China Liquid Biopsy Industry Landscape: A Comprehensive Scan of 6 Segments and 64 Companies

Advances in modern medicine have significantly reduced cancer mortality rates, yet annual cancer reports continue to draw considerable attention, with global new cases and deaths remaining in the millions each year.

Conventional cancer treatments, including chemotherapy, radiotherapy, and surgery, all have inherent limitations. The emergence of liquid biopsy holds the promise of revolutionizing traditional techniques for early cancer diagnosis and recurrence monitoring, providing real-time and effective technical support for precise medication guidance and treatment planning.

After several years of development, this new technology, which has received acclaim from MIT, has evolved into a massive global industry, becoming a hot and continuously expanding market. According to a report by Galaxy Securities, the liquid biopsy market is projected to maintain a compound annual growth rate (CAGR) of 21.7% over the next decade, with the global market size reaching $28.6 billion.

In June this year, VCBeat released five-year investment and financing data on the liquid biopsy sectors in China and the United States. A comparison of these figures reveals that although China’s liquid biopsy industry started slightly later than its U.S. counterpart, Chinese companies are rapidly catching up by building on the experience gained in the U.S. market, thereby gradually narrowing the gap.

So, what is the current state of development for Chinese liquid biopsy companies? How are these enterprises positioning themselves within the industry landscape, and what are the key challenges to be overcome and the critical success factors? To address these questions, VCBeat has decided to conduct a comprehensive review of their strategic layouts.

Relevant Enterprise Scanning

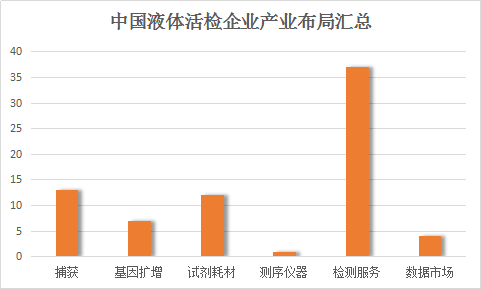

Liquid biopsy can be divided into six subfields, namely the upstream markets for capture, gene amplification, reagents, and instruments; the midstream market for testing services; and the downstream data market.

Due to the significant technical challenges in the upstream market, more companies have chosen to establish their presence in the midstream segment. Currently, there are 13 companies involved in the upstream capture market, six companies focused on gene amplification, and 37 companies operating in the midstream segment.

Capture and gene amplification are prerequisites for detection.Here, "capture" is a broad concept that encompasses the capture of viable circulating tumor cells (CTCs) as well as cell-free circulating tumor DNA (ctDNA), representing the first step in liquid biopsy.

Circulating tumor cells (CTCs) are present at extremely low levels in the peripheral blood of cancer patients and are even scarcer in precancerous lesions or early-stage tumors. Typically, only 1–10 CTCs are found in 10 mL of a patient’s blood, whereas the same volume contains approximately 50 billion red blood cells and hundreds of millions of white blood cells. Therefore, cell capture represents the most upstream technology for companies specializing in CTC-based detection.

ctDNA detection is technically less challenging. Circulating tumor DNA (ctDNA) fragments are present in the blood of nearly every individual, albeit at very low levels. The primary challenges in ctDNA-based detection lie in amplifying trace amounts of ctDNA and enhancing the sensitivity and specificity of the assay.

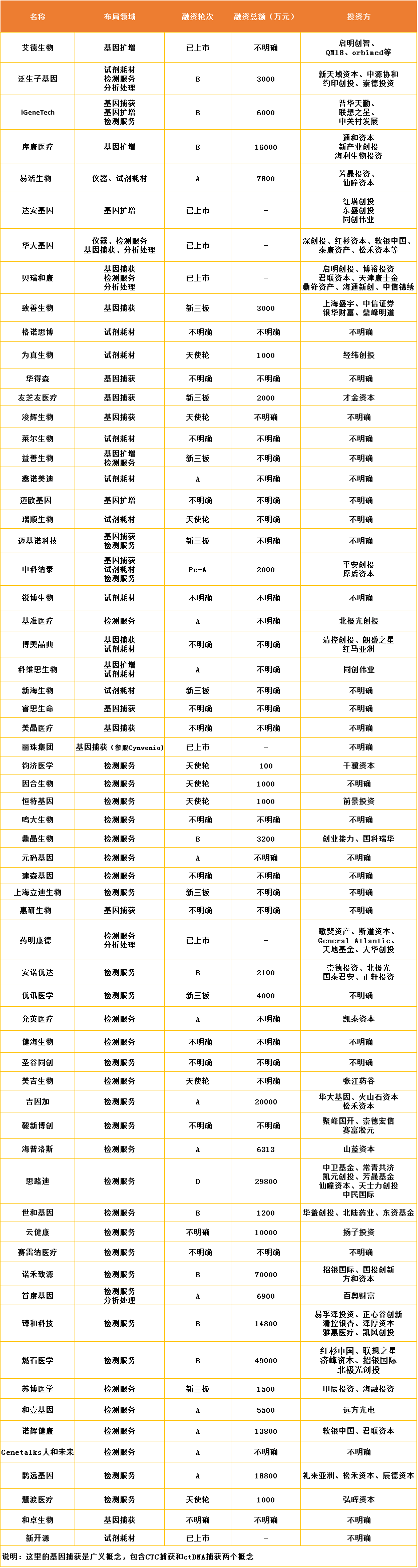

From the perspective of financing rounds, domestic companies involved in liquid biopsy can be divided into two categories. One category consists of listed companies and enterprises on the New Third Board that entered the field at a later stage; the other comprises startups predominantly founded by overseas-returnee teams.

There are seven listed companies with a presence in this sector. With the exception of BGI Genomics and Berry Oncology, nearly all other companies have entered the market through investment, acquisitions, or business expansion. AmoyDx is also developing two major product lines for companion diagnostic reagents based on PCR technology and next-generation sequencing (NGS) technology.

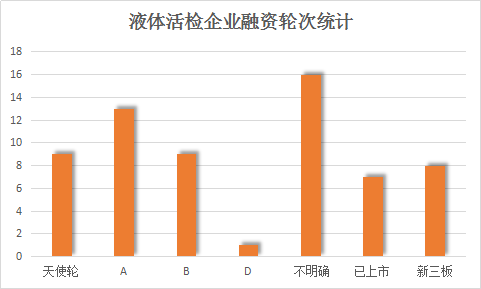

Most startups have already secured Series A or Series B funding. Among them, Burning Rock Biotech emerged as the company with the highest disclosed financing amount, raising RMB 490 million. (Novogene’s total financing reached RMB 700 million; however, since liquid biopsy represents only one segment of Novogene’s business portfolio, it is excluded from this comparison.)

Genetron Health, Genomics, Zhenhe Technology, and New Horizon Health have also secured substantial financing rounds, amounting to RMB 200 million, RMB 188 million, RMB 148 million, and RMB 276 million, respectively. Companies that have reached Series A generally raise funds in the tens of millions, often exceeding RMB 100 million.

Upstream Industry: Capture Technology Is the Core

The upstream industry comprises four components: capture, gene amplification, reagents and consumables, and sequencing instruments. As previously mentioned, capture and gene amplification are prerequisites for conducting the test.

Currently, liquid biopsy technologies can be mainly divided into two categories: one is ctDNA testing, and the other is TCT testing.

CTC detection is technically challenging, primarily because physical separation methods fail to isolate smaller tumor cells and are prone to contamination with impurities. Meanwhile, the immunoaffinity approach requires the identification of cell surface antigens to design more universally applicable antibodies. Consequently, CTC detection is severely constrained by cell capture technologies.

CellSearch Circulating Tumor Cell Detection System is a novel product developed by Johnson & Johnson for the enumeration and analysis of circulating tumor cells (CTCs). It is the first and only commercially available CTC detection product approved by both the FDA and CFDA for the management of malignant diseases.

However, due to significant limitations in its capture method and the inability to capture live cells for subsequent drug-guidance testing, the system was discontinued as early as 2016.

CellSearch’s capture technology is based on immunomagnetic affinity, which labels and magnetizes circulating tumor cells (CTCs) by binding antibodies to antigens specifically expressed on the tumor cell surface.

Other domestic applications of immune enrichment technology include Zhongke Natai’s Tumor Catcher and Geno Biotech’s Cytoplorare. Among them, Tumor Catcher is based on peptide-coated magnetic bead capture technology, while Cytoplorare utilizes folate antibodies and primarily targets lung cancer.

Another approach is the physical separation method, which achieves isolation of CTCs from normal cells by leveraging characteristics such as cell size, density, and charge polarity. Commonly used techniques include filtration, microfluidics, and electrode-based methods.

Yishan Biotech’s Canpatrol platform employs a filtration-based method that purifies circulating tumor cells (CTCs) by leveraging size differences between CTCs and normal cells through membrane filtration.

In 2016, BGI Genomics signed a strategic cooperation agreement with Singapore-based liquid biopsy company Clearbridge BioMedics to expand the promotion and application of its CTC enrichment and separation system, ClearCell® FX1, in China.

ClearCell® FX1 utilizes microfluidic technology. Zhuo Bio’s UniCyte Cell Capture Instrument is also based on microfluidic technology, enabling the capture of circulating cells present at concentrations as low as one part per million.

ctDNA Testing and Non-Invasive Prenatal Testing Share Similarities. ctDNA is primarily derived from apoptotic tumor cells. Depending on the clinical stage of cancer patients, the proportion of ctDNA in cell-free DNA (cfDNA) varies; therefore, ctDNA testing is widely used for early diagnosis of tumors and monitoring of recurrence.

Benefiting from advances in sequencing technology, circulating tumor DNA (ctDNA) analysis is poised to be the first liquid biopsy technique to reach clinical maturity. Currently, ctDNA research primarily follows two approaches: one directly obtains ctDNA sequence information using sequencing technologies, while the other employs DNA amplification techniques to quantify the concentration of ctDNA containing specific sequences.

The former requires capturing, isolating, and purifying specific sequences prior to sequencing; amplicon sequencing, in contrast, employs specific primers to perform multi-stage PCR on samples, followed by purification to obtain specific sequences for sequencing.

Both methods require prior completion of gene capture and amplification; however, most commercial capture kits rely on customization by foreign companies, such as Illumina, Life Technologies, and Agilent Technologies.

In 2015, AgiTech launched its independently developed and optimized TargetSeq, a solution-based chip capture method, and MultipSeq, a multiplex PCR targeted amplification method. These represent the two mainstream categories of genomic DNA targeted capture products currently available and are among the few “Made in China” offerings.

Midstream Sector: Channel Marketing and Sample Accumulation

The midstream segment, namely the testing services sector, is the component that directly faces the market. Distribution channels, technology, and sample accumulation are all indispensable. This segment hosts the largest number of companies, totaling 37. However, their business models vary: some capture market share through channel dominance, while others rely on extensive sample accumulation to achieve gradual yet substantial growth.

By establishing partnerships with institutions such as ZhongAn Insurance, Taikang Life, iKang Guobin, Peking Union Medical College Hospital, Zhejiang Cancer Hospital, and DXY, New Horizon Health has built a multi-dimensional distribution channel covering insurance, health checkups, hospitals, mobile healthcare, and even community centers, making it a typical channel-driven company.

In addition, companies such as Da An Gene and Youxun Medical have also secured resources through hospital channels, while Dian Diagnostics has established marketing channels across China by leveraging its network of laboratories. Although WuXi AppTec has not officially launched liquid biopsy products, it has been actively making strategic moves in the industry by capitalizing on the resources it has accumulated over many years in the pharmaceutical sector.

In 2015, HelixGene and Shenzhen People’s Hospital launched the Ten Thousand Genomes Project. Berry Genomics leveraged 400,000 Chinese female genomic data samples previously accumulated through its non-invasive prenatal testing market. Kexun Biology collaborated with multiple hospitals in China to establish a cancer mutation database for the Chinese population.

BGI Genomics has also invested heavily in this area. As early as 2014, BGI Genomics launched the “100,000-Person Oncology Research Initiative” and the “10,000-Person Oncology ‘Baseline’ Study.”

Of course, enterprises do not face a single-choice question when it comes to channel marketing versus sample accumulation. For instance, large-scale companies such as BGI Genomics, Berry Genomics, WuXi AppTec, and Daan Gene have actually made strategic layouts in both areas.

After launching the OncoEvo series in July 2015, Berry Genomics officially entered the field of tumor liquid biopsy, subsequently expanding its testing scope from initially focusing solely on non-small cell lung cancer to encompassing gynecologic and gastrointestinal cancers.

Years of dedication to the non-invasive prenatal testing (NIPT) sector have provided the company with channel advantages for its expansion into oncology. Leveraging its strengths in NIPT, Berry Genomics has established a hospital-centric testing network and forged partnerships with numerous leading medical institutions in China, including Peking University Cancer Hospital, Peking Union Medical College Hospital, and West China Hospital of Sichuan University.

In August 2015, Berry Genomics joined forces with Alibaba Cloud to launch the “Shenzhou Genetic Data Cloud” project, analyzing the massive volume of samples previously accumulated to facilitate precise interpretation of personal genomic data. Although no specific genomics initiative was launched, leveraging the channel advantages in their respective strategic domains, Phase I of the “Shenzhou Genetic Data Cloud” has already reached a sample size of 400,000, with Phase II expected to exceed one million samples.

Downstream Segment: Oncology Big Data and Analytics

Downstream processes refer to the analysis, processing, and interpretation of data following the sequencing step.

Both CTC and ctDNA testing require in-depth knowledge of cancer genomics to support data interpretation.

Benefiting from advances in sequencing technology, next-generation technologies have greatly enriched and supplemented our understanding of cancer genomics. Coupled with the increasing maturity of the liquid biopsy industry in recent years, our knowledge of the genetic information underlying cancer has continued to grow.

However, achieving more precise interpretation requires not only the integration of sequencing technologies and omics research but also relies on the accumulation of sequencing samples. This is why companies in the midstream sector devote significant efforts to building up their sample volumes.

Beyond oncology big data, WuXi AppTec and BGI Genomics approach the field from the perspective of tumor analysis and interpretation.

Shoudu Gene provides free database resources to a broad community of cancer genomics researchers through the China Cancer Cloud Platform, a public-welfare data platform.

WuXi AppTec established its subsidiary, WuXi NextCODE, following the acquisition of NextCODE. As an industry-leading company in genetic analysis and bioinformatics, NextCODE’s strong heritage has been preserved.

In June 2016, a collaboration agreement was signed with Fudan University to provide gene sequencing and data analysis services. During the same month, its subsidiary, BGI Bioinformatics (Mingma Biology), stood out among numerous competitors by providing cancer genome data analysis services for the UK National Genomics Programme. Additionally, Mingma Biology partnered with Huawei to develop a prominent precision medicine cloud platform, establishing itself as a leader in China’s bioinformatics cloud sector.

WuXi AppTec is not a pure-play genomics company; however, leveraging its expertise in bioinformatics and its internationally renowned reputation as a CRO, it has established strategic partnerships with prominent companies across multiple countries, entering the liquid biopsy industry from the downstream segment.

Starting from one’s core competencies and gradually delving into a new field may offer valuable insights for other companies with expansion plans.

Industry Landscape