Will Medical Mall Be the Simplest Path for Chinese Real Estate Developers to Enter Healthcare?

By Luo Mei, Yang Juan

Since the beginning of this year, real estate developers have accelerated their transformation. Taking Wanda Group as an example, news of its forays into the healthcare sector emerges every two months.

In April 2017, Wanda Group formally signed a strategic cooperation memorandum with the Chengdu Municipal People's Government, under which both parties agreed to invest RMB 70 billion to build a world-class medical industry center. In July, Wanda Group signed three new investment projects in Kunming, planning to invest RMB 50 billion in Kunming City to create a world-class medical and general health industrial park centered on healthcare and wellness, while integrating functions such as sports, regenerative care, vacationing, commerce, business, and residential living. In August, Wanda established a new General Health Group, signaling that Wanda had strategically prioritized the development of the general health industry.

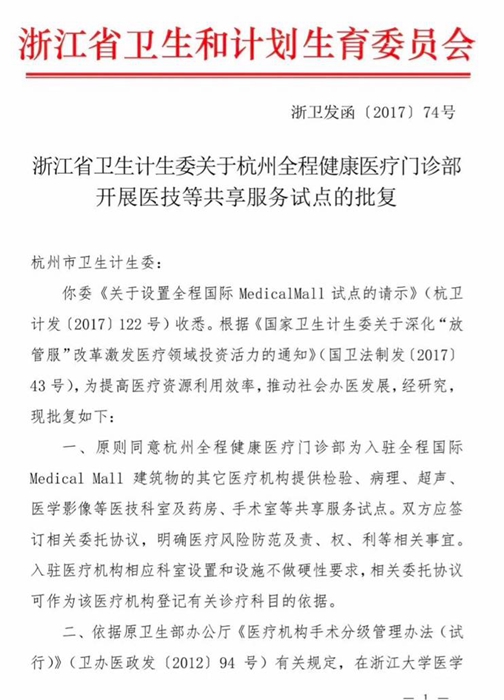

In recent days, the “Medical Mall” has also taken social media by storm. Approved by the Zhejiang Provincial Health and Family Planning Commission, this Medical Mall is located in the Hangzhou Tower 501 Urban Life Plaza. Floors 1–5 are designated as shopping areas, while floors 6–20 are entirely devoted to medical services. Consumers can enjoy a multidimensional experience that integrates retail shopping with healthcare services, thereby alleviating the anxiety often associated with visiting hospitals.

Sir Run Run Shaw International Medical Center, Zhang Qiang Doctor Group’s Sijun Surgical Clinic, Weienuo Pediatric Clinic, Hangzhou Stomatological Hospital Outpatient Department, and Yanshu Medical Aesthetics Clinic under the Song Weimin Doctor Group have successively settled into the Medical Mall, ushering in a new wave of enthusiasm.

According toVCBeat (WeChat ID: vcbeat)According to incomplete statistics, more than 30 real estate developers in China, including Vanke, Evergrande, Wanda, and Greentown, have entered the healthcare sector. These companies are strategically focusing on community services, particularly in the field of community health and medical services, by implementing their respective operational models. This trend has spurred the development of a large number of senior living real estate projects and integrated medical-care facilities.

In these senior living real estate or integrated medical-care projects, the prevailing view among industry insiders is that while pivoting direction is easy, achieving success is an uphill battle. This is because the healthcare industry requires high barriers to entry, advanced technology, and substantial investment, while being heavily dependent on policy support. Even if real estate developers have sufficient capital to operate such projects, they often struggle to recruit suitable personnel for management and operations.

So, is there a simple and feasible path for real estate developers to transform? Have overseas real estate developers encountered similar challenges? And how have they turned these difficulties into opportunities?

Through extensive research conducted by VCBeat, it has been found that clinics have long been present in shopping malls abroad. The physicians in these clinics adopt a patient-centered approach, making medical consultations as convenient and enjoyable as shopping. This type of healthcare setting is known by the trendy term “Medical Mall.”

At Medical Mall, physicians provide patients with one-stop services ranging from clinic consultations, laboratory and radiology services, to outpatient surgeries, aiming to encourage patients to access their daily healthcare needs within a collaborative network.

A successful Medical Mall is not only bustling with activity but also ensures high patient satisfaction, as patients enjoy the most convenient medical services. It features supporting amenities such as parking lots, restaurants, retail stores, and lounges, alongside comprehensive medical facilities.

In fact, these medical facilities are all meticulously planned. For instance, outpatient clinics for orthopedic conditions may be located in the same area as sports medicine or physical therapy centers; proton therapy equipment may be situated adjacent to the oncology center; and within outpatient clinics or hospitals specializing in cardiovascular diseases, it is entirely possible to have cardiologists, cardiovascular surgeons, and interventional specialists available simultaneously.

Such clinical support systems offer advantages to both patients and healthcare institutions. Patients enjoy greater convenience in accessing medical care, as they can obtain a variety of medical services simultaneously without traveling long distances. Meanwhile, institutions operating within the platform can reduce healthcare costs by sharing space, staff, equipment, and technology, while also securing a stable base of patients.

Over the past two decades, competition among major shopping malls in the United States has intensified alongside economic growth. Compounded by poor management, sluggish consumer spending growth, and the disruptive impact of e-commerce, many shopping malls now face the predicament of closure and bankruptcy.

According to relevant statistical data, more than 19% of the current 2,000 regional shopping malls have ultimately become what people refer to as “Dead Malls.”

To survive in a fiercely competitive market, major shopping mall developers are beginning to seek new uses for existing spaces, such as adding educational, medical, and office facilities. Physicians believe that these underutilized mall spaces offer an ideal opportunity to provide differentiated medical services that are more accessible and closer to patients.

Thus, by leasing vacant retail spaces in shopping malls, these physicians not only generated profits for mall developers but also brought medical services into retail environments, giving rise to a new economic phenomenon.Namely, the “Medical Mall” model of one-stop healthcare services, which is entirely different from traditional forms of healthcare delivery.

The Medical Mall model offers numerous benefits to both patients and healthcare providers. For instance, it allows users to address their medical and health needs while shopping, with the added convenience of easy parking, thereby alleviating the difficulty of accessing medical care to a certain extent.

At a time when healthcare demands in American society are continuously increasing,AdvocatePatient-Centeredmedical services,This has also indirectly fueled the growth of the Medical Mall.

Furthermore, hospitals and physicians within medical malls can also benefit from expanded clinical and office spaces. By serving local residents, this centralized, clustered service model is more effective at attracting patients. In low-income areas, the medical mall design can both increase access to healthcare and serve as an engine for community economic revitalization. For example, the Jackson Medical Mall in Jackson, Mississippi, is a medical mall designed to serve underserved populations (African Americans), with the aim of improving healthcare access and stimulating the local economy.

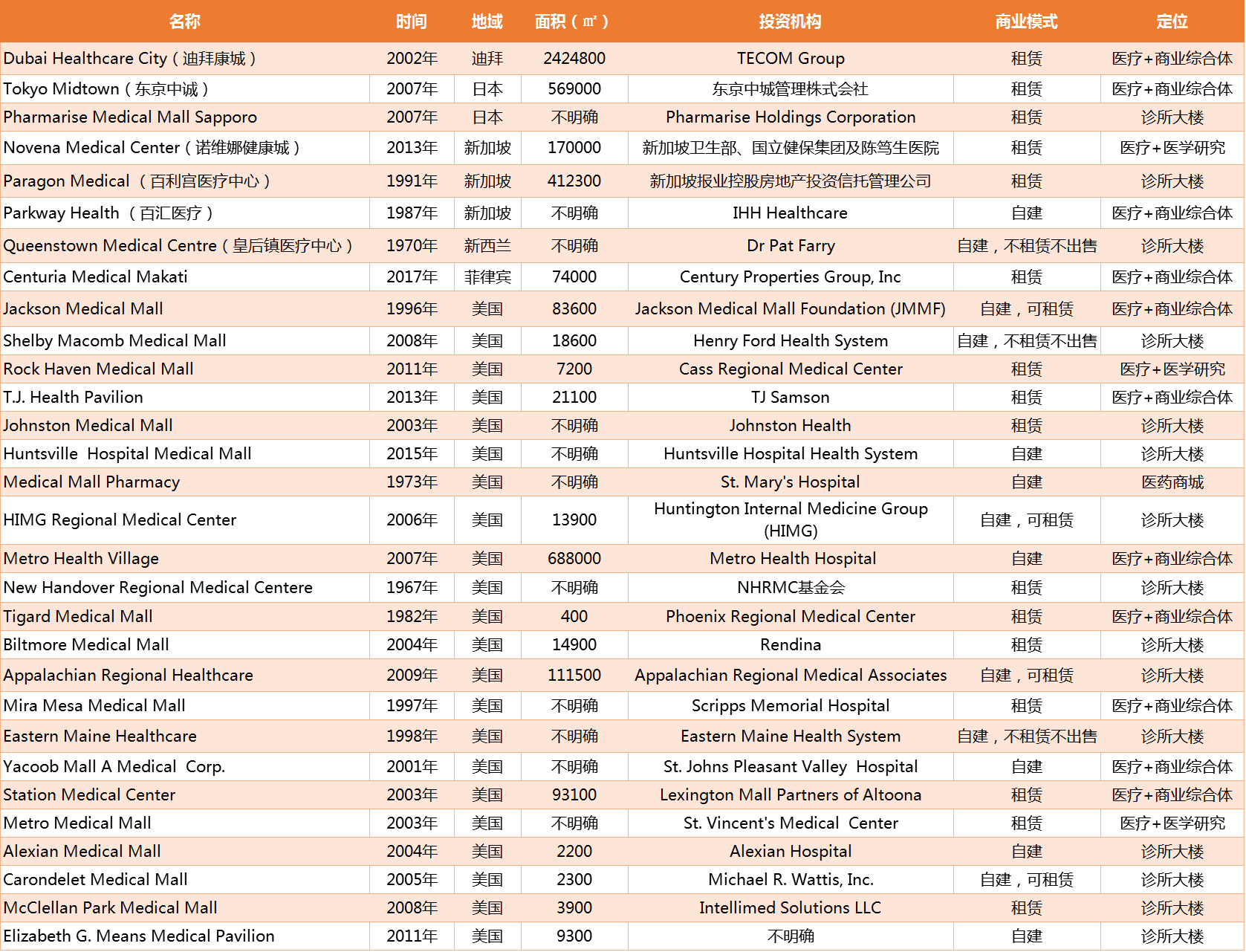

Do Medical Malls exist in other countries? To find the answer, VCBeat compiled a list of 30 Medical Malls across Europe, North America, Asia, and Oceania, ultimately revealing that the United States has 22, more than any other country. The details are as follows:

As can be seen, the United States, Singapore, Japan, the Philippines, and New Zealand have given rise to numerous innovative healthcare models, including medical office buildings, integrated healthcare and medical research facilities, and healthcare-commercial mixed-use complexes. Among these, the healthcare-commercial mixed-use model has been vigorously promoted and has received widespread acclaim.

Note:Commercial complexes are based on building clusters, integrating five core functions: commercial retail, business offices, hotels and catering, apartment residences, and comprehensive entertainment. Commercial complexes include services such as shopping, entertainment, dining, hotels, tourism, office work, and education.

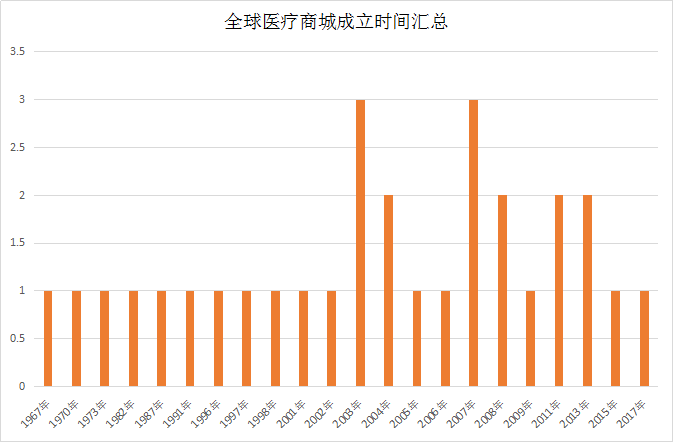

In terms of timeline, no clear trend has been observed. Among them, New Handover Regional Medical Center in the United States was established earliest (in 1967). From a longitudinal perspective, there were relatively more medical malls newly established in 2003 and 2007. However, in recent years, with the rise of the “healthcare + commercial center” model in Asia, medical malls in regions such as Singapore and Malaysia have shown a growth trend.

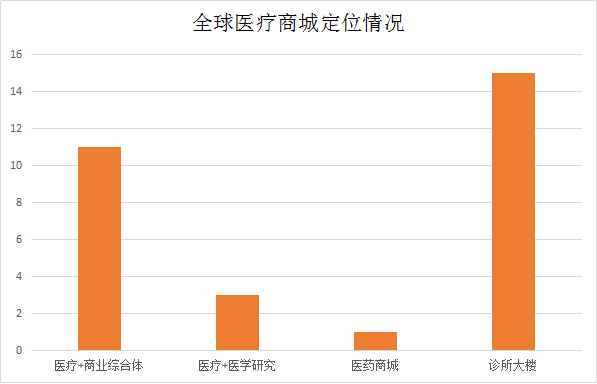

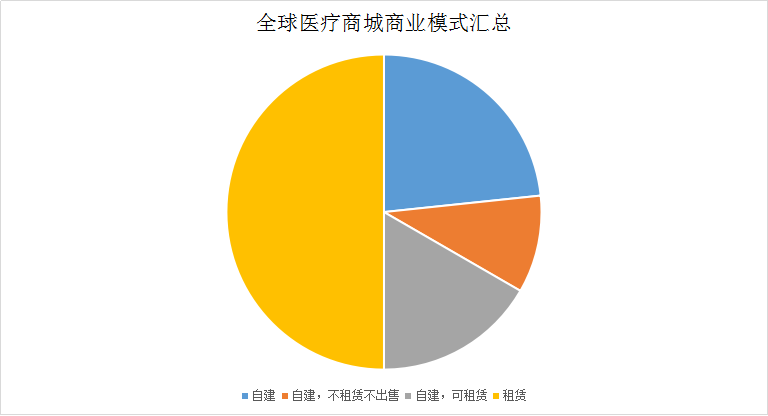

These 30 medical malls have slightly different positioning, and we broadly categorize them into four types: “Healthcare + Commercial Complex,” “Healthcare + Medical Research,” “Clinic Building,” and “Pharmaceutical Mall.”

Eleven companies adopt a “healthcare + commercial complex” business model, meaning that customers visiting the mall can enjoy one-stop medical services as well as shopping, dining, hotel stays, and entertainment. Fifteen companies operate under a “clinic building” model, which houses various types of hospitals and specialized clinics in fields such as pediatrics, orthopedics, dentistry, traditional Chinese medicine, and medical aesthetics and plastic surgery.

The business models of the final three companies are “Healthcare + Medical Research.” In addition to providing clinical diagnosis and treatment services, these complexes host medical universities or medical associations conducting in-depth research on-site.

Additionally, Medical Mall Pharmacy is a special case; it is a pharmaceutical marketplace that has attracted numerous high-quality pharmacies.

In terms of profitability, it can be observed that the majority of medical e-commerce platforms generate profits through leasing models, while a small portion rely on self-built and self-operated infrastructure.

One notable difference is the medical e-commerce platforms in Asian regions (Singapore, Malaysia, and the Philippines)It is largeSome are composed of real estate developers, investment firms, or trust companies, whereas most medical malls in the United States are established by large hospitals, physician groups, or government entities.

Over the past two decades, the “medical mall” model in the United States has continued to expand and strengthen. One of the most significant reasons for this growth is the imposition of caps on hospital charges by health insurance companies. Consequently, healthcare institutions have had to conduct their medical operations either by building their own medical malls or by leasing space within existing ones.

According to incomplete statistics from VCBeat, there are currently more than 50 medical malls in the United States. While their operational models vary, they all adopt the “leasing” model of shopping malls, where various healthcare institutions rent different spaces under one roof to provide patients with a more convenient combination of products and services.

According to a study published in BMC Health Services Research, 870 (62.4%) of the 1,395 enclosed shopping malls in the United States lease space to one or more optometry tenants, and 241 (17.3%) lease to one or more dental practices. Additionally, 89 malls (6.4%) offer other types of healthcare services, most commonly general outpatient and specialty outpatient clinics, as well as psychological counseling services and urgent care.

Depending on the founders and investors, U.S. healthcare marketplaces can generally be categorized into the following two types:

1. Medical marketplace funded and established by large hospitals

One of the earliest medical malls in the United States is the Jackson Medical Mall, established in 1995. It was built on the site of Jackson’s first shopping mall. After the mall went bankrupt, Dr. Aaron Shirley, a downtown resident and former project director of Mississippi’s largest community health center, envisioned transforming the failed shopping center into a state-of-the-art medical facility to provide high-quality healthcare services to local residents.

Jackson Medical Mall, spanning 850,000 square feet, houses clinics operated by the Hinds County Health Department as well as numerous specialty clinics affiliated with the University of Mississippi Medical Center, offering a wide range of medical services including cardiology, obstetrics and gynecology, and oncology. Embodying the spirit of a shopping mall, Jackson Medical Mall also features other amenities such as a grocery store, restaurants, a beauty salon, and a shoe store.

This is a win-win model for both hospitals and patients. By adopting the “medical mall” model, hospitals can renovate existing shopping malls or areas near hospital buildings with new equipment, without incurring the substantial costs of demolishing the original shopping malls and rebuilding hospitals from scratch. The new facilities can provide outpatient and diagnostic services at a location near the hospital, allowing for a more flexible suite of medical services.

For patients, a “one-stop shop” model of integrated healthcare means accessing multiple medical services during a single visit, eliminating the need to travel between different locations. Procedures such as tooth extraction, health check-ups, or cosmetic surgery can all be completed within the same building. Moreover, patients can dine, watch movies, or go shopping while receiving care. Truly, it allows for seamless integration of medical treatment and leisure activities.

2. Medical Mall Established by Doctors/Investors

Another medical mall established by physicians or investors. In 1998, 30 physicians who leased space at St. John Mercy Medical Center in Washington, Missouri, United States, built a brand-new, 85,000-square-foot facility called Patients First Health Care. Their motivation was not only to serve local patients but also, importantly, to provide larger office spaces for physicians who had previously worked in the crowded St. John Mercy Medical Center.

Medical malls initiated by physicians or investors are often smaller than hospital-sponsored ones and are frequently located near retail centers. Owners of medical malls can derive significant benefits, including lower overhead, easier access to patient and physician resources, an increased base for patient referrals, and greater control.

By providing convenient and efficient alternatives to emergency room visits and inpatient care, the “medical mall” model can play a significant role in reducing healthcare costs and may help curb the rise in health insurance premiums. The number of self-pay patients is steadily increasing and may become the norm in healthcare delivery. The medical mall model creates new markets for hospitals, private practitioners, specialists, and developers to better serve patients.

Case 1: Dubai Healthcare City

As a major global trade hub and financial center, Dubai has long been synonymous with opulence. In the realm of medical commerce, Dubai is equally unapologetic about its grandeur, having established an ultra-luxurious healthcare hub—Dubai Healthcare City.

Dubai Healthcare City (DHCC) is a world-class healthcare center proposed in 2002 by Sheikh Mohammed bin Rashid Al Maktoum, Vice President and Prime Minister of the UAE and Ruler of Dubai. It was established to meet the demand for high-quality medical care and health management among the 2 billion people living between Europe and East Asia. The entire project, with an investment of $1.8 billion, was led and developed by TECOM Group. Dubai Healthcare City comprises hospitals, clinics, medical colleges, nursing schools, life sciences research centers, and specialized laboratories.

To date, Dubai Healthcare City is home to two large-scale hospitals, over 160 outpatient clinics and diagnostic laboratories, more than 1,700 licensed professionals from nearly 90 countries, and 200 specialized wellness and commercial retail service facilities. The entire Dubai Healthcare City is primarily divided into a medical zone and a leisure and convalescence zone.

Dr. Michael's Dental Clinic in Dubai Healthcare City

The medical zone covers an area of 380,000 square meters (570 mu),Four Services Provided:

1. Traditional Medical Services.Bringing together physician offices, ambulatory surgery centers, general hospitals, specialty hospitals, rehabilitation and long-term care facilities, hospice care, and diagnostic laboratories to provide highly convenient, one-stop medical services.

2. Alternative Medical Services.Centers Integrating Eastern Medicine and Other Health Programs Offer CAM Therapies Across 12 Domains: Homeopathy, Ayurveda, Traditional Chinese Medicine, Unani Medicine, Osteopathy, Therapeutic Massage, Naturopathy, Guided Imagery, Tai Chi, Pilates, Chiropractic Spinal Manipulation, and Yoga.

3. Medical Education and Research.Home healthcare, dentistry, nursing, and health training schools, etc., including the Boston University Dubai School of Dentistry, Harvard Medical School Dubai Center, and other basic medical services such as pharmacies, medical equipment, and medical consulting.

4. Related Support Services.For example: visa centers, five-star hotels, mineral spring spa resorts, shopping malls, retail and beverage stores, etc.

The vacation and wellness resort spans 1.76 million square meters (2,640 mu), offering home-style hospitals with continuous care, outpatient services, luxury hot spring resorts, and comprehensive health services. Its facilities include a community hospital for healthcare, community outpatient clinics, disease prevention and convalescence centers, beauty centers, and sports rehabilitation centers.

Overall, Dubai Health City is an integrated medical complex that combines clinical care, rehabilitation and recuperation, vacation tourism, and education and research.

Case 2: Jackson Medical Mall, USA

Jackson Medical Mall (hereinafter referred to as “Jackson Medical Mall”) is one of the earliest and largest medical malls in the United States, covering an area of approximately 900,000 square feet. Established in 1996, Jackson Medical Mall was transformed by Dr. Aaron Shirley from an abandoned shopping center into a modern healthcare and retail hub. Through strategic partnerships with the University of Mississippi Medical Center (UMMC), Jackson State University, and Tougaloo College, it provides medical services to low-income areas (African American communities). In addition, the mall bears the mission of promoting regional economic development and has introduced Mississippi’s only African American-owned bank.

Through its leasing operations, Jackson Medical Mall has secured more than 80 tenants in the healthcare, retail, and social services sectors, as well as four public and private event venues. Throughout the year, dozens of organizations and their supporters utilize these facilities. The mall houses 22 medical institutions, including the UMMC Renal Dialysis Clinic, the UMMC Cancer Institute, and the Mississippi Society of Eye Physicians and Surgeons, along with 20 lifestyle service stores, three educational institutions, eight university departments, 26 offices, and 26 medical center training bases.

Jackson Medical Mall provides comprehensive healthcare services, ranging from general and specialty outpatient clinics to medical education. The facility serves over 200,000 patients annually, with an average of 4,600 to 5,000 vehicles entering its gates each day.

According to the 2016 annual report released by the Jackson Medical Mall Foundation (JMMF), the actual controlling entity of the Jackson Medical Mall, the mall generated $12,983,203 in revenue last year, with lease and related income accounting for 78%. However, the mall also incurred expenditures of $12,420,489 during the same period, 71% of which were allocated to daily management and operational service costs. Consequently, the Jackson Medical Mall’s net income for the year amounted to only $562,714. Nevertheless, as the Jackson Medical Mall is primarily community-service oriented rather than commercially driven, its core mission is to serve local residents and stimulate economic development in the surrounding area.

Case 3: Centuria Medical Makati, Philippines

Centuria Medical Makati (hereinafter referred to as “Centuria Medical Mall”) is the first and largest medical mall in the Philippines, located in the bustling heart of Makati. It is a 28-story advanced medical building housing more than 700 leaders in the healthcare industry.

Centuria Medical Mall features experienced, professional physicians and operates as a premier HMO, dedicated to providing consumers with affordable traditional and top-tier medical services. By integrating the technical expertise of Grade A tertiary hospitals with the luxurious and relaxed ambiance of a lifestyle shopping center, the mall serves as a one-stop destination for all outpatient medical needs, including dentistry, orthopedics, urology, plastic and cosmetic surgery, multi-organ procedures, obstetrics and gynecology, ophthalmology, and more.

The urgent care clinic is located on the ground floor of this stylish medical tower and is open 24 hours a day. The seventh floor houses the Ambulatory Surgery Center, catering to more specialized medical needs such as plastic and cosmetic surgery, ENT-HNS, gastroenterology, OB-GYN, ophthalmology, orthopedics, and urology. The eighth floor is the Examination Center, offering tailored screening tests based on the individualized needs of specific patients. The ninth floor features an advanced laboratory for high-precision diagnostics, supported by high-quality services and a thoughtfully designed, modern clinical environment. Numerous myRisk hereditary cancer tests and non-invasive prenatal screenings are just some of the many advanced diagnostic services provided by the center.

It is reported that Centuria Medical Mall will also open the region’s first free, non-profit comprehensive breast cancer treatment center. The Asian Breast Center is affiliated with Morristown Medical Center, a leading cancer institution that has been ranked among the top five hospitals in New York and among the top 50 hospitals in the United States.

Certainly, in addition to a wide range of medical services, Centuria Medical Mall has established Executive Guest Suites and the Haus Fitness Center on the eighth floor to enhance patient comfort and convenience. Much like a traditional shopping mall, Centuria Medical Mall also hosts banks, ATMs, convenience stores, and other franchise retailers, including 7-Eleven, Belly Smiles, Healthy Cravings, and Metrobank.

Centuria Medical Mall has attracted widespread attention from all sectors since its establishment was announced at the beginning of this year. The mall is currently in a soft-opening phase and is expected to officially open on September 23, 2017.

Here is a classic case: Many years ago, Parkway Holdings was merely a small real estate company in Singapore. It transformed into the healthcare sector by leasing rooms to physicians for establishing private practices. These physicians could share the facilities and services provided by the hospital, which also supported clinics in purchasing expensive equipment through equity participation. Frequent interaction and collaboration among clinics, including joint consultations, created significantly greater value than a simple physical aggregation would have.This flexible, mutually beneficial “Parkway Model” has propelled Parkway to become the leading private healthcare provider in Southeast Asia.

What kind of chemical reaction would occur if domestic real estate developers also chose to transform into Medical Malls?

Taking the Chengdu Wanda Reign International Medical and Health Center as an example, its platform architecture shares similarities with the Parkway model. The project features seven core “TOP business formats,” including West China Health Services, Postpartum Recovery Center, Premium Health Management, Medical Aesthetics Institution, Overseas Medical Services, Medical Institution Liaison Offices, and Traditional Chinese Medicine (TCM) Wellness Club. Wanda will provide tenant institutions with space, property management services, and business support, including access to premium clubs such as the “Elite Club.”

In terms of business diversity, the Wanda Reign International Medical and Health Center is clearly superior to the “Parkway Model.” Furthermore, its tenants are not individual physicians or small- and medium-sized clinics, but rather world-class institutions such as IHG.

“A Wanda manager described it this way: ‘Our seven core business formats do not operate in silos; rather, they are closely interconnected. Health check-up services and health management can be bundled with Traditional Chinese Medicine (TCM) wellness programs, and their clients can also access overseas medical services. Medical aesthetic clinics can share customers with postpartum recovery centers... All these sectors can drive patient traffic to the medical institution offices. Just as a comprehensive physical complex enables a cyclical flow of visitors, our various business formats will form a resource ecosystem and a closed-loop industrial chain, delivering substantial benefits to every tenant.’”

In terms of transformation, Huarong Property has clearly taken a step ahead of Wanda.On August 25, 2017, Huarong Real Estate partnered with Health Intelligence Valley,Investment of over RMB 4 billion,Transform the Huarong Commercial Real Estate property near Ranjiaba in Yubei District, Chongqing, into a commercial complex integrating dining, entertainment, and leisure facilities, including hotels, cinemas, and health services.

If Huarong is viewed as a platform, shopping constitutes one of its modules, as does the broader health and wellness sector, with additional modules such as education and training likely to be incorporated in the future. As more modules are integrated, the dimensions of this composite platform will become increasingly diverse. There are multiple ways to combine these modules: each module can operate as an independent mall, such as a commercial district Shopping Mall or a Medical Mall, or they can be layered as several service formats within a single shopping center.

Thus, for real estate developers seeking to transition into the healthcare industry, the Medical Mall model may be the most straightforward approach that is already being implemented.Of course, everything has just begun. Whether this model is suitable for Chinese users remains to be verified, and we do not rule out the emergence of newer Mall models in the future. Nevertheless, the patient-centric philosophy and the trend of shifting from passive healthcare to proactive healthcare are irreversible.