How 30 Real Estate Developers Entered Healthcare: Four Hard-Earned Lessons from Billions in Investments

By Luo Mei, Gao Kangping, Gao Daolong, Li Yanyu

As China enters an aging society, healthcare services will remain the most significant public livelihood demand for a considerable period in the future.

Keen-sensed developers, such as Vanke, Evergrande, Wanda, and Greentown, have already deployed efforts in community services, particularly in the field of community health and medical services, through approaches they deem feasible, thereby spawning a large number of elderly care real estate projects or integrated medical-care initiatives.

National policies encourage private capital to invest in healthcare, vigorously promote new medical models, and especially advocate for a transition from “disease treatment” to “health intervention” centered around family doctor services.

Leveraging the community as an entry point, with its residents and their lifestyle needs serving as core resources, is a key focus for real estate developers. However, the specific form in which medical services should be delivered within communities remains a proposition under long-term exploration.

Real estate development trends are undergoing significant changes. First, there is a shift from product competition to service competition. Second, there is a transition from real estate development to community operations. Third, there is an expansion from single-property business to integrated, innovative community platform services.

These ongoing changes are driven by three factors: first, the inevitable shift in the real estate industry from new development to existing property management; second, the redirection of social capital spurred by emerging industries such as healthcare; and third, the broader trends of urbanization and urban renewal.

In 2011, Vanke applied to the Shenzhen municipal government for permission to operate medical facilities in Shenzhen. In 2013, Vanke Children’s Hospital was slated to be located in the Bao’an Central District of Shenzhen, but it had not yet entered the construction phase. Also in 2013, Vanke announced a joint investment totaling RMB 250 million with Shanghai New Hongqiao International Medical Center and Fudan Medical Industry Investment Co., Ltd., among others, to establish the Fudan-Vanke International Children’s Hospital.

Yihua Health entered the healthcare sector in 2014 by acquiring 100% equity interest in Guangdong Zhongan Kang Logistics Group Co., Ltd. for RMB 720 million. The latter is a professional service provider specializing in “integrated non-clinical” comprehensive medical logistics services. In October of the same year, the Guangdong Internet Hospital, established in collaboration with the Second People’s Hospital of Guangdong Province, was officially launched. In February 2015, Yihua Real Estate was renamed Yihua Health, marking its formal entry into the healthcare industry.

In March 2015, Lujing Holdings entered into a strategic partnership with Beijing Children’s Hospital. In September, the company unveiled a private placement plan to raise RMB 10.05 billion. The proceeds were earmarked for the construction of four physical hospitals—namely, the Beijing Children’s Hospital Group Oncology Hospital (RMB 1 billion), the Beijing Children’s Hospital Group Hospital for Pediatric Genetic Disorders (RMB 960 million), the Tongzhou International Oncology Hospital (RMB 2.3 billion), and Nanning Ming’an Hospital (RMB 2.1 billion)—one medical center, the Precision Oncology Medical Center (RMB 1.95 billion), and two platforms: the Cloud Platform for Pediatric Health Management (RMB 1.03 billion) and the Medical Health Data Management Platform (RMB 100 million). This move marked Lujing Holdings’ comprehensive transformation into the healthcare industry.

In January 2016, Wanda announced that it had signed a cooperation agreement with International Hospital Group (hereinafter referred to as “IHG”) in Beijing. Wanda would invest a total of RMB 15 billion to build three comprehensive international hospitals in Shanghai, Chengdu, and Qingdao. On April 6, 2017, Wanda Group formally signed a strategic cooperation memorandum with the Chengdu Municipal People’s Government. The two parties agreed to invest RMB 70 billion to create a world-class medical industry center. It is imperative for Wanda to transition to an “asset-light” operational model.

In addition to major developments in the real estate sector, the state has also introduced numerous policies for the big health industry.

In December 2010, the “Opinions on Further Encouraging and Guiding Social Capital to Establish Medical Institutions” explicitly proposed encouraging social capital to invest in healthcare. Encouraging and guiding social capital to establish medical institutions helps increase healthcare resources, expand service supply, and meet the multi-level and diversified healthcare needs of the public.

In October 2013, the State Council issued the “Several Opinions on Promoting the Development of the Health Service Industry,” further clarifying a diversified landscape for medical service provision and guiding resources toward scarce types of medical institutions. Enterprises, charitable organizations, foundations, commercial insurance institutions, and other entities are encouraged to invest in the healthcare service sector through various models, including establishing new facilities, participating in restructuring, entrusted management, and public-private partnerships. Meanwhile, approval procedures for project initiation, establishment, practice licensing, and designation as medical insurance providers have been streamlined for scarce-type medical institutions such as rehabilitation hospitals, geriatric hospitals, children’s hospitals, and nursing homes.

The Opinion proposes that by 2020, a health service industry system covering the entire life cycle will be basically established, creating a number of well-known brands and healthy, self-sustaining clusters of health service industries, with the total scale of the health service industry reaching more than 8 trillion yuan.

In January 2014, the “Several Opinions on Accelerating the Development of Socially Run Medical Institutions” was issued, fully opening up the medical sector to social capital and simplifying and lowering approval thresholds. For applications regarding the establishment of non-public medical institutions, the evaluation will focus on key indicators such as personnel qualifications and technical capabilities. Requirements for operational metrics, including bed capacity and outpatient/emergency visit volumes, may be applied with appropriate flexibility based on actual circumstances.

On March 30, 2014, the State Council issued the “Notice on Printing and Distributing the Outline of the National Healthcare Service System Plan (2015–2020),” proposing to vigorously develop non-public medical institutions, actively promote the development of mobile internet, the application of health big data, and health information services and smart healthcare services that benefit the entire population.

In June 2015, the “Several Policy Measures on Promoting the Accelerated Development of Socially Operated Medical Institutions” was issued, incorporating socially operated medical institutions into medical insurance schemes and allowing for-profit healthcare institutions to access capital markets through listing, thereby further relaxing market entry requirements. The policy also streamlined and standardized approval procedures for medical institutions, publicly disclosed regional healthcare resource planning, and controlled the scale expansion of public hospitals. Meanwhile, it implemented tax policies and included socially operated medical institutions in the designated network of medical insurance providers.

On June 24, 2016, the State Council issued the "Guiding Opinions on Promoting and Regulating the Application and Development of Health and Medical Big Data," pointing out that health and medical big data are important foundational strategic resources for the country. It specifically mentioned "Internet + Health and Medical Care," encouraging cooperation between the government and social forces, focusing on revitalizing and integrating existing resources, actively encouraging social forces to innovate and develop health and medical services, integrating online and offline resources, and exploring internet-based health and medical service models. Efforts will be made to increase policy support. The promotion and application of Public-Private Partnership (PPP) models will be encouraged, guiding social capital to participate in the infrastructure construction, application development, and operational services of health and medical big data.

In September 2016, China’s first industry standard for “Specification for Elderly Tourism Services of Travel Agencies,” drafted under the leadership of Professor Yao Yanbo from the College of Tourism and Service Management at Nankai University, was approved and announced by the China National Tourism Administration and officially implemented on September 1, 2016.

On October 25, 2016, the Central Committee of the Communist Party of China and the State Council issued the Outline of the “Healthy China 2030” Plan, which serves as the action guide for advancing the construction of a Healthy China over the next 15 years. The Outline points out the need to establish a “trinity” mechanism for major disease prevention and control involving specialized public health institutions, general and specialized hospitals, and primary healthcare institutions; to establish mechanisms for information sharing and interconnectivity; to promote the integrated development of chronic disease prevention, treatment, and management; and to achieve the integration of medical care and disease prevention.

In particular, for the elderly population, the Outline emphasizes advancing the development of healthcare service systems for older adults and extending medical and health services into communities and households. It calls for improving collaboration mechanisms between medical institutions and eldercare facilities, supporting the provision of medical services within eldercare institutions. The integration of traditional Chinese medicine with eldercare should be promoted to advance combined medical and eldercare models, providing older adults with integrated health and eldercare services encompassing inpatient treatment during acute phases, nursing care during rehabilitation, daily living assistance during stable phases, and palliative care. This approach aims to closely align comprehensive prevention, control, and management services for chronic diseases with home-based, community-based, and institutional eldercare. Social forces are encouraged to establish institutions that integrate medical and eldercare services.

As evident from the aforementioned documents, the health service industry is a strategic sector earmarked for unequivocal national development in the future. With a massive market size exceeding RMB 8 trillion, it warrants in-depth cultivation and strategic positioning. Furthermore, the state adopts an attitude of active support and vigorous promotion toward “Internet + Healthcare,” while simultaneously encouraging non-governmental entities and social capital to participate in the health service industry.

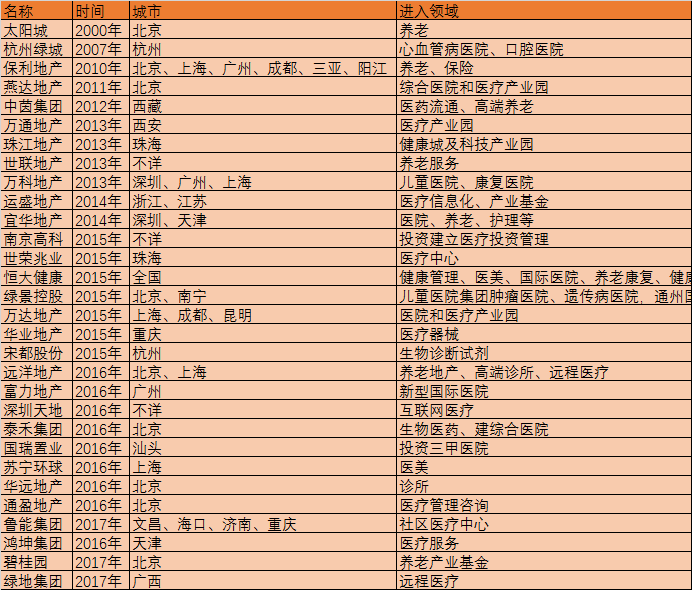

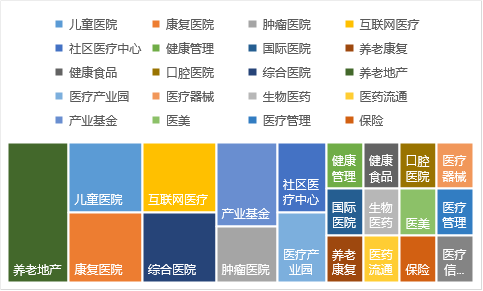

So, which real estate developers have entered the healthcare industry? As shown in the figure:

Note: The data collected in this article includes only “real estate + healthcare” projects and some representative senior living real estate projects.

Based on incomplete statistics, this article examines the healthcare business layouts of these 30 real estate developers, with data analyzed across several dimensions: timeline, real estate company, sector, capital scale, entry mode, and partners.

Data source: as of July 20, 2017

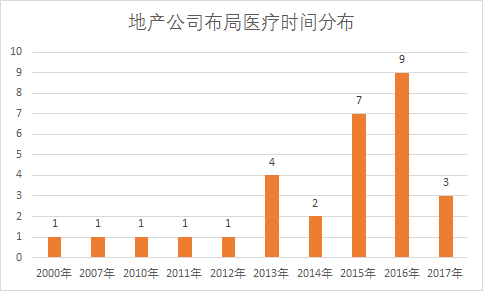

First, in terms of the timing of real estate developers’ entry into the healthcare sector, the earliest instance occurred in 2000 with one company, while the peak was reached in 2016 with nine companies. Entries were relatively concentrated in 2013, 2015, and July 2017. It is evident that prior to 2012, few real estate developers ventured into the healthcare field, whereas after 2013, there was an explosive growth in such entries.

From a temporal perspective, several factors contributed to the surge in the real estate and healthcare sectors in 2013. One key factor was the advent of the so-called “Silver Age” of the real estate industry. At that time, Yu Liang, President of Vanke Group, published an article stating that “the real estate industry has passed its golden age; the era when anyone could simply bend down and pick up gold is over, and real estate has entered the Silver Age.” Around this period, real estate companies began to diversify their business operations, venturing into energy, commerce, logistics, education, healthcare, and other fields, with healthcare and wellness emerging as a particularly significant segment. In that year, real estate firms such as Vanke, Winson, Pearl River, and Worldunion commenced their expansion into the healthcare sector.

For instance, Vanke had previously established a specialized team for elderly care real estate, developing the “Suiyuan Jiashu” project in Liangzhu Cultural Village, and introduced the concept of “neighborhood-style elderly care” in 2013. Meanwhile, it launched projects in sectors such as elderly care, education, and logistics, positioning itself as an “urban supporting service provider.” Subsequently, it announced plans to build three children’s hospitals and collaborations with rehabilitation hospitals and general hospitals.

The second reason for the booming convergence of real estate and healthcare is that the medical and health sector itself is undergoing a significant period of transformation and upgrading, presenting an optimal window for market entry. Specific driving factors include demographic shifts stimulating demand for medical and health consumption, rising household incomes leading to greater willingness to invest in health-related needs, and government policies encouraging private capital to enter the healthcare sector. The synergy between endogenous factors and external environmental conditions constitutes the primary driver behind the explosive growth of the “real estate + healthcare” model.

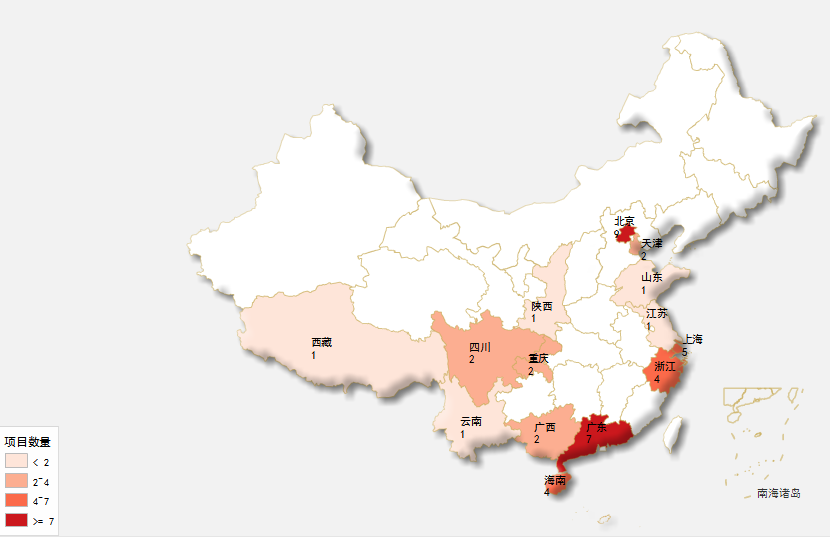

From a geographical perspective, real estate + healthcare projects are mainly concentrated in developed cities of developed provinces. For example, 9 projects have been implemented in Beijing, 7 in Guangdong, and Shanghai and Zhejiang each have 4 and 5 respectively. Other projects are distributed across multiple provinces and cities nationwide, including Sichuan, Chongqing, Hainan, etc.

Consequently, real estate-plus-healthcare projects are predominantly located in developed cities due to the local accumulation of high-end medical resources, enabling real estate companies to fully leverage these assets when establishing healthcare initiatives. Furthermore, as most real estate-plus-healthcare ventures focus on premium healthcare services, they can readily access a sufficient base of target audiences and consumers in these locations.

Two other locations worth mentioning are Hainan and Chengdu. Projects established in Hainan are predominantly focused on elderly care and health wellness, which aligns closely with the province’s strategic positioning. Leveraging its unique natural resource endowments, Hainan has long been a key region for domestic tourism, leisure, and real estate development. The State Council’s approval in 2010 to build an “International Tourism Island” further accelerated its emergence as a priority province for investment and development. Cities such as Sanya, Wenchang, and Haikou have become highly sought-after hubs for real estate development. Amid intensifying competition in the sector, enriching service offerings by integrating medical resources has become a key strategic measure for real estate companies. Notable examples include Poly Real Estate’s elderly care and insurance businesses, and Luneng Real Estate’s community medical center projects.

As a strategic pivot for the economy in western China, Chengdu has attracted increasing attention from investors in recent years. On one hand, it has laid a solid economic foundation by accommodating the transfer of manufacturing industries from coastal regions; on the other hand, it has encouraged the establishment of industries such as IT and biopharmaceuticals, thereby attracting an influx of industrial talent. A case in point is the “Medical Industrial Park” cooperation agreement signed between the Chengdu Municipal Government and Wanda Real Estate in the first half of this year. With a proposed investment of RMB 70 billion, the project aims to introduce world-class hospitals and healthcare-related enterprises, adopting an “industry incubation” approach that differs significantly from other real estate-plus-healthcare models focused primarily on consumption.

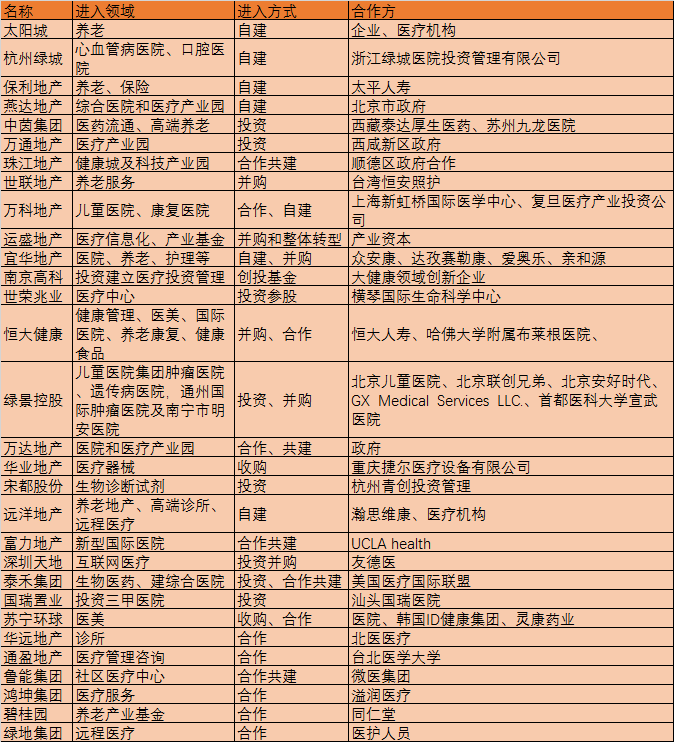

In terms of sector coverage, the projects undertaken by real estate companies essentially span the entire “pharmaceuticals, healthcare, and insurance” industry chain, with a particular focus on senior living real estate, hospitals, internet-based healthcare, industrial funds, and medical industrial parks.

Real estate companies entering the healthcare sector primarily consider synergy with their core businesses. Consequently, areas closely related to real estate development, such as hospitals and industrial parks, have become key investment focuses for the “real estate + healthcare” model, while investments in other sectors are determined based on long-term prospects and industry characteristics.

Taking senior housing real estate as an example, it essentially involves integrating elderly care facilities and services into traditional real estate development. The barriers to development and operation are relatively low. Furthermore, by collaborating with professional elderly care institutions during operations, developers can achieve a model characterized by “heavy capital investment but light operational burden.”

Among the collected data, the operational model of Sun City demonstrates typical characteristics. It officially launched its senior living community in 2003, adopting a business model primarily based on commercial real estate, with only a portion of its residential projects designated as senior apartments. Customer acquisition was achieved through a combination of sales and held assets. The community is equipped with facilities such as a community hospital, wellness center, and university for the elderly, providing comprehensive services encompassing housing, care, medical treatment, and health management for elderly residents. Currently, Sun City has developed senior living real estate projects in multiple regions across China, ranking among the most successful ventures in the sector.

In addition, hospitals—including general hospitals, children’s hospitals, oncology hospitals, and specialized hospitals—represent another key focus area for real estate developers’ strategic布局. Given their nature, such investments demand a higher degree of professional expertise. Common implementation approaches include acquiring or self-building hospitals and establishing hospital management companies. The primary objective of hospital construction is to serve residents within the developers’ property projects. However, such projects are highly susceptible to failure due to factors such as lengthy approval processes, extended investment cycles, shortages of qualified personnel, and inadequate operational capabilities. For instance, Vanke’s 2013 announcement to establish three children’s hospitals ultimately did not progress to the implementation stage for these reasons.

If direct entry into the healthcare sector by real estate developers is prone to setbacks, there is an alternative indirect approach: industry funds. Previously, VCBeat compiled data on healthcare-related industry funds established by listed companies since 2015. The number of such funds exceeded 100, with a total scale surpassing RMB 100 billion. Among the participants, real estate developers were present, though more often in the role of partners rather than lead initiators. Based on the data we have collected for this analysis, only two medical funds were initiated primarily by real estate companies: the industrial M&A fund established by Winson Real Estate in 2014, and the elderly care industry fund launched by Country Garden in April of this year.

Real estate companies, with their ample cash flow, face no financial pressure in establishing small- to medium-sized funds ranging from hundreds of millions to billions of yuan. The key lies in identifying suitable investment projects and ensuring effective post-investment operations. The projects they invest in are also expected to align with the sectors the real estate companies intend to enter. By “substituting self-construction with investment,” these companies can similarly achieve the effect of cross-industry expansion into healthcare.

Overall, the primary focus of the real estate plus healthcare model remains on medical services, with limited involvement in upstream and downstream pharmaceutical production or hospital management. The strategy emphasizes synergy with the core real estate business, prioritizing functional integration over broad operational expansion.

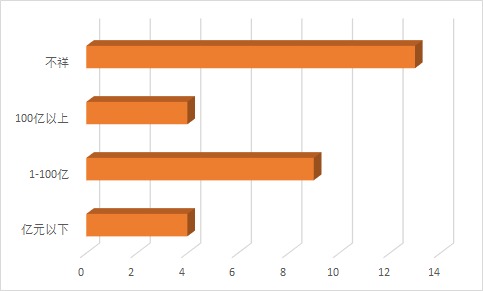

From the list, it can be seen that the investment scale of real estate developers entering the medical field is mainly classified into three categories: 1-10 billion yuan, over 10 billion yuan, and above 10 billion yuan. Meanwhile, those without disclosed detailed amounts are categorized separately.

In terms of scale, projects are primarily concentrated in the range of RMB 100 million to RMB 10 billion, with RMB 1 billion being the most common. For real estate companies, investments within this range are quite suitable. Given their size, such investments offer excellent opportunities for trial and error; even if an investment fails, they can exit quickly. This also facilitates simultaneous business expansion across multiple regions, providing greater scalability. Furthermore, healthcare is not a capital-intensive sector, so its demand for funding is relatively modest.

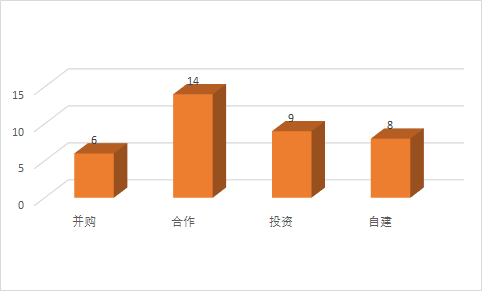

According to the list, real estate developers enter the healthcare sector primarily through mergers and acquisitions, partnerships, investments, and self-built projects.

Collaboration is the primary mode of entry for the "real estate + healthcare" model. The main reason real estate companies choose to enter the healthcare sector through partnerships is their lack of familiarity with the industry; therefore, they need to identify suitable partners to provide support, thereby gaining successful operational experience and ensuring effective resource implementation.

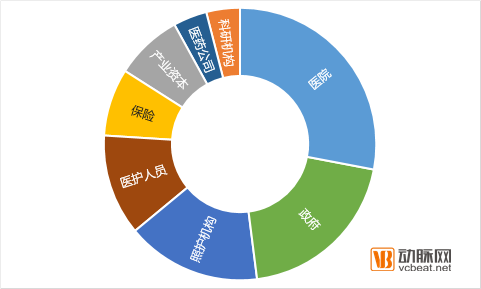

In terms of specific distribution, hospitals, government entities, care institutions, and healthcare professionals are the primary partners for real estate companies, while other stakeholders such as industrial capital, insurance institutions, and pharmaceutical and medical device companies also account for a certain proportion.

In summary, the above analysis leads to systematic conclusions regarding the “real estate + healthcare” model. First, the emergence of this model is driven by both environmental factors—namely, adjustments in the real estate sector and the development of the healthcare industry—and external factors related to real estate companies’ strategic efforts to achieve synergistic layouts. In terms of specific implementation, real estate companies expand their healthcare initiatives with a focus on their core business. Whether developing senior living properties or integrating hospitals into building projects, the primary target audience remains the residents or users of their own developments, indicating limited external spillover effects. Second, when entering the healthcare sector, real estate companies need to collaborate with professional institutions or organizations, relying on these partners to provide management support or business consulting services.

From an investment perspective, there have been relatively few healthcare investment funds initiated by real estate companies, or direct investments in the healthcare sector. This is because healthcare is inherently a long-cycle industry with slow capital recovery, which differs significantly from the construction and capital recoupment cycles typical of real estate firms, making it less attractive to such companies.

In fact, it is no longer novel for real estate developers to pivot, and they have adopted diverse approaches to enter the healthcare sector. However, while transitioning into a new industry may be straightforward, how can one truly take root and flourish within it?

A reporter reached out to an entrepreneur who is well-versed in both healthcare and real estate and is currently thriving in the medical industry, hoping to draw insights from his experience and offer food for thought to real estate developers.

This entrepreneur is Yu Haobo, a physician by profession. He serves as the Chairman of Liaoning Weilan Real Estate Development Co., Ltd. and the Chairman of Blue Card (International) Health Group. He has introduced the innovative concept of “Third-Generation Housing” and the widely acclaimed “Blue Card Model.”

So, what steps did Yu Haobo take on the path to success?

Step 1: From Real Estate to Senior Living Real Estate

In Yu Haobo’s view, real estate developers have gone through three stages: the first generation of housing consisted of employer-assigned accommodations; the second generation introduced property management services. “We see that properties are well maintained, yet those who create value for these homes do not receive adequate care.” Therefore, he proposed that, building upon the property management foundation of the second-generation housing, the focus should be elevated to encompass health, medical care, and humanistic support for residents—defining what he calls the third generation of housing.

On the other hand, Yu Haobo also felt that transformation was essential to differentiate his business from other real estate developers. Thus, he considered senior living real estate a potential shortcut. However, upon actually entering this sector, he realized that the core of senior living real estate is not “real estate,” but rather “senior care.”

Currently, only a small proportion of elderly people receive care in institutional settings, with the majority opting for home-based care. During his practice, Yu Haobo identified healthcare as the most significant challenge in home-based elder care. While daily caregiving services can be outsourced to confinement nannies or personal care aides at varying costs ranging from several thousand yuan, medical expenses constitute the largest portion of expenditures. It is virtually impossible to hire a full-time general practitioner from Peking Union Medical College Hospital to provide dedicated care for an elderly individual, given the distinct professional value and scarcity of such medical expertise.

Step 2: From Senior Living Real Estate to Medical Services

After some time, Yu Haobo shifted his focus from elderly care to healthcare. This is because elderly care is a systematic endeavor, with healthcare at its core; by excelling in healthcare, the provision of elderly care naturally follows.

Since he has chosen to enter the healthcare industry, he must be determined to burn his bridges. He began to analyze the pros and cons of mergers and acquisitions, partnerships, and self-built facilities one by one:

For instance, in the case of mergers and acquisitions (M&A), funding is not an issue for real estate developers. The key question is what targets they can actually acquire. Could they, for example, acquire Peking Union Medical College Hospital?

From the perspective of healthcare institutions themselves, those with high brand recognition are generally not available for acquisition; institutions that are open to being acquired may often have relatively weak brand presence.

If he opted for collaboration, there were few institutions available to Yu Haobo at the time. He had always aimed to provide high-quality community medical services to residents and sought partnerships with renowned Grade A tertiary hospitals. However, physicians at these hospitals were overworked and unwilling to leave their positions in public hospitals, making this path unfeasible as well.

"Why not just build it from the ground up?" he began to consider. By his standards, establishing a community-based medical and diagnostic facility was not as simple as opening a small clinic, hiring a few doctors and nurses, and purchasing some medical equipment.

Step 3: Establish the Blue Card Medical Service Model

Since we are entering the healthcare sector, we must offer a comprehensive suite of services. He aims to provide residents with a complete healthcare solution that integrates an online network with a network of offline clinics. The online network serves as the technological backbone for the offline clinic network. This model is analogous to the Taobao platform, which supports numerous individual Taobao stores; in this context, each store represents a medical institution within various elderly care communities.

With his background as a physician, he holds distinct advantages in designing the architecture of healthcare services. To deliver specialized services that address the comprehensive needs of individuals, he founded Blue Card (International) Health Group after extensive research, exploration, and inquiry.

This group is an international, standardized, professional, and multi-dimensional service organization. Guided by the mission of “promoting health concepts and enjoying a healthy lifestyle,” it integrates high-quality global medical and healthcare resources, adopts advanced international health management technologies and service models, and operates as a chain service provider offering personal healthcare physicians and exclusive personalized health solutions. Leveraging modern “mobile cloud” technology and the Blue Card Headquarters Cloud Platform, it facilitates seamless communication between members and expert medical teams, ensuring 24/7, 365-day-a-year health protection for its members.

Step 4: Partner with real estate developers, with Blue Card providing medical services

Now, Yu Haobo has come up with the simplest way to replicate the Blue Card model: partner with real estate developers. The developers will focus entirely on building housing, while medical services are provided through clinics affiliated with the Blue Card program, thereby completing the elderly care service offering. Developers specialize in property development, professional medical teams handle healthcare services, specialized elderly care teams manage senior living services, and dedicated catering teams provide food services.

There are three types of collaboration models:

The first model involves the developer taking a hands-off approach, focusing solely on delivering high-quality park services, while BlueCard establishes a wholly-owned clinic within the park.

The second model involves developers recognizing the value of elderly care services and being willing to collaborate with Blue Card to jointly establish clinics.

The third model is the franchise approach.For example, a developer may wish to provide a comprehensive suite of medical services independently but face challenges in designing service workflows, procuring medical equipment, and coordinating with specialists. By partnering with LanKa through a franchise model, the developer can gain access to support spanning initial design, equipment procurement, clinic renovation, and long-term operational management. Through these three models, Yu Haobo aims to expand the LanKa model across China.

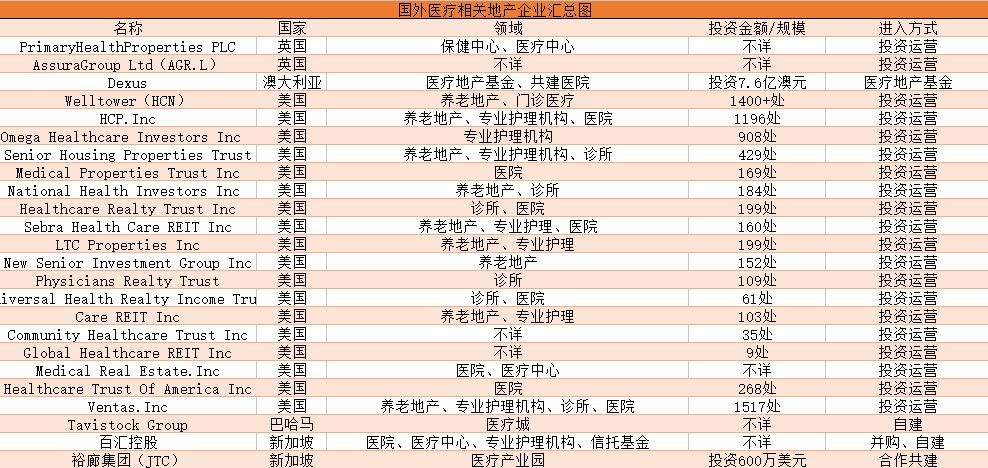

In China, the trend of real estate companies entering the healthcare sector has become widespread. What about abroad? Which international real estate developers have ventured into healthcare, and how have they approached it?

Let's first look at some overseas healthcare + real estate data:

Note: In the “Investment Amount/Scale” column of the table, the investment amount is denominated in currency, indicating a total investment of XX yuan for the project; scale is measured in “locations,” referring to the company’s ownership of XX properties.

U.S. Healthcare Real Estate Investment Trusts (REITs)

Unlike domestic real estate developers in China, which invest in and primarily operate medical institutions, the U.S. real estate sector mainly adopts the “Real Estate Investment Trust” (hereinafter referred to as “REITs”) model. REITs are companies that own and operate income-generating real estate assets. These owned and operated real estate assets span various industries, with the healthcare sector being just one component.

“Healthcare Real Estate Investment Trusts” primarily operate the following projects:

1. Senior Housing: Includes mutual-aid senior living and independent living, both of which provide medical services;

2. Hospital Projects: The majority of hospital projects are long-term care facilities and long-term continuous medical nursing homes;

3. Skilled Nursing Facility (SNF): Primarily provides long-term care for elderly patients, covering services that do not require the support or resources of an acute-care hospital;

4. Medical Office Building: Medical office buildings are among the few pure healthcare-related assets invested in by Healthcare Real Estate Investment Trusts (REITs), including physician clinics, ambulatory surgery centers, and more;

5. Biotech Parks (Life Science Lab): A very small number of healthcare real estate investment trusts (REITs) operate life science park laboratory projects, which are not mainstream in the healthcare real estate sector.

In summary, the primary scope of the U.S. "healthcare real estate" sector encompasses healthcare service institutions focused on outpatient and ambulatory surgical care, as well as service areas that do not rely heavily on advanced medical technologies or facilities but require long-term medical support and collaboration.

U.S. healthcare real estate investment trusts (REITs) primarily operate their properties through two models: the net lease model and the triple-net lease model.

Under the net lease model, REIT companies lease senior care/medical properties to operators and collect fixed annual rent (the gross rental yield for senior living communities is typically 8–12% of the property value, adjusted upward based on the Consumer Price Index), while all direct operating expenses, community maintenance costs, taxes, insurance premiums, and other related fees are borne by the lessee.

Therefore, under the net lease model, REIT companies maintain high gross profit margins, with net rental income accounting for over 80% of gross rental income. They bear virtually no operational risk, and their performance is less affected by financial crises (unless tenants go bankrupt). In contrast, tenants (operators) retain all operating revenue and the residual income after deducting rent expenses and operating costs, while assuming the majority of operational risks.

Under the entrusted operation model, REIT companies entrust their properties to operators. The operators charge an annual management fee equivalent to 5–6% of operating revenue, but they do not bear the risk of operational losses nor do they receive residual earnings. All operating revenue belongs to the REIT company (in the United States, the operating revenue per unit in senior living communities is approximately $3,000–$4,000, which is 3–4 times the rental income), and all operating costs are also borne by the REIT company. Correspondingly, the REIT company receives rental income and residual operating earnings, while assuming the majority of operational risks.

Under the net lease model, REITs face the lowest risk and enjoy the most stable returns. Therefore, to reduce capital costs, traditionally, the majority of properties held by REITs are operated under net leases, while a small portion are managed under entrusted operation models.

Case: U.S. HCN: A 5×5 Diversified Investment Matrix

In the United States, large REITs typically adopt an umbrella partnership structure, acquiring property assets from other companies in exchange for non-controlling interests in their REIT subsidiaries. This asset-for-equity swap creates a win-win scenario: sellers can defer capital gains taxes until they liquidate their shares and participate in any appreciation of the assets during that period, while the REIT reduces acquisition costs and avoids excessive dilution of its parent company’s equity. In recent years, HCN has acquired approximately $1 billion worth of property assets through DownREIT transactions.

Take Health Care REIT (ticker: HCN), a 46-year-old company with a portfolio of 1,328 properties and a market capitalization of $27.3 billion, as an example. HCN is a true giant among healthcare REITs, with its property types covering the four tenant categories encompassed within the scope of healthcare REIT real estate usage:

· Senior Living Apartments (for individuals aged 55 and older who do not require extensive medical care)

· Private nursing homes (housing elderly residents requiring medical care, equipped with medical devices and staff)

· Medical Office Building (for doctors and other professionals)

·Hospital Building

87% of its revenue comes from self-pay medical institutions, so changes in the government health insurance system have little impact on it. This gives it an absolute advantage in the industry. In addition, HCN’s revenue figures are also very impressive, with double-digit growth in operating income in recent years, and dividends and FFO (funds from operations) are advancing hand in hand:

As the largest senior housing REIT in the United States, HCN emphasizes diversification across investment channels and asset types, proposing a “5×5” investment model. This approach employs five investment channels—leased properties, investment management platforms, development and redevelopment, debt investments, and DownREITs (umbrella partnership real estate investment trusts)—to invest in five asset classes: senior living communities, life science properties, medical office buildings (MOBs), skilled nursing facility properties, and hospital properties.

In terms of operations, HCN is less directly involved in the development and redevelopment of senior living communities. However, in other healthcare real estate sectors, such as life science laboratory buildings or medical office buildings, HCN will moderately participate in development if pre-leasing rates exceed 50%. Overall, the total value of its land bank and properties under construction does not exceed 5% of its total assets.

In terms of debt investments, HCN held bonds of several senior housing and healthcare real estate companies during the financial crisis. As a major creditor, HCN seized advantageous opportunities for distressed acquisitions during subsequent debt restructurings. For instance, in its 2010 acquisition of HCR ManorCare, HCN leveraged its position as a creditor, having previously held $1.72 billion in debt issued by HCR ManorCare. By the end of 2010, its $2 billion portfolio of debt investments generated $160 million in interest income for the company.

Australian Healthcare Property Trust

In Australia’s real estate investment trust (REIT) sector, diversified REITs dominate, with primary investments directed toward industrial assets, office buildings, and shopping centers. By contrast, in the more developed U.S. market, REIT investments are more diversified. The S&P U.S. REIT Index shows that 13% of investments are allocated to hospitals and tourist resorts, 16% to residential properties, and 13% to other specialized property categories, including prisons, data centers, and baseball stadiums.

Australia’s healthcare sector is underinvested, presenting significant long-term opportunities. Demand for healthcare services is driven by favorable demographic trends. As healthcare constitutes an essential, non-discretionary consumer good, medical real estate is less susceptible to cyclical factors compared to other property types.

The total value of Australia’s healthcare real estate is estimated at AUD 125 billion, with the asset scale of hospitals and medical centers alone comparable to that of the entire industrial real estate market. Meanwhile, the total size of pension funds amounts to USD 1.5 trillion.

Case: Australia's Dexus Group

Dexus is one of the top 50 companies by market capitalization on the Australian Securities Exchange, specializing in office and industrial property investments in Australia. It currently holds assets exceeding AUD 22 billion across the country, directly owning assets worth AUD 11 billion, while managing AUD 11.7 billion worth of office, retail, and industrial properties for third-party clients. Its services extend to over 30,000 professional investors in more than 20 countries.

Established in 1984, Dexus has navigated the Australian real estate landscape for 33 years. Now, this giant among Australian real estate investment trusts (REITs) is diversifying into the emerging sector of healthcare real estate. Its asset-light model has enabled Dexus to achieve higher returns and a lower ratio of negative equity.

On June 28, 2017, Dexus announced a joint venture with Commercial & General (C&G) to establish a joint platform and launch an institutional unlisted healthcare property fund. The fund’s seed assets comprise two hospitals in Adelaide valued at AUD 370 million, one of which is under construction. The new fund will also pursue additional investment opportunities in New South Wales and Queensland, with a further AUD 390 million in capital commitments.

The fund’s responsible entity will be wholly owned by the Dexus Group as part of its capital management platform. As part of the joint venture, Dexus and C&G will jointly invest in the fund and establish a co-investment manager. Dexus’s initial co-investment amounts to approximately USD 80 million.

Dexus stated that it looks forward to expanding the scale of its healthcare property investment portfolio together with C&G, believing that it will benefit in the future from the mega-trends of population growth and aging.

Currently, the seed assets of Dexus’s Australian Healthcare Fund are Adelaide Hospital and GP Plus Health Care Centres.

Calvary Hospital Adelaide is a 57,000-square-meter private hospital currently under construction. Located at the corner of Angas and Pulteney Streets in the Adelaide Central Business District, the hospital will provide clinical services, consulting suites, and a 24-hour emergency department. Its accommodation capacity includes 343 overnight beds, comprising an intensive care unit with 62 beds.

The project commenced in May 2010 and was scheduled for completion in the first half of 2019. Upon completion, the hospital will be leased and operated by Calvary Health Care Adelaide Limited, with both parties having signed a 30-year triple net lease agreement.

Triple Net Lease: The designated lessee (tenant) is solely responsible for all costs associated with the leased asset, in addition to the rental fees specified in the lease application. This lease structure requires the lessee to pay the net amount of three types of costs, including net real estate taxes on the leased asset, net building insurance, and net common area maintenance. This type of lease is also known as a Triple Net (NNN) lease.

The GP Plus Healthcare Centre (Elizabeth, SA) is located at 16 Playford Avenue, Elizabeth, in the northern suburbs of Adelaide, and was completed in 2010.The property is a modern, campus-style, purpose-built primary healthcare facility offering 35 consultant suites. It is currently leased to the Government of South Australia, with a weighted average lease term (WALT) of 13 years and a net lettable area of 4,600 square meters.

Similar to U.S. REITs, the Australian real estate sector also adopts an asset-light operational model by channeling capital into healthcare real estate. While healthcare real estate shares some common drivers with office and retail properties, its distinguishing feature is longer lease terms, typically exceeding 20 years. Property holders are exempt from operational and management responsibilities and can achieve attractive risk-adjusted returns. For instance, in the aforementioned case of Dexus Group’s investment in Adelaide’s Calvary Hospital, a triple-net lease structure was employed. Under this arrangement, apart from the initial capital expenditure for property development, all other operating expenses are borne by Calvary Health Care Adelaide Limited, thereby generating stable returns following a one-time investment.

Real Estate Developers Pivot to Healthcare – Singapore’s Parkway Holdings

Parkway Healthcare Group is a member of Parkway Holdings (Singapore) Ltd. (hereinafter referred to as “Parkway”). Initially a small property developer, Parkway entered the healthcare industry after acquiring Gleneagles Hospital in 1987. In Singapore, Parkway operates Mount Elizabeth Hospital, Gleneagles Hospital, and East Coast Hospital.

Currently, the Group operates 15 hospitals across Asia, with 3,277 beds and over 1,500 renowned medical specialists, offering a wide range of specialized services. It has rapidly emerged as the largest publicly listed premium healthcare provider in Asia.

In 1987, Parkway acquired Gleneagles Hospital for S$46 million, thereby entering the healthcare industry.

In 1989, Parkway entered the Malaysian healthcare industry by acquiring a 70% stake in Penang Clinic, which was subsequently renamed Gleneagles Medical Centre Penang.

In 1995, Parkway acquired Mount Elizabeth Hospital and East Coast Hospital (now known as Parkway East Hospital), as well as the Shenton Medical Group’s primary care clinic chain in Singapore (now known as Parkway Shenton), thereby becoming Southeast Asia’s largest private healthcare provider.

On September 14, 2005, Parkway acquired a 31% stake in Pantai Holdings for USD 82.8 million, becoming the largest shareholder of Malaysia’s leading private healthcare service provider.

In 2012, Parkway was acquired by IHH Healthcare, the world’s second-largest healthcare group. Parkway’s business units are primarily divided into Parkway Pantai, Acibadem Holdings, International Medical College, and Parkway Life Real Estate Investment Trust, with a market valuation reaching $15 billion in 2016.

In accordance with the relevant agreements on China’s accession to the World Trade Organization, foreign investors were not yet permitted to establish wholly foreign-owned hospitals in China; instead, they could only operate joint-venture hospitals through partnerships with domestic hospitals. In 2007, Parkway acquired equity stakes in a medical center located in Shanghai and established the Gleneagles Surgery Center, thereby formally entering the Chinese market.

In addition to investment holding, in 2007, Parkway Holdings partnered with Huashan Hospital to establish the Shanghai Parkway Huaying Outpatient Clinic, with Parkway Holdings holding a 70% stake and total investment exceeding USD 8 million, making it the largest single foreign-invested project in China’s healthcare services sector to date.

During its overall transformation, Parkway Holdings, similar to some domestic real estate developers in China, opted for investment mergers and acquisitions or joint ventures, focusing on high-end medical services. This approach aligns with the strategies adopted by Chinese real estate giants such as Wanda, Evergrande, and R&F.

Meanwhile, Yunsen Real Estate (now transformed into Yunsen Medical), which also underwent a comprehensive transformation in China, primarily entered the market through healthcare informatization and industrial investment funds. In 2015, Yunsen Real Estate acquired 100% equity of Beijing Medix Technology Co., Ltd., with a total investment not exceeding RMB 550 million.

Yunsheng Medical focuses on internet-based health management, telemedicine, and medical services. Its subsidiaries and core partners include Shanghai Rongda Information and Singapore Jianzi Technology Co., Ltd. The company has achieved international or domestic leading standards in regional health informatization, ECG informatization, wearable devices, and cardiac data operational services. Yunsheng adopted a transformation strategy shifting from providing industrial products to delivering services, achieving a year-on-year revenue growth rate of 104.77% in 2016 (compared to -17.86% in the same period of 2015), with its operating income turning from loss to profit.