Rock Health Reports Record-Breaking H1 2017: 188 Digital Health Companies Raise $3.5B

Previously, we shared with our readers StartUp Health’s report on investment and financing in the digital health industry in 2017 (StartUp Health Releases H1 2017 Report: Investment and Financing Surpass $6 Billion, with Digital Health and Patient Education Continuing to Heat Up). Rock Health, another well-known incubator for digital health startups in the United States, headquartered in the San Francisco Bay Area, has also released its semi-annual investment and financing report.

VCBeat (WeChat ID: vcbeat) has excerpted and compiled the key sections of the report to provide insights into how another industry leader analyzes the financing landscape in the first half of this year.

Record-Breaking First Half

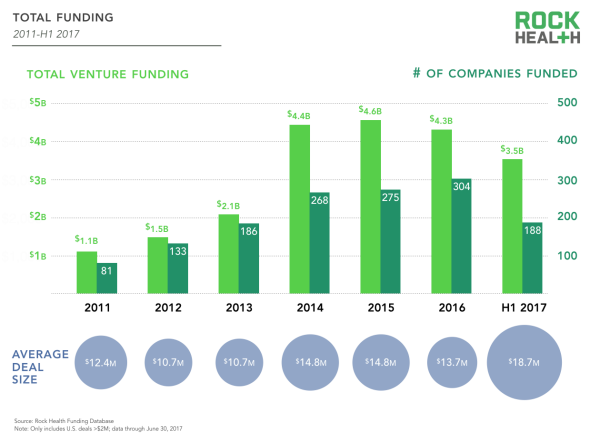

As the digital health sector matures, investors are pouring increasing amounts of capital into this field. In the first half of 2017, a total of 188 digital health companies secured $3.5 billion in funding, setting records for both the number of funded companies and the total amount of capital raised.

It should be noted that, unlike the previous report by StartUp Health,Rock Health’s research scope is limited to U.S.-headquartered digital health companies with transaction amounts exceeding $2 million.Excluded from the report’s statistical scope are companies that do not belong solely to the digital health industry, such as healthcare service providers like One Medical and Oscar, biotechnology/diagnostics companies like Grail and Theranos, and software companies like Zenefits and Reputation.com.

There are also various international companies, such as the German startup Clue, even though many of their users and funders are based in the United States; these entities rely on diverse funding sources, including grants or government subsidies, non-dilutive crowdfunding, or venture capital investments under $2 million.

Therefore, the statistical data in the report will differ from that of StartUp Health.

The final three months of the first half of 2017 made a substantial contribution to achieving this record. In Rock Health’s Q1 report released at the end of last quarter, investment and financing activity was still described as “business as usual.” Since then, we have witnessed a dramatic surge.

"Undoubtedly, the second quarter of 2017 was a record-breaking quarter."Although media headlines remain dominated by the various uncertainties surrounding U.S. healthcare reform, political volatility has not dampened investors’ interest in digital health.

For entrepreneurs, specific policy agendas are never the biggest concern; industry transparency is the cornerstone for fostering innovation and growth. Therefore, we were surprised to find that digital health investment experienced its strongest quarter during this period of greatest uncertainty in medical history.

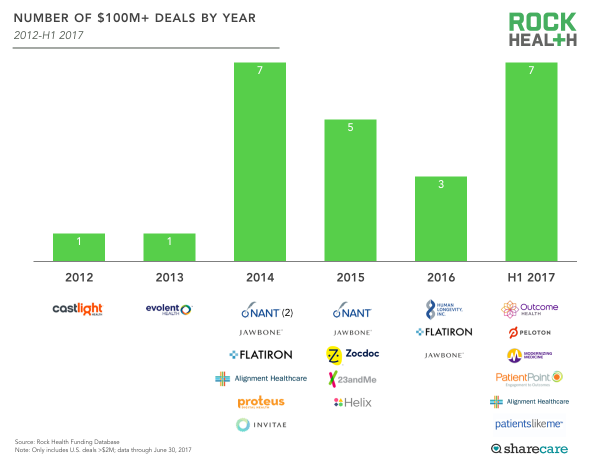

In addition to its remarkable performance in terms of transaction volume and value, the first half of 2017 also saw seven record-breaking deals exceeding $100 million each.Among them, Outcome Health and Peloton Interactive accounted for the two largest digital health deals.。

Perhaps even more exciting is that 2017 is only halfway through. Although no digital health companies have gone public this year, we will focus on highly capitalized companies that may be preparing for an IPO, particularly those that have raised substantial funds in recent months.

Double Records in Transaction Volume and Financing Amount

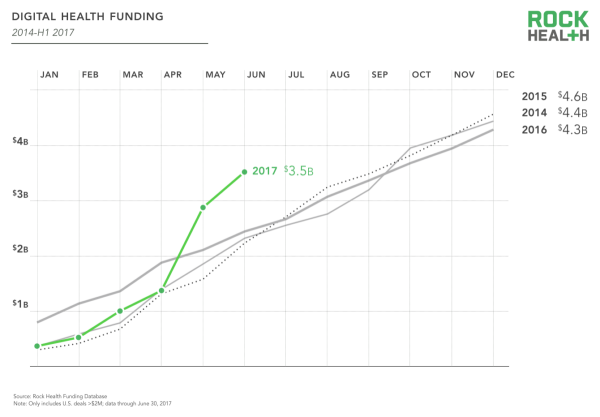

In the first half of 2017, both the number and value of transactions in the digital health sector reached record highs. Investment activity saw an unexpected surge in the second quarter. As shown in the chart below, while the transaction volume in Q1 did not differ significantly from that of the same period in the previous three years, funding rose sharply to unprecedented levels starting in April, ultimately driving total financing for the first half of the year to a record high.

The growth in capital investment was primarily driven by several large-scale deals. However, with the number of transactions in the first half of the year also reaching a record high of 188, this surge in financing is not an anomaly attributable to a few outlier deals, but rather demonstrates investors’ optimism toward the digital healthcare industry.

In terms of transaction volume, as shown in the figure, although last year’s transaction volume moderated compared with 2016, the average transaction amount this year has reached a record high of $18.7 million. (Editor’s note: If the two largest transactions mentioned above—Outcome Health and Peloton Interactive—are excluded, the average transaction size still stands at $14.5 million.)

The $100 Million Club: 7 Deals Exceeding $100 Million

According to the statistical scope defined by Rock Health, a total of seven companies raised over $100 million in funding in the first half of 2017. The surge in mega-deals during this period meant that, with just half of 2017 elapsed, the number of nine-figure transactions had already surpassed the totals for the previous two years and equaled the full-year record set in 2014.

The top two mega-deals in the first half of the year were Outcome Health’s record-breaking $500 million Series A financing, and Peloton Interactive’s $325 million funding round led by Wellington Management, Fidelity Investments, KPCB, and True Ventures.

Prior to the second quarter of 2017, the largest recorded digital health transaction was BlackRock’s $300 million investment in Jawbone in 2015.

The specific details of the seven mega-deals are as follows:

1. Outcome Health (Chicago)

Subfield: Consumer Health Information

Target Customers: Medical Suppliers

Transaction Amount: $500 million

Major Investors: Goldman Sachs, Google Capital

2. Peloton (New York)

Subfield: Smart Fitness Equipment

Target Customers: Consumers

Transaction Amount: $325 million

Major Investors: Wellington Management, KPCB, True Ventures

3. Modernizing Medicine (Boca Raton, Florida)

Subfield: EMR

Target Audience: Licensed Physicians

Transaction Amount: $206 Million

Major Investor: Warburg Pincus

4. Patient Point (Cincinnati, Ohio)

Subfield: Consumer Health Information

Target Customers: Medical Suppliers

Transaction Amount: $140 million

Key Investors: Searchlight Capital Partners, Silver Point Capital

5. Alignment Healthcare (Irvine, California)

Subfield: Population Health Management

Target Customers: Consumers, Medical Suppliers

Transaction Amount: $115 million

Major Investor: Warburg Pincus

6. PatientsLikeMe (Cambridge, Massachusetts)

Subfield: Patient Community

Target Customers: Pharmacies

Transaction Amount: $100 Million

Major Investor: iCarbonX

7. Share Care (Atlanta)

Subfield: Consumer Health Information

Target Customers: Employers, Health Insurance Providers, Healthcare Suppliers

Transaction Amount: $100 Million

Major Investor: Summit Partners

As the digital health market matures, many companies in the industry are beginning to demonstrate profit potential, with pre-IPO investments from growth-stage and private equity investors becoming increasingly frequent and substantial.

Although the majority of venture capital funds continue to flow into Silicon Valley, we should also note thatAmong the seven digital health mega-deals exceeding $100 million in the first half of 2017, none involved companies based in the San Francisco Bay Area; instead, they were distributed across the United States.。

Since Rock Health began tracking digital health investment and financing in 2011, 18 companies have each raised $100 million across 24 funding rounds. Companies such as Alignment Healthcare, Flatiron Health, Jawbone, and NantHealth have secured multiple funding rounds valued at over $100 million each.

Nearly one-quarter of these 18 companies continued to raise public capital through initial public offerings (IPOs), including Castlight Health, Evolent Health, Invitae, and NantHealth. Regrettably, Jawbone, a pioneer founded in 1999 that entered the smart wearable market in 2011, has filed for bankruptcy liquidation.

Both Consumer-Facing and Business-Facing Companies Are Favored by Investors

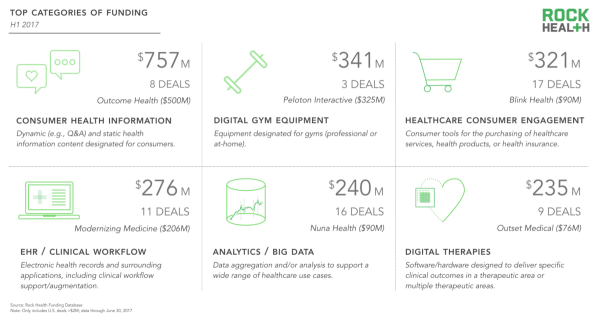

Several mega-deals in the first half of 2017 profoundly reshaped the landscape of the most investor-favored subsectors within the digital health industry. As shown in the figure, the top six subsectors accounted for 63% of all digital health financing.Furthermore, compared with last year’s rankings, only “Analytics/Big Data” appeared on the list in both years.

Specifically, the top six subfields are:

1. Consumer Health Information

Content: Dynamic or static health information customized for consumers

Financing Amount: $757 million

Transaction Volume: 8 transactions

Largest Deal: Outcome Health ($500 million)

2. Smart Fitness Equipment

Content: Smart devices designed for gyms or home fitness

Financing Amount: $341 million

Transaction Volume: 3 transactions

Largest Deal: Peloton Interact ($325 million)

3. Healthcare Consumer Engagement

Content: Consumer tools for purchasing medical services, medical products, or health insurance, etc.

Financing Amount: $321 million

Transaction Volume: 17 transactions

Largest Deal: Blink Health ($90 million)

4. EHR/Clinical Workflows

Content: Electronic Health Records and Their Peripheral Applications, Including Clinical Workflow Support/Enhancement

Financing Amount: $276 million

Transaction Volume: 11 Transactions

Largest Transaction: Modernizing Medicine ($206 million)

5. Analytics/Big Data

Content: Leveraging data aggregation and/or analysis to support healthcare use cases

Financing Amount: $240 million

Transaction Volume: 16 Transactions

Largest Deal: Nuna Health ($90 million)

6. Digital Therapeutic Solutions

Content: Delivery of clinical treatment protocols using specialized software/hardware at one or more locations

Financing Amount: $235 million

Transaction Volume: 9 Transactions

Largest Deal: Outset Medical ($76 million)

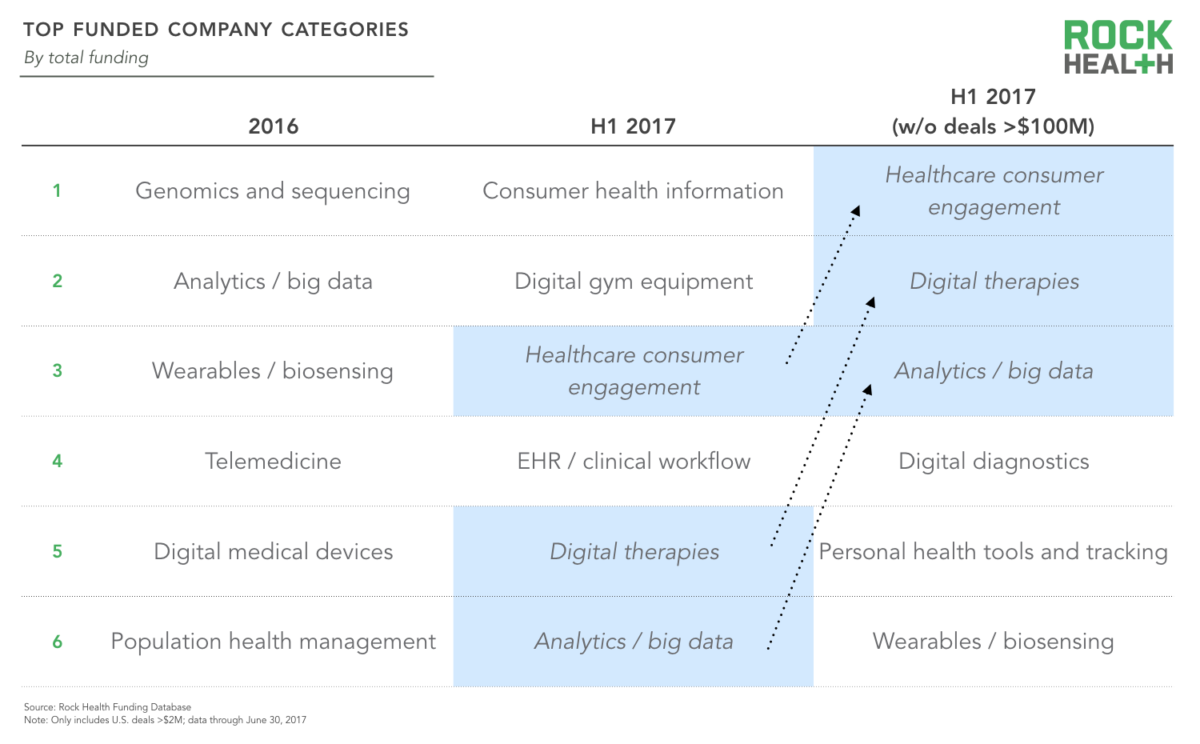

Due to the impact of mega-deals worth over $100 million, it is difficult to fully discern from the above rankings which subsectors’ companies are truly favored by investors. Therefore, Rock Health also compiled a comparative ranking that excludes these $100 million-plus mega-deals.

As shown in the figure below, after excluding mega-deals, only half of the top six subsectors (consumer health engagement, digital therapeutics, and analytics/big data) remained on the list. In other areas, such as smart fitness equipment, which originally ranked second, dropped off the list immediately after excluding Peloton’s $325 million deal.

Furthermore, since 2011, there have been only seven companies in this sector. The comparison chart before and after excluding mega-deals clearly demonstrates the diversity of investor interest, indicating that they are keen on both consumer-facing and enterprise-focused companies.

Notably, the chart below also compares the subsectors most popular with investors in 2016; only analytics/big data appeared in the rankings for the first half of 2017. After excluding mega-deals worth hundreds of millions of dollars, only two categories—analytics/big data and wearables/biosensors—remained on the list.

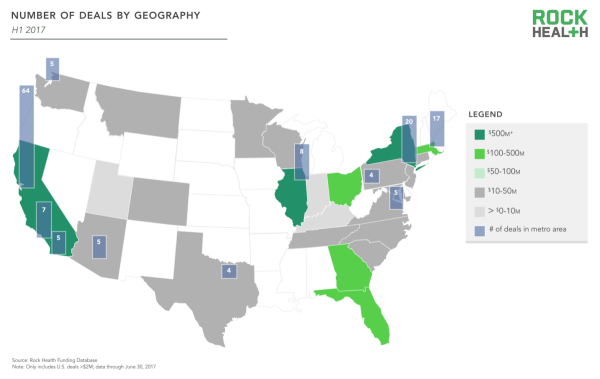

Portfolio companies are distributed across 25 U.S. states, with California accounting for one-third of the total funding raised.

At the state level, California continues to lead by a wide margin, while New York and Illinois have entered the top tier for the first time, with companies headquartered in these two states each raising over $500 million. Meanwhile, Florida and Georgia have joined the second tier—represented by traditional powerhouse Massachusetts—with fundraising totals between $100 million and $500 million.

From the perspective of various metropolitan areas, the San Francisco Bay Area continues to live up to expectations, consolidating its position as the world leader in the digital health industry. With 64 deals in the first half of the year, it holds its own against the combined total of 80 deals from the ten metropolitan areas ranking immediately behind it.

Notably, the transaction volume outside traditional digital health hubs has increased, with startups in Cincinnati, Bethesda, Miami, Milwaukee, Nashville, and St. Cloud each securing investments exceeding $20 million.

Digital healthcare continues to receive support from long-tail capital

In the first half of 2017, 331 distinct investors completed transactions in the digital health sector. Among them, 138 investors (42%) were making their inaugural investments in this field. Of course, some observers argue that a portion of these investors are merely “tourists” who will soon exit the digital health space.

Venture capital firms continue to execute various deals in this sector, indicating that not only are digital health companies maturing alongside the market, but their investors are also evolving: moving beyond a previously casual, dabbler-like investment approach toward more confident and committed capital allocation.

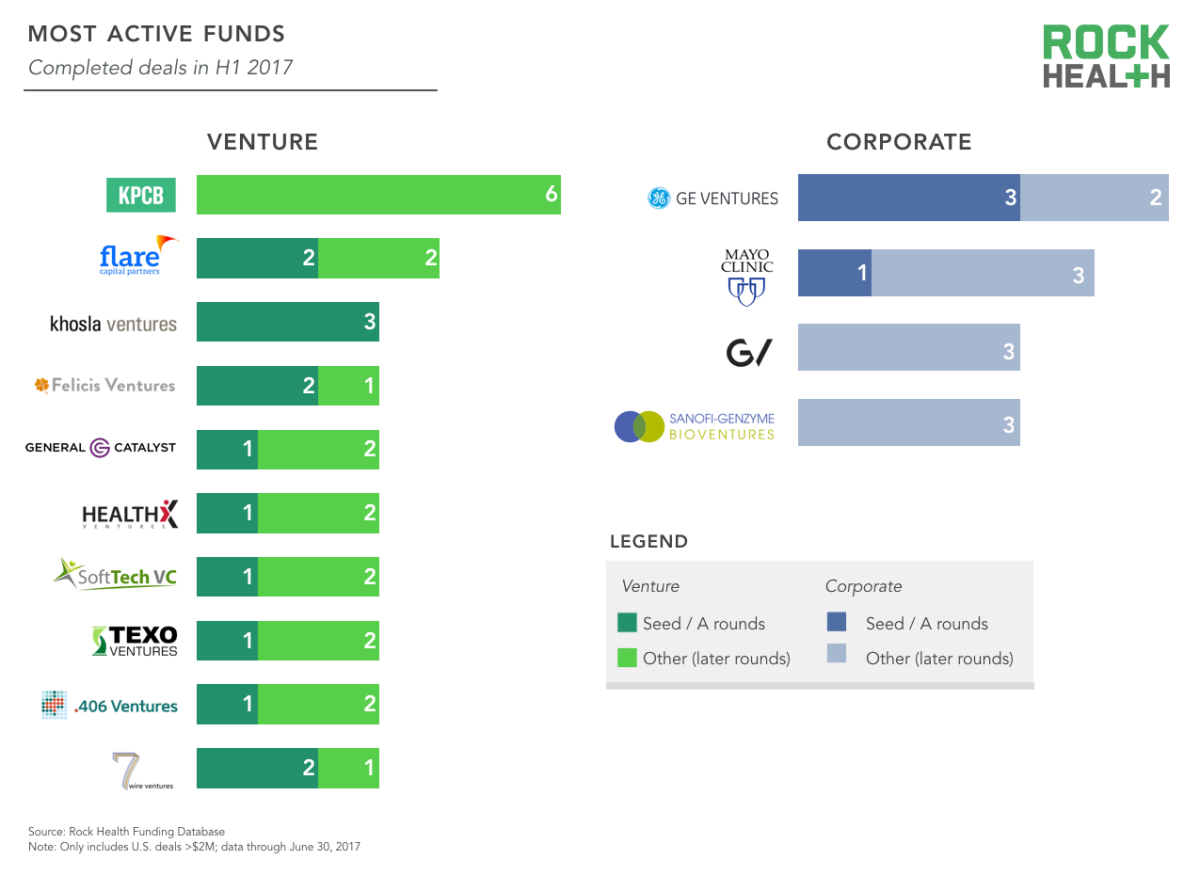

As shown in the figure below,Venture capital firms are the most active., a total of 12 companies made more than three investments in the first half of 2017, with KPCB and Flare Capital Partners ranking first and second, having completed six and four deals, respectively.

In terms of the ranking of the most active investors, the situation in the first half of this year is largely consistent with that of previous years. For example, Khosla Ventures and .406 Ventures each completed three deals in the first half of this year, matching their total of six deals for the entire last year.

Somewhat surprisingly, Andreessen Horowitz, which had been highly active previously—completing six deals last year and a total of 21 deals over the past six years—has not closed any deals so far this year.

Furthermore, in terms of investments in healthcare suppliers, UPMC, which completed six deals last year, has only closed one transaction so far this year, causing it to drop out of the rankings. Meanwhile, the Mayo Clinic has doubled its investment volume in the first half of the year: historically, it averaged no more than two deals annually, but it has already made four investments year-to-date.

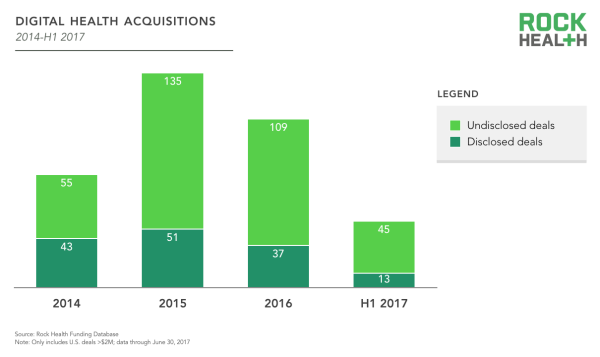

M&A Activity Slows: Only 58 Deals in the First Half of 2017

There were 58 M&A transactions in the first half of 2017, a decline from 87 in the same period last year (the full-year figure for the previous year was 146, with 98 in 2014 and 186 in 2015). It should be noted that only U.S. transactions valued at over $2 million are included, with data current as of June 30, 2017.

Notable transactions year-to-date include: McKesson’s acquisition of CoverMyMeds for up to $1.1 billion in cash; Teladoc’s $440 million acquisition of Boston-based Best Doctors; and Castlight Health’s $135 million acquisition of the employee health platform Jiff. Additionally, Apple acquired Beddit, a consumer-focused sleep monitoring system, on undisclosed terms.

In recent years, digital health companies have been popular acquisition targets, accounting for 24 of the deals among the companies we track. However, year-to-date, nearly all types of acquirers—including digital health firms, medical device manufacturers, payers, technology companies, and healthcare providers—have engaged in half as much M&A activity in the first half of this year as would have been projected based on last year’s total deal volume.

The top five subsectors in the M&A exit rankings include: Payer Management, Healthcare Consumer Engagement, Analytics/Big Data, Corporate Health, and Life Sciences Tools. Two of these subsectors—Healthcare Consumer Engagement and Analytics/Big Data—also appeared on the list of the most investor-popular sectors.

Furthermore, the inclusion of the payer management and corporate health subsectors in the M&A exit rankings indicates that many companies are not focused on the direct-to-consumer market. Corporate health companies are gaining momentum, with five M&A transactions recorded in the first half of this year alone, compared to a total of only six such deals across the entire years of 2015 and 2016.

However, as previously mentioned, half of the companies on the investment ranking list remain consumer-centric, focusing on areas such as consumer health information, smart fitness devices, and consumer engagement in healthcare.

Therefore, if mergers and acquisitions as an exit strategy reflect the dominance of traditional enterprises in the healthcare sector, then judging from the list of investments most favored by investors,Investors remain highly bullish on the potential of companies targeting the consumer market.. Moreover, according to Rock Health’s previously released annual consumer survey report, numerous consumers are also highly interested in the development of such companies.

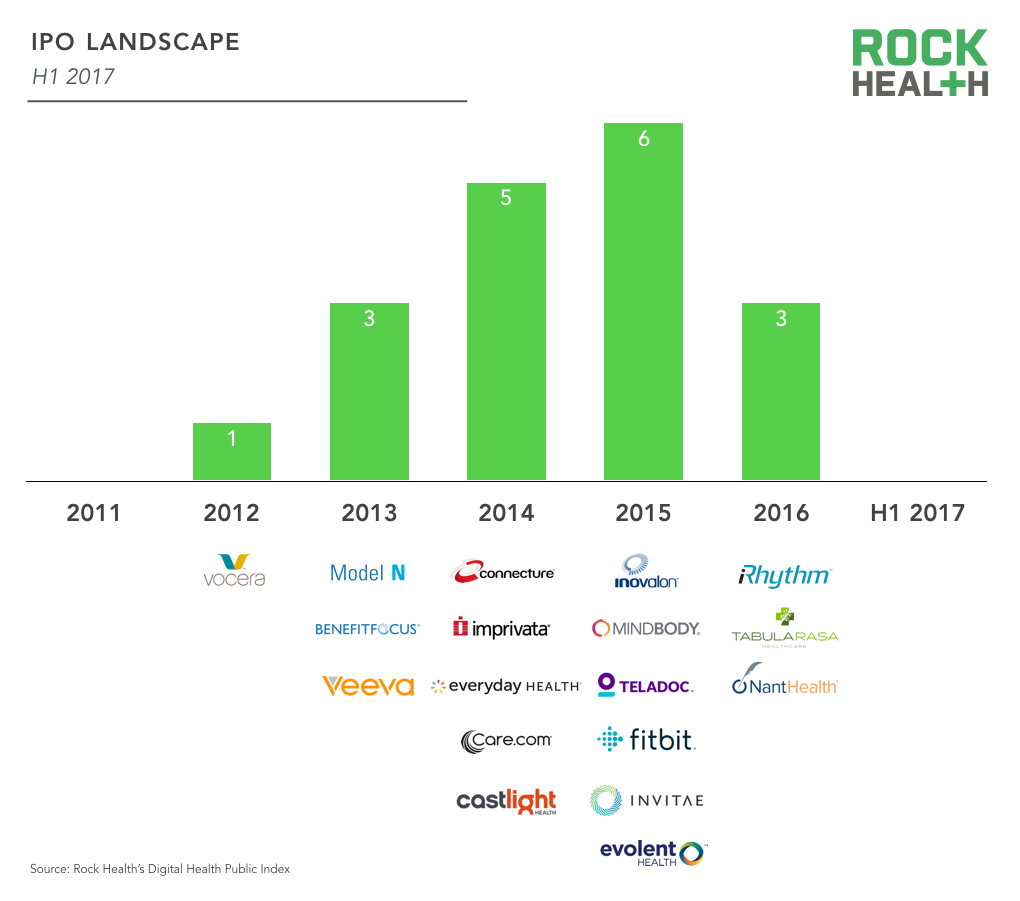

No IPO has occurred from 2017 to date, but a breakthrough is expected within the year.

From 2017 to date, there have been a total of 70 IPOs, including 11 in the software industry, 14 in the biotechnology industry, and zero in the digital health industry. (Editor’s note: Although Blue Apron went public in late June, it is not included in these statistics as it does not fall under our definition of a digital health company. Headquartered in New York, the company provides fresh ingredients and corresponding recipes to millions of users each month, aiming to promote user health through nutritional planning. Consequently, some industry peers consider it a member of the digital health sector.)

Although IPO activity in the digital health sector was nearly nonexistent in the first half of 2017, we still believe that many highly capitalized digital health companies will embark on their IPO journeys within the year.

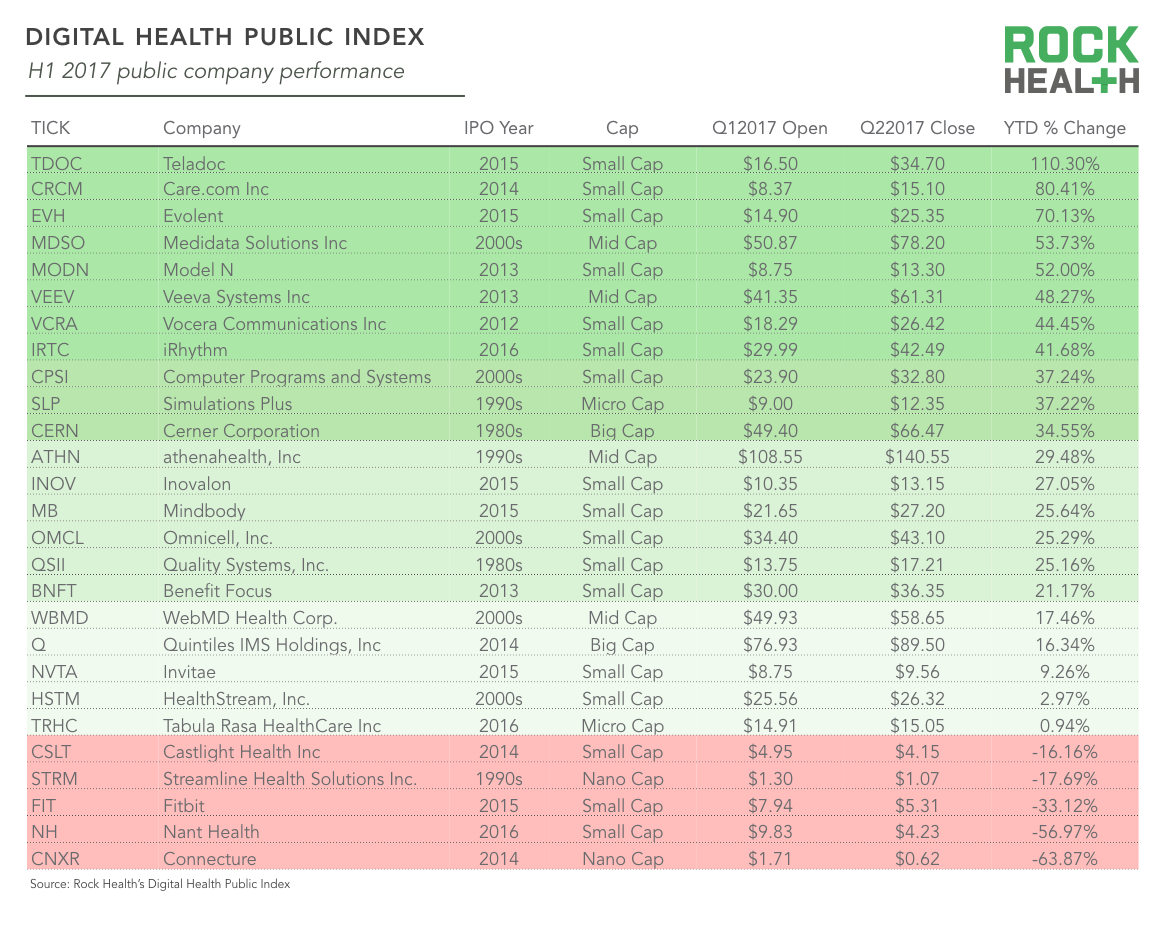

As shown in the figure below, overall, the index of listed companies in the digital health industry rose by 30% year-on-year in the first half of this year, while the S&P 500 Index increased by only 8%.

First half of 2017,Most digital health companies’ stocks posted positive returns this quarter, with the biggest winners including Teladoc (up 110%), Care.com (up 80%), and Evolent Health (up 70%).。

Compared with previous years, 2017 was more of a “transition year” for Fitbit, as it focused on exploring additional medical applications, and its stock hit a 52-week low during that quarter. In the digital health sector, only the five companies highlighted in red traded below their opening prices in 2017.

Future Outlook: Healthcare Policies Will Not Impact Investment Trends in the Second Half of 2017

We anticipate that the strong momentum observed in the first half of this year will continue throughout the full year, setting new records in total funding amount, number of transactions, and average deal size. With the robust growth of businesses across companies in the industry, we expect new digital health IPO activities to emerge in the near future.

We also hope that digital health will receive greater regulatory attention and clearer guidance. Just last month, newly appointed FDA Commissioner Scott Gottlieb announced the imminent launch of a new “Digital Health Innovation Action Plan.”

The initiative aims to further clarify digital health regulations and reform current market approval policies for digital health products, thereby eliminating the need for startups to seek the FDA’s position on each individual project during development. The industry has responded optimistically to the announcement, and its impact on the sector is expected to become increasingly evident in the coming months.

In the future, Rock Health will closely monitor the intense debate surrounding the healthcare industry (although we still believe that ambiguous policies will not affect investment and financing activities in the second half of 2017). Venture capitalists raise funds in advance and deploy them over several years; therefore, their investment transaction volumes do not necessarily align with the policy environment at any given time.

While the new U.S. policy may indeed jeopardize the survival of certain types of startups, it will also carve out new opportunities for others. Therefore, we anticipate a shift in the types of startups that secure funding in the future.

The focus of the U.S. government’s debate on healthcare policy is on reforming health insurance coverage (particularly Medicaid), but reforms to government payment and delivery systems are also proceeding in parallel. Neither the Republican proposals in the Senate nor those in the House of Representatives pose a threat to the CMS Innovation Center or MACRA (i.e., CMS’s new value-based payment program for clinicians).

Therefore, as healthcare services gradually shift toward value-based payment—a model supported by both the Democratic and Republican parties—the need for innovations to improve healthcare delivery remains urgent. How to provide lower-cost healthcare products to patient populations will continue to be a focal point of attention.

Furthermore, under the Trump administration, the trend of “patients as consumers” will continue to gain significant momentum. Although Republican proposals in both the Senate and the House of Representatives may increase patients’ healthcare costs, they will also create more opportunities for enterprises to innovate around providing more affordable medical solutions.

Regardless of the outcome of healthcare policy reforms, we look forward to seeing digital health startups continue to meet patients’ urgent needs and improve the quality of medical services.

References:

https://rockhealth.com/reports/2017-midyear-funding-review-a-record-breaking-first-half/