Pharmaceutical Terminal Market Growth Slows as Retail Pharmacies Emerge as a Rising Force

“Unbridled growth is no longer sustainable; compliance, innovation, and adaptation to the new ecosystem will be the key to survival for future enterprises.” At the 2017 Xipu Conference held recently, Wu Han, President of Sinohealth Information, pointed out that as healthcare reform enters its deep-water zone, and following China’s accession to the ICH (International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use) and the implementation of DRGs (Diagnosis-Related Groups), pharmaceutical companies will face greater challenges.

VCBeat (WeChat ID: vcbeat) has learned that the total size of China’s pharmaceutical terminal market (excluding medicinal herbs) reached RMB 1.4909 trillion in 2016, a year-on-year increase of 8.2%, with the projected growth rate for 2017 expected to decline to 5.8%. Comprehensive reform measures—including the expansion of zero-markup policies, healthcare insurance cost containment, price reductions through drug tendering, centralized procurement and negotiation, and healthcare insurance price negotiations—are the primary factors constraining continued high growth in pharmaceutical sales.

Growth Rate to Rationalize, Likely Stabilizing with a Moderate Decline

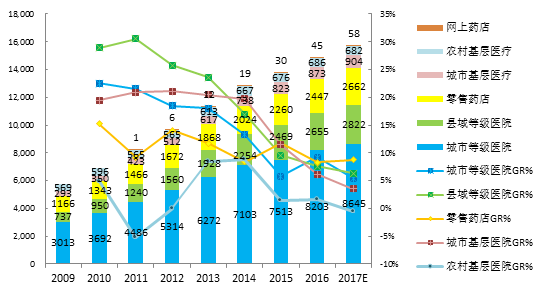

Since its inception in 2007 and through to the current critical phase, China’s new healthcare reform has had an increasingly prominent impact on the pharmaceutical and health industries after a decade of exploration and practice. During the initial stage characterized by “strengthening primary care and increasing investment,” the industry benefited from policy dividends, achieving annual growth rates exceeding 17% for five consecutive years, with a peak of 20% in 2010. As the reform entered the stage of “cost control and efficiency improvement,” systematic and multi-dimensional new policies have caused the industry’s growth rate to fall consistently into single digits since 2015. According to monitoring data from Zhongkang CMH, the market size of drugs across six major terminals grew from RMB 483.5 billion in 2008 to RMB 1.4909 trillion in 2016, representing a compound annual growth rate (CAGR) of 15.1%.

Figure 1 Overall Market Size (in RMB 100 million) and Growth of Pharmaceuticals

Improving drug quality, reducing drug prices, and curbing drug abuse will be the main themes of future industry policy guidance, with the growth rate of the pharmaceutical industry likely to stabilize and decline. It is estimated that in 2017, China's pharmaceutical market size will reach 1.5773 trillion yuan, a 5.8% increase from 2016, indicating a slowing growth rate. In the future, as key policies of the new healthcare reform are further implemented, technological innovation becomes fully integrated, commercial insurance strengthens, and cross-industry integration accelerates, industrial dominance will shift towards consumers, fostering a dual-market structure of basic healthcare and health consumption; the growth pole of the health industry will gradually transition from products to services; and a supply chain structure combining specialized division of labor and systematic service will gradually take shape.

City-level Hospitals Maintain a Dominant Share of the Pharmaceutical Terminal Market

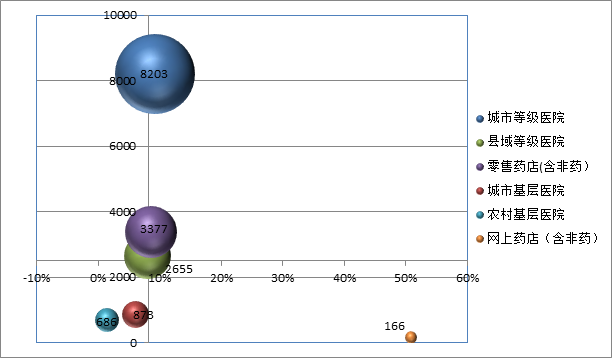

Figure 2. Market Share (in RMB 100 million) and Growth Rate of the Six Major Terminals in China's Pharmaceutical Market, 2016

Note: Bubble size represents share

According to research data from Zhongkang CMH, in terms of market share across six major terminal channels in 2016, urban tertiary hospitals accounted for 55.0% of the entire pharmaceutical market; county-level tertiary hospitals accounted for 17.8%; urban primary healthcare institutions and rural primary healthcare institutions each accounted for less than 6.0%; retail pharmacies accounted for 16.4%; and online pharmacies accounted for only 0.3%.

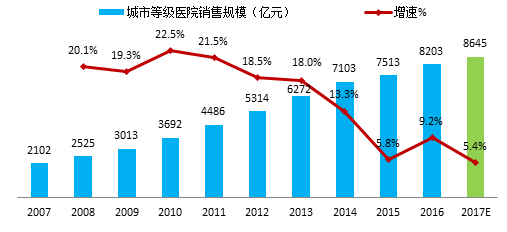

Figure 3 Market Size (in RMB 100 million) and Growth of Urban Hospitals by Tier, 2007–2017

Classified hospitals accounted for 87.9% of the total drug sales volume across all hospital terminals, and they will remain the largest pharmaceutical terminal in the future. Among them, urban classified hospitals continue to hold an unshakable position as the primary pharmaceutical terminal: in 2016, the market size of drug sales in urban classified hospitals reached RMB 820.3 billion, a year-on-year increase of 9.2%.

Although the new healthcare reform aims to reallocate medical resources and effectively divert patients from overcrowded tertiary hospitals to primary care institutions through measures such as tiered diagnosis and treatment, reforms in classified hospitals have not yet been fully implemented, and patients’ healthcare-seeking habits remain deeply entrenched. According to data from the National Health and Family Planning Commission, from January to April 2017, the number of hospital visits reached 1.06 billion, a year-on-year increase of 3.0%. Among these, visits to tertiary hospitals surged by 5.4%, far exceeding the national average growth rate of 1.0%. In contrast, patient visits to primary care institutions grew slowly or declined slightly, with outpatient visits at township health centers decreasing by 2.7% year on year.

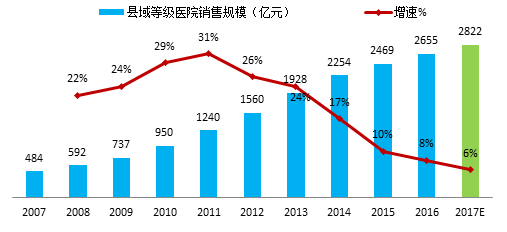

Figure 4 Market Size (in RMB 100 million) and Growth of County-Level Tiered Hospitals, 2007–2017

In 2016, the market size of pharmaceutical sales in county-level tiered hospitals reached RMB 265.5 billion, representing a year-on-year increase of 7.5% and a compound annual growth rate (CAGR) of 20.8%. The rapid expansion of this market in recent years was primarily driven by increased patient demand resulting from the expanded coverage and higher funding levels of the New Rural Cooperative Medical Scheme (NRCMS), as well as changes in medication patterns due to the penetration of branded drugs into lower-tier markets. With NRCMS coverage already reaching 95%, leaving limited room for further expansion, and the widening implementation of zero-markup drug policies, the high-speed growth of the county-level tiered hospital market has begun to slow down. It is projected to grow by 6.3% in 2017, with the market size reaching RMB 282.2 billion.

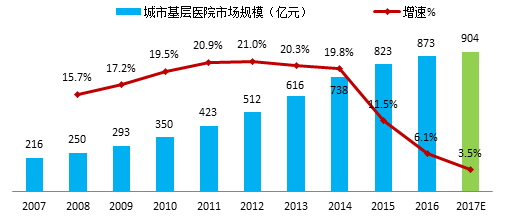

Figure 5 Market Size (in RMB 100 million) and Growth of Urban Primary Hospitals, 2007–2017

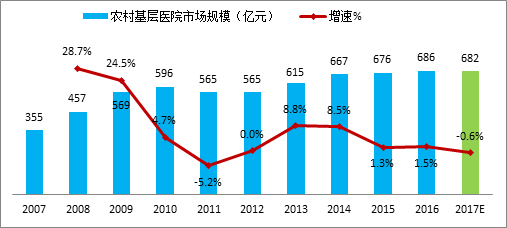

Figure 6 Market Size (in RMB 100 Million) and Growth of Rural Primary Hospitals, 2007–2017

At the primary care level, driven by policies under the new healthcare reform—such as the promotion of tiered diagnosis and treatment, first-contact care at primary institutions to foster the development of primary healthcare, and the New Rural Cooperative Medical Scheme (NRCMS) enhancing residents’ payment capacity—the primary healthcare market experienced a brief period of growth. However, due to the strengthening of public health service functions at primary care institutions and changes in performance assessment methods, the volume of primary medical services has returned to a state of moderate growth. Data from the National Health and Family Planning Commission (NHFPC) shows that from January to April 2017, primary medical and health institutions recorded 1.42 billion patient visits, a year-on-year decrease of 0.7%, and 13.319 million discharges, a year-on-year decrease of 1.6%. Although there have been favorable factors such as a slight relaxation of restrictions on the use of non-essential medicines in some regions, the overall growth of the primary pharmaceutical market has tended to stabilize. Future growth in the primary healthcare market will mainly benefit from the comprehensive implementation of the Medical Consortium model.

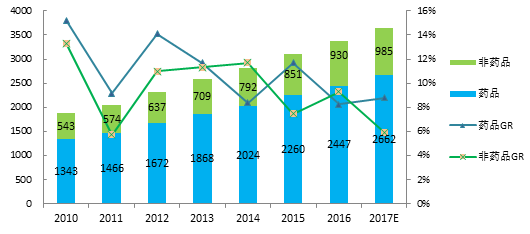

Figure 7. Retail Market Size (in RMB 100 Million) and Growth of Pharmaceuticals and Non-Pharmaceuticals in the Retail Market, 2009–2016

Driven by policies promoting the separation of prescribing and dispensing and the outflow of prescriptions from hospitals, the market share of retail pharmacies is gradually increasing. In 2016, the total size of China’s pharmaceutical retail market reached RMB 337.7 billion, representing an 8.5% year-on-year growth from 2015. It is projected that in 2017, the growth rate of the retail terminal pharmaceutical market will stabilize; however, bolstered by favorable policies such as the separation of prescribing and dispensing, prescription outflow, and the channel shift of high-priced drugs (new and specialty drugs), growth at the retail terminal will outpace that at the hospital terminal.

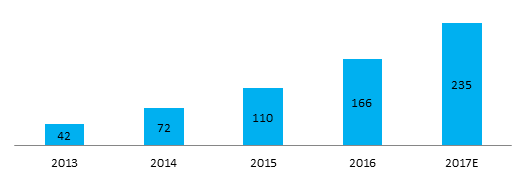

Figure 8 Sales Volume of Online Pharmacies (RMB 100 million)

Driven by the disruptive development of the internet, online pharmacies, which emerged in 2011, are still in a stage of high growth, with their market share showing a trend of continuous increase. In 2016, the total sales volume of online pharmacies in China reached 23.5 billion yuan, representing a 50.9% increase compared to 2015. Among this, the sales volume of drugs amounted to 4.5 billion yuan, accounting for 27.1% of the overall business of online pharmacies. Since the sale of prescription drugs over the internet has not yet been legalized, it is expected that the proportion of drug sales on the internet will further decline to 24.7% in 2017.

The Rise of Retail Pharmacies: Unlocking Potential, Poised for Growth

Driven by factors such as rising per capita disposable income and the upgrading of health consumption, the pharmaceutical and health industry has achieved rapid growth. Among these developments, the status of retail pharmacies has risen significantly, with a market size of RMB 337.7 billion, making them one of the major forces in the industry.

1. Increased Market Concentration: Chain Store Penetration Rate to Surpass 50%

After a period of unregulated expansion, the pharmaceutical retail industry has entered a phase characterized by branding and chain-store development. According to the annual statistical report of the China Food and Drug Administration (CFDA), the total number of registered pharmacies nationwide reached 447,000 in 2016, a decrease of 1,023 from 2015. For the first time, the total number of pharmacy outlets declined. The number of independent pharmacies dropped by another 6.9% compared with 2015, while the chain store penetration rate increased by 3.6 percentage points to 49.4%. Despite the rise in chain store penetration, the average number of outlets per chain enterprise showed a downward trend, primarily due to lowered policy standards for qualifying as a chain pharmacy in certain regions. The chain store penetration rate for retail pharmacies is expected to exceed 50% in 2017.

2. Market Size Expansion: Reaching RMB 364.7 Billion in 2017

Factors such as urbanization, population aging, and rising fertility rates have not only driven the growth in health consumption demand but also brought favorable conditions to retail pharmacies. According to data from Sinopharm CMH, in 2016, the sales volume of pharmaceuticals at retail terminals reached RMB 244.7 billion, a year-on-year increase of 8%; non-pharmaceutical sales amounted to RMB 93 billion, up by 12% year on year. The overall retail market size is projected to reach RMB 364.7 billion in 2017, representing an 8.0% year-on-year growth.

As the growth rate of online pharmacies slowed after peaking in 2015, their impact on foot traffic at brick-and-mortar pharmacies diminished, leading to a gradual recovery in customer visits. According to data from Sinohealth CMH, the average monthly number of transactions per comparable sample store reached 3,277 in 2016, a year-on-year increase of 3.8%; the average transaction value was RMB 57.7 per customer per visit, up 2.8% year on year. Notably, the increase in transaction volume contributed 58% to the sales growth of pharmacies.

Meanwhile, the trend toward scale in retail pharmacies has become increasingly evident. The sales scale of the top 100 chain retailers has risen year by year, reaching RMB 123.5 billion in 2016 and accounting for 36.6% of the retail market. In 2016, mergers and acquisitions were relatively active among chain enterprises with annual sales exceeding RMB 1 billion, and the share of sales accounted for by the top 100 chains increased by 2.5 percentage points compared with 2015.

3. Consumption Upgrading Boosts Category Development

Influenced by factors such as public hospital reforms, medical insurance cost containment, and pharmaceutical companies losing or abandoning bids, drug manufacturers are increasingly seeking to expand into the out-of-hospital market. The surge in Direct-to-Patient (DTP) pharmacies has become the vanguard driving the growth of prescription drug sales in retail pharmacies. According to research data from Sinohealth CMH, OTC drug sales in the retail market reached RMB 125.1 billion, accounting for a 51.1% market share, while prescription (RX) drug sales amounted to RMB 119.6 billion, representing a 48.9% market share. Notably, prescription drugs contributed 61.2% to the incremental growth. It is projected that the growth rate of RX drugs in the retail market will continue to exceed that of OTC drugs over the next year.

Notably, within the prescription drug segment, antineoplastic and immunomodulating agents accounted for 4.05% of the retail terminal prescription drug market in 2016, representing a year-on-year growth of 60.4%. Their market share is projected to rise to 4.86% in 2017, maintaining robust growth at 40.7%. It is foreseeable that, driven by policies facilitating the outflow of prescriptions from hospitals and influenced by factors such as the rising incidence of chronic diseases due to population aging, the importance of prescription drugs in pharmacies will continue to strengthen.

Meanwhile, factors such as consumption upgrading and heightened health awareness have driven the growth of high-value OTC categories with wellness and healthcare benefits. According to research data from Zhongkang CMH, among key categories in retail pharmacies, medicinal herbs have shown the most significant growth trend: the year-on-year growth rate surged from 8.3% in 2015 to at least 17.9%, and is projected to maintain robust double-digit growth (16.0%) in 2017. This indicates that future consumer demand for health and wellness will become a primary pain point for companies to address.

It is evident that the vast potential of retail pharmacies is being unlocked. According to forecasts by Sinohealth, over the next decade, assuming the complete implementation of the separation of prescribing and dispensing, the market size of retail pharmacies will reach RMB 1.72 trillion (at constant prices), accounting for approximately 65% of the entire terminal pharmaceutical market. Industry concentration will also increase significantly, with the chain pharmacy rate reaching 70%. The sector will complete its business model iteration from a mere distribution channel to a focus on service and value creation, evolving into one of the main pillars of China’s pharmaceutical market.