IPO Market Rebounds: 25 Pharma Companies Go Public in First Half, Total Market Cap Exceeds RMB 150 Billion

IPO Market Rebounds: 25 Pharmaceutical Companies List in H1, Raising Over RMB 10 Billion with a Combined Market Cap Exceeding RMB 150 BillionAs a “perennial sunrise industry,” the pharmaceutical sector is highly favored by capital markets due to its high growth potential and counter-cyclical resilience. Post-listing stock performance has been robust, with maximum gains exceeding 800%.

VCBeat (WeChat ID: vcbeat) scanned pharmaceutical companies that entered the capital market in the first half of the year, compared the data with that of previous years, and provided an overview of their performance in the capital market.

IPO Companies in the First Half of the Year Have Surpassed Last Year's Total

Data released by Baker McKenzie in July this year shows that the recovery of China’s IPO market has exceeded expectations. In the first half of 2017, the number of domestic IPOs increased by 213%, and the amount of financing from domestic listings rose by 160% to reach $16 billion.

The broader market performed well, and with the China Securities Regulatory Commission (CSRC) accelerating the IPO review process, the number of pharmaceutical companies listing on capital markets in the first half of this year (as of July 31) far exceeded previous levels.

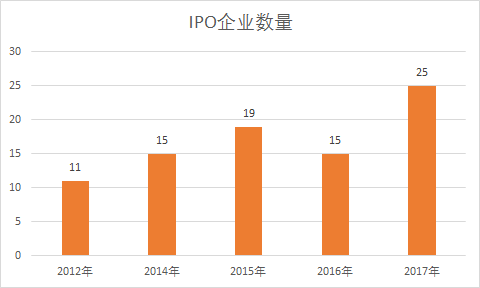

Data shows that pharmaceutical companies have been actively pursuing initial public offerings (IPOs) since 2012. In 2012, 11 pharmaceutical companies successfully completed their IPOs. In 2013, the China Securities Regulatory Commission (CSRC) conducted rigorous financial reviews of IPO applicants, leading to a temporary suspension of IPO activities. From 2014 to 2016, IPOs resumed, with pharmaceutical companies returning to the CSRC’s review queue, and the number of IPOs saw a slight rebound. This year, as of July alone, 25 pharmaceutical companies have successfully gone public, far exceeding the annual average of previous years.

According to previous statistics from VCBeat, as of mid-May this year, the number of healthcare companies waiting in line for an initial public offering (IPO) reached 56. Based on the review status by the China Securities Regulatory Commission (CSRC), it is expected that more than 40 healthcare companies will enter the capital market this year, setting a new record for the highest number of companies entering the capital market in history.

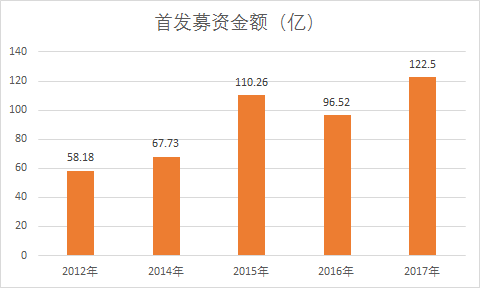

We reviewed the fundraising performance of pharmaceutical companies that went public over the past five years and found that IPO proceeds in the first half of this year reached a record high of RMB 12.25 billion. In other years, only 2015 saw total IPO fundraising exceed RMB 10 billion.

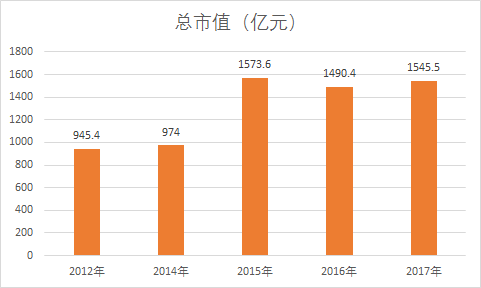

Additionally, we compiled statistics on the market capitalization of recently IPOed companies (as of the morning close on July 31) and found that companies going public in the first half of this year held no significant advantage in terms of total market capitalization. Despite a substantially larger number of listings compared to last year, their aggregate market cap remained roughly on par with last year’s level and still fell short of the 2015 figure.

Current Market Capitalization of Listed Pharmaceutical Companies Over the Years

This also indirectly demonstrates that the pharmaceutical industry is a relatively mature sector, where leading players have secured advantages such as access to capital by listing on financial markets, thereby further solidifying their dominant positions. In contrast, newcomers in the capital markets are mostly technology-first enterprises; although currently smaller in scale, they possess greater growth potential.

Overall, a comparison of this year’s IPO data with historical figures reveals that pharmaceutical companies have shown a stronger willingness to enter the capital markets amid a favorable overall market trend. The China Securities Regulatory Commission’s supportive stance toward new listings has also facilitated the opening of the IPO gateway for pharmaceutical enterprises.

One company IPOs per week on average

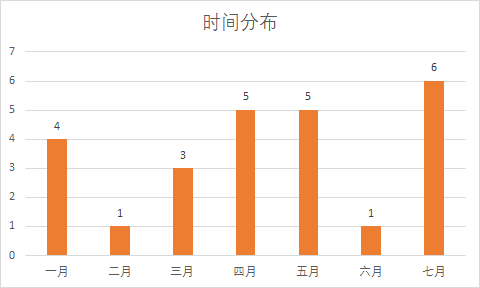

Below, we will conduct a detailed analysis of the IPO data for pharmaceutical companies this year. First, let us examine the summary table of pharmaceutical companies that entered the capital market in the first half of this year. From January 6 to July 31, a total of 25 pharmaceutical companies successfully completed their initial public offerings (IPOs). On average, one company went public every 8.4 days (approximately once a week).

Data cutoff date: July 31

On a monthly basis, there is no particular temporal pattern, with IPOs distributed relatively evenly. In July, six companies successfully completed their initial public offerings (IPOs), marking a minor peak for the year’s listings. These newly listed companies included Dashenlin Pharmaceutical Chain in pharmaceutical commerce, Intco Medical in medical devices, and BGI Genomics in the field of genomics.

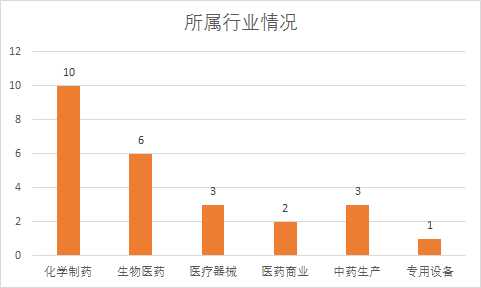

In terms of industry sectors, chemical pharmaceuticals is the most prominent field, with 10 companies, followed by biopharmaceuticals, which has 6 companies. Other sectors, such as medical devices, pharmaceutical commerce, traditional Chinese medicine (TCM) production, and specialized equipment, also have a presence.

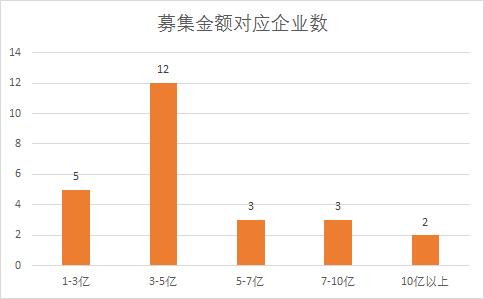

In terms of funds raised, the performance of pharmaceutical companies that went public in the first half of this year was not particularly outstanding. Five companies raised between RMB 100 million and RMB 300 million. The majority of companies raised funds in the range of RMB 300 million to RMB 500 million, with a total of 23 companies raising less than RMB 1 billion. Two companies raised more than RMB 1 billion: Xintian Pharmaceutical and Situo Biotechnology, which raised RMB 1.185 billion and RMB 1.074 billion, respectively. Other companies, such as Dashenlin Pharmacies, Rongtai Health, and Jidan Biotechnology, also secured substantial amounts of funding.

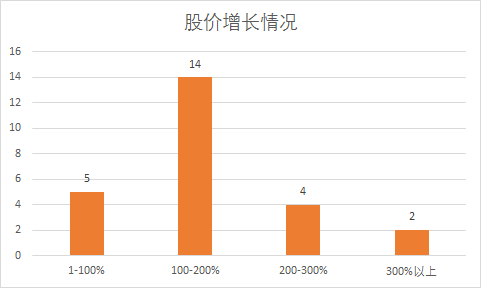

Judging from the post-listing growth performance, pharmaceutical stocks listed as new or secondary-new shares in the first half of this year have demonstrated robust performance, with an average price increase of 173.98%, effectively doubling their market capitalization after listing. Five companies recorded gains in the 1–100% range (Dashenlin posted a first-day gain of 44.01% and is expected to continue its upward trend). The largest group, comprising 14 companies, saw increases in the approximate range of 100–200%. CanSino Biologics, Sonoscape Medical, and BGI Genomics all surged by more than 300%, with CanSino Biologics leading the pack with a remarkable gain of 884.43%.

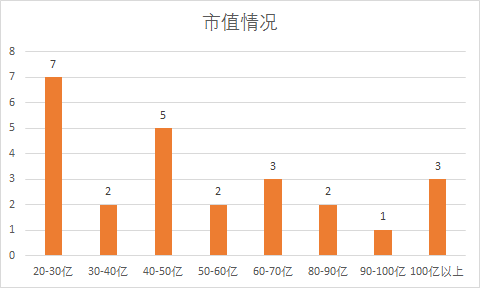

Based on market capitalizations as of the morning session on July 31, the distribution of market caps for companies that went public in the first half of the year was relatively uniform. Each market cap bracket below RMB 10 billion included at least two companies. The 2–3 billion RMB bracket had the highest number of companies, with seven, followed by the 4–5 billion RMB bracket, with five. Three companies had market capitalizations exceeding RMB 10 billion: BGI Genomics, Dashenlin Pharmaceutical Group, and Kangtai Biological Products. Among them, BGI Genomics, listed as the first next-generation sequencing (NGS) stock, led with a current market capitalization of RMB 22.417 billion.

In addition, we have compiled price-to-earnings (P/E) ratio data for new listings and recently listed stocks from the first half of this year to assess the sustainability of their growth in the capital market. According to our statistics, the issuance P/E ratios for pharmaceutical IPOs in the first half of this year were all around 22.98, whereas the average P/E ratio for listed pharmaceutical companies stands at 50. This indicates substantial upside potential for these new stocks following their market debut.

We compiled two sets of price-to-earnings (P/E) ratio data—TTM and LYR—for IPOs and recently listed stocks during the first half of the year. The former is calculated as current share price divided by earnings per share (EPS) over the most recent 12 months, reflecting the relationship between the current stock price and historical performance. The latter is calculated similarly, using the current share price divided by the EPS reported in the previous year’s annual report, thereby providing an assessment of the company’s growth potential.

In the first half of this year, the average TTM (Trailing Twelve Months) P/E ratio for pharmaceutical stocks that went public was 50.18, with a minimum of 26.80 for Jianyou Shares and a maximum of 135.16 for Kangtai Biological Products; the average LYR (Last Year Ratio) P/E was 40.58, with a minimum of 20.43 for Autek China and a maximum of 138.29 for Kangtai Biological Products.

In summary, driven by the resumption of IPO approvals, pharmaceutical companies also witnessed an IPO surge in the first half of this year. Data from January to July alone surpassed the full-year totals of previous years, with both the number of IPO-listed companies and the scale of financing reaching record highs.

The pharmaceutical industry is relatively mature. After years of development, leading pharmaceutical companies have all gone public. Under the influence of new technologies and trends, small-scale innovative enterprises in fields such as biopharmaceuticals, new materials, and genetics are still entering the capital market. In addition, driven by policies encouraging private investment in the medical services sector, medical service targets are showing strong growth momentum, with promising future prospects.

Case Study Analysis

BGI was founded in 1999 and participated early on in the Human Genome Project, one of the “Three Major Scientific Projects of the 20th Century,” completing 1% of the human genome sequencing task, thereby establishing BGI’s technological advantage in the field of genomics.

Subsequently, BGI completed the Rice Genome Project in 2001, marking China’s pioneering achievement worldwide in delivering the working draft sequence and database of the rice (indica) genome. The related paper was featured on the cover of *Science*, bolstering BGI’s international prominence. However, at that time, BGI still operated under the auspices of the Chinese Academy of Sciences, with its commercial prospects and profit model remaining unclear.

In 2007, Wang Jian, founder of BGI, resigned from his position as Deputy Director of the Beijing Genomics Institute and led BGI to relocate south to Shenzhen, marking BGI’s return to private-sector status. That year, BGI successively purchased multiple gene sequencers from companies such as Illumina, Life Technologies, and Roche, thereby initiating its deployment of commercial gene sequencing services.

In 2010, BGI purchased more than 100 gene sequencers from Illumina in a single transaction. This order, the largest in BGI’s corporate history, also propelled BGI to become the world’s largest sequencing center. In 2012, BGI acquired Complete Genomics (CG), a U.S.-based manufacturer of gene sequencing instruments, for $117.6 million, marking its entry into the upstream segment of the gene sequencing industry.

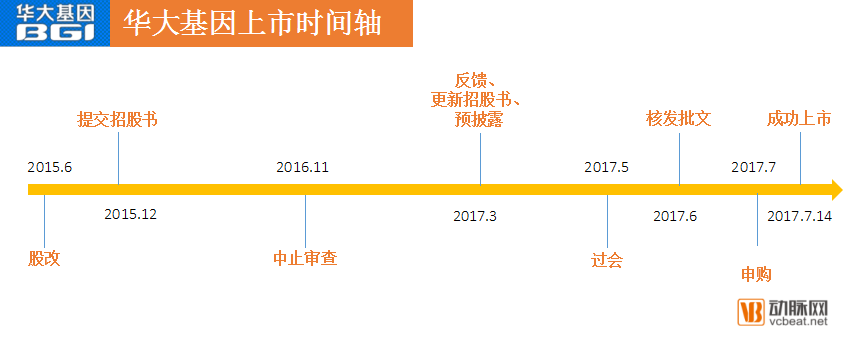

From the perspective of its listing journey, BGI Genomics’ path to going public was arguably fraught with challenges. As early as 2014, BGI initiated internal restructuring to clarify its equity structure. In February 2015, BGI embarked on a new round of financing, introducing institutional investors such as Shenzhen Gaoheyulin and China Life Insurance, with total investment amounting to RMB 2 billion—the largest financing round for BGI Genomics prior to its IPO.

In August 2015, BGI Genomics announced its plan to conduct an initial public offering (IPO) on China’s domestic securities market. In December of the same year, it submitted its prospectus to the ChiNext Board and entered the queue for regulatory review. In December 2016, the ChiNext Board responded that BGI Genomics’ “application documents were incomplete, preventing the continuation of the review process,” resulting in the termination of the IPO review.

According to the prospectus, BGI Genomics’ core business is genetic testing, providing genomics-based diagnostic and research services to medical institutions, research organizations, enterprises, and public institutions. Over the past three years, BGI Genomics reported annual revenues of RMB 1.131 billion, RMB 1.319 billion, and RMB 1.711 billion, with net profits of RMB 58 million, RMB 272 million, and RMB 350 million, respectively.

By March this year, BGI Genomics received feedback on its IPO application, entering the final sprint phase of its listing. On July 14, BGI Genomics held its bell-ringing ceremony on the ChiNext board, securing the title of “the first NGS stock.” Following its IPO, BGI Genomics hit the daily price ceiling for 18 consecutive trading days. As of the market close on August 10, its share price stood at RMB 106.40, with a total market capitalization of RMB 42.571 billion.

Kangtai Biological Products was established in 1992, with approval from the Ministry of Finance and the Shenzhen Municipal Government. At that time, its primary mandate was to introduce a project for recombinant (yeast) hepatitis B vaccine production. In 2002, Kangtai Biological underwent shareholding reform and entered the pre-IPO tutoring phase. Subsequently, the company underwent multiple rounds of restructuring to attract social capital.

Kangtai Biologicals’ prospectus discloses that its core business involves the research and development, production, and sales of human vaccines. Its main products include recombinant hepatitis B vaccine (Saccharomyces cerevisiae) (in three strengths: 10 µg, 20 µg, and 60 µg), Haemophilus influenzae type b conjugate vaccine, measles-rubella combined live attenuated vaccine, and acellular diphtheria-tetanus-pertussis–Haemophilus influenzae type b combination vaccine, among others. Since its establishment, the company’s core business has not undergone any significant changes.

Kangtai Biological Products is one of the earliest enterprises in China engaged in the production of recombinant hepatitis B vaccine (Saccharomyces cerevisiae). Currently, its two production bases are located in the Science and Technology Industrial Park in Nanshan District, Shenzhen, and the Daxing Biomedical Industry Base of the Zhongguancun Science Park in Daxing District, Beijing. Additionally, the Kangtai Biological Guangming Vaccine R&D and Production Base, covering an area of 62,400 square meters, is under construction.

Kangtai Biological possesses a domestically advanced vaccine R&D center. Through years of continuous research and innovation, it has established a robust pipeline of vaccine products characterized by a diverse portfolio, an optimized product structure, and strong market prospects. In addition to the four products already on the market, Kangtai Biological currently has 24 projects in development: four have submitted applications for drug registration approval, eight have obtained clinical trial approvals, three have applied for clinical studies, and nine are in the preclinical research stage. To date, the company has been granted 27 patents, including 26 invention patents and one utility model patent.

In terms of production and sales model, Kantaibio adopts a “production based on sales” approach. Its primary end customers are disease prevention and control institutions at all levels and vaccination units. The company formulates sales plans and guides production based on market sales performance and forecasts. Financial data show that Kantaibio’s annual revenues for the past three years were RMB 303 million, RMB 453 million, and RMB 552 million, respectively, with net profits of RMB 31 million, RMB 63 million, and RMB 86 million, respectively.

Sonoscape Medical’s predecessor, Sonoscape Limited, was established in 2002 under the leadership of Yao Jinzhong. As one of the pioneers and founders of China’s ultrasound instrumentation industry, Mr. Yao has been engaged in the research, development, and manufacturing of ultrasound equipment since the 1960s. He previously served as Director of the Shantou Ultrasound Instrument Research Institute, as well as Deputy General Manager and Chief Engineer of Shantou Ultrasound Electronic Instrument Co., Ltd. In 2014, Sonoscape Limited underwent shareholding restructuring and completed the corresponding industrial and commercial registration changes.

Sonoscape’s core business involves the research and development, manufacturing, and sales of medical diagnostic equipment. After more than a decade of development, Sonoscape has established a comprehensive portfolio of medical ultrasound diagnostic products and expanded into the field of medical endoscopy, gradually diversifying its product lines within the medical diagnostic equipment sector.

In terms of sales networks, SonoScape has established branches or offices in 29 provincial-level administrative regions across China, with its international sales and service network covering more than 120 countries and regions, including the United States, Italy, Russia, Germany, and Brazil.

Financial data shows that ultrasound diagnostic equipment is the main source of revenue for Sonoscape Medical, accounting for about 90% of its total revenue, while medical endoscopes and accessories account for around 10%.

Over the past three years, Sonoscape Medical’s revenues were RMB 640 million, RMB 686 million, and RMB 719 million, with net profits of RMB 131 million, RMB 106 million, and RMB 130 million, respectively. After its listing, Sonoscape Medical’s total market capitalization once exceeded RMB 10 billion. As of August 10, its closing price was RMB 20.68 per share, with a total market capitalization of RMB 8.272 billion.

Founded in 1999 and headquartered in Guangzhou, Dashenlin is a group enterprise integrating pharmaceutical retail, manufacturing, and wholesale. It primarily engages in direct-operated chain retail services for Western and Chinese proprietary medicines, ginseng and deer antler tonics, traditional Chinese medicine decoction pieces, health supplements, medical devices, and other products.

According to the prospectus, Dashenlin opened an average of approximately 400 new stores annually across China. By the end of 2016, the company operated a total of 2,409 stores. Guangdong Province served as its core market, with 1,809 stores, followed by Guangxi and Henan. The company also had a presence in Jiangxi, Fujian, and Zhejiang provinces.

Data shows that Dashenlin’s main business revenue for the past three years was RMB 4.451 billion, RMB 5.152 billion, and RMB 6.154 billion, respectively. The average annual revenue growth rates in 2015 and 2016 were 15.84% and 19.14%, significantly exceeding the growth rates of the pharmaceutical retail sector and listed chain pharmacies during the same period.

On July 31, Dashenlin held its IPO bell-ringing ceremony, issuing 40.01 million new shares and raising RMB 989 million. According to its prospectus, the proceeds will be used to expand its pharmaceutical retail network and construct logistics centers, with a plan to add more than 1,300 stores within three years.

Based on benchmarking cases, Dashenlin bears certain similarities to Yixintang, a pharmaceutical retail chain that went public earlier. Both are regional leaders aiming to expand into the national market following their IPOs. After its listing in 2014, Yixintang expanded its store count by 600–700 outlets annually, reaching over 4,000 stores by the end of the first quarter of this year. Based on this trajectory, Dashenlin’s store count may also surpass 4,000 within the next three years.

In terms of the overall pharmaceutical retail market, data from the Ministry of Commerce shows that the market size had grown to RMB 332.3 billion by the end of 2015 and is expected to exceed RMB 350 billion in 2016. With the implementation of policies such as the separation of prescribing and dispensing and the outflow of prescriptions, the pharmaceutical retail market is poised for continued expansion. Beneficiaries include regional leaders and already-listed industry giants.

Currently, listed companies in the pharmaceutical retail sector include Yixintang, Yifeng Pharmacy, and Laobaixing Pharmacy. Retail pharmacy chains planning to enter the capital market this year include Shuyu Civilian Pharmacy and Jianzhijia. The pharmaceutical retail market will undergo further M&A consolidation, with capital serving as a significant driving force.

As of the market close on August 10, Dashenlin closed at RMB 37.91 per share, with a total market capitalization of RMB 15.164 billion, making it the leading listed company in the pharmaceutical retail sector.

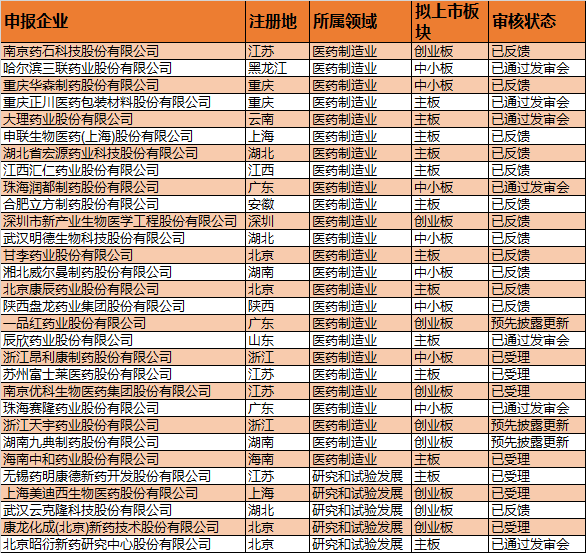

Appendix: Information on Companies Filing for Initial Public Offering (IPO)