2017 Interim Reports of Medical Imaging Giants GE, Philips, and Siemens: Two Thriving, One Struggling

In late July, GE and Philips successively announced their Q2 financial reports. Coupled with Siemens’ semi-annual results released in May, the 2017 half-year financial reports of the “GPS” trio in the medical sector (GE, Philips, and Siemens) were all unveiled. The published data revealed a mixed performance: two companies posted gains while one faced challenges.

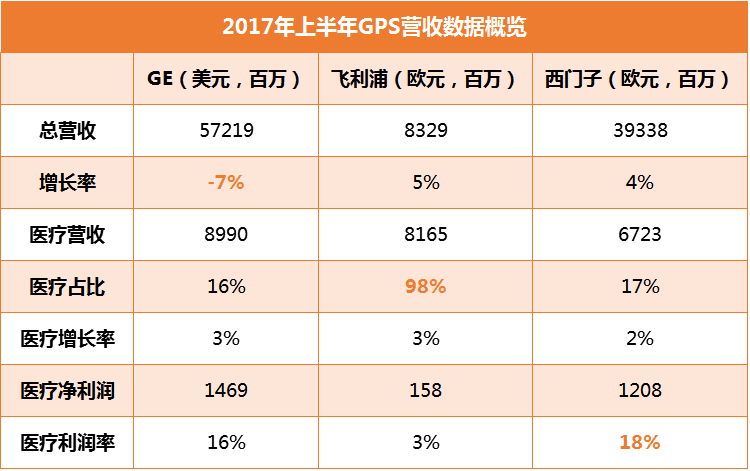

In the first half of 2017, in terms of total group revenue, GE ranked first, Siemens second, and Philips third. However, in the healthcare sector, GE remained in first place, Philips surged to second, and Siemens fell to third.

Although GE ranked first in overall revenue, its growth rate was negative. In particular, after the release of its second-quarter financial report, GE’s stock price fell by nearly 3% on the same day.

Although Philips’ overall revenue is far lower than that of GE and Siemens, its healthcare business now accounts for 98% of total revenue, with a growth rate of 5%, the highest among the three. This is primarily because Philips began gradually divesting its lighting business in 2016, operating it as an independent entity, and the Q2 2017 financial report no longer includes data from the lighting segment.

Siemens has maintained relatively stable development, ranking second in total revenue and achieving a 4% growth rate. In its healthcare business, the profit margin reached as high as 18%, the highest among the three companies.

Below, VCBeat (WeChat ID: vcbeat) will provide readers with an interpretation of the semi-annual reports from the three giants—GE, Philips, and Siemens—and list the major news events involving these three companies during the first half of the year.

On July 24, 2017, GE released its Q2 financial report, and its stock price immediately dropped by nearly 3% on the day of the announcement. Meanwhile, GE’s first-half financial results were also freshly released. In the first half of 2017, GE reported revenue of $57.2 billion, the highest among the three GPS companies, but its growth rate was negative (-7%). The primary reason was that GE’s Energy Connections business performed poorly in the first half of the year, offsetting the growth advantages of its renewable energy and power businesses.

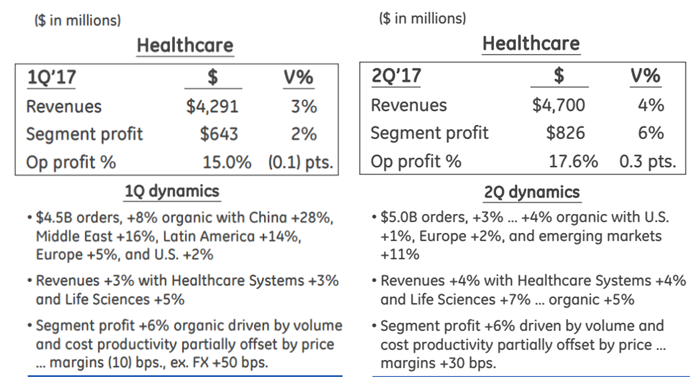

GE 2017 Q1 & Q2 Healthcare Revenue Data

In the healthcare segment, GE’s healthcare revenue in the first half of the year amounted to $8.99 billion, accounting for approximately 16% of its total revenue during the same period. Revenue maintained steady growth in both quarters: $4.29 billion in the first quarter, representing a 3% increase, and $4.7 billion in the second quarter, reflecting a 4% increase. Significant revenue growth was observed in both the Healthcare Systems and Life Sciences sectors during the first half of the year.

GE Healthcare’s profit growth in the first half of the year was driven by an increase in order volume and productivity. Orders in emerging markets, particularly in Latin America, the Middle East, and China, continued to grow steadily. However, the growth rate slowed significantly in the second quarter, dropping sharply from 48% in the first quarter to 11%.

GE: Key Events in the First Half of 2017

On March 13, 2017, GE Healthcare expanded its maternal and infant health business by acquiring the UK-based company Monica Healthcare. Monica Healthcare, a privately held enterprise with 12 years of history, is dedicated to improving birth experiences and enhancing the standardization of obstetric care through wearable wireless fetal monitoring devices.

On April 10, 2017, GE Healthcare and CBMG (Cellular Biomedicine Group) announced a strategic partnership. The two parties will establish a joint laboratory at CBMG’s newly built GMP manufacturing facility in Zhangjiang, Shanghai, to jointly develop high-quality industrial manufacturing processes for chimeric antigen receptor T cells (CAR-T cells) and stem cells, aiming to co-develop a highly integrated and automated cell therapy manufacturing system.

On June 12, 2017, GE announced the appointment of Kieran Murphy as its next Chairman and CEO. Currently serving as President and CEO of GE Healthcare Life Sciences, Murphy will officially assume the role of CEO of GE Group on August 1, and will take over the Chairmanship on January 1 of the following year.

On July 20, 2017, GE Healthcare acquired Novia Strategies to expand its clinical consulting capabilities and help more healthcare institutions achieve breakthrough results.

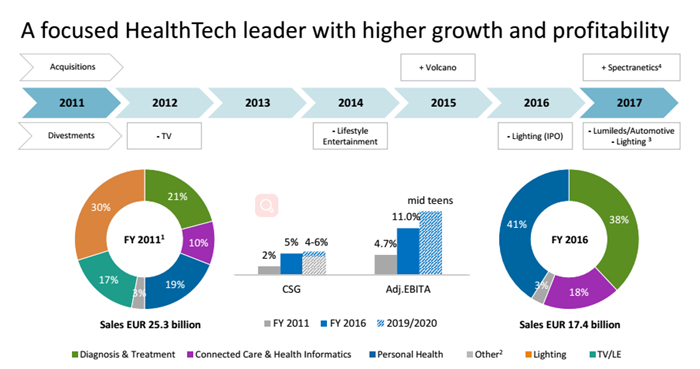

Among the “GPS” trio, Philips is the most healthcare-focused company, having successively divested its non-healthcare businesses. In February 2016, the company announced the spin-off of its lighting business, which was separately listed in May of the same year. At that time, Philips still held a 71.225% stake in the lighting business; however, following the release of its second-quarter 2017 financial results, Philips’ shareholding in the lighting business had been reduced to 41%.

Philips' Business Landscape Changes from 2011 to 2017

Following Philips’ divestiture of its lighting business, the revenue reported in its Q2 2017 financial statements comprised only four major segments: Diagnosis and Treatment, Connected Care and Health Informatics, Personal Health, and Others. Consequently, Philips’ total revenue for the first half of the year declined significantly, amounting to just €8.329 billion (while Philips Lighting recorded sales of €26.7 billion in the same period).

Although Philips Healthcare’s overall profit margin in the first half of the year lagged significantly behind those of GE and Siemens, its healthcare business accounted for 98% of total revenue and maintained a 5% growth rate, the fastest among the “GPS” trio.

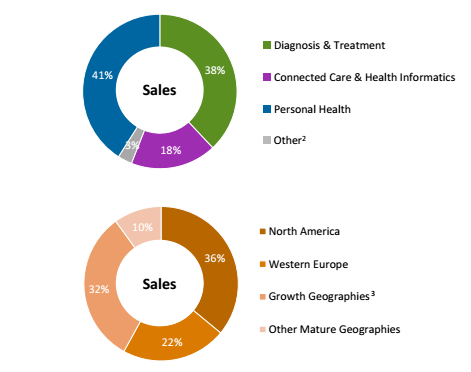

Philips Q2 2017 Financial Report: Sales Distribution Chart (by Business & Region)

This growth rate was primarily driven by a 6% increase in Philips’ Personal Health business. Additionally, the Connected Care & Health Informatics segment grew by 3%, while the Diagnosis & Treatment segment rose by 5%. This suggests that, following its transformation, Philips’ largest revenue stream may now come from consumer-facing (C-end) customers.

In the first half of the year, Philips’ order volume experienced single-digit growth, primarily driven by its Diagnosis and Treatment, Connected Care, and Healthcare Informatics businesses. This growth was largely attributable to the China and Latin America regions, where expansion was quite rapid. While Western Europe and North America also saw growth, it was modest, remaining in the single digits. However, a significant decline in business performance in Africa and India offset Philips’ overall growth during the first half of the year.

Philips: Key Events in the First Half of 2017

On February 27, 2017, Philips partnered with the German startup Onelife Health to expand its digital health services in the field of maternal and child healthcare.

On May 22, 2017, Philips expanded its sleep and respiratory care business by acquiring the U.S.-based company RespirTech. RespirTech is an American respiratory technology company that primarily provides innovative airway clearance solutions for patients with chronic respiratory diseases, such as chronic obstructive pulmonary disease (COPD) and cystic fibrosis. The combination of Philips’ leading respiratory care product portfolio with RespirTech’s respiratory disease treatment solutions will further strengthen Philips’ market position in delivering care management across both hospital and home settings.

On June 1, 2017, Philips partnered with Illumina and Navican to accelerate the integration of precision medicine into global healthcare systems. The new solution will leverage Navican’s TheraMap Precision Cancer Care™ service and the Philips IntelliSpace Genomics platform to integrate large-scale genomic analysis with comprehensive contextual clinical patient data. The Philips platform seamlessly incorporates Illumina’s next-generation sequencing technology.

On June 28, 2017, Philips acquired Spectranetics for €1.9 billion to accelerate the expansion of its image-guided therapy devices for treating cardiac and peripheral vascular diseases. Philips holds a leading position in the €6 billion image-guided therapy market, with a unique portfolio of interventional imaging systems and devices, as well as navigation software and services.

Spectranetics is a leader in vascular interventions for the treatment of coronary and peripheral artery disease, and the premier provider of tools for the minimally invasive removal of leads from implanted cardiac pacemakers and implantable cardioverter-defibrillators (ICDs), with annual sales ranging from $293 million to $360 million. The acquisition of Spectranetics will further expand Philips’ Image-Guided Therapy business group.

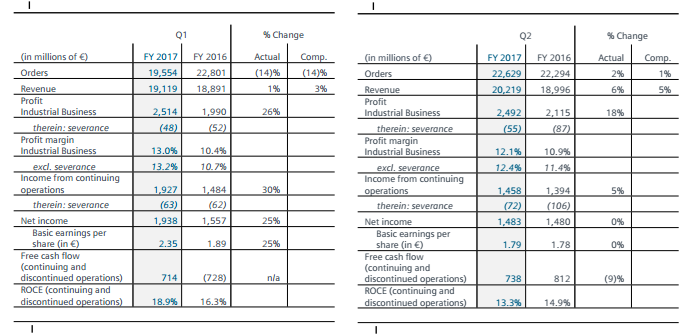

Siemens’ total revenue in the second quarter of 2017 reached €20.2 billion, representing a 6% increase compared with the second quarter of fiscal year 2016. Combined with the first-quarter revenue of €19.1 billion, Siemens’ total revenue for the first half of 2017 amounted to €39.3 billion, reflecting a 4% growth in revenue.

In the healthcare business, Siemens achieved an overall industry-leading commercial profit margin of 18%, ranking first among the “GPS” trio.

Siemens Q1 & Q2 2017 Data

Since May 2016, when Siemens announced the spin-off of its healthcare division and its rebranding as Siemens Healthineers, this decision has been implemented as part of Siemens’ 2010–2020 strategic development plan. Siemens Healthineers operates as an independently managed company under the Siemens umbrella.

In November 2016, Siemens announced plans to spin off Healthineers as an independent publicly traded company, with a business scale approaching $15 billion; Siemens’ stock price rose by 4.6% on the day of the announcement.

On August 3, 2017, Siemens released its second-quarter financial results and officially announced that it would spin off Siemens Healthineers for an initial public offering (IPO) in the first half of 2018. At that time, Siemens Healthineers was valued at €40 billion (approximately RMB 319.1 billion).

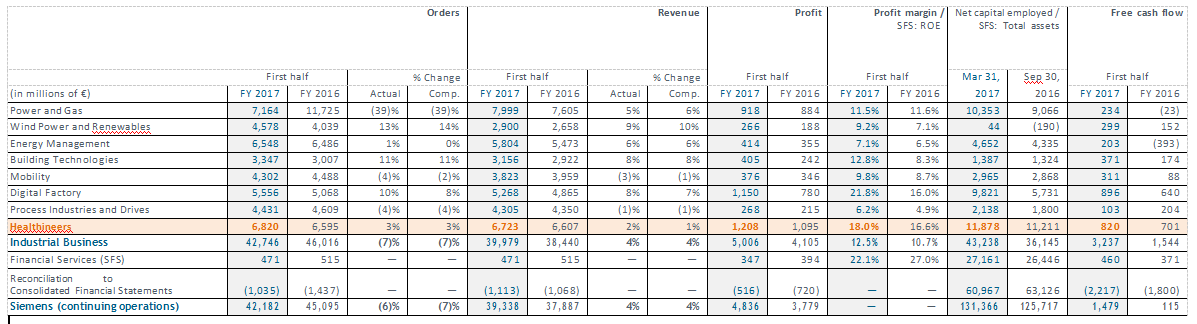

Revenue Data of Siemens' Various Divisions in the First Half of 2017 (Orange Represents Siemens Healthineers)

In the first half of 2017, Siemens Healthineers reported revenue of €6.72 billion, accounting for 17% of the group’s total revenue, which was roughly equivalent to GE Healthcare’s share (16%) within its parent company.

Orders across all business segments of Siemens Healthineers have grown, primarily driven by its two core divisions—Diagnostic Imaging and Advanced Therapies—with China in particular achieving double-digit growth. Revenue has also increased across all businesses, with the most significant growth seen in Diagnostic Imaging, concentrated mainly in Asia and Australia.

Siemens: Key Events in the First Half of 2017

At the end of the second quarter of fiscal year 2017, Siemens acquired all shares of Mentor Graphics. At the beginning of the third quarter, Siemens completed the merger of its wind power business with Gamesa.

In its healthcare business, on July 21, 2017, Siemens Healthineers entered into an agreement to acquire Epocal, a subsidiary of Alere, to enrich its blood gas product portfolio. Epocal is dedicated to developing and providing point-of-care testing (POCT) blood diagnostic systems, including the epoc® Blood Analysis System and handheld wireless testing solutions. However, this transaction was contingent upon Abbott’s completion of the acquisition of Alere, as well as obtaining antitrust approvals and fulfilling other customary closing conditions.