Why Are Real Estate Developers Rushing into the Health Industry? Ambitions Behind the 'Health + Property' Trend

1

# This Week’s Most Watched Subsectors

#Healthcare Real Estate#

Real Estate Developers’ Ambitions to Cross Over into Healthcare Begin to Emerge

On the evening of August 2, major media outlets rushed to report on Wanda’s establishment of a new big health group.Following Wanda Commercial, Wanda Culture, Wanda Network, and Wanda Financial, this new addition to the Wanda Group signals a clear strategic focus on the big health industry. It also clarifies recent uncertainties surrounding Wanda’s asset restructuring, including hurdles in overseas mergers and acquisitions and divestitures of domestic assets.Why Are Real Estate Developers Such as Vanke, Evergrande, Wanda, and Greentown Actively Entering the Health Industry? What Areas Are They Primarily Investing In? What Challenges Will They Face During Their Transition?

VCBeat Perspective

1. Traditional real estate developers are facing the dilemma of an economic downturn and are adjusting their strategic direction; with a promising outlook for the healthcare industry, investing in medical real estate has become one of the top priorities for these developers.

Although China’s total fixed-asset investment has maintained an overall upward trend, the growth rate has declined since 2012, with investment growth stabilizing. Meanwhile, the growth rate of real estate investment has shown a sharp decline. In terms of the share of residential investment within total real estate development investment, the proportion of residential investment has been gradually decreasing. Between 2008 and 2014, the share of residential investment dropped by 4.5 percentage points, indicating that the growth rate of residential investment has lagged behind that of overall real estate investment. This reflects a gradual shift in capital allocation from residential construction to other specialized construction sectors.

From a policy perspective, the proposals of the 13th Five-Year Plan elevated “Healthy China” to a national strategy, unlocking a trillion-yuan market and positioning the domestic healthcare industry as a new engine for economic growth. In recent years, the state has also introduced various favorable policies to encourage social capital investment in the healthcare sector. Furthermore, the healthcare industry not only boasts promising prospects but also offers substantial profit margins. In 2014, the industry’s total operating revenue reached RMB 684.636 billion, a year-on-year increase of 13.57%, while operating profits amounted to RMB 63.386 billion, up 17.71% year on year. Compared with the squeezed profit margins in the real estate sector, the healthcare industry’s robust profitability and strong growth potential have attracted significant inflows of real estate capital.

2. Real estate developers transitioning into the healthcare sector should first prioritize businesses with high synergy, such as medical real estate development and hospital investment—areas characterized by heavy asset attributes and high development margins.

Real estate developers’ investment layouts in the healthcare industry are primarily divided into four sectors: (1) healthcare real estate development, (2) hospital investment and operation, (3) medical devices, pharmaceuticals, and services, and (4) non-clinical services. Among these, (1) and (2) represent the preferred entry paths for mainstream real estate developers, presenting both opportunities and challenges. Sectors (3) and (4) are relatively niche; notably, sector (3) involves a complete departure from real estate and a thorough transformation, thus holding limited representative significance. Furthermore, regarding market entry strategies, smaller real estate developers tend to favor mergers and acquisitions (M&A). However, whether they possess comprehensive M&A strategies, conduct thorough due diligence, and ensure effective post-merger integration (such as establishing dedicated integration departments) remains an intriguing subject of discussion.

3. Hospital investment is emerging as a new trend among Chinese real estate developers in recent years; however, the recruitment of high-quality physicians, hospital management and operations, and hospital brand building remain significant long-term challenges.

In the United States, the healthcare real estate sector has developed a relatively mature system, whereas China’s investment model for healthcare real estate differs significantly. Data on healthcare real estate investment trusts (REITs) indicate that while senior housing and skilled nursing facility models are highly favored by institutional investors in the U.S., hospital investments are not mainstream—a trend that is exactly the opposite of what is seen in China.

Although factors such as cultural backgrounds and the lack of insurance payment mechanisms have made the short-term prospects for heavy-asset investments in China’s senior living real estate and nursing homes uncertain, the huge demand from an aging society means that both sectors are likely to mirror the U.S. market in the future, accounting for half of the healthcare real estate sector.

Meanwhile, hospital investment has emerged as a new trend among domestic real estate developers in recent years. However, recruiting high-quality physicians, managing hospital operations, and building hospital brands remain long-term challenges. The PPP (Public-Private Partnership) model, actively promoted by the government, may benefit investors to some extent, but its effectiveness still needs to be tested by the market. In the United States, large hospital institutions typically choose to build their own facilities to meet requirements related to medical processes, compliance, and equipment, while institutional investors are less involved.

Artery Report

Evergrande Enters the Big Health Sector as Real Estate Firms Cross Over into Healthcare

How Have Wealthy Real Estate Developers Fared in Their Foray into the Healthcare Sector?

2

# This Week's Must-Read Hot Stories

Author: Wang Xiaoxing

On August 3, Tencent officially launched its AI medical imaging product—Tencent Miying.

This is Tencent’s first AI product applied in the medical field. Tencent Miying comprises six artificial intelligence systems, covering diseases such as esophageal cancer, lung cancer, diabetic retinopathy, cervical cancer, and breast cancer. Among these, its intelligent screening system for early-stage esophageal cancer is the most mature, achieving a laboratory accuracy rate of 90%, and has now entered the preclinical trial phase.

At the Alibaba Cloud Apsara Conference Shenzhen Summit on March 29, 2017, the ET Medical Brain was officially launched. Now, Tencent has also entered the medical AI field with six product systems. Will the entry of these tech giants deliver a fatal blow to entrepreneurs in the medical AI sector?

First, China’s healthcare market is vast and cannot be captured by just one or two companies;

Secondly, although Tencent and Alibaba possess significant advantages in AI talent and computing power, the founders of startups are either masters or PhDs from national-level laboratories or experts returning from overseas studies, all of whom are independent AI talents. They entered the medical field 1-2 years earlier than AT, and their products are relatively more mature;

Furthermore, hospitals, as key stakeholders in medical AI, will not rely solely on VCBeat’s assessments. Currently, many medical AI startups have established collaborations with numerous large Grade 3A hospitals. With hospitals as partners, these startups gain access to a continuous stream of medical data. In addition, many startup products are already in clinical trial or even certification stages, and their systems are continuously collecting data on their own. Therefore, these companies are not overly concerned about data availability.

Finally, in terms of funding, although startups do not have the deep pockets of AT (Alibaba and Tencent), the recent investment boom in AI has enabled most artificial intelligence companies to secure substantial financing. In China, there have been 93 publicly disclosed financing events in the medical AI sector, with 57 of them explicitly revealing the amounts raised. Within China alone, financing rounds in the tens of millions and hundreds of millions of RMB account for more than 65% of these deals. Therefore, medical AI companies are not facing a capital shortage in the short term.

Author: Luo Mei

Faced with a vast healthcare market, how will Wanda carve out its share of the trillion-yuan medical sector following the establishment of its new Big Health Group? How can an asset-light strategy be applied to the big health industry? As a company adept at commercial real estate operations, how will Wanda break into the high-barrier healthcare sector? What transformation pathways have other real estate developers pursued? What noteworthy experiences can be drawn from Wanda’s big health model? Are there any successful examples of overseas real estate enterprises that have successfully transformed and can serve as references?

In 2015, Wanda Group began to propose a transformation, no longer acting as a real estate developer and actively adjusting its strategy. In a public speech, Wang Jianlin, Chairman of Wanda Group, mentioned that he hoped Wanda could remove "real estate" from its business within three to five years.

To facilitate the transformation, Wang Jianlin proposed the “2211 Strategy,” which aims to achieve total assets of $200 billion and a market capitalization exceeding $200 billion within five years, while reaching annual corporate revenue of $100 billion and net profits of at least $10 billion. Additionally, the proportion of revenue derived from real estate is to be reduced to below 30%.

On July 10, 2017, Wanda Commercial and Sunac China issued a joint announcement stating that Wanda Commercial would transfer 91% of the equity and debt of its 13 cultural tourism projects to Sunac for RMB 29.575 billion. Also included in the transaction were 76 hotels, valued at RMB 33.595 billion.

This is the largest M&A deal in the history of China’s real estate sector, yet Wanda Group has provided little further official interpretation. What many fail to realize is that Wang Jianlin had already mapped out this move as part of his de-real-estate strategy two years ago.

Wanda Group, while not having fully completed its divestment from real estate, is relentlessly expanding its footprint in the big health industry.

In other words, beyond its real estate and commercial operations, Wanda Group’s hospital division is becoming another prominent hallmark of the company.

Authors: Luo Mei, Gao Kangping, Gao Daolong, Li Yanyu

As China enters an aging society, healthcare services will remain the most significant public welfare demand for a long period to come.

Keenly perceptive developers, such as Vanke, Evergrande, Wanda, and Greentown, have already strategically positioned themselves in community services—particularly in the realm of community health and medical care—by implementing approaches they deem feasible, thereby spurring the emergence of a large number of senior housing projects and integrated medical-care-and-elderly-care initiatives.

National policies encourage private capital to invest in healthcare, vigorously promote new medical models, and especially advocate for a transition from “disease treatment” to “health intervention,” centered on family doctor services.

Leveraging the community as an entry point by utilizing its residents and their daily living needs as core resources is a key focus for real estate developers. However, the specific form in which medical services should be delivered within communities remains a proposition under long-term exploration.

Trends in real estate development are undergoing significant changes. First, there is a shift from product competition to service competition; second, a transition from property development to community operation; and third, an expansion from single-property business lines to integrated, innovative community platform services.

These ongoing changes are driven by three factors: first, the inevitable shift in the real estate industry from new development to existing property management; second, the redirection of social capital guided by emerging industries such as healthcare and medical services; and third, the trends associated with urbanization development and renewal.

Nurse Multi-Site Practice Takes Effect: What Does It Bring to China’s Dormant Home Nursing Market?

Author: Li Yanyu

Not long ago, the Beijing Municipal Health and Family Planning Commission issued the “Notice on Implementing Regional Registration for Nurses” (hereinafter referred to as the “Notice”), announcing that registered nurses in Beijing would be permitted to engage in multi-site practice starting August 1. Well before this date took effect, rumors had already been rife within the industry. Across the entire nursing sector, companies providing at-home nursing services are arguably the group most significantly impacted by the policy, aside from public hospitals and nurses themselves.

Can Beijing’s new policy completely resolve the myriad challenges and widespread skepticism previously raised by the industry regarding nurses’ multi-site practice? Can multi-site practice for nurses truly be implemented effectively? What impact will this have on the nursing sector, and even on enterprises?

The rapid development of health service industries, such as the integration of medical and elderly care, private capital investment in healthcare, and “Internet + Nursing,” has further expanded the scope of nursing services, gradually extending them from institutions to communities and homes. Meanwhile, the establishment of a tiered diagnosis and treatment system has imposed new requirements on primary-level nursing service capabilities.

In recent years, the State Council, the National Health and Family Planning Commission, and the Beijing Municipal Government have issued a series of policies to encourage and guide the development of health service sectors such as privately run medical institutions, integrated medical and elderly care, and home-based nursing. Relevant medical institutions have earnestly implemented these policies and actively explored new models, thereby meeting part of the public’s health needs.

Against this backdrop, the policy promoting multi-site practice for nurses was officially implemented on August 1. The notice stipulates that, effective August 1, the “Place of Practice” field in the Nurse Practicing Certificate for nurses registering in Beijing will be recorded as “Beijing.” This provision implies that nurses are no longer restricted to a single practicing institution, making “moonlighting” a legal and compliant practice.

There is a significant gap between the current community health service institution-led primary care nursing model and the public’s growing demand for nursing services. It is widely believed that nurses in primary care institutions suffer from low incomes and limited staffing quotas. However, the reality is that, apart from nurses in large tertiary hospitals, even those in ordinary secondary and tertiary hospitals do not have an easy time.

3

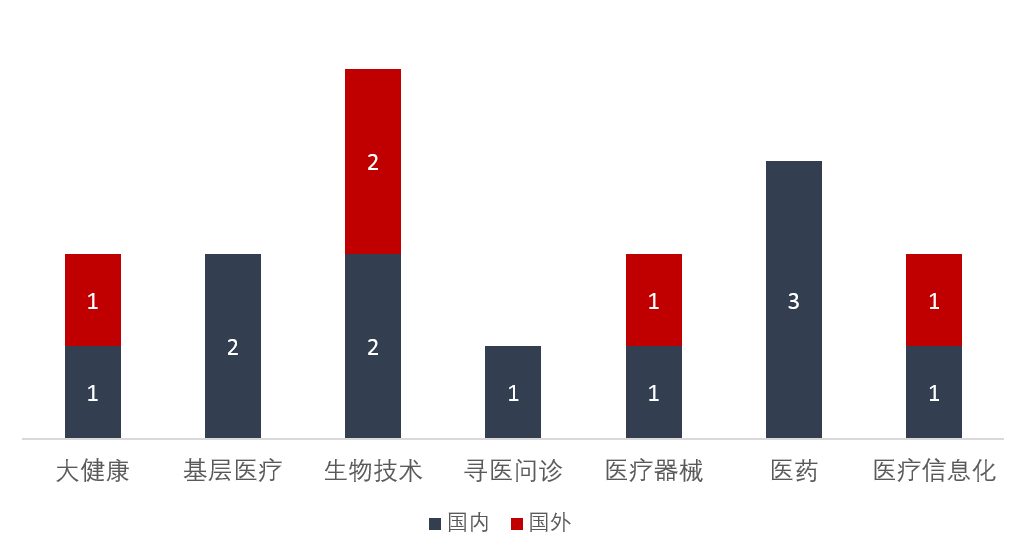

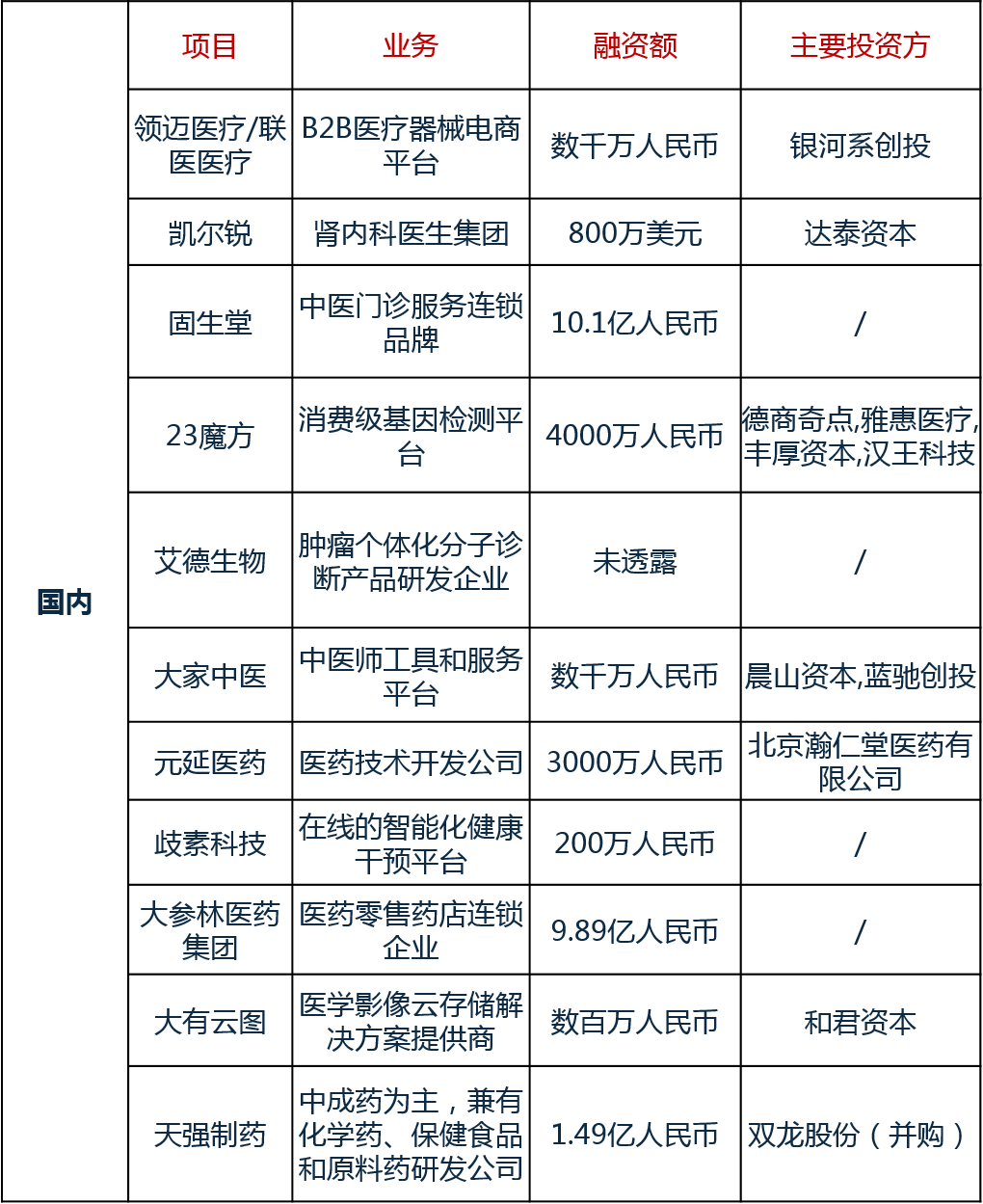

This Week's Financing Events in the Healthcare Sector

4

This Week’s Healthcare Industry Activity Updates

For more content, please refer to the VCBeat Knowledge Base!