Comprehensive Analysis of the Medical and Health Industry on China's NEEQ: 674 Companies Reviewed from 20 Perspectives

China’s healthcare industry is rooted in traditional pharmaceuticals and medical devices, extending into branches such as health management, wellness, rehabilitation and nursing care, and elderly care services. With technological advancements, the healthcare sector has increasingly intersected and integrated with next-generation information technologies represented by artificial intelligence, big data, and the Internet of Things (IoT). This convergence has given rise to new healthcare segments—including precision medicine, pharmaceutical e-commerce, mobile health, smart healthcare, and healthcare informatization—collectively forming a new healthcare ecosystem.

In 2016, China’s healthcare industry experienced rapid development. The issuance and implementation of the “Healthy China 2030” Planning Outline drove the industry’s scale to a rapid expansion, reaching RMB 3.2 trillion. Continuous breakthroughs in medical technology were accompanied by vigorous capital investment. With economic growth and the gradual onset of consumption upgrading, technological innovation became more extensively and deeply integrated with medical services, propelling the healthcare industry into a golden age of development in 2017.

The full name of the “Third Board” market is the “National Equities Exchange and Quotations,” which was officially launched on July 16, 2001.

Currently, the National Equities Exchange and Quotations (NEEQ) is no longer limited to unlisted joint-stock companies in the Zhongguancun Science Park; instead, it has become a national equity trading platform for unlisted joint-stock companies. It primarily serves innovative, entrepreneurial, and growing small, medium, and micro enterprises, thereby complementing the limitations of stock exchanges.

The primary differences between the NEEQ and the main board stock exchanges are as follows:

I. Different Target Clients. The New Third Board is primarily positioned to serve the development of innovative, entrepreneurial, and growing small, medium, and micro enterprises (SMMEs). These enterprises are generally small in scale and have not yet established stable profit models, but they represent the most dynamic segment of the corporate landscape.

II. Differences in Investor Base. The Main Board market is primarily composed of small and medium-sized investors, whereas the National Equities Exchange and Quotations (NEEQ) implements a stricter investor suitability regime with higher entry thresholds, resulting in an investor base dominated by institutional investors.

III. The “New Third Board” serves as an intermediary between micro, small, and medium-sized enterprises (MSMEs) and industrial capital, primarily providing services for corporate development, capital injection, and exit strategies, rather than focusing on trading activities.

Currently, the New Third Board primarily adopts two trading methods:

I. Agreement-based Trading Model: The buyer and seller negotiate with each other, and upon successful negotiation and confirmation of transaction details, the transfer is executed through the National Equities Exchange and Quotations (NEEQ) system via agreement-based transfer;

II. Market Maker Model: This model involves qualified legal entities with sufficient financial strength and credibility acting as market makers. They continuously provide bid and ask prices to investors, execute buy and sell orders at these quoted prices, and trade with investors using their own capital and securities, thereby providing immediacy and liquidity to the market.

Companies listed on the National Equities Exchange and Quotations (NEEQ) are representative of small and medium-sized innovative enterprises, characterized by their large number and diverse stages of development. This provides a robust sample for mapping the current state of healthcare enterprises through a systematic analysis of NEEQ-listed companies.

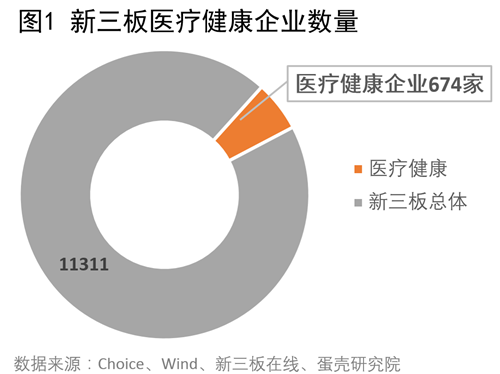

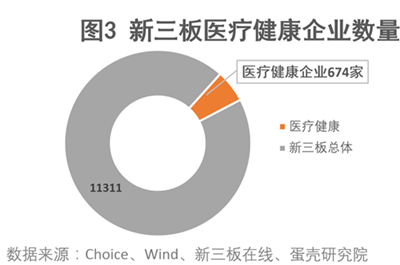

VCBeat·VBInsight, in accordance with the industry classification standards of the China Securities Regulatory Commission (CSRC), compiled a list of companies involved in healthcare (excluding those whose primary business is animal treatment). As of July 20, 2017, there were a total of 11,273 companies listed on the National Equities Exchange and Quotations (NEEQ) system, among which 674 were categorized under the healthcare concept, accounting for 5.97% of the total number of NEEQ-listed companies.

NEEQ-listed companies in the healthcare sector are building on traditional pharmaceuticals and medical devices to extend into emerging industry segments, including health management, wellness, rehabilitation and nursing care, and elderly care services.

With the advancement of technology, healthcare has become increasingly intertwined and integrated with next-generation information technologies represented by artificial intelligence, big data, and the Internet of Things. This convergence has given rise to new forms of health industry, including precision medicine, pharmaceutical e-commerce, mobile health, smart healthcare, and healthcare informatization, which together constitute a new healthcare system.

As of July 20, 2017 (hereinafter the same), there were a total of 11,273 companies listed on the National Equities Exchange and Quotations (NEEQ), among which 674 were in the healthcare sector, accounting for 5.97% of the total number of NEEQ-listed companies.

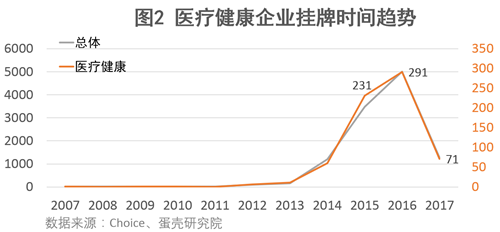

Driven by healthcare industrial policies and favorable listing regulations, the number of listed companies in the healthcare sector has experienced explosive growth since 2015. As of July 20, 2017, the number of listed entities had increased by 331.82% compared to 2014, with the total number of healthcare enterprises expected to surpass 1,000 this year.

Most healthcare-related companies are innovative technology enterprises with generally good liquidity.

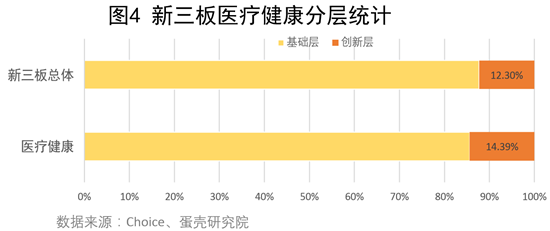

Stratification Status:Since the end of 2015, the China Securities Regulatory Commission (CSRC) has classified companies listed on the National Equities Exchange and Quotations (NEEQ) into the Base Tier and the Innovation Tier, establishing tiered criteria to allocate relatively higher-quality enterprises to the Innovation Tier.

The tiered system has led to a concentration of market resources in the Innovation Tier, meaning that companies listed in this tier can enjoy greater convenience and priority access to services. They also attract more market attention in terms of corporate branding, strategic development, and financing capabilities, thereby achieving better growth.

The number of healthcare concept companies in the Innovation Tier stands at 80, accounting for 14.39% of all healthcare concept companies and 6.97% of the total number of companies in the NEEQ Innovation Tier. Meanwhile, companies in the NEEQ Innovation Tier represent 12.30% of the total number of listed companies on the National Equities Exchange and Quotations (NEEQ).

Polarization of Income: Most Companies Struggle on the Brink of Profit and Loss

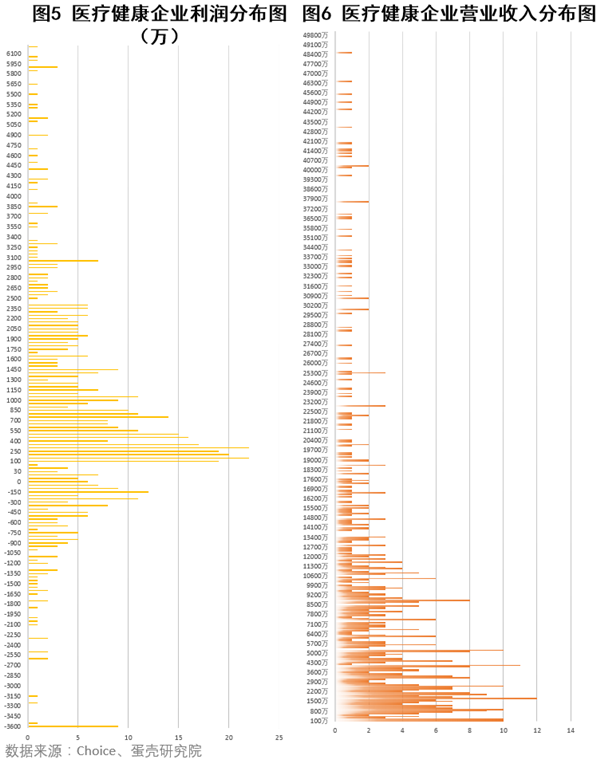

As of July 20, 2017, 658 healthcare companies had disclosed their 2016 annual reports. The average annual operating revenue for 2016 was RMB 120.0258 million, with 27 companies reporting revenues exceeding RMB 500 million. The average net profit attributable to shareholders of the parent company was RMB 12.8943 million, and 10 companies reported net profits attributable to shareholders of the parent company exceeding RMB 100 million.

We plotted the distribution charts of operating revenue and net profit attributable to parent company shareholders for healthcare companies listed on the National Equities Exchange and Quotations (NEEQ) (see Figures 5 and 6).

Currently, the revenues of healthcare companies listed on the New Third Board are concentrated in the range of RMB 1 million to RMB 90 million. A few companies with outstanding performance have pushed the overall average revenue up to RMB 120.0258 million. The distribution of average net profit for these companies is clustered around the break-even point, indicating generally low profitability.

The inclusivity of the NEEQ has attracted companies at various stages of development, with a predominance of growth-stage enterprises. Consequently, the financial data of revenue giants stand out prominently, rendering average figures less reference-worthy in certain contexts.

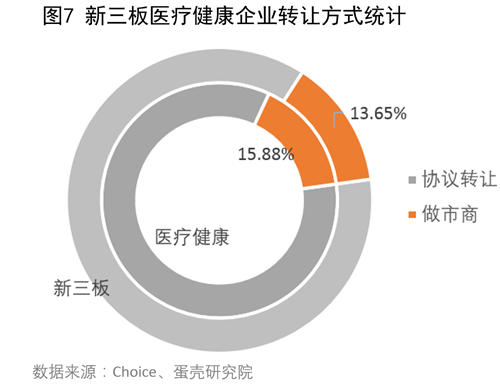

Favored by market makers, with good liquidity

There are 107 healthcare-themed companies adopting the market-making transfer method on the National Equities Exchange and Quotations (NEEQ), accounting for 6.89% of all NEEQ companies under market-making transfer and 15.88% of all NEEQ healthcare-themed companies.Higher than the average of 13.65% for market-making transfers on the NEEQ. This further demonstrates that listed healthcare companies exhibit strong technological innovation capabilities and higher overall liquidity.

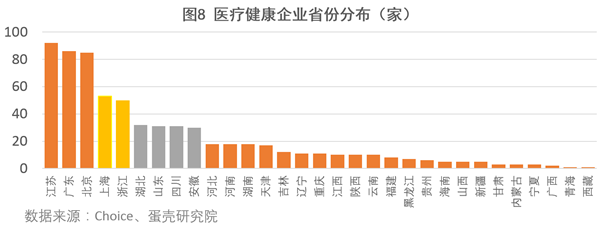

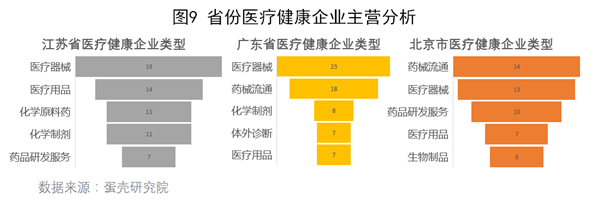

# Ranking First in Jiangsu Province, Leading the Yangtze River Delta

Most healthcare-focused companies are concentrated in economically developed regions, with the Yangtze River Delta having the largest number of such enterprises.

In terms of provincial distribution, Jiangsu Province leads China with 96 healthcare-related companies listed on the National Equities Exchange and Quotations (NEEQ) system. Beijing and Guangdong follow closely, each with 85 such companies, while Shanghai ranks fourth with 65 enterprises.

An analysis of the core business activities of healthcare enterprises in Jiangsu Province, Guangdong Province, and Beijing reveals that their primary operational focuses exhibit strong regional characteristics.

As the industrial foundation of the Yangtze River Delta region, Jiangsu Province boasts a relatively complete supporting supply chain for light industry. The healthcare sector in Jiangsu is predominantly composed of manufacturing enterprises specializing in medical devices, medical supplies, and active pharmaceutical ingredient (API) production.

Medical and health supplies form the foundation of the entire healthcare industry, characterized by high technological content and substantial demand. Thanks to its well-developed industrial chain resources, Jiangsu Province has become a hub for medical and health manufacturing enterprises, ranking as the leading province in China for such companies listed on the National Equities Exchange and Quotations (NEEQ).

Guangdong Province accounts for nearly the entire Pearl River Delta economic belt. Like Jiangsu Province, it boasts abundant resources across the pharmaceutical industry chain, making various medical device manufacturers the most significant component of Guangdong’s healthcare enterprises.

Guangzhou and Shenzhen, with their respective strengths in trade and innovation, have contributed to a higher proportion of local pharmaceutical and medical device distribution and R&D enterprises in Guangdong Province compared to Jiangsu Province.

Beijing, the nation’s scientific and technological hub, boasts abundant academic resources, with pharmaceutical R&D and biologics emerging as key industries. Meanwhile, its unique geographic advantages have attracted a large cluster of pharmaceutical and medical device distribution enterprises.

Through an analysis of the types of healthcare enterprises in the aforementioned three provinces and municipalities, it is evident that regional locational advantages and corporate development are mutually reinforcing, and a well-developed industrial chain can inject greater vitality into related enterprises.

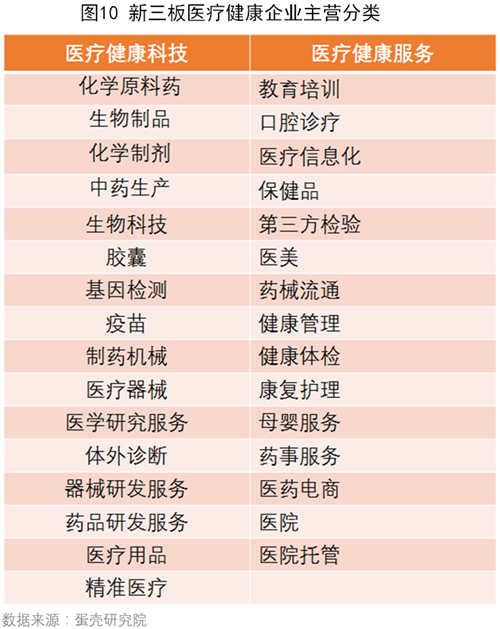

Drawing on the industry classification standards of the China Securities Regulatory Commission (CSRC) and leveraging our expertise in the healthcare sector, we categorize healthcare enterprises into two major segments—Healthcare Technology and Healthcare Services—comprising 31 subcategories. This framework aims to assess the development of companies across various healthcare subsectors through the dual lenses of technology and services.

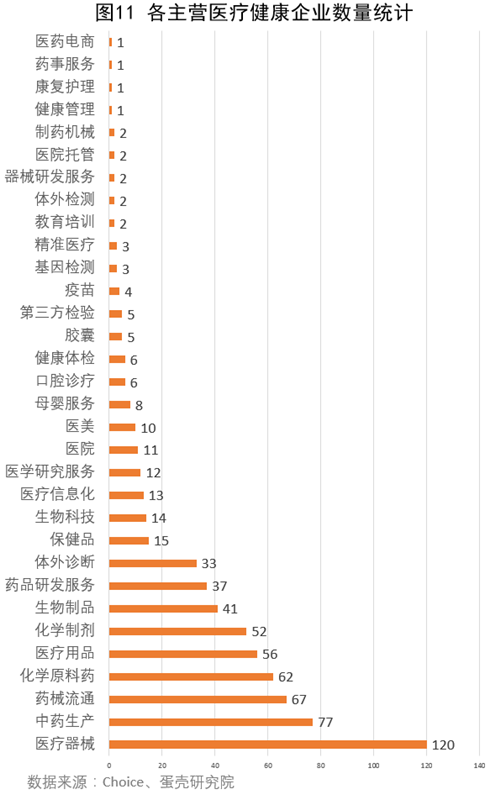

In terms of the number of enterprises, traditional manufacturers and distributors of medical-related products firmly occupy the first tier among healthcare companies listed on the New Third Board.

The number of technology-driven enterprises, represented by in vitro diagnostics and biotechnology, which have developed alongside technological advancements, as well as new types of medical service providers, represented by dental care and medical aesthetics, which have grown with consumption upgrades, has reached the second tier.

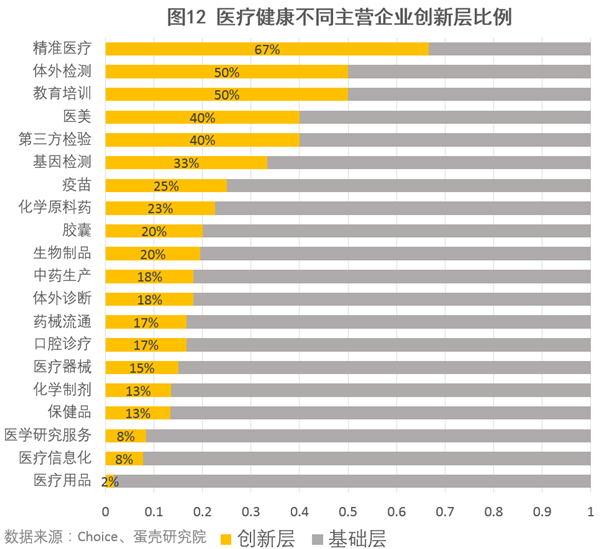

More encouragingly, over 50% of the emerging innovative enterprises that have grown alongside technological advancements and the consumer boom have entered the Innovation Tier of the National Equities Exchange and Quotations (NEEQ).

Currently, among healthcare enterprises across various sectors, those in the innovation tier that rank highest are predominantly concentrated in niche areas such as precision medicine, in vitro diagnostics (IVD), and education and training, which have emerged due to technological advancements and service upgrades. This indicates that the healthcare sector is undergoing innovation and transformation beyond its traditional models.

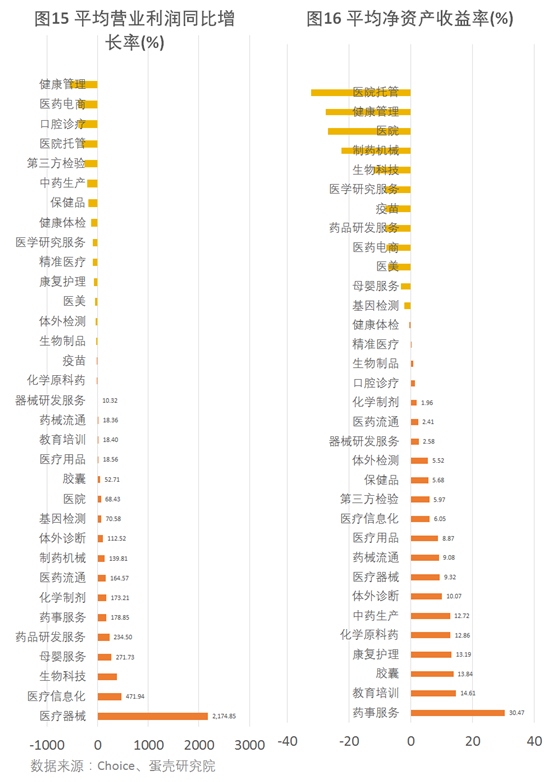

The four charts above illustrate the current development stages of various sub-sectors within the healthcare industry.

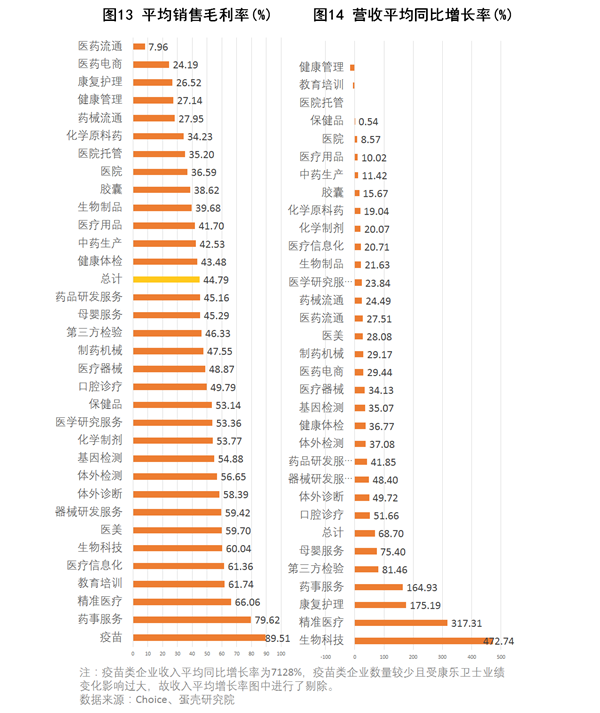

Traditional medical supply sectors, represented by active pharmaceutical ingredients (APIs), traditional Chinese medicine (TCM) production, and the distribution of pharmaceuticals and medical devices, have entered a stage of perfect competition. While the industry foundation is solid and early investments are beginning to yield returns, gross profit margins on sales remain low, with manufacturers competing fiercely within the existing market.

Emerging healthcare service companies, represented by those in health management, third-party laboratory testing, health check-ups, and medical aesthetics, are currently in the market expansion phase. Although these emerging services boast high gross margins, typical strategies for such companies during this period of rapid industry growth involve continuous investment and swift expansion.

Technology-driven healthcare companies, represented by those in the vaccine and precision medicine sectors, have entered a period of rapid growth. Breakthroughs in life sciences have enabled these enterprises to achieve high gross profit margins on sales, allowing them to recoup their initial investments. Consequently, this category of companies has reached an explosive phase of industry expansion characterized by high growth and high output.

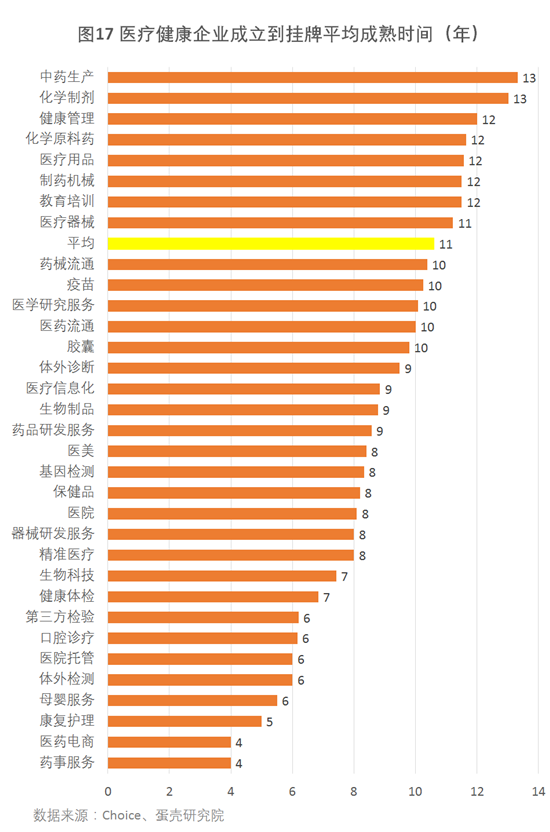

Accelerated Maturation of Companies in Emerging Business Sectors

Regarding the corporate maturity cycle, we measured this metric by calculating the time elapsed from establishment to listing for all healthcare companies. The average maturity cycle for healthcare companies listed on the NEEQ (New Third Board) is 10.6 years. Emerging technology and medical service enterprises demonstrate a trend of rapid development and maturation, with the time from establishment to listing being significantly shorter than the industry average.

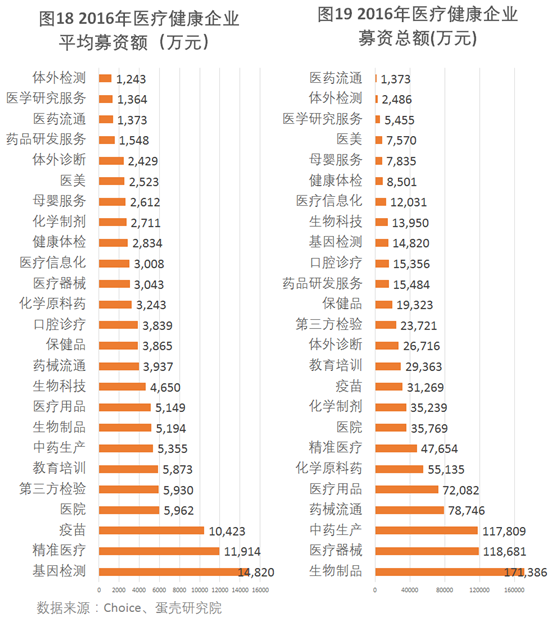

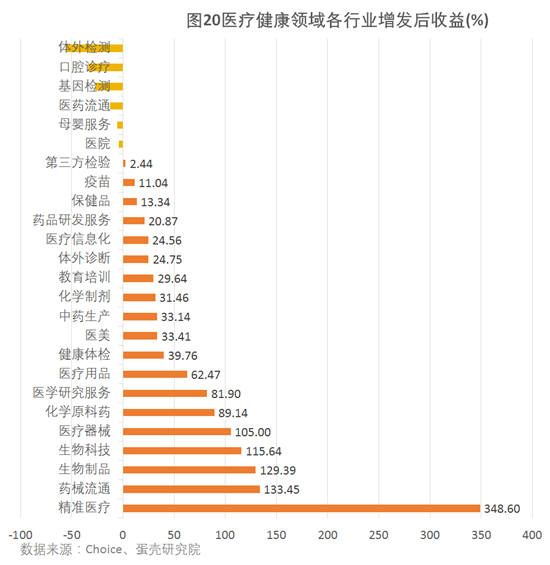

Due to liquidity issues on the NEEQ, corporate market capitalizations have not been effectively priced by the market. Therefore, we assess the degree of investor favor from another perspective—financing capability—to indirectly reflect the development status of enterprises in this industry.

In 2016, companies listed on the healthcare sector of the National Equities Exchange and Quotations (NEEQ) carried out a cumulative total of 234 private placements, raising RMB 9.677 billion in total financing. The financing efficiency was relatively high, ranking first among all sectors.

This indicates a high level of confidence among investors in the healthcare industry. Investors participating through private placements are generally more optimistic about the long-term development of enterprises compared to ordinary investors, reflecting broad market consensus and positive outlook for healthcare companies.

Capital markets are astute; the development trajectory of an industry typically undergoesThe nascent stage of technology, policy promotion, breakthroughs in technological commercialization, and the stage of consumer adoption, before finally entering the period of value stabilization.

As mentioned in the previous chapter, healthcare technology companies in a period of rapid industry expansion have received frenzied capital investment. Although they do not dominate in terms of the number of enterprises, healthcare technology firms rank among the top in both total financing amount and average deal size, yielding substantial returns for investors. It is believed that over the next two years, capital will continue to drive the advancement of the healthcare industry, represented by healthcare technology, until it reaches a stage of stable value under perfect competition.

Although emerging healthcare service companies are developing at a slightly slower pace than health tech enterprises, industry investments have begun to yield initial results. Capital is already positioning itself in this sector; although the competitive intensity may escalate more gradually, please be patient and allow time for these strategic moves to unfold.

Currently, healthcare technology companies, represented by those specializing in precision medicine and in vitro diagnostics, have moved past the phase of technological monopoly dominated by a few oligarchs. Through technological advancements, these companies have achieved significant breakthroughs in their respective fields, and the market has entered a stage of perfect competition.

With the advent of consumption upgrades, healthcare service enterprises have seen the emergence of new business models, including dental clinics, postpartum care centers, hospital management outsourcing, and third-party medical centers. As demand for follow-up medical services surges, these enterprises will overcome the challenges of high expansion costs and stagnant gross margins through standardized, assembly-line replication.

Gross profit margin often reflects a company’s industry standing with its upstream and downstream partners, as well as the premium derived from its brand and technology, serving as a key indicator for evaluating a company’s product and service capabilities.

In the preceding section, we compiled statistics on the gross profit margins of various sectors within the healthcare industry to characterize their industry-specific features.

Whether for investment or entrepreneurship, our focus lies on specific companies. Next, we will use gross profit margin as the primary metric to identify highly competitive enterprises within each niche sector for your reference.

The above constitutes the complete content of this report. To download the PDF version, please scan the QR code below.

This is a research report on healthcare companies listed on the New Third Board, titled “Capital’s Choice: A Review of the Healthcare Industry on the New Third Board.” Taking an overview of these companies as its starting point, the report examines the current state of the industry and follows the trail of capital to identify development trends in the healthcare sector.

Scan the QR code below to becomeVCBeat Official Member, you can obtainPDF Version《Capital’s Choice: A Review of the Healthcare Industry on the New Third Board》. And, in the coming year, you will have unlimited access to the completeIndustry Trend Report, timely grasp the latest globalInvestment and Financing Information, boasting a comprehensiveMedical Enterprise Database, and alsoMassive Resource Matching。

Scan the code to become a VCBeat member,

Beta Version Trial Price: 365 yuan/year.