents worldwide, governments have strengthened regulatory oversight, while corporate mergers and restructurings have also taken place.Currently, fewer than 20 plasma-derived therapeutic products manufacturers remain overseas, including five in the United States and eight in Europe., and products from several major companies, including CSL Behring, Baxter, Grifols, and Octapharma, account for 80%–85% of the blood products market share, with industry concentration expected to become even more pronounced in the future.

Currently, the global annual plasma collection volume is approximately 30,000 metric tons, with major industry players such as CSL Behring, Baxter, Grifols, and Octapharma accounting for around 80% of the primary market.

Global plasma-derived therapeutics giants can extract more than 20 protein components from plasma. Most manufacturers are capable of producing human albumin, intravenous immunoglobulin (IVIG), specific human immunoglobulins, plasma-derived coagulation factors, and protease inhibitors from plasma.

In terms of sales revenue, human serum albumin accounts for approximately 20% of the market share, intravenous immunoglobulin and specific immunoglobulins (immunoglobulin preparations) account for around 30%, coagulation factors account for about 35%, and other products make up the remaining 15%. In the U.S. market, immunoglobulin products account for nearly half of total sales (excluding recombinant products).

Collection of Source Plasma in Major Countries Worldwide

First, the United States. As the world’s most important source of plasma, the U.S. is one of the few countries that achieve self-sufficiency in blood products and are able to export them, while most other countries rely partially on imports to meet domestic demand.

According to the April 2016 issue of Science News, the annual plasma collection capacity in the United States ranges between 15,000 and 20,000 metric tons. This capacity not only meets the domestic demand for blood products but also results in more than half of the plasma being exported abroad in the form of source plasma or finished products.

In the United States, approximately 90% of the plasma used for the production of blood products is sourced from paid donations of source plasma, while 10% comes from recovered plasma separated from whole blood donated through unpaid voluntary systems. Accordingly, plasma collection institutions are divided into two categories: commercial plasma collection centers that operate with government approval and compensate donors; and non-profit blood collection organizations such as the American Red Cross Blood Services and America’s Blood Centers.

Several large plasma protein product manufacturers and intermediary organizations, along with more than 500 plasmapheresis stations and over 2,000 blood collection centers, constitute the organizational framework spanning from source plasma to plasma-derived medicinal products. Notably, nearly 80% of plasmapheresis stations are affiliated with four international plasma derivatives giants: Grifols (Spain), CSL (Australia), Baxter (United States), and Octapharma (Switzerland).

In the United States, the establishment of plasma collection centers operates entirely on market mechanisms, with supply, demand, and prices regulated by market forces. Specifically, companies establish plasmapheresis centers based on their own strategic plans and in compliance with federal and local regulations; once these centers pass inspection by the U.S. Food and Drug Administration (FDA), they are permitted to collect plasma. Under this mechanism, the bottleneck in upstream resources for the U.S. blood products industry has been alleviated. The FDA is primarily responsible for ensuring that plasmapheresis centers meet standards to prevent the transmission of infectious diseases, while the number of plasma collection centers is adjusted solely by market dynamics.

Next is Europe. According to the "China Blood Products Industry Market Research and Investment Decision Report (2014-2020)" by AskCI Consulting, most European countries have adopted a policy of national control to ensure blood safety, meaning that the collection and application of domestic plasma are completed by local enterprises or government organizations. Only a few countries, such as Germany, have relatively open policies regarding plasma source control. Therefore, no single enterprise operates plasma collection centers across all European countries. The overall plasma collection volume in Europe is limited and insufficient to meet regional demand, resulting in virtually no exports. However, most European countries have adopted relatively open policies for importing blood products, allowing shortages to be supplemented through external imports.

China’s blood product manufacturing industry began in the early 1960s and has a history of more than 50 years, with only two to three manufacturers at its inception. In the 1980s, as profits from producing freeze-dried human plasma increased significantly and salting-out processes for plasma protein separation were adopted, many local blood stations, blood stations affiliated with major military regions, and some research institutions also began producing blood products, bringing the total number of manufacturers to approximately 70.

In the 1990s, the Ministry of Health explicitly ordered the phase-out of lyophilized human plasma production and prohibited the use of salting-out processes. Most manufacturers shut down.

In 1998, the blood products industry implemented a Good Manufacturing Practice (GMP) market access system: only enterprises that passed the national drug GMP certification were permitted to manufacture and distribute blood products. At that time, a total of 33 enterprises in China received certification. As of December 31, 2016, there were approximately 28 blood product manufacturers in China, among which 25 had obtained certification under the 2010 version of GMP. The product portfolios of most manufacturers primarily consist of human albumin, intravenous immunoglobulin (IVIG), and specific human immunoglobulins (such as hepatitis B human immunoglobulin, rabies human immunoglobulin, and tetanus human immunoglobulin). A small number of manufacturers are capable of producing coagulation factor products (such as coagulation factor VIII and fibrinogen). There remains a significant gap between the variety of blood products that Chinese manufacturers can produce and those available in developed countries.

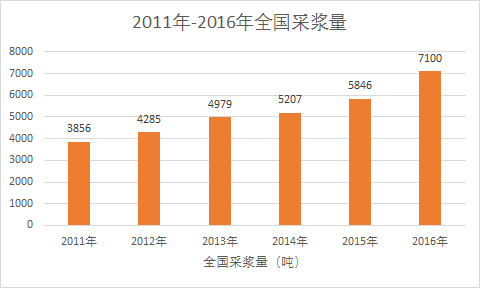

In 2016, the national plasma collection volume for blood products in China was approximately 7,100 tons. The scale of blood product manufacturers in China varies, with annual plasma processing volumes ranging from tens to hundreds of tons; however, the quality and technical standards of their products are comparable.

Market Size of China's Blood Products Industry

The market capacity of blood products can be observed from two perspectives: one is plasma collection volume, which represents the raw materials available for production across the entire industry; the other is the number of batch release approvals, which reflects the detailed conditions of each sub-segment within the broader blood products category.

As of December 31, 2016, there were over 200 plasmapheresis stations across China. The plasma collection volume in 2016 reached approximately 7,100 tons, hitting a record high.

Data sources: Website of the National Health and Family Planning Commission of the People's Republic of China, industry association data, and internet-based information on the blood products industry

Meanwhile, from the perspective of global per capita consumption of blood products, there is still a significant gap between China's per capita usage and that of developed countries in Europe and the United States.

Based on product characteristics and market performance, the segmented market analysis and batch release volumes for each product are as follows:

a. Human Albumin

Domestic market demand will grow steadily. This is primarily driven by the following factors: first, with a population exceeding 1.3 billion, there is a large populace and rapidly growing demand for healthcare, offering substantial market potential; second, rapid economic development has led to rising national income and improving medical insurance benefits; third, continuous advancements in medical capabilities have enabled conditions previously considered untreatable to be managed through routine clinical practice.

Based on feedback from the domestic market, given the unique nature of raw materials for blood products, Chinese consumers tend to prefer domestically produced blood products. Imported products serve as a supplement to the insufficient domestic production capacity, and demand for domestically produced human serum albumin remains strong.

From 2012 to 2016, the volume of human serum albumin released by batch certification showed a steady growth trend, with increases in both domestically produced and imported quantities. However, due to limited domestic production capacity and a significant gap between supply and demand, the proportion of imported products rose rapidly, increasing from 47.87% in 2012 to 58.98% in 2015. In 2016, the share of imported products declined slightly compared to 2015, standing at 56.71%.

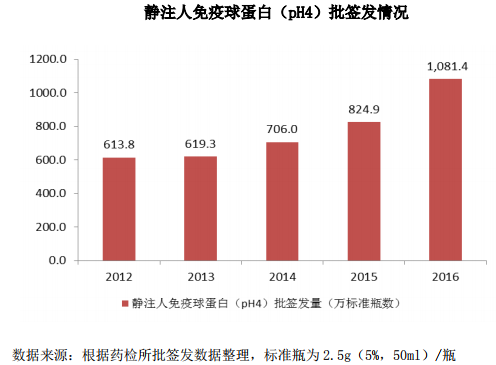

b. Intravenous Human Immunoglobulin

In the long term, the human immunoglobulin market still has enormous room for growth and potential. Human immunoglobulin has been used in clinical practice in China for only about a decade, whereas its application abroad spans several decades. There remain many potential areas of use in terms of indications and eligible disease types, and the generally administered therapeutic doses in clinical practice are still relatively low.

In recent years, with the growing recognition by clinicians of the efficacy of human immunoglobulin, the exposure of limitations associated with certain existing medications (such as antibiotics), and the enhanced affordability for patients, therapeutic effective dosages are aligning with advanced international medical standards. As imports of such products are prohibited, the supply-demand imbalance is expected to persist for an extended period.

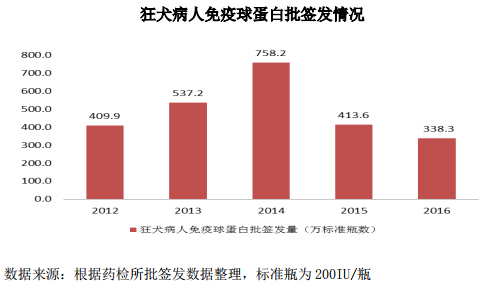

c. Specific Human Immunoglobulin

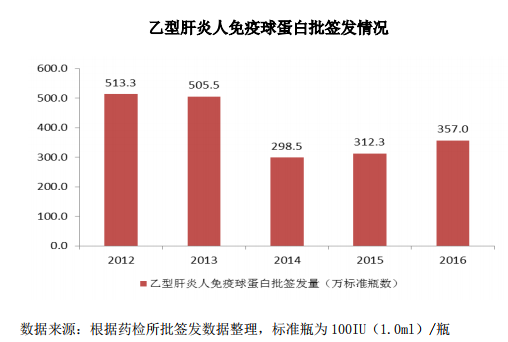

Currently, the specific human immunoglobulins produced in China mainly include hepatitis B human immunoglobulin, tetanus human immunoglobulin, and rabies human immunoglobulin. China is a country with a high incidence of hepatitis B, with a large base population of HBsAg-positive individuals and patients. The batch release status of hepatitis B human immunoglobulin is as follows:

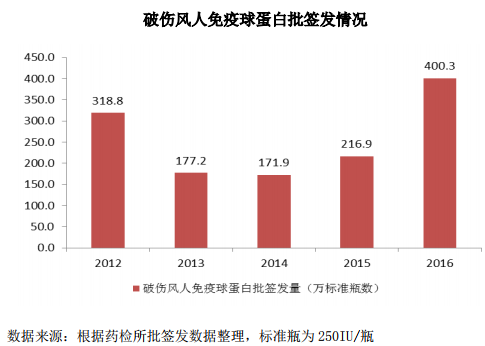

Human Tetanus Immunoglobulin is an upgraded product of Tetanus Antitoxin, with significantly higher safety and efficacy in prevention and treatment. As the healthcare environment improves and payment capacity increases, its market size will gradually expand.

China ranks second worldwide in the incidence and mortality rates of rabies. With traditional prophylactic vaccination regimens, it takes 7–10 days after administration for antibody titers to reach protective levels, limiting their efficacy in emergency treatment. In contrast, following the injection of human rabies immunoglobulin (HRIG), antibody titers in the blood rapidly rise to protective concentrations within tens of minutes to several hours, making it highly effective for post-exposure prophylaxis, such as in cases of accidental bites. Both the World Health Organization (WHO) and China’s Guidelines for Post-Exposure Prophylaxis of Rabies mandate the administration of human rabies immunoglobulin for Category III rabies exposures.

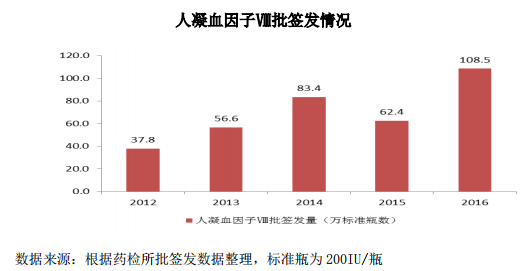

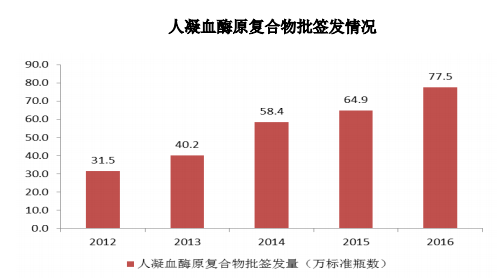

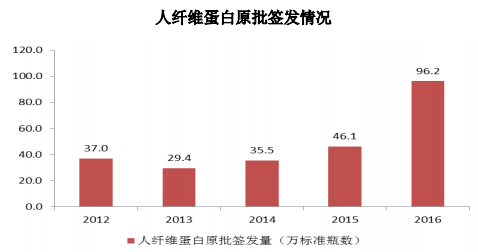

d. Coagulation factor products

The market for coagulation factor products still holds substantial room for growth and potential. For instance, hemophilia is a lifelong condition that requires long-term dependence on coagulation factors to manage bleeding episodes. Coagulation factors represent the largest category in global blood product sales by value. Currently, per capita consumption of coagulation factors in China remains at an extremely low level. With the continuous improvement of healthcare standards in China, coagulation factors are poised for very broad prospects in the domestic market.

Coagulation factor products mainly include human coagulation factor VIII, human prothrombin complex concentrate, and human fibrinogen. Only a few manufacturers in China produce these products.

Domestic batch release data for human fibrinogen are as follows:

Currently, only recombinant human coagulation factor VIII is permitted for import, while human plasma-derived coagulation factor VIII remains prohibited from import. If this policy persists in the future, the robust domestic demand for coagulation factor products will be met primarily by domestic production.

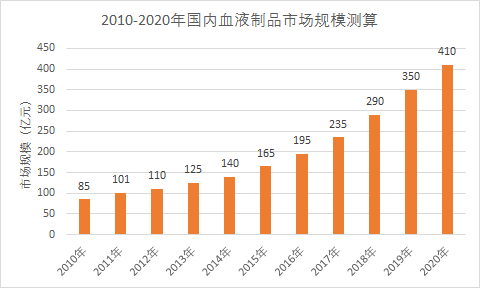

Industry Scale Could Reach RMB 40 Billion Within Five Years

In recent years, China’s large population base, the aging of society, and the continuous expansion of indications for blood products have stimulated the growing downstream demand for blood products in China.

A research report by China Galaxy Securities pointed out that the compound annual growth rate (CAGR) of China's blood products market was 14.2% from 2010 to 2015. In 2015, the market size reached RMB 16.5 billion. As a scarce resource, blood products are expected to maintain high prosperity over the next five years, with a projected CAGR of 20.0% from 2016 to 2020, bringing the market size to RMB 41 billion by 2020.

In the 2017 edition of the National Reimbursement Drug List for Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance, a total of eight blood products were included, with four newly added varieties. The increase in product varieties, coupled with expanded reimbursement coverage, will correspondingly boost demand for these blood products, thereby stimulating another acceleration in the growth of the blood products industry.

Sources: China Industry Information Network, Pharmaceutical Industry Information Center, China Galaxy Securities Research Department

Overview of Domestic Blood Product Companies in China

As of December 31, 2016, there were approximately 28 blood product manufacturers in China, of which 25 had passed the GMP certification under the 2010 edition. These include:

1. CNBG

China National Biotec Group (hereinafter referred to as “CNBG”), a subsidiary of Sinopharm, oversees six biological products research institutes located in Beijing, Changchun, Chengdu, Lanzhou, Shanghai, and Wuhan, as well as enterprises such as Tiantan Biological. As one of China’s longest-established professional institutions dedicated to the research and production of vaccines and blood products, CNBG is an integrated biotechnology enterprise encompassing scientific research and development, manufacturing, and commercial operations.

The entities within CNBG engaged in blood products include the Shanghai Institute of Biological Products, the Lanzhou Institute of Biological Products, the Wuhan Institute of Biological Products, and Chengdu Rongsheng, a subsidiary of Tiantan Biological.

2. Hualan Biological Engineering Inc.

Hualan Biological Engineering Inc. (Stock Code: 002007), established in 1992, is a national high-tech enterprise engaged in the research and development and production of blood products and vaccines. Currently, Hualan Biological has more than twenty wholly-owned subsidiaries.

Hualan Biological primarily manufactures blood products under the "Hualan" brand, including Human Albumin, Intravenous Immunoglobulin (pH4), Human Immunoglobulin, and Prothrombin Complex Concentrate.

3. Shanghai RAAS

Shanghai RAAS Blood Products Co., Ltd. was listed on the SME Board of the Shenzhen Stock Exchange in June 2008 (stock code: 002252). In 2014, Shanghai RAAS acquired Banghe Pharmaceutical Co., Ltd. (later renamed “Zhengzhou RAAS Blood Products Co., Ltd.”) and Tonglu Bio-Pharmaceutical Co., Ltd. In 2016, Shanghai RAAS gained control of a 90% equity stake in Zhejiang Haikang Biological Products Co., Ltd. through its subsidiary, Tonglu Bio-Pharmaceutical.

Shanghai RAAS is primarily engaged in the production and sale of blood products, vaccines, diagnostic reagents and testing devices, and testing technologies, as well as the provision of testing services. Its main products include Human Albumin, Intravenous Immunoglobulin (pH4), Human Coagulation Factor VIII, Human Prothrombin Complex, Human Fibrinogen, Lyophilized Human Thrombin, and Topical Lyophilized Fibrin Sealant.

4. Sichuan Shuyang

Sichuan Shuyang, established in 1985, is a large comprehensive pharmaceutical enterprise primarily engaged in the research and development, production, and sales of blood products. It is a key advantageous enterprise and a high-tech enterprise in Sichuan Province, and is currently affiliated with China Grand Pharmaceutical Group.

5. Taibang Bio

China Biologic Products Holdings, Inc. (NASDAQ: CBPO) owns subsidiaries Shandong Taibang Biological Products Co., Ltd. and Guizhou Taibang Biological Products Co., Ltd., and holds a stake in Xi’an Huitian Blood Products Co., Ltd.

Shandong Taibang is a joint venture established on November 1, 2002, through the restructuring of the Shandong Institute of Biological Products. The company primarily focuses on blood products and biochemical pharmaceuticals, operating GMP-certified production workshops for blood products and small-volume injections.

Guizhou Taibang Biological Products Co., Ltd. is a biopharmaceutical enterprise tasked with the national emergency production of blood products, and it is a key pillar enterprise in Guizhou Province’s biopharmaceutical industry. The company currently operates manufacturing workshops for blood products and small-volume injections.

6. Boya Bio-pharmaceutical

Boyabio was established in 1993 and listed on the ChiNext board of the Shenzhen Stock Exchange on March 8, 2012. The company currently offers products including human albumin, intravenous immunoglobulin (pH 4), fibrinogen, and specific human immunoglobulins.

7. ST Biochemistry

Zhenxing Biochemistry Co., Ltd. (ST Biochemistry, 000403) is a diversified conglomerate with business operations spanning electric power, biopharmaceuticals, and blood products. According to ST Biochemistry’s official statements, the company has prioritized the development of Guangdong Shuanglin’s blood products segment as its primary strategic focus. It will continue to strategically expand its blood products business by establishing new plasmapheresis centers and increasing plasma collection volumes at existing stations. As reported in its annual report, Guangdong Shuanglin operated eight plasmapheresis centers, with a total plasma collection volume of 301.58 metric tons in 2016.

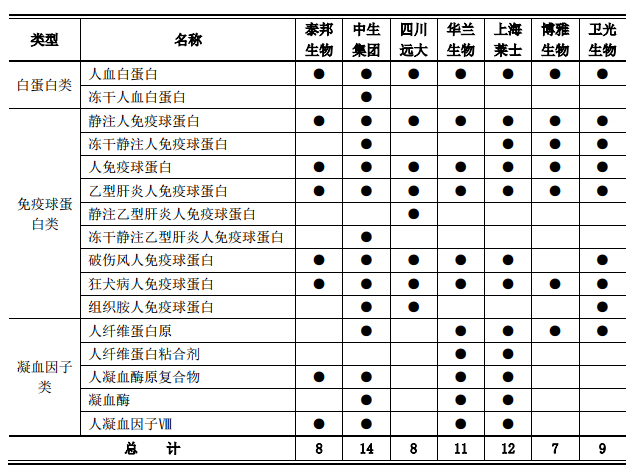

Approval Status of Blood Product Manufacturers

China’s blood product manufacturers exhibit relatively low levels of plasma purification and comprehensive utilization, with their product portfolios predominantly consisting of human albumin and intravenous immunoglobulin (IVIG). Hualan Biological Engineering Inc. is capable of producing 11 types of products, while the various blood product subsidiaries under China National Biotec Group (CNBG) collectively produce 14 types. Some other enterprises can manufacture 7–9 types, whereas the remaining companies are limited to producing only 3–4 types.

As of the end of 2016, the status of production approvals for blood products among major blood product manufacturers in China was as follows:

Data source: National Medical Products Administration website

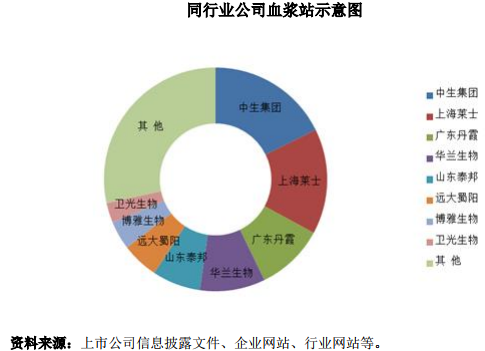

Distribution and Market Share of Plasma Collection Centers

As of December 2016, the distribution and market share of plasma collection centers among peer companies were as follows:

Among the 25 blood product manufacturers, plasma collection stations are relatively concentrated, with the top five companies accounting for more than 50% of all stations. The distribution of plasma collection stations among peer companies exhibits certain regional characteristics. For instance, Shanghai RAAS’s stations are primarily located in Anhui and Guangxi; Hualan Biological Engineering’s stations are mainly in Chongqing and Henan; Tiantan Biological Products’ stations are predominantly in Sichuan; and Guangdong Danxia Biopharmaceutical’s stations are largely concentrated in Guangdong.

Market Share Status

In July 2004, the State Food and Drug Administration issued the Administrative Measures for Lot Release of Biological Products, stipulating that blood products shall be subject to a lot release system (i.e., blood products may only be sold or imported after passing mandatory testing). Currently, market demand for blood products is substantial, and most companies proceed with sales immediately upon obtaining lot release approval. Therefore, lot release data generally reflects the market conditions of the blood products industry.

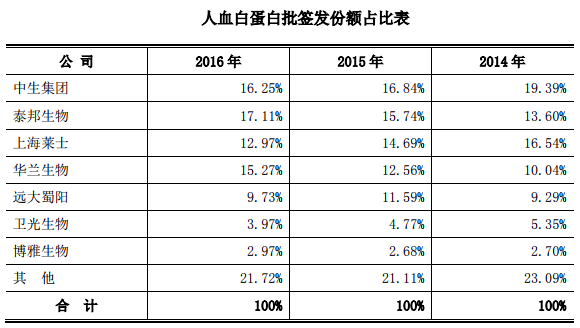

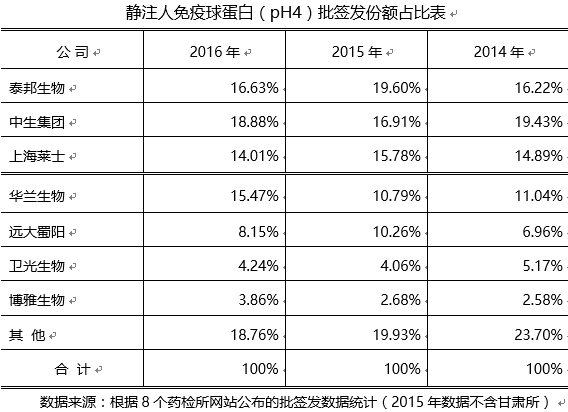

Below, we primarily discuss two major products: Human Albumin and Intravenous Immunoglobulin (pH4). Their market shares, based on the proportion of batch release approvals, are as follows:

Data source: Compiled from batch release data published on the websites of eight drug testing institutes (data for 2015 excludes the Gansu Institute).

Note 1: CNBG data includes Chengdu Rongsheng, Wuhan Institute, Lanzhou Institute, and Shanghai Institute; Taibang Biopharma includes Shandong Taibang, GuiShizhou Taibang, Xi'an Huitian; Shanghai RAAS including Zhengzhou RAAS and Tonglu Bio; Hualan Biological Engineering including Hualan Chongqing;

Note 2: Human albumin is converted based on 10 g/vial.

As shown in the table above, the market share of human serum albumin is relatively concentrated. Among the 25 companies, the top five enterprises’ market

The total market share exceeds 60%.

Note 1: Data for China National Biotec Group (CNBG) includes Chengdu Rongsheng, Wuhan Institute, Lanzhou Institute, and Shanghai Institute; Taitai Biological includes Shandong Taibang, GuiZhoutai Bang, Xi'an Huitian; Shanghai RAAS includes Zhengzhou RAAS and Tonglu Biological; Hualan Biological includes Hualan Chongqing;

Note 2: Intravenous Immunoglobulin (pH 4) is calculated at 2.5 g per bottle.

As shown in the table above, the market share of Intravenous Human Immunoglobulin (pH 4) is relatively concentrated, with 25 blood product manufacturers

Among the enterprises, the top five companies account for a combined market share of over 60%.

Analysis of the Prospects for China's Blood Products Industry

1. Enhance the comprehensive utilization rate of plasma and develop new products.

To fully and rationally utilize valuable plasma resources, manufacturers should upgrade production equipment and improve manufacturing processes. They should actively adopt new protein separation and purification technologies and methods to enhance product yield and purity, promote the upgrading of existing products and production technologies, actively pursue comprehensive utilization of plasma proteins, vigorously research and develop new products, and adjust product portfolios in accordance with market demands. In addition, the application of genetic engineering techniques in blood product research should be encouraged and guided, with focused efforts on the development of recombinant plasma proteins.

2. Improve product quality and reduce risks in clinical applications

Over the past few decades, quality management of blood products has established a relatively effective model that has demonstrated favorable outcomes in practical applications. However, there is still room for improvement and enhancement in the quality control methods and techniques applied throughout the process from plasma to finished products, particularly in the appropriate selection of testing methods and reagents, the rational determination of test items, and the active development of reference standards.

In summary, quality management for blood products must adhere to high standards and strict requirements while remaining practical and grounded in reality. Production and quality management departments should diligently implement Total Quality Management (TQM) and strictly conduct production and management activities in accordance with Good Manufacturing Practice (GMP) requirements.

3. Actively engage in domestic and international exchanges, and introduce advanced technologies and management practices

While safeguarding intellectual property rights, we should actively engage in management and technical exchanges, particularly by creating conditions and opportunities for international collaboration and pursuing targeted technology introduction. It is essential to establish information networks and databases to build a comprehensive system for collecting data and information on the production capacity, standards, development trends, and strategic directions of the blood products industry both domestically and internationally. Furthermore, financial investment and supportive policies should be implemented to facilitate the introduction, adoption, and upgrading of new technologies.

References

Prospectus for the Initial Public Offering of Shares by Shenzhen Weiguang Biological Products Co., Ltd.

Analysis of the Current Status and Policies of China's Blood Products Industry in 2017 - China Industry Information Network

http://www.chyxx.com/industry/201706/531394.html

Statistical Review of the Market Size of China's Blood Products Industry in 2016 – China Industrial Information Network

http://www.chyxx.com/industry/201701/485147.html

Galaxy Securities: In-Depth Report on Hualan Biological Engineering (20170106)