US-China GPO Model Benchmarking: With 73% Penetration and Over $300 Billion in Annual Procurement in the US, How Can GPO Succeed in China?

“China’s healthcare reform efforts frequently cite the U.S. model, yet this approach is likely ill-suited to China’s context. Significant differences exist between China and the United States in terms of ownership structures, payment mechanisms, and the degree of marketization. Without addressing these fundamental disparities, blindly adopting the U.S. model will not succeed. Pilot programs for Group Purchasing Organizations (GPOs) can be implemented in conjunction with China’s centralized tendering and volume-based procurement systems, which would help lower drug prices and curb the growth of pharmaceutical expenditures.” This statement was made by an official from the Guangzhou Healthcare Reform Office regarding GPO initiatives at a recent internal seminar.

In July, Guangzhou City and Hubei Province successively expressed their intent to pilot the Group Purchasing Organization (GPO) procurement model in government documents, marking another exploration following the implementation of GPOs in Shanghai and Shenzhen. In the future, GPO procurement may become a significant method for hospital procurement under the framework of centralized bidding and volume-based procurement systems.

However, the implementation of Group Purchasing Organization (GPO) procurement has encountered numerous challenges, with frequent criticisms regarding excessive government intervention, monopolistic practices, and lack of transparency. In the context where the separation of prescribing and dispensing has not been fully realized, hospitals exhibit weak incentives for cost containment, which has also hindered the penetration of GPO procurement models into hospital operations.

Amid pilot initiatives across various regions and active industry discussions, VCBeat (WeChat ID: vcbeat) has reviewed the development models and historical evolution of Group Purchasing Organizations (GPOs) in the United States, compared them with the current state of GPOs in China, and aimed to identify the unresolved challenges hindering the successful implementation of GPOs in the Chinese market.

U.S. GPOs can reduce procurement costs by 10%–15%.

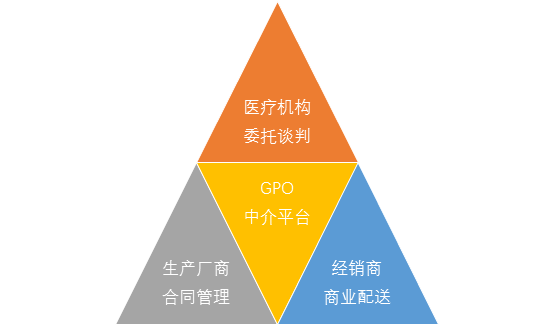

GPO, a buzzword in the pharmaceutical industry in recent years, stands for Group Purchasing Organization, i.e., centralized procurement organization, which originated in the United States.

A Group Purchasing Organization (GPO) is an intermediary entity held by multiple shareholders (GPO members). GPO procurement refers to the centralized purchasing activities conducted by healthcare institutions, with the aim of reducing the purchase prices of products and services such as pharmaceuticals, medical devices, and consumables, or helping member units lower communication costs and improve procurement efficiency.

The business model of Group Purchasing Organizations (GPOs) involves aggregating the demand of healthcare institutions to negotiate with upstream suppliers, thereby reducing procurement prices and transaction costs, while charging suppliers contract administration fees. The rationale for GPOs lies in the cost-containment needs of payers and healthcare providers, who seek to lower procurement expenses through centralized purchasing. In terms of cost-control mechanisms, GPOs primarily consolidate the demand of healthcare institutions to exert pressure on suppliers, securing cost concessions. Generally, the contract administration fees charged by GPOs to manufacturers account for approximately 1%–3% of the total contract value. To increase revenue, GPOs can expand their membership base or scale up procurement volumes to secure higher fee percentages.

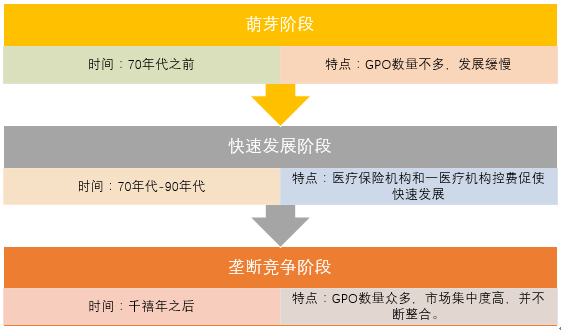

The earliest Group Purchasing Organization (GPO) in the United States emerged in the early 20th century. The New York Hospital Council was established in 1910, with its primary purpose being to unite hospitals for negotiating prices of laundry services with upstream providers, thus embodying the rudimentary form of a GPO.

However, GPOs in the United States saw little significant growth until the 1970s. This was because the prevailing healthcare payment model at the time was Fee-for-Service (FFS), which resulted in limited pressure on healthcare institutions to control costs, thereby leaving little room for GPOs to exert influence. By 1962, there were only 10 GPO organizations nationwide.

The development of GPOs is closely tied to the shift in healthcare payers in the United States. Since the 1970s, commercial health insurance has emerged as a major payer, and insurers have faced significant pressure to control costs amid rising healthcare expenditures.

In 1977, Medicare, the largest public health insurance program in the United States, transitioned from a fee-for-service model to a prospective payment system (PPS), thereby unleashing the demand for cost containment among healthcare institutions. Driven by these converging factors, group purchasing organizations (GPOs) rapidly expanded; at that time, more than 40 GPOs primarily provided centralized procurement services for Medicare.

By 1983, the Medicare prospective payment system had been further tightened. In addition, in 1986, the U.S. Congress included the practice of Group Purchasing Organizations (GPOs) collecting administrative fees from vendors within the “safe harbor” exemptions of the Federal Anti-Kickback Statute, thereby granting legal recognition to GPO fee structures. As a result, GPOs experienced explosive growth during the 1980s and 1990s, with the number of GPO organizations exceeding 200.

By the end of 2013, there were more than 600 active Group Purchasing Organizations (GPOs) in the United States, including 30 large national GPOs. Nationwide, 96% of acute care hospitals, 98% of community hospitals, and 97% of non-governmental, non-profit hospitals had joined at least one GPO, with approximately 73% of all U.S. hospitals procuring supplies through GPOs.

U.S. GPOs are characterized by two key features: high market concentration and large procurement scale. The top nine GPOs collectively account for over 73% of the market share. Vizient, the largest GPO, has an annual procurement volume of $100 billion and a market share of approximately 33%. Premier, the second-largest GPO, is listed on the NASDAQ with an annual procurement volume of $50 billion and a market share of around 16%. According to estimates by the Healthcare Supply Chain Association (HSCA), the penetration rate of GPOs in U.S. hospital procurement reached 73%, with total procurement amounting to $306.2 billion in 2016.

In terms of cost-control effectiveness, U.S. Group Purchasing Organizations (GPOs) can help healthcare institutions reduce costs by 10%–18%. Based on an annual total procurement volume of approximately $300 billion, the savings generated for the entire U.S. healthcare system are estimated to range from $30 billion to $70 billion.

Only Shanghai and Shenzhen in China have implemented GPO.

In China, following the implementation of the “New Healthcare Reform,” the separation of pharmaceuticals from medical services has been steadily advanced. Drugs have gradually shifted from being a source of revenue for hospitals to becoming a cost center. Domestic healthcare institutions are also exploring diverse cost-containment strategies, with Group Purchasing Organizations (GPOs) being one of their chosen approaches.

Currently, only Shanghai and Shenzhen have implemented Group Purchasing Organizations (GPOs) in China. Additionally, cities and regions such as Guangzhou, Hubei Province, and Chongqing have expressed interest in adopting GPOs; however, no concrete plans have been established, and they have not yet entered the substantive implementation phase. The following section provides a detailed overview of the GPO implementation in Shanghai and Shenzhen.

Shanghai was the first region in China to pilot Group Purchasing Organization (GPO) initiatives. In December 2015, it convened a coordination meeting on pharmaceutical group purchasing to discuss policy requirements and operational workflows, and engaged in communications with supply enterprises.

On February 29, 2016, Shanghai’s “Five Hospitals and Six Districts” established a Group Purchasing Organization (GPO) Alliance for pharmaceuticals in public medical institutions, entrusting the Shanghai Yijian Health Affairs Center with its administration. The Shanghai Yijian Health Affairs Service Center is funded by the Shanghai Medical and Health Development Foundation, which is supervised by the Shanghai Municipal Health and Family Planning Commission. This structure imbued Shanghai’s GPO with a strong official character from its inception.

In terms of implementation results, as of April this year, the Medical and Health Center has led the first round of group procurement for five batches of drugs. In May this year, Fudan University Shanghai Cancer Center joined the procurement alliance, expanding the Shanghai GPO from “five hospitals and six campuses” to “six hospitals and six campuses.”

Following Shanghai, the Shenzhen Municipal Health and Family Planning Commission issued three documents in August last year, providing detailed specifications for Group Purchasing Organizations (GPOs). These requirements mandated that GPOs possess relevant pharmaceutical operation licenses, supply capabilities, and settlement platforms, and be selected through a public tendering process.

According to the selection principles of the Shenzhen Municipal Health and Family Planning Commission, during the pilot period, the total cost of drugs under centralized procurement by the Group Purchasing Organization (GPO) must be reduced by more than 30% compared with the 2015 Guangdong Provincial Drug Electronic Trading Platform. By 2017, the proportion of drug revenue to total business revenue in public hospitals across the city shall decrease by more than 25%, thereby curbing the rise in drug costs.

On August 3, the Shenzhen Municipal Health and Family Planning Commission announced the selection results, with QuanYaoWang, a subsidiary of Neptunus Group, winning the bid. On September 25, QuanYaoWang, acting as the drug group purchasing organization for Shenzhen’s public hospitals, signed entrusted supply agreements separately with the first batch of reform pilot hospitals under municipal and district-level administration. The number of hospitals participating in this initial phase reached 25.

On April 7 this year, the National Development and Reform Commission (NDRC) issued a statement announcing that, in response to reports from enterprises and industry associations, it had jointly investigated with the Guangdong Provincial Development and Reform Commission the Shenzhen Municipal Health and Family Planning Commission for suspected abuse of administrative power to eliminate or restrict competition during the implementation of pilot group purchasing programs for pharmaceuticals in public hospitals. The investigation confirmed that the Shenzhen Municipal Health and Family Planning Commission had violated the Anti-Monopoly Law, including:

I. Only one group purchasing organization (selected as Quanyaowang Pharmaceutical) is permitted to provide pharmaceutical group purchasing services; II. Public hospitals in Shenzhen and pharmaceutical manufacturers are restricted to using the services provided by Quanyaowang Pharmaceutical; III. Pharmaceutical distribution enterprises are designated exclusively by Quanyaowang.

The Shenzhen Municipal Health and Family Planning Commission stated that it would implement three rectification measures, including ensuring the autonomy of public hospitals in drug procurement, ensuring the autonomy of drug distribution enterprises, and ensuring the autonomy of drug manufacturers.

The National Development and Reform Commission (NDRC) also stated that the experience of mature market economies has demonstrated that group purchasing models for pharmaceuticals can effectively reduce drug procurement prices, save on healthcare expenditures, and alleviate the financial burden on patients. Fair competition among pharmaceutical group purchasing organizations is one of the keys to achieving these objectives.

As of now, the group purchasing business of Quanyaowang is still in operation, and the proposed transaction results for the second batch have been announced.

In addition, Guangzhou’s new round of “healthcare reform” was launched on July 15. In terms of drug procurement, Guangzhou may also establish a Group Purchasing Organization (GPO) platform to continue deepening its exploration of the “volume-based procurement” model.

Differences Between Chinese and U.S. GPOs Lie in Healthcare Systems and Implementing Entities

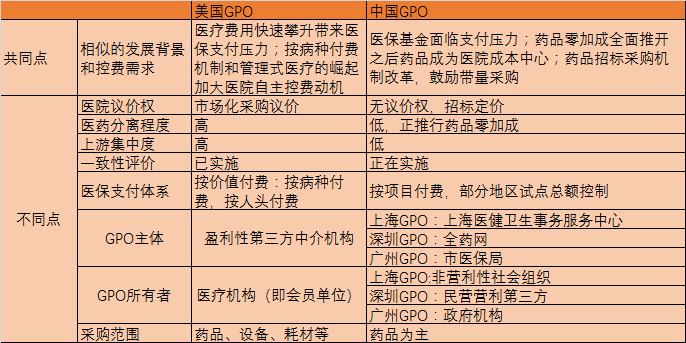

The development of Group Purchasing Organizations (GPOs) in the United States has a century-long history, with a relatively mature market experience. It serves as an important reference for China’s GPO development. However, while learning from the U.S. experience, it is essential to understand not only the practices but also the underlying rationale by identifying the similarities and differences between the two contexts.

Source: Orient Securities’ In-Depth Report on the Biopharmaceutical Industry

In terms of similarities, both Chinese and US Group Purchasing Organizations (GPOs) are products of the need for cost containment. Since the 1970s in the United States, rapidly rising healthcare costs have exerted pressure on medical insurance payments; meanwhile, the implementation of diagnosis-related group (DRG) payment mechanisms and the rise of managed care have strengthened hospitals’ incentives to control costs independently, thereby facilitating the rapid development of GPOs. In China, similar pressures exist regarding medical insurance payments. Furthermore, following the comprehensive implementation of the zero-markup policy for pharmaceuticals, drugs have shifted from being a source of revenue for hospitals to a cost center, thus driving hospitals’ demand for cost containment.

However, there are fundamental differences between the healthcare systems of China and the United States, such as hospital ownership, health insurance systems, and payment methods. Therefore, the implementation of Group Purchasing Organizations (GPOs) in China must be aligned with national conditions.

U.S. Group Purchasing Organizations (GPOs) are initiated by hospitals, which, as owners and managers of the GPOs, ensure alignment between the GPOs’ interests and those of the hospitals. In contrast, China’s GPOs have diverse initiators and managers, with few being hospital-initiated. Based on implemented cases, the Shanghai GPO is a non-profit organization under the guidance of the Shanghai Healthcare Reform Office; the Shenzhen GPO is a socially operated pharmaceutical enterprise selected through a competitive process; and the Guangzhou GPO is directly administered by the Municipal Healthcare Security Administration.

It can be said that the U.S. GPO market is more market-oriented, whereas Chinese GPOs rely to some extent on government agencies.

Furthermore, the rise of Group Purchasing Organizations (GPOs) in the United States was driven by the need to control costs for social insurance institutions and healthcare providers. In contrast, the primary motivation for GPOs in China is to control expenditures within the national medical insurance fund, with participation from medical insurance administrative authorities. Due to this distinction, Chinese GPOs are highly prone to adopting a “lowest-price-only” procurement strategy during operations. For instance, Quanyao Network has pledged a 30% reduction in overall procurement costs, a figure that exceeds the 10%–18% average achieved by mature U.S. GPOs. Consequently, the implementation process will inevitably favor low-priced suppliers.

Medical institutions in the United States that participate in Group Purchasing Organizations (GPOs) possess greater autonomy, enabling them to freely decide whether to join or withdraw from a GPO. In contrast, the procurement authority of hospitals in China is constrained by the bidding system. To date, volume-based procurement and government-led GPOs lack effective price negotiation capabilities, resulting in insufficient awareness and initiative among hospitals regarding participation.

Where Are China's GPOs Headed?

In summary, GPOs bear a strong resemblance to volume-based procurement (VBP), but place greater emphasis on third-party involvement and market-oriented mechanisms. The VBP model, characterized by "volume-based procurement with linked price and quantity," integrates the interplay among supply, demand, and pricing. For hospitals, it ensures drug supply and reduces drug prices; for pharmaceutical distributors, it lowers marketing and administrative costs. When properly implemented, this approach yields benefits for all stakeholders.

Prior to the adoption of the Group Purchasing Organization (GPO) model, China had a long history of implementing “volume-based procurement.” The earliest initiative originated in Shanghai’s Minhang District with the “one product, one specification, one distributor” policy, aimed at curbing medical corruption through centralized procurement. Subsequently, in 2014, Anhui Province introduced its own volume-based procurement policy, conducted at the municipal level, which established a province-wide “16+1” procurement model. By leveraging purchase volumes to negotiate lower prices, hospitals retained a margin equivalent to 15% below the medical insurance reimbursement price, thereby offsetting the revenue loss from the zero-markup policy on drug sales.

Currently, volume-based procurement is part of the pharmaceutical tendering system, with the tendering offices led by local Health and Family Planning Commissions serving as the leading authorities. However, in some regions, volume-based procurement has come under the leadership of healthcare security administration departments. For instance, Shanghai’s volume-based procurement is spearheaded by its Healthcare Security Bureau, while the competent authority for tendering and procurement in Sanming City, Fujian Province (now known as the “Sanming Alliance”) is the Sanming Healthcare Security Fund Management Center. These developments indicate that the volume-based procurement model is undergoing certain transformations within the broader tendering framework.

Since the advent of the GPO model, it has faced significant scrutiny. For instance, the Shanghai GPO has been criticized for irregularities such as an unclear quantitative evaluation system in the bidding process, a number of winning bidders exceeding the limits set by original rules, and certain enterprises being granted privileged access to secondary price negotiations.

The Shanghai Medical and Health Center stated that it is positioned as a “third-party organization,” with the government responsible for formulating relevant policies and the Center tasked with their concrete implementation. While challenges in communication with enterprises may arise during implementation, the process is expected to become smoother as systematic experience is accumulated. The aforementioned commitment by the Shenzhen Municipal Health and Family Planning Commission also indicates that, during the implementation of Group Purchasing Organizations (GPOs), transparency and openness of information, autonomy of all participating parties, and full competition should be ensured.

It is also worth noting that the long-established pharmaceutical sales landscape in China has ingrained a reliance on drug sales revenue within hospitals. Even after the implementation of the zero-markup policy, hospitals continue to benefit through gray-area practices such as rebates from pharmaceutical companies, thereby fostering a preference for high-priced drugs—a trend that contradicts the principles of Group Purchasing Organizations (GPOs). However, entrusting or transferring procurement authority to third parties may help curb the phenomenon of “funding healthcare with drug profits.”

However, cost containment, drug price reduction, and curbing the growth of healthcare expenditures constitute critical “political” mandates for the entire healthcare system. Under the leadership of relevant authorities, various initiatives—including Group Purchasing Organizations (GPOs)—are being piloted. GPOs are likely to be expanded to more regions in the future and may eventually form a nationwide network.

Once Group Purchasing Organizations (GPOs) achieve scale, they may fundamentally impact the marketing practices of pharmaceutical manufacturers, leading to changes in their promotional and lobbying activities. The comprehensive evaluation based on volume-price linkage and quality prioritization also incentivizes pharmaceutical companies to focus on improving product quality. From the perspective of pharmaceutical distributors, GPOs are driving further consolidation among distribution enterprises, potentially promoting mergers and acquisitions within the industry.