Capital Gates Open: Who Will Be the Next IPO in China's Billion-Dollar NGS Market?

With the successive listings of BGI Genomics and Berry Oncology, the door to public offerings for China’s NGS industry has officially opened.

Not only that, but NGS-related stocks in the capital market also rose during this period. Rongzhi Lian hit its daily upper limit on the day BGI Genomics went public, while stocks of Zhongyuan Union and Daan Gene also saw significant gains. If 2014 was the inaugural year for the large-scale adoption of genetic testing, then 2017 was undoubtedly the inaugural year for the capitalization of sequencing companies.

So, after the capital market has opened its arms to the NGS industry, who will be the next to go public? VCBeat (WeChat ID: vcbeat) has conducted a brief analysis on this.

Secondary Market: Inverted Triangle Layout

First, VCBeat has mapped out the industry layouts of secondary-market NGS companies and related concept stocks.

As shown in the industry landscape, secondary market companies’ layout in this field presents an inverted triangle shape, with the upstream market being the key segment.

Among them, a total of four companies have established operations in the production of sequencing instruments.

After acquiring Complete Genomics (CG), BGI Group introduced the BGISEQ platform following technological improvements; DAAN Gene and Berry Genomics launched sequencing platforms in partnership with Thermo Fisher Scientific and Illumina, respectively; while Xinjiang Zixin Pharmaceutical partnered with the Chinese Academy of Sciences to release a domestically produced sequencer.

Even in the secondary market, the sequencing instrument segment remains a high ground for the industry.

In the secondary market, BGI Genomics and Berry Genomics are fully-fledged NGS companies and were the first two in the industry to go public. Currently, they remain the only two companies in the sector that have established a comprehensive industrial layout covering the upstream, midstream, and downstream segments.

Other concept stocks have entered certain segments of the industry through business expansion or investment.

Among them, Hongchang Technology has gained prominence in the medical device sector by undertaking contract manufacturing services for gene storage boards (DNA chips). The company’s gene storage product line has obtained U.S. FDA clearance and become a supplier to Thermo Fisher Scientific, integrating it into the global mainstream supply chain of the gene sequencing industry.

Da An Gene focuses on market commercialization, with significant investments in non-invasive prenatal testing (NIPT) and the consumer market. Zhongyuan Union Cell & Gene Engineering Corp. invests in Panacea Biotech and iCarbonX to target the oncology and consumer markets.

In addition to its comprehensive industry-wide layout, another strategy in the secondary market is to focus on commercialization.

Primary Market: Crowding into the Midstream Segment

Corporate layouts in the primary market differ significantly from those in the secondary market, with most companies concentrated in the midstream segment, while upstream and downstream segments have relatively lower company density. There are four companies involved in the sequencing instrument market: CapitalBio Technology, Annoroad Gene Technology, HybriTech, and Hanhai Genomics. Among them, Hanhai Genomics launched a single-molecule sequencer this year, which belongs to third-generation sequencing technology; this will not be discussed here for now.

Unlike the secondary market, which spans multiple industries, companies in the primary market often focus exclusively on a single sector. Fully immersed in their respective industries, these enterprises have a deeper understanding of industry-specific pain points. Consequently, primary market players demonstrate greater focus and specialization in their industry positioning compared to those in the secondary market.

Consequently, 38 companies have established positions in the primary market targeting downstream segments that are largely neglected in the secondary market, including a number of specialized firms.

We have decided to adopt a secondary-market investment strategy as a reference point to identify potential IPO candidates from the primary market and analyze their near-term listing prospects. Given the difficulty in obtaining financial data for private companies, we assess their likelihood of going public based on financing activities and corporate valuations.

In the primary market, three companies have followed a similar path to BGI Genomics and Berry Genomics by completing full industry chain layouts: CapitalBio Corporation, HybriGene, and Annoroad Gene Technology.

CapitalBio Corporation was established in 2000, founded in collaboration with Tsinghua University, Huazhong University of Science and Technology, the Chinese Academy of Medical Sciences, and the Academy of Military Medical Sciences, with a registered capital of RMB 376.5 million.

As of 2016, CapitalBio had rapidly evolved into a group-based operational structure encompassing five research institutes (Institute of Health Sciences, Institute of Translational Medicine, Institute of Engineering Translation, Institute of Translational Bioinformatics, and Institute of Health Technology) and five subsidiaries (CapitalBio Jingdian, CapitalBio Medicine, CapitalBio Yihe, CapitalBio Muhua, and CapitalBio Xinjing).

Although not yet publicly listed, this Tsinghua Holdings-affiliated company has consistently remained a leader in the industry.

BioCapital has been legally incorporated and in continuous operation for more than three years, with no material changes in its business operations, thus complying with these regulations. Its controlling shareholder is Tsinghua Holdings Co., Ltd., which holds a 69.32% equity stake in the company. Therefore, Tsinghua Holdings is the actual controlling legal entity of the company, and there have been no material changes in the actual controller in recent years.

In 2010, CapitalBio Corporation underwent a change in its shareholding structure, which was widely interpreted by external observers as a move to prepare for an initial public offering (IPO); however, the company ultimately did not pursue this path.

According to some sources, CapitalBio Technology initially targeted an IPO on the U.S. NASDAQ, but the plan was rejected years ago due to the involvement of the Academy of Military Sciences among its major shareholders. The company later planned to list domestically, but the listing proposal was again rejected due to internal equity issues.

Ultimately, the company was split into five entities, with each subsidiary conducting separate financing rounds, thereby circumventing the impact of property rights issues on its initial public offering (IPO). It is understood that these five companies have secured Series A or Series B financing to varying degrees. This suggests that BioCapital is most likely pursuing a spin-off IPO strategy.

Founded in 2008, Huayinkang has established the Shenzhen Huayinkang High-Throughput Biotechnology Research Institute, Shenzhen Huayinkang Gene Technology Co., Ltd., the Huayinkang Genetic Testing Center, and numerous branch offices across China. It has grown into a high-tech biotechnology group centered on genetic technology, featuring an integrated industry chain that encompasses research and development, production, and application.

It is worth noting that this is one of the few domestic manufacturers of sequencing instruments in China.

In May 2015, Huayinkang underwent a joint-stock reform: all of the 95.2740% equity interest held by Sheng Sitong was transferred to Guangzhou Kangxinrui Gene Health Technology Co., Ltd. Following the reform, Kangxinrui’s shareholding ratio stood at 96.2640%. However, as Sheng Sitong held a 73.3959% stake in Kangxinrui and was its actual controller, the actual controller of Huayinkang remained unchanged after this joint-stock reform.

Huayinkang secured three rounds of financing in 2011 and 2015, with only the Series B round in September 2011 disclosing specific amounts. Assuming the “tens of millions” to be RMB 30 million, Huayinkang’s total financing amounted to approximately RMB 70 million. Based on a 15% equity stake sold, Huayinkang’s valuation was approximately RMB 467 million.

However, VCBeat published last year“Future Healthcare Top 100”Prior to the ranking’s release, Huayinkang confirmed that the company’s valuation had already exceeded RMB 2 billion.

Annuoda Gene Technology, established in 2012, specializes in the industrial application of next-generation sequencing technology in the fields of human medical health and life sciences research.

In March 2017, Annoroad Gene Technology announced the official launch of the NextSeq 550AR, a desktop high-throughput sequencer certified by the China Food and Drug Administration (CFDA). Simultaneously, it released a certified kit for the detection of fetal chromosomal aneuploidies (T21, T18, and T13) based on the NextSeq 550AR sequencing platform. This marked the company’s completion of its full industrial layout.

In November 2015, the company’s largest shareholder, Chuanshi Aomei Gene Technology (Beijing) Co., Ltd., saw its shareholding decrease from 31.4% to 0%, while the new shareholder, Ningbo Meishan Bonded Port Area Shifeng Huafu Investment Management Partnership (Limited Partnership), acquired a 26.4% stake, becoming the largest shareholder.

However, as the actual controller of both companies is Chen Chongjian, the actual controller of Annoroad Gene Technology has not changed.

According to public records, Annoroad has completed three rounds of financing to date, although the specific amounts for these rounds were not disclosed. Verified by VCBeat, Annoroad’s latest valuation is now approaching RMB 4 billion.

Another path in the secondary market is commercialization layout, which refers to the midstream segment oriented toward the market end. In the primary market, many companies follow this route.

By compiling publicly available data, we have selected the ten companies with the highest financing amounts: Novogene, Burning Rock Biotech, New Horizon Health, Genetron Health, Shanghai Cellular Group, Koonen Genetics, SeqHealth Medical, 3D Medicines, Biomarker Technologies, and Genetron Health.

Among these companies, six—Genetron Health, Kunyuan Gene, Xukang Medical, New Horizon Health, 3D Medicines, and Burning Rock Biotech—have been established for less than three years or exactly three years, making their likelihood of an initial public offering (IPO) relatively low.

After this screening process, the remaining companies are Novogene, Biomarker Technologies, Shanghai Cell Therapy Group, and Genetron Health.

Novogene

Novogene was established in 2011, focusing on pioneering the application of cutting-edge molecular biology technologies and high-performance computing in the fields of life sciences and human health. Headquartered in Beijing, the company operates laboratories or experimental bases in Tianjin, Nanjing, the United States, and Singapore, and has subsidiaries in Hong Kong, the United States, and the United Kingdom.

In 2014, Novogene underwent an equity change: Li Ruiqiang’s shareholding decreased from the original 96.5% to 71%, while a new shareholder, Zhiyuan Hegu, held a 24% stake. Following the change, Li Ruiqiang remained the largest shareholder, so the actual controller did not change.

Novogene secured RMB 200 million in Series A financing from SDIC Innovation in 2015. The following year, Novogene raised another RMB 500 million in its Series B round. Based on a 15% equity stake sold, Novogene’s valuation was approximately RMB 47 billion, approaching that of publicly listed companies.

In November 2016, Huang Helong, Assistant to the President of Novogene, revealed the company’s intention to pursue an initial public offering (IPO). In fact, as early as July 2016, Novogene had converted from a limited liability company to a joint-stock limited company, a mandatory step prior to going public.

It can thus be inferred that Novogene is highly likely to become the next company to go public.

Biomarker Technologies was founded in 2009. Leveraging the development and application of high-throughput sequencing and bioinformatics technologies, the company focuses on core businesses including scientific services, medical genetic testing, and biological cloud platforms. It primarily serves domestic and international research institutions, universities, independent laboratories, pharmaceutical companies, healthcare organizations, corporate clients, and individual consumers.

Biomarker Technologies completed its Series A and Series B financing rounds in 2014 and 2015, respectively. The Series B round raised RMB 100 million, while the specific amount for the Series A round was not disclosed. Based on previous valuation methods, Biomarker Technologies was valued at approximately RMB 867 million.

Shanghai Cell Group

Shanghai Cell Group, established in 2013, is a municipal-level engineering technology research center approved by the Shanghai Municipal Science and Technology Commission. The center comprises the Shanghai Institute of Cell Therapy, the Cell Therapy Production Center, the Cell Storage Bank, the Shanghai Wu Mengchao Oncology Medical Center, Shanghai Baize Medical Laboratory, Shanghai Baize Cell Medical Aesthetics Center, and Shanghai Baize Medical Devices Co., Ltd. Its business scope covers cell therapy, cell cryopreservation, genetic testing, and medical big data, with the aim of building an internationally renowned cell therapy center that integrates production, treatment, and R&D, ranking among the top in China and leading globally.

In April 2016, Yaoji Poker, an investor in Shanghai Cell Therapy Group, issued a capital increase report announcing a joint investment of RMB 185 million in the company together with Legend Capital.

Pursuant to the capital increase agreement, the pre-money valuation of Cell Group was RMB 650 million. Following this capital increase, Legend Capital and the Company invested a total of RMB 185 million, with Legend Capital contributing RMB 160 million and the Company contributing RMB 25 million. The post-money valuation of Cell Group amounted to RMB 835 million.

Additionally, according to the company’s annual report, the total operating revenue in 2014 was RMB 8.0355544 million, with a net profit of -RMB 8.6612443 million.

In 2015, the company's total operating revenue was RMB 13.48349023 million, representing an increase of approximately 67% compared to 2014; however, the net profit for that year was not disclosed.

Founded in 2013, Genetron Health is dedicated to the effective application of genomics across all aspects of cancer diagnosis and treatment. By collaborating with medical and research institutions, it provides reliable molecular diagnostic and therapeutic solutions, as well as professional cancer genetic risk assessments, for cancer patients, individuals at high risk for cancer, and the general healthy population.

The Company has established dual R&D centers in North Carolina, USA, and Beijing, China, and set up clinical medical testing centers in Beijing, Shanghai, Hangzhou, and Chongqing.

In 2014, Genetron Health secured Series A financing from CDH Investments, amounting to tens of millions of RMB; in 2016, the company raised RMB 100 million in Series B financing from Vcanbio.

According to the announcement at that time, Vcanbio Capitalized on Genetron Health with RMB 100 million to hold a 10% equity interest in the target company; meanwhile, after increasing its capital contribution to the target company, the Company decided to acquire a 5% equity interest in the target company held by Beijing Jinchuang Junlian Investment Management Center (Limited Partnership) for RMB 23 million. Following the capital increase and equity acquisition, the Company held a 15% equity interest in the target company.

Based on this calculation, Fan Shengzi’s valuation exceeds RMB 1 billion. For a startup, this is an outstanding achievement.

According to the National Enterprise Credit Information Publicity System, Genetron Health incurred a loss of RMB 3.59 million in 2014. Although the company has likely gradually achieved profitability as product commercialization has been realized, it is unlikely to pursue an initial public offering (IPO) in the near term.

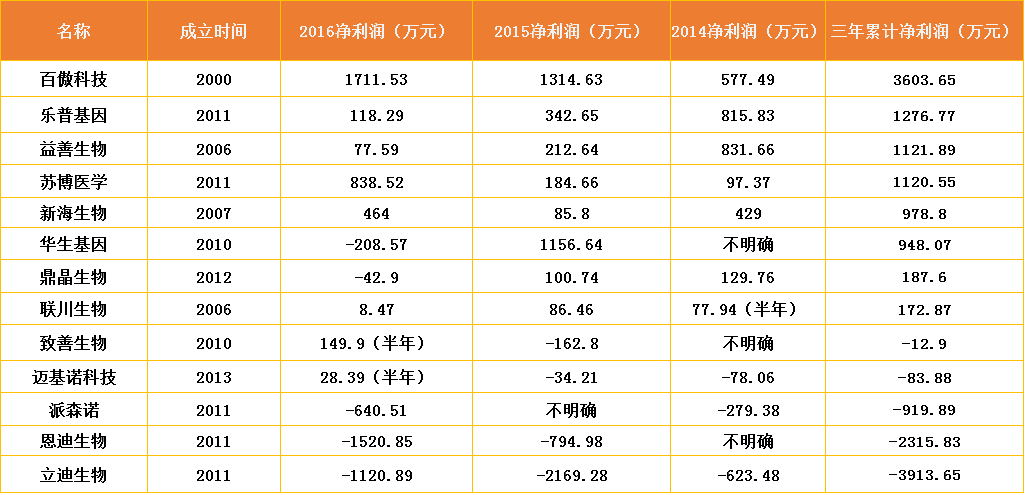

Currently, we have identified 13 companies in the industry listed on the National Equities Exchange and Quotations (NEEQ).

Based on the net profits of the past three years, four companies meeting the basic criteria were ultimately selected: Bio-Venture Technology, E-Sun Biotech, Subo Medical, and Lepu Gene.

Baiao Technology, established in 2000, is a high-tech enterprise specializing in the development, manufacturing, and sales of personalized medicine genetic diagnostic products and related accessories. In 2005, the company obtained the first CFDA registration approval for a personalized medicine genetic testing product in China.

Leveraging its “colorimetric chip technology,” the company has developed a series of test kits and chip-based products, four of which have obtained Class III in vitro diagnostic (IVD) registration certification from the China Food and Drug Administration (CFDA). To date, Bio-Technology’s products have been adopted by 300 large and medium-sized general hospitals across China.

The Company’s net profits for 2014, 2015, and 2016 were RMB 36.0365 million, respectively; meanwhile, there was no change in the actual controller during these three years, thereby meeting the basic listing requirements for the ChiNext Board.

According to data retrieved from the National Equities Exchange and Quotations (NEEQ), Baiao Technology has a total share capital of 63.4325 million shares, with a current market capitalization of RMB 565 million. Although it meets the basic listing requirements for the ChiNext Board, its market capitalization is relatively low compared to companies already trading on the secondary market.

Yishan Biotech is an emerging leader in China’s liquid biopsy sector. Its independently developed CanPatrol CTC detection platform overcomes the biomarker limitations of first-generation CTC technologies and is broadly applicable to most cancer types. The related research was published in the internationally renowned journal PLOS ONE.

Established in 2006, this national high-tech enterprise specializes in the research, development, and manufacturing of real-time personalized medical products for oncology. The company has independently undertaken multiple major scientific and industrialization projects, including personalized medicine initiatives under the National Major Science and Technology Special Projects during the 12th Five-Year Plan period, pioneering the field of personalized medicine in China. Committed to becoming a leading enterprise in personalized healthcare, the company focuses on real-time diagnostic products and services for individualized cancer treatment. Currently, it operates four medical laboratories and plans to establish a nationwide product sales network within three years.

Yishan Biotech’s net profits for the three years from 2014 to 2016 were RMB 775,900, RMB 2.1264 million, and RMB 8.316 million, respectively, totaling over RMB 10 million. During this period, there were no significant changes in the company’s actual controller. With a total share capital of 69 million shares, the company meets the basic listing requirements. Currently, the company’s market capitalization is approximately RMB 637 million, which remains relatively low compared to secondary market valuations.

In addition, the company was urgently suspended from trading in February 2017 due to violations of relevant regulations, including the Regulations on the Supervision and Administration of Medical Devices and the Measures for the Supervision and Administration of Medical Device Operations. Given the impact of this incident on the company, the likelihood of Yishan Biology going public in the near future appears to be low.

Subo Medicine, established in 2011, is a specialized and cutting-edge institution dedicated to research and testing services in the gene sequencing industry. Holding a medical institution practice license, the company had, as of August 2016, extended its service network to cover 28 provincial-level administrative regions, 228 prefecture-level cities, and 987 counties and districts across China, with 289 partner institutions.

The company’s net profits for the three years from 2014 to 2016 were RMB 8.3852 million, RMB 1.8466 million, and RMB 973,700, respectively, with a cumulative total exceeding RMB 10 million.

According to the company's 2016 public transfer prospectus, its controlling shareholder is Nanjing Zigong. Nanjing Zigong currently holds 7.645 million shares of the company, accounting for 62.55% of the total share capital. As its shareholding ratio exceeds 50% of the company's total share capital, Nanjing Zigong is the company's controlling shareholder.

The company’s controlling shareholder is Nanjing Zigong. Currently, Shi Qi, Feng He, and Wu Lijian hold 30%, 40%, and 30% of the shares in Nanjing Zigong, respectively. Wu Lijian and Shi Qi are mother and son; together, they hold a 60% equity interest in Nanjing Zigong, while Feng He holds a 40% equity interest.

In addition, Shi Qi’s wife, Xie Haiming, directly holds an 8.64% stake in Subo Medicine, while Feng He directly holds a 5.76% stake. Shi Qi controls a 9% stake in Subo Medicine through Suqian Ziyou. Shi Qi, Wu Lijian, and Feng He indirectly control Subo Medicine through Nanjing Zigong.

At the time of the company’s establishment, Shi Qi and Feng He, for personal reasons and to facilitate operational convenience, entrusted Wu Lijian to hold their equity interests in Subo Medicine on their behalf. Wu Lijian, Shi Qi and his mother, and Feng He agreed on an equity holding ratio of 6:4. Subsequently, Wu Lijian restored the actual equity structure of Subo Limited by transferring his equity interests therein to Nanjing Zigong, Xie Haiming, and Feng He.

Therefore, during the reporting period, the company’s actual controllers remained Shi Qi, Wu Lijian, and Feng He, with no changes occurring. Subo Medicine’s total issued share capital amounts to 30.5556 million shares, meeting the basic listing requirements for the ChiNext board.

Data from the New Third Board shows that the company’s current market capitalization stands at RMB 800 million. Although this valuation is relatively low compared with NGS stocks and concept stocks, it is already comparable to that of companies in certain other industries.

Lepu Genetics is a platform centered on cardiovascular molecular diagnostics and high-throughput gene sequencing, primarily providing molecular diagnostic reagents and testing services. Leveraging next-generation sequencing (NGS) platforms, the company has established product lines for cardiovascular high-throughput sequencing, non-invasive prenatal screening, and tumor gene sequencing services. It has currently formed three major business segments: third-party basic medical laboratory testing services, high-throughput sequencing services, and the research, development, and sales of cardiovascular molecular diagnostic reagents.

The company's net profits for the three years from 2014 to 2016 were RMB 8.1583 million, RMB 3.4265 million, and RMB 1.1829 million, respectively.RMB 10,000, with a cumulative total exceeding RMB 10 million.

Lepu Gene's controlling shareholder, Lejian Medical, is a subsidiary of Lepu Medical. Lepu Medical holds a 60% stake in Lejian Medical, and Lejian Medical holds a 90% stake in Lepu Gene.

Lepu Gene is a subsidiary indirectly controlled by Lepu Medical, and both entities are under the control of the same party. The actual controller of Lepu Medical is Pu Zhongjie. Therefore, the actual controller of Lepu Gene is Pu Zhongjie.

Lepu Medical issued the “Announcement on Adjustments to the Shareholding of Its Actual Controller” in June 2017; however, this adjustment did not constitute a significant change in Lepu Medical’s actual controller. In other words, there was no change in the actual controller of Lepu Gene.

Meanwhile, Lepu Gene currently has a total issued share capital of 52 million shares, meeting the basic listing requirements. The company’s shares are currently suspended from trading, so its specific market capitalization cannot be determined at this time.

In summary, considering both corporate scale and IPO intentions, Novogene and Annoroad Gene Technology are more likely to become the next companies to go public. Additionally, subsidiaries of CapitalBio Corporation, including CapitalBio Jingdian, CapitalBio Yihe, and CapitalBio Muhua, all have plans for independent listings. Among them, CapitalBio Jingdian is the largest of the five subsidiaries and is most likely to list first.

Among NEEQ-listed companies, four meet the basic listing requirements, with Subo Medicine having the highest market capitalization.

However, the aforementioned issues only pertain to a relatively fundamental level. A company’s IPO and development are also influenced by technology, policy, market environment, and human factors. As the capital markets for next-generation sequencing (NGS) have just begun to open up, VCBeat, as an observer and recorder of the healthcare industry, will continue to monitor and document the sector’s development and transformation.