WuXi AppTec Files IPO Prospectus, Aiming to Become China's Leading Pharma Stock as CRO Market Nears RMB 100 Billion by 2020

Domestic CRO company WuXi AppTec disclosed its IPO prospectus early last month, which was accepted by the China Securities Regulatory Commission (CSRC). The prospectus indicates that WuXi AppTec plans to raise RMB 5.741 billion. If successful, this offering would set a record for the largest fundraising in the biopharmaceutical industry over the past six years.

WuXi AppTec is positioned as a small-molecule chemical drug CRO platform, providing professional services to pharmaceutical companies and R&D institutions throughout the drug development process. Benefiting from the accelerated implementation of consistency evaluations, China’s formal accession to the ICH, and the rollout of the Marketing Authorization Holder (MAH) system, CRO firms have generally reaped benefits. WuXi AppTec’s planned listing on the Main Board further demonstrates that the capital market has begun to pay significant attention to the CRO sector.

Prior to WuXi AppTec’s IPO plans, Quantum Hi-Tech announced in June of this year that it would acquire the CRO firm ChemPartner for RMB 2.38 billion; earlier still, Baihuacun acquired Huawei Pharma to pivot toward pharmaceutical R&D, and Yatai Pharmaceutical acquired Shanghai New Summit, among other deals, signaling that CRO companies are being heavily favored by both the industry and capital markets.

VCBeat (WeChat ID: vcbeat) provides a concise overview of the development history of the CRO industry and introduces high-quality domestic and international CRO companies, aiming to conduct a preliminary scan of the CRO sector.

Multiple Factors Drive the Development of the CRO Industry

CRO (Contract Research Organizations): Contract research organizations generally refer to academic or commercial scientific institutions that provide specialized services to pharmaceutical companies and R&D institutions during the drug development process through contractual agreements.

Several factors have contributed to the emergence of Contract Research Organizations (CROs). First, the high degree of social division of labor has led to the separation of research and development (R&D) from manufacturing in the pharmaceutical and biotechnology industries, thereby driving the growth of outsourced R&D services. Second, drug development is inherently a time-consuming, capital-intensive, and high-risk endeavor. Many small pharmaceutical companies lack independent R&D institutions or possess limited R&D capabilities, necessitating the outsourcing of their R&D activities. For large corporations, outsourcing R&D also helps mitigate development risks and facilitates the pursuit of diversified R&D initiatives.

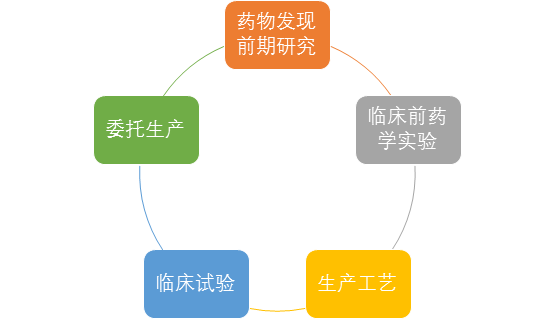

From the perspective of business scope, CRO services encompass preclinical research, clinical trials, technology transfer, and consulting, covering the entire process from new drug discovery and clinical development to regulatory registration. As the CRO market matures, diverse business models have emerged, including contract manufacturing and collaborative R&D between manufacturers and research institutions, making CRO an increasingly vital segment of the pharmaceutical and biotechnology industry.

CRO Service Scope

Top 10 Global CRO Companies Account for Half of the Market

CROs originated in the United States. During the 1970s and 1980s, the U.S. initiated reforms in healthcare payment models, shifting from fee-for-service to prospective payment systems and managed care, which significantly impacted pharmaceutical companies. In response to an increasingly stringent market environment for drug consumption, U.S. pharmaceutical firms placed greater emphasis on R&D investment for new drugs, giving rise to the outsourcing of research and development.

From the mid-1980s to the 1990s, companies such as Parexel, PPD, ICON, and Covance were established and went public, marking a period of rapid growth for the U.S. CRO market. After 2000, these leading U.S.-based CROs began expanding globally and pursuing mergers and acquisitions within the industry, gradually diversifying their service offerings to cover the entire lifecycle from new drug discovery to post-marketing consultation.

As an inevitable outcome of specialized social division of labor in the field of new drug development, CRO companies have achieved rapid growth by leveraging advantages such as cost-effectiveness and operational efficiency, gradually becoming an indispensable link in the pharmaceutical R&D industry chain.

Furthermore, CROs do not merely provide outsourced R&D services; their offerings often extend to contract manufacturing and contract development and manufacturing (CMO/CDMO). These services cover both the R&D and contract manufacturing stages of new drug development. Collectively referred to as pharmaceutical services, these business lines are typically encompassed by most large-scale pharmaceutical service enterprises.

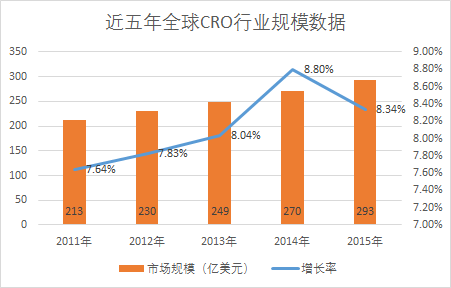

According to data from Southern Pharmaceutical Institute, global sales in the pharmaceutical services industry have experienced rapid growth in recent years, rising from $28.831 billion in 2010 to $45.587 billion in 2016, with a compound annual growth rate (CAGR) of 7.93%. As the largest segment within this industry, the CRO market size increased from $21.3 billion in 2011 to $29.3 billion in 2015, representing a CAGR of 8.25%.

Data Source: CFDA Southern Institute of Pharmaceutical Economics

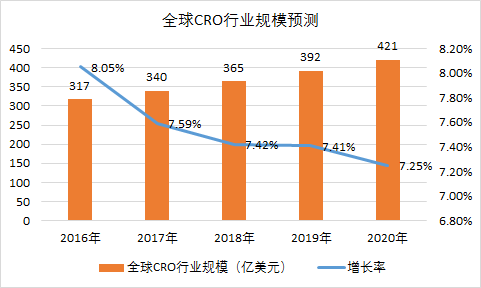

According to forecasts by the Southern Institute, global CRO industry sales will reach $31.7 billion in 2016 and $42.1 billion by 2020, with a compound annual growth rate (CAGR) of 7.42%, slightly lower than the level of the previous five years.

Data source: Southern Institute of Pharmaceutical Economics, CFDA

Introduction to Globally Renowned CRO Companies

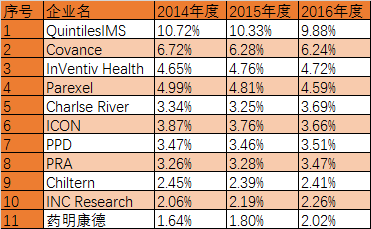

The global CRO market is highly concentrated. According to data from IMAP Global, a mergers and acquisitions advisory firm, the top ten CRO companies hold more than 45% of the market share and are continuously engaging in cross-industry M&A consolidation to further strengthen their market dominance. The majority of these dominant players are U.S.-listed companies, including Quintiles, Covance, Parexel, and ICON.

Quintiles is the world’s largest CRO company. It was founded in 1982 by Dennis Gillings in North Carolina, United States, initially serving only the U.S. market. The company began its international expansion in 1987 by opening offices in Europe and entered the Asian market in 1993.

In 1994, Quintiles went public on the NASDAQ. Leveraging capital market support post-IPO, it pursued mergers and acquisitions to achieve rapid growth. In 2000, Quintiles established its PharmaBio division to provide pharmaceutical companies with funding, technical expertise, and sales teams, aiming to earn post-launch sales commissions while sharing both risks and rewards with its partners.

During this period, the collaboration between Quintiles and Eli Lilly stood out as a classic example. At that time, Eli Lilly had submitted an antidepressant drug to the FDA for approval. Quintiles entered into a cooperation agreement with Eli Lilly regarding this drug, providing an upfront investment of $70 million and deploying a sales team of hundreds to facilitate its commercialization in the U.S. market. Following its launch, the drug achieved strong sales performance, yielding substantial returns for Quintiles. However, this model was not scalable on a large scale, and its revenue stream was highly volatile. Investors were skeptical of this approach, which adversely affected the company’s stock price. In 2003, Quintiles was delisted.

In 2013, Quintiles spun off its PharmaBio business, retaining its traditional clinical trial services and post-launch commercial services for pharmaceuticals. The company restarted its IPO plan, raising $947 million, and its stock price continued to rise after the listing.

In May 2016, Quintiles announced its merger with IMS Health, a global leader in strategic consulting services for the pharmaceutical and healthcare industries. The merged company was renamed Quintiles IMS Holdings, Inc., further solidifying and enhancing its industry position by providing comprehensive commercial service solutions to pharmaceutical companies.

Data from the Southern Institute shows that Quintiles holds a market share of approximately 10% in the global CRO industry, with figures of 10.72% in 2014, 10.33% in 2015, and 9.88% in 2016. Quintiles currently employs more than 50,000 people, with subsidiaries and offices spanning over 100 countries and regions worldwide. As of the market close on August 1, Quintiles’ total market capitalization reached $19.866 billion.

Covance was originally the pharmaceutical services division of Corning Glass. In April 1996, Corning spun off its relevant laboratory and pharmaceutical services companies to form two new entities: Quest Diagnostics and Covance. Covance began trading as an independent company on the New York Stock Exchange.

In 2007, Covance established a central laboratory in Shanghai, marking its entry into the Chinese market.

In 2008, Covance acquired a minority stake in Caprion Proteomics to further strengthen its biomarker services offered to clients. Caprion Proteomics is a leading proteomics service provider in the pharmaceutical industry. In the same year, Covance acquired Eli Lilly’s campus in Greenfield, Indiana, and executed a 10-year service agreement with Eli Lilly.

In the following years, Covance pursued a series of acquisitions, including Merck’s gene expression laboratory in Seattle. Under the agreement, Merck also entered into a $145 million contract to purchase gene analysis services from Covance. In the same year, Covance acquired Swiss Pharma Contract, a clinical research company based in Basel, Switzerland. The following year, Covance signed a 10-year strategic R&D alliance agreement with Sanofi and acquired its research centers in France and the United Kingdom.

In 2015, LabCorp, an IVD laboratory oligopolist in the United States, acquired Covance Inc. to form a world-leading medical diagnostics company that provides comprehensive clinical laboratory services and end-to-end solutions for drug and diagnostic R&D and commercialization.

According to data from Southern Pharma Institute, Covance is currently the second-largest CRO service provider, with a market share of 6.24% in 2016.

InVentiv Health is the world’s third-largest contract research organization (CRO). According to data from the Southern Institute of Pharmaceutical Industry, the company held a 4.72% market share in 2016. This May, INC Research, the tenth-ranked CRO with a 2.26% market share in 2016, announced its merger with InVentiv Health. On this basis, the combined entity’s market share will approach or surpass that of Covance, challenging for the second position in the CRO industry.

INC Research was incorporated in the State of Delaware, United States, on August 13, 2010. As a leading global contract research organization (CRO), it specializes in clinical development services for Phase I through Phase IV trials in the biopharmaceutical and medical device industries. The company is highly regarded within the industry for its clinical development expertise in complex therapeutic areas, including central nervous system disorders and oncology.

In their merger announcement, the two companies stated that the combination of the world’s third-largest CRO service provider and a leading CCO service provider would generate strong business synergies. The merged entity will have 22,000 employees, with operations in more than 60 countries and serving clients in over 110 countries.

Leading Global CRO Companies and Their Market Share

Data source: CFDA Southern Institute of Pharmaceutical Economics

Following the merger of InVentiv Health and INC Research, the global CRO market will become further consolidated, with the top ten service providers accounting for approximately 50% of the market share.

In the future, the CRO industry will exhibit three major trends. First, new drug development is gaining increasing attention, and pharmaceutical companies are ramping up R&D expenditures, laying a solid foundation for sustained growth in the CRO sector. Second, mounting pressure from rising R&D costs and prolonged development cycles is strengthening pharmaceutical companies’ willingness to engage external CRO firms to convert fixed costs into variable ones. Third, the CRO industry is poised to trend toward integrated development, with CRO services spanning multiple stages—from drug discovery and preclinical research to new drug registration and post-marketing services—thereby covering the entire lifecycle of pharmaceutical products.

China's CRO Industry Enters a Phase of M&A and Consolidation

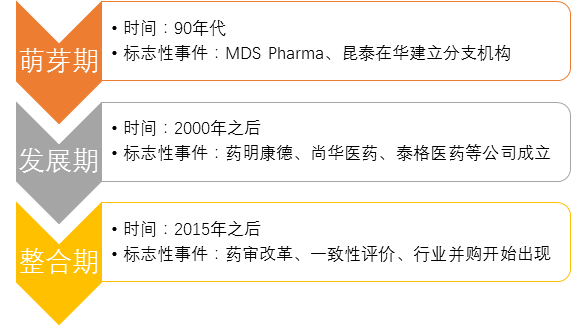

Similar to the pharmaceutical industry, China’s CRO sector developed relatively late and was likewise introduced by foreign enterprises. In 1996, MDS Pharma Services invested in establishing the first true CRO company in China, primarily engaged in clinical research services, marking the nascent stage of China’s CRO industry. In 2000, WuXi AppTec was founded, followed by the establishment of companies such as Pharmaron, Boji Medical, and Tigermed, ushering China’s domestic CRO industry into a period of growth.

Several key factors are influencing the development of China’s CRO industry. First, the domestic pharmaceutical market is gradually aligning with international standards, while multinational pharmaceutical companies are steadily increasing their R&D investment in China. Second, policy-driven initiatives—such as reforms in drug review and approval and the consistency evaluation program—have spurred rapid expansion of the outsourcing market for R&D and clinical trial services. Third, driven by healthcare payment system reforms and cost-containment measures within medical insurance, new drug development has garnered growing attention from Chinese pharmaceutical companies; CROs can, to a certain extent, help offset deficiencies in these companies’ in-house R&D capabilities.

First, multinational pharmaceutical companies have increased their investments in China. According to statistics from Qianzhan Industry Research Institute, since 2000, these companies have invested over RMB 10 billion in China and established dozens of new R&D centers.

Source: Qianzhan Industry Research Institute

According to forecasts by Qianzhan Industry Research Institute, as approval timelines shorten and demand in the pharmaceutical market remains robust, China will continue to attract foreign pharmaceutical companies into its market. As multinational corporations expand their R&D operations within China, leading domestic CROs will be the first to secure collaboration opportunities with these multinational pharmaceutical firms. They will gradually become preferred suppliers and key strategic partners for multinational pharmaceutical companies in China, gaining strong financial support and access to global R&D resources, thereby enjoying industry benefits on a priority basis.

Secondly, policy-driven factors such as the reform of China’s drug approval process and the consistency evaluation should be considered. Here, we can refer to a policy checklist to understand the relevant laws applicable to China’s pharmaceutical services industry.

As evident from the aforementioned policies, China’s pharmaceutical market is transitioning from being dominated by generic drugs to being led by innovative drugs, with policy incentives strongly favoring innovation. Previously, Chinese pharmaceutical R&D enterprises primarily focused on generics, resulting in limited demand for pharmacological and toxicological services and a relatively small preclinical CRO market. Following national top-level design mandates that emphasize new drug innovation and gradual alignment with international standards, pharmaceutical companies have increased their investment in innovative drug R&D, thereby directly driving growth in the CRO industry.

Furthermore, China’s pharmaceutical industry is in a golden period of rapid development, and the incremental market space provides robust market support for the growth of pharmaceutical R&D services. In terms of the drug sales market, since 2012, the terminal drug market has maintained a compound annual growth rate (CAGR) of 13.09%. By 2016, the size of the drug market had approached RMB 1.5 trillion, making China the second-largest pharmaceutical market globally, from which domestic pharmaceutical companies have directly benefited.

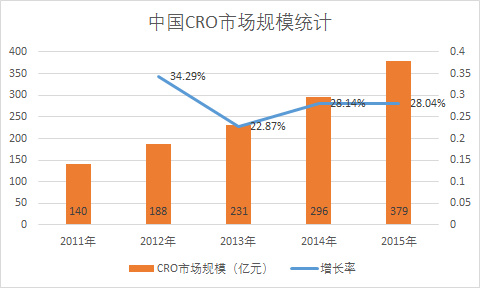

According to data from Southern Pharmaceutical Institute, sales in China’s CRO industry rose from RMB 14 billion in 2011 to RMB 37.9 billion in 2015, representing a compound annual growth rate (CAGR) of 22.04%, which exceeded the growth rate of the global CRO market during the same period.

Data Source: Southern Institute of Pharmaceutical Industry. The sales figures presented here represent domestic sales by local enterprises and exclude their overseas sales.

The Southern Institute projects that sales in China’s CRO market will reach RMB 46.2 billion in 2016, with a compound annual growth rate (CAGR) of 20.79% over the next five years, bringing the market size to RMB 97.5 billion by 2020.

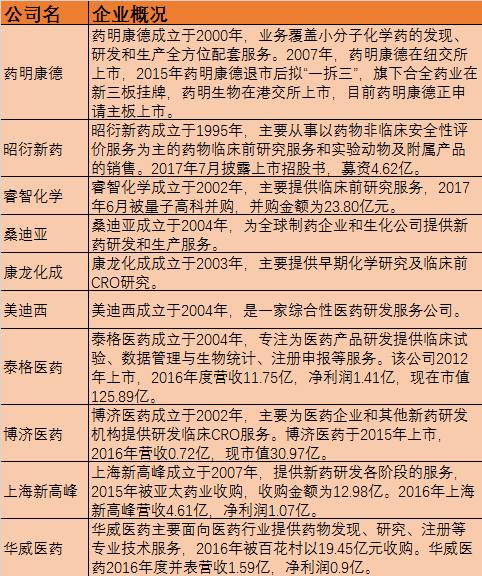

Overview of Domestic CRO Companies

Recently, WuXi AppTec applied for a listing on the main board, aiming to raise RMB 5.74 billion. It is poised to become this year’s most highly valued new pharmaceutical stock, and upon its listing, its market capitalization is expected to challenge the leading position among domestic pharmaceutical companies. WuXi AppTec’s confidence stems from its role as one of the pioneers of China’s CRO industry, allowing it to fully benefit from the industry’s growth dividends. In addition to WuXi AppTec, other companies such as Tigermed, Boji Medicine, ChemPartner, Shanghai New Summit, and Joinn Laboratories have maintained certain competitive advantages in their respective niche markets and have gained favor in the capital markets.

Overview of Domestic CRO Companies

References:

Prospectus for the Initial Public Offering of WuXi AppTec New Drug Development Co., Ltd. (Draft Submitted on July 4, 2017)

http://www.csrc.gov.cn/pub/zjhpublic/G00306202/201707/t20170714_320498.htm

Current Development Status and Future Prospects of the CRO Industry in China and Abroad_China Industry Information Network

http://www.chyxx.com/industry/201406/253193.html

Multinational Pharma Giants Set Up R&D Centers in China, Making the Country a Key Strategic Hub for Global CROs | The Economist - Qianzhan.com

http://www.qianzhan.com/analyst/detail/220/170414-cda63d46.html

Industry Consolidation + Technological Upgrading: Leading the Development of the CRO Industry