Challenges Remain as China Mandates Zero Drug Markup Policy Across All Public Hospitals by End of September

2017 can be described as a “major year” for healthcare reform. From the beginning of the year to the present, various competent authorities and local governments have successively issued nearly one hundred policies covering all aspects of pharmaceuticals, medical services, and more, marking the comprehensive entry of healthcare reform into deep waters.

In terms of healthcare service price reform, top-level design mandates “aggregate control, structural adjustment, selective increases and decreases, and gradual implementation.” The reform pathway has become increasingly clear, starting with measures such as separating medical services from pharmaceutical sales, introducing medical service fees, controlling the proportion of pharmaceutical costs, and curbing the consumption of medical consumables.

Since its implementation in 2009, the zero-markup policy has remained a focal point of discussion in healthcare reform. Recently, as the deadline for nationwide rollout approaches, the topic has become ubiquitous at industry seminars, emerging as a prominent feature of major summits. In light of this, VCBeat (WeChat ID: vcbeat) has compiled relevant policies and diverse perspectives to provide a comprehensive and detailed analysis of the objectives and challenges associated with the zero-markup policy.

The Drug Markup Policy Has Been in Place for Half a Century

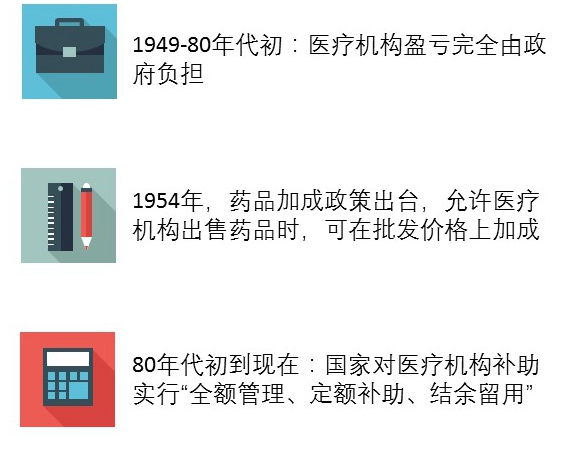

The introduction of the drug markup policy in public hospitals can be traced back to the mid-1950s. Prior to the implementation of drug markups, public hospitals were fully funded by the government. Medical service prices were kept low, and drugs were supplied at prices close to cost, with the aim of ensuring that low-income populations could afford medical care and medications. During this period, the government repeatedly reduced registration fees and bed charges to further alleviate the financial burden of seeking medical treatment.

The drug price markup policy was introduced in 1954. At that time, the state allowed medical institutions to add a markup to the wholesale price when retailing drugs, thereby establishing the retail price. The markup rates were capped at no more than 15% for Western medicines, 16% for proprietary Chinese medicines, and 29% for traditional Chinese herbal medicines. The purpose of this policy was to further supplement hospital operational funding beyond fiscal appropriations and to incentivize the provision of medical services.

By the 1980s, the revenue structure of medical institutions underwent another adjustment. The state implemented a policy of “full-scale management, fixed-amount subsidies, and retention of surpluses” for financial appropriations to medical institutions. Specifically, the government provided hospitals with fixed-amount subsidies based on the number of staffed beds, while the revenue generated independently by hospitals could be used to improve medical facilities or fund collective welfare and individual bonuses. This approach partially addressed the issue of insufficient fiscal investment, but also led to a rising proportion of drug revenue in hospital income.

Changes in China's Fiscal Policy for Public Hospitals

In their paper titled “A Historical Review of China’s Hospital Drug Markup Policy and Its Impact,” scholars Zhang Mo and Bian Ying from the Institute of Chinese Medical Sciences at the University of Macau presented statistical data showing that from 1984 to 1994, drug revenues of healthcare institutions nationwide increased by 5.6-fold, while drug expenditures rose by 6.5-fold during the same period. In 1994, drug revenues accounted for 55.3% of the total revenues of healthcare institutions. Subsequently, the proportion of drug revenues in the total revenues of healthcare institutions fluctuated around 50%, reaching 46% of operational revenues in 2008.

It can be said that drug markups have partially substituted for government fiscal inputs, becoming a significant source of revenue for public medical institutions, a situation known as “funding healthcare through pharmaceuticals.”

In 2009, the “New Healthcare Reform” was launched, initiating measures to address the practice of “funding healthcare through drug markups.” The Opinions on Deepening the Reform of the Medical and Healthcare System pointed out that drug price reforms should start at the grassroots level, transform the operational mechanisms of primary medical and healthcare institutions, reform the policy on drug markups, and implement zero-markup sales of drugs.

Within the public hospital system, emphasis is placed on the public-welfare nature and social benefits of public hospitals, adhering to a patient-centered approach and standardizing medication use, diagnostic examinations, and medical practices. We will promote the separation of pharmaceutical services from medical services and actively explore various effective methods to gradually reform the mechanism of “subsidizing healthcare with drug profits.” This includes gradually reforming or abolishing the drug markup policy through measures such as implementing differential markups for drug procurement and sales, and establishing pharmaceutical care service fees. Meanwhile, we will improve the compensation mechanism for public hospitals by appropriately adjusting medical service prices, increasing government funding, and reforming payment methods.

In the subsequent years, reforms of drug pricing were gradually rolled out. Starting in 2012, the zero-markup policy for pharmaceuticals was implemented in more county-level hospitals, and from 2013 to 2014, pilot programs for zero-markup drugs were launched in certain provincial and municipal tertiary hospitals. Following the implementation of the zero-markup policy, the proportion of drug revenue in total hospital income continued to decline, leading to significant changes in the composition of hospital revenue.

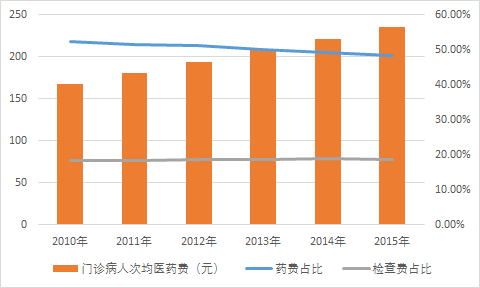

Table 1: Changes in Average Medical Expenses per Outpatient Visit and the Proportion of Drug Costs

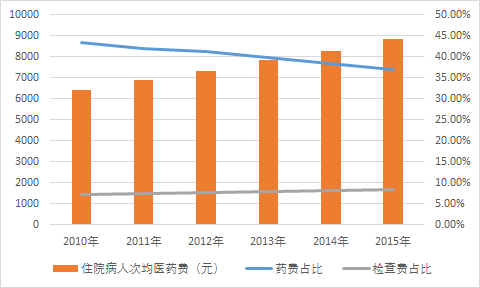

Table 2: Changes in Average Medical Expenses per Inpatient and the Proportion of Drug Costs

Source: Yixuejie Think Tank

The above data indicate that since the implementation of the zero-markup policy, both outpatient and inpatient average medical expenses have risen; however, the proportion of pharmaceutical costs has shown a year-on-year decline, while examination fees have exhibited a slight increase.

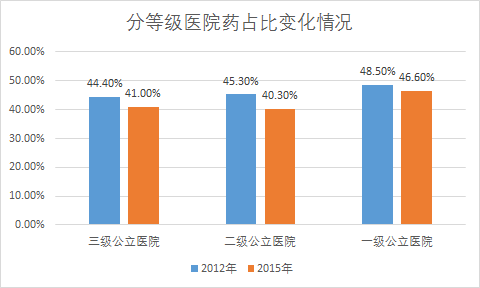

By hospital tier, drug revenue as a percentage of total revenue in tertiary public hospitals decreased from 44.4% in 2012 to 41.0% in 2015; in secondary public hospitals, it declined from 45.3% in 2012 to 40.3% in 2015; and in primary public hospitals, it dropped from 48.5% in 2012 to 46.6% in 2015.

Source: Medical World Think Tank

Zero-Markup Policy Enters Final Sprint Phase

From the implementation across various regions, we see both the structural adjustments of Beijing’s healthcare reform and the aggregate cost control measures characteristic of Guangdong’s healthcare reform.

On March 22 this year, the Beijing Municipal People’s Government issued the Implementation Plan for the Comprehensive Reform of Separating Prescribing from Dispensing. The plan aims to transform the operational mechanisms of public medical institutions and standardize medical practices by abolishing drug markups and establishing medical service fees. It seeks to reduce artificially inflated prices and costs of drugs, medical devices, and consumables through measures such as transparent procurement of pharmaceutical products and health insurance cost containment. Furthermore, it intends to regulate medical service pricing and gradually establish a dynamic adjustment mechanism for medical service prices based on changes in cost and revenue structures. The plan also strengthens supervision and management of medical institutions, improves cost and expense control mechanisms, establishes a classified fiscal compensation mechanism, and advances reforms in health insurance payment methods. These efforts are designed to enhance the public-welfare nature of public medical institutions and increase the public’s sense of gain.

According to relevant officials from the Beijing Municipal Health and Family Planning Commission, the post-reform drug pricing mechanism will be based on a transparent procurement system. This approach involves disclosing drug quality indicators and winning bid prices nationwide to all pharmaceutical manufacturers, while ensuring drug quality and safety. Additionally, information regarding medical institutions’ procurement, usage, and changes in drug varieties will be made public. These measures aim to eliminate the previous lack of transparency in drug pricing and related information. Under this new framework, drug procurement prices are expected to decrease by an average of 8%.

On July 23, marking 100 days since the implementation of Beijing’s healthcare reform, data released by the Beijing Municipal Health and Family Planning Commission showed that a total of 60 million patient visits had been recorded in Beijing since the new policy took effect on April 8. Estimates indicate an average daily reduction of RMB 35 million in medical expenses. Over the 100-day period, centralized “sunshine” procurement alone saved RMB 1.37 billion in drug costs, with the average drug price decreasing by more than 8% cumulatively.

While drug costs declined, adjustments were made to the pricing of medical services, with service fees increased. This had a favorable effect on patient triage and distribution: outpatient and emergency visits at tertiary medical institutions decreased by 12.7%, those at secondary hospitals decreased by 4.9%, while outpatient and emergency visits at primary hospitals and community health centers rose by 10%.

On May 5, the General Office of the State Council issued the "Key Tasks for Deepening the Reform of the Medical and Healthcare System in 2017," requiring that comprehensive reform of public hospitals be fully rolled out by the end of September this year, with all public hospitals abolishing drug markups (except for traditional Chinese medicine decoction pieces). Reforms in management systems, medical service pricing, personnel compensation, pharmaceutical distribution, and health insurance payment methods should be coordinated and advanced. The proportion of medical service revenue in total hospital revenue should be gradually increased. In 2017, the ratio of pharmaceutical expenditure to total medical expenditure (excluding traditional Chinese medicine decoction pieces) in public hospitals across the first four batches of 200 pilot cities was generally reduced to around 30%, and the cost of sanitary materials per 100 yuan of medical revenue (excluding drug revenue) was lowered to below 20 yuan. This also marks the final sprint phase for the complete abolition of drug markups.

On June 29, the website of the People's Government of Guangdong Province released the "Notice of the General Office of the People's Government of Guangdong Province on Issuing the Key Tasks for Deepening the Reform of the Medical and Health Care System in Guangdong Province in 2017" (hereinafter referred to as the "Notice"), which outlined 55 key tasks for healthcare reform. The Notice requires all public hospitals in Guangdong to completely eliminate drug markups (with the exception of traditional Chinese medicine decoction pieces) by the end of July, while simultaneously implementing adjustments to medical service prices.

Guangdong’s new round of healthcare reform places greater emphasis on “aggregate cost control,” namely, curbing the average growth rate of medical expenses in public hospitals through measures such as the two-invoice system, separation of prescribing from dispensing, and health insurance fund management, thereby ensuring that the overall growth in residents’ total health expenditure remains within a specified range (not exceeding 10%).

What Issues Remain to Be Resolved with Zero Markup?

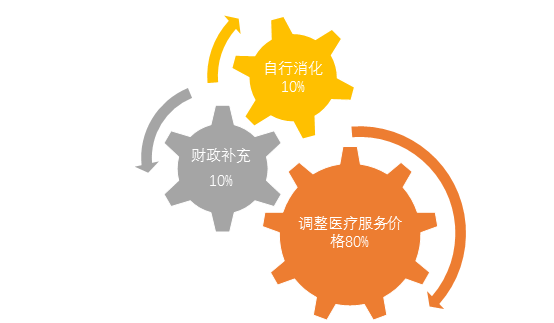

Following the elimination of drug markups, hospitals’ revenue shortfalls are covered through three channels: 80% from adjustments to medical service pricing, 10% from government fiscal subsidies, and 10% absorbed internally by the hospitals. However, in actual implementation, deviations may occur in all three areas.

For instance, following price adjustments for medical services, patients are likely to choose other hospitals due to the price increases; in regions with fiscal constraints, financial subsidies may not be fully implemented; and hospitals, lacking refined management capabilities, may be unable to absorb the revenue shortfall.

Similar cases have previously been reported in the media. At a conference in late 2016, Sun Hong, President of Xiangya Hospital of Central South University, stated that after the implementation of the zero-markup policy, Xiangya Hospital attempted to offset the resulting revenue loss by adjusting medical service prices. However, the increased revenue in the first quarter of 2016 compensated for only 50.78% of the decline. Although prices for a few medical services were subsequently adjusted, the compensation ratio reached merely 53% from January to August, falling far short of the 80% target projected by regulatory authorities. Based on these figures, Xiangya Hospital’s revenue was projected to decrease by RMB 200 million in 2016. To ensure that the compensation and benefits of medical staff remained unaffected, the hospital reduced its equipment procurement budget for 2017 by RMB 50 million.

According to Zhu Fu, President of the Affiliated People’s Hospital of Jiangsu University, Zhenjiang, Jiangsu Province, implemented the zero-markup drug pricing reform as early as 2013. The compensation mechanism was structured such that price adjustments in Jiangsu covered 77%, government fiscal subsidies accounted for 10%, and hospitals bore 13%. However, during implementation, fiscal funding was only provided in the first year; no further financial support was granted from the second year onward. Consequently, hospitals are required to absorb nearly one-quarter of the annual losses resulting from the zero-markup policy, imposing significant financial pressure.

To offset the losses resulting from the elimination of drug markups, some hospitals have sought to extract concessions from pharmaceutical suppliers by demanding kickbacks or prolonging payment delays. Given that hospitals serve as the primary distribution channel and hold a monopolistic position in drug sales, suppliers find it difficult to challenge the bargaining power of these institutions. Consequently, the pressure stemming from the abolition of drug markups has been partially shifted onto pharmaceutical suppliers.

Furthermore, after the elimination of drug markups, pharmaceuticals effectively became an operational cost for hospitals, prompting some institutions to pilot “pharmacy trusteeship.” Pharmacy trusteeship refers to a model in which hospitals, through contractual agreements, entrust the management of their pharmacies to pharmaceutical distribution enterprises, while retaining ownership of the pharmacy assets. From a commercial perspective, hospitals should pay management fees to the enterprises for operating the pharmacies; however, in practice, the winning bidders are required to pay contracting fees to the hospitals.

In such circumstances, pharmaceutical companies and hospitals have formed new interest-based relationships: pharmaceutical companies gain access to the drug distribution market, while hospitals shift cost pressures and reap benefits. Moreover, since agreements between hospitals and pharmaceutical companies are predominantly exclusive in nature, they effectively result in unfair competition within the pharmaceutical market.

This situation has also drawn the attention of relevant authorities. On July 21, the Guangdong Provincial Development and Reform Commission organized public consultations and seminars involving university scholars, public medical institutions, and pharmaceutical companies, and drafted the “Anti-Monopoly Enforcement Guidelines for Pharmacy Trusteeship.” The Guangdong Provincial Price Supervision Bureau stated that the formulation and issuance of these guidelines by anti-monopoly enforcement agencies aim to clarify enforcement principles and approaches to all parties involved, require them to foster a sense of fair competition, and ensure the healthy and orderly development of the province’s pharmaceutical industry.

It is worth noting that the adjustment of medical service prices following the elimination of drug markups has varying impacts on patients with different needs. Under current price adjustment principles, the increased costs are attributed to healthcare professionals’ services, while expenses for drugs and diagnostic tests have been reduced. This may alleviate the financial burden for patients requiring long-term medication, but could increase the burden for those primarily needing medical services. Meanwhile, hospitals might encourage longer hospital stays or provide additional services to increase patient expenditures, thereby compensating for the losses from the removal of drug markups. This could lead to issues such as “offsetting medical costs through excessive testing” or overtreatment.

No reform can accommodate the interests of all parties; the advancement of reform is, in essence, a process of interest-based bargaining among various stakeholders.

The Post-"Zero Markup" Era Has Arrived

We can crunch the numbers to clarify the impact of abolishing drug markups on the revenue of public hospitals. Assuming an average drug-to-revenue ratio of 45% for public hospitals, eliminating a 15% drug markup would directly reduce revenue by 6.7%. For most public hospitals, this amounts to millions of yuan, significantly affecting their compensation levels.

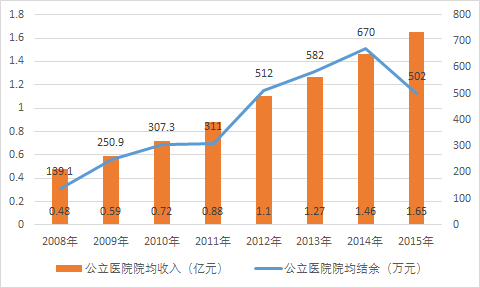

Data Source: Medical World Think Tank

The above data show that the average revenue per public hospital maintained continuous growth from 2008 to 2015, but the growth rate declined after 2012, being more significantly affected by the zero-markup policy. In terms of surplus, the average surplus per public hospital also increased year-on-year from 2008 to 2015, but reached a turning point in 2015, marking the first decline in eight years. This also signifies the formal entry into the post-"zero-markup" era.

The zero-markup policy was introduced against the backdrop of persistently high drug prices, the continuous growth in drug utilization by healthcare institutions, and the urgent need to dismantle the “drug-revenue-dependent” model of hospital financing. Underlying these phenomena are the rising out-of-pocket medical expenses for residents, mounting pressure on medical insurance funds, and the potential for commercial bribery in the pharmaceutical sector inherent in the “drug-revenue-dependent” model.

Regulators have pinned their hopes on the elimination of drug markups, with objectives including reducing medical costs, strengthening hospital management of drug utilization, and curbing the growth of healthcare expenditures; standardizing physicians’ practice behaviors, promoting rational drug use, and eliminating excessive prescribing and inappropriate medication practices; emphasizing the public-welfare nature of public healthcare institutions to prevent excessive profit-seeking; and dismantling the “drug-revenue-dependent” model while enhancing the emphasis placed by healthcare institutions on medical technology and service quality.

In the Post-"Zero Markup" Era, How Stakeholders Respond Has Become a Focal Point of Industry Discussion. After the implementation of zero markups, how should hospitals develop? First, they should strengthen communication with government departments and strive to secure reasonable compensation policies. Second, they should reach agreements with drug suppliers to engage in "secondary price negotiations" on drug supply prices, ensuring that drug costs are controlled within a reasonable framework. Third, they should implement refined internal management to mobilize employee enthusiasm and alleviate the pressure of reduced revenue through such meticulous management.

For retail pharmacies, the separation of prescribing and dispensing may bring significant incremental growth through prescription outflow. How to capture this growth may become a key issue for retail pharmacies to consider. However, the zero-markup policy was not implemented abruptly; pharmacies across various regions have accumulated certain experience during its implementation.

Countermeasures include “trading price for volume,” diversifying operations, and providing pharmaceutical care services. Breaking this down, “trading price for volume” refers to aligning retail pharmacy prices with hospital prices—or setting them slightly lower—after the elimination of drug markups in hospitals, thereby driving foot traffic. Once customer flow is secured, pharmacies can further enhance their appeal by expanding product categories and offering non-pharmaceutical goods. Additionally, many prescription drugs that fail to win bids in hospital procurement present a significant opportunity for pharmacies to sell them through the Direct-to-Patient (DTP) model.

One key aspect is the transition from “selling pharmaceuticals” to “providing services.” Retail pharmacies must offer customers more professional and convenient services, including O2O medication delivery, chronic disease management, and health check-ups. Additionally, they can collaborate with internet healthcare platforms to explore remote consultations and electronic prescriptions, thereby further enhancing their capabilities in medical service provision.

Of course, whether it is the zero-markup policy or the separation of prescribing from dispensing, pharmaceutical manufacturers and distributors will inevitably experience growing pains during their transition. Their existing sales channels and profit structures will be significantly impacted, necessitating corresponding adjustments in market strategies. From another perspective, while healthcare reform is underway, pharmaceutical reform is also progressing. The state encourages new drug research and development, establishes green channels for drugs with proven efficacy and urgent clinical needs, continuously accelerates drug registration and approval processes, and gradually aligns regulatory standards with international practices.

In fact, medicine and pharmaceuticals are inextricably linked. While it is essential to recognize the challenges presented by this round of reforms, it is equally important to identify the opportunities within these challenges. The direction of the new healthcare reform is correct; through continuous practical adjustments to its details, it may ultimately provide all stakeholders with a clear implementation plan that safeguards their interests.