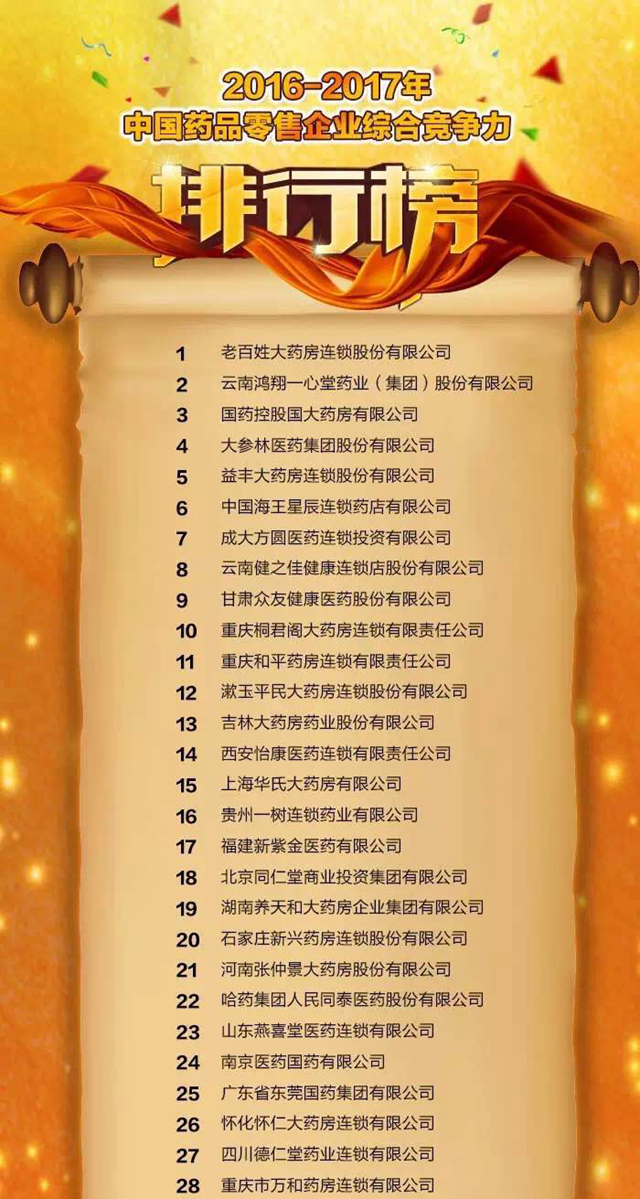

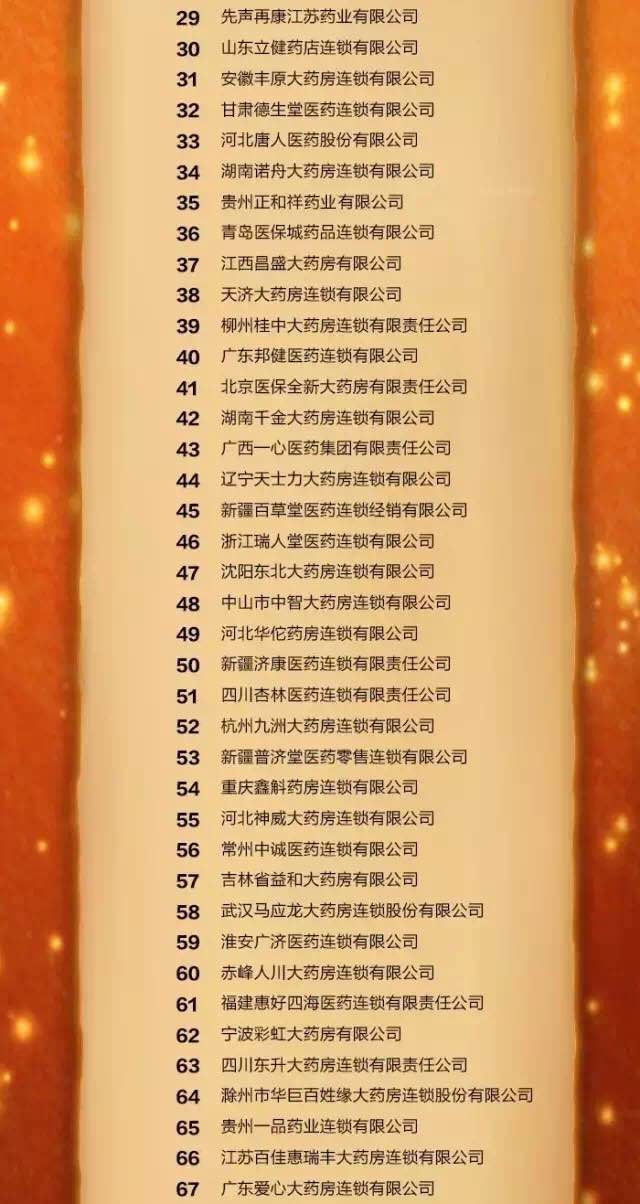

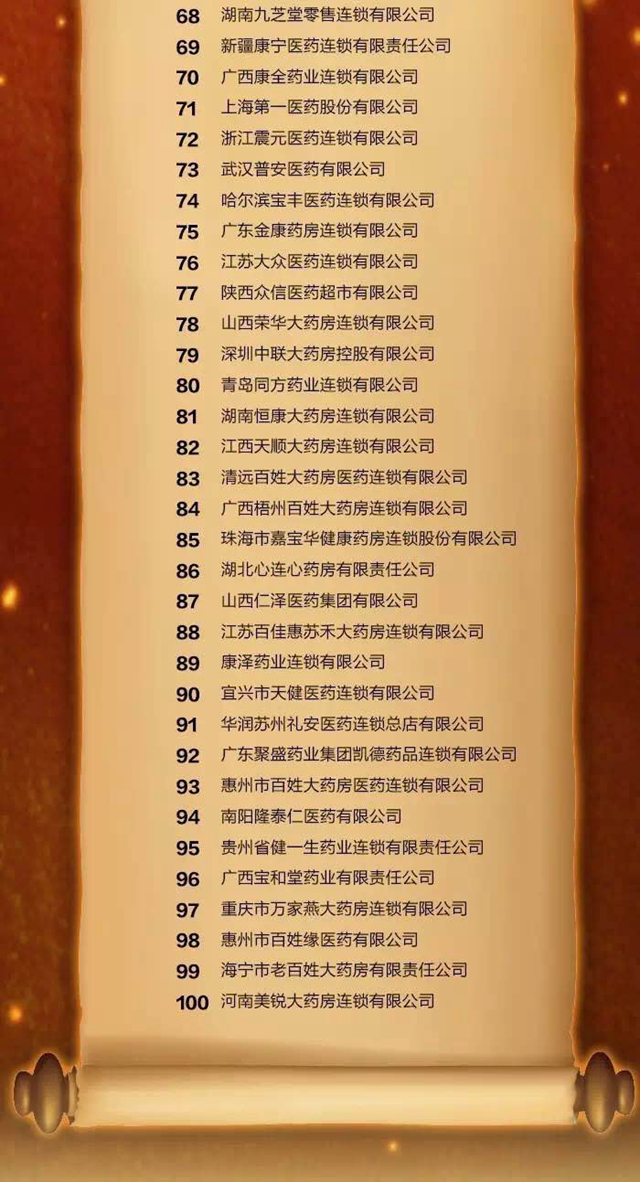

Top 100 Pharmaceutical Retail Chains Announced: 2% of Enterprises Capture 36.6% Market Share Amid Industry Transformation

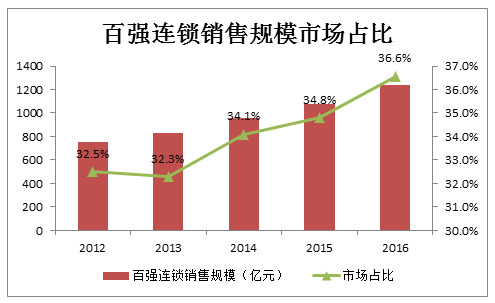

VCBeat (WeChat ID: vcbeat) has learned that the “2016–2017 China Pharmaceutical Retail Enterprises Comprehensive Competitiveness Ranking” was unveiled on the evening of August 18 at the 2017 Xipu Conference. The top 100 pharmacy chains are leading the pharmaceutical retail industry; although they account for less than 2% of the total number of enterprises, they capture 36.6% of China’s pharmaceutical retail market, amounting to RMB 123.5 billion. As market concentration continues to rise in the future, changes in the landscape of the pharmaceutical retail market will trigger a series of domino effects.

The Landscape of the Pharmaceutical Retail Industry Is Shifting

(1) Ranking Changes Reflect Turmoil in Industrial Transformation

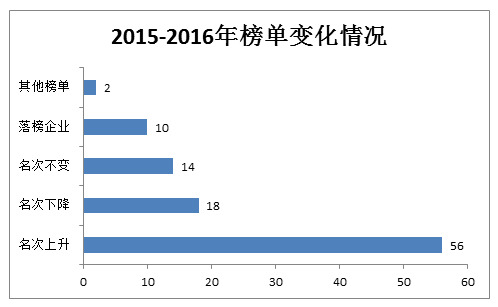

Compared with the 2015–2016 rankings, 28 companies dropped in rank, and 10 fell out of the top 100. The company with the largest decline within the list dropped by 10 positions. Among the companies that dropped off the list, four were acquired in 2016, with their financial statements consolidated into those of their parent companies. With the increasing number of newly listed and pre-IPO companies and the involvement of other capital, competition for mergers and acquisitions has intensified. Chain enterprises with annual sales scales of RMB 200 million to RMB 1 billion and relatively high operational quality have become the most sought-after targets. Meanwhile, most chain enterprises with scales below RMB 200 million are also adopting a wait-and-see attitude, hoping to secure favorable valuations.

It is worth noting that if small and medium-sized chain pharmacy enterprises remain stagnant in their operations, they will increasingly lose value amid the future wave of mergers and acquisitions.

(2) The polarization of the rankings has become more pronounced

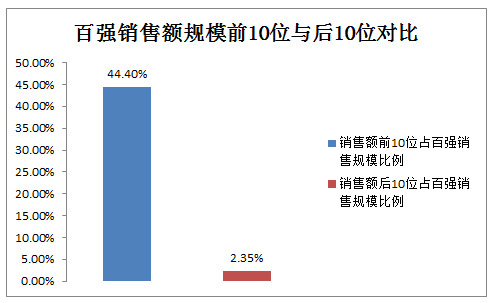

Among the top 100 enterprises, the top 10 by sales volume accounted for 44.4% of the total sales scale of the entire top 100, which is 18.87 times that of the bottom ten. As leading companies at the forefront transition towards an oligopolistic cluster, this gap is expected to widen further. It is foreseeable that, compared to the flexibility of single stores and small chains, medium and small-sized chain enterprises will face increasing pressure on their future survival space.

(3) The role of capital in optimizing industrial structure will continue to manifest

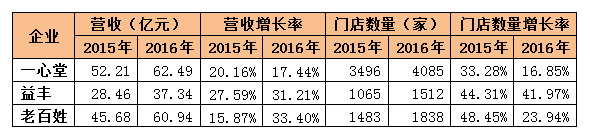

Changes in Revenue and Store Count of the Three Major Listed Companies

(Data source: Annual reports of listed companies)

In 2016, the sales volume of the top 100 chain stores accounted for 36.6% of China's retail market, an increase of 1.8 percentage points from 2015, indicating a continuous rise in market concentration.

The significant increase in market concentration is primarily evident among the leading large and medium-sized chain enterprises, as mergers and acquisitions represent the fastest means of expansion. On average, the pace of scale expansion for smaller and medium-sized chain enterprises ranked lower remains modest.

The three major chain enterprises that went public first have leveraged their capital advantages to maintain a rational approach to mergers and acquisitions, yet they have never slowed their pace of expansion. In 2016, among the three, Yifeng Pharmacy achieved the highest store count growth rate at 41.97%, while Laobaixing Pharmacy recorded the highest revenue growth rate at 33.4%, both significantly surpassing the overall average of the top 100 pharmaceutical retailers. Within just one year, these three publicly listed companies collectively added 1,391 stores and increased their annual sales by RMB 3.442 billion.

The recent listing of Dashenlin and the impending listings of other pharmacy chains will further intensify the competition for mergers and acquisitions. The entry of industrial capital and non-industry investors has further muddied the waters in the race for acquisition targets, while the structural changes in the industry driven by capital inflows are poised to reach new historical highs.

(4) Growing Challenges to Traditional Business Models

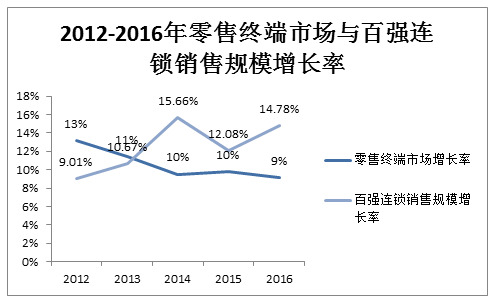

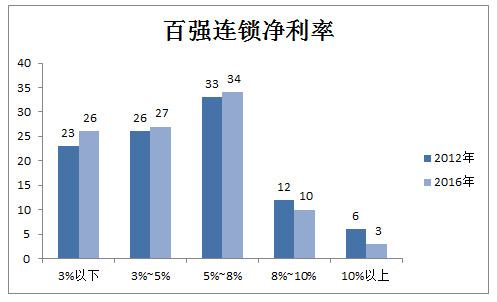

The sales scale growth rate of the top 100 enterprises was significantly higher than the industry average, reaching 14.78% in 2016, while the growth rate of the pharmaceutical retail market was 9.18%. However, despite the rapid expansion of corporate sales, profit margins did not show significant improvement. Compared with 2012, the number of enterprises achieving high profit margins decreased markedly. With no substantial improvement in core business profits, rising operational costs—primarily driven by labor and rent expenses—further squeezed corporate profitability.

(5) Gradual Enhancement of Professionalization

Among the top 100 pharmacy chains, 22 have a licensed pharmacist-to-store ratio of exactly one or higher, while 78 still maintain a ratio below one. In 2016, the overall licensed pharmacist-to-store ratio for the top 100 chains was 0.76, slightly higher than the national average of 0.68 for community pharmacies. This trend is driven partly by the new Good Supply Practice (GSP) regulations, which mandate that each newly opened store must be staffed with at least one licensed pharmacist, and partly by chain pharmacies’ increasing emphasis on professionalization to capture a larger share of the prescription drug market. Overall, the number of licensed pharmacists in the top 100 chains has grown significantly over the past two years, bringing them increasingly into compliance with regulatory requirements.

(6) Growing Emphasis on Brand Building

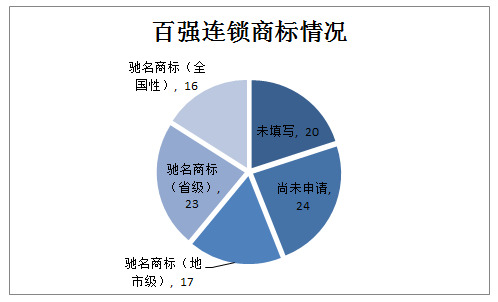

Among the top 100 pharmacy chains, 56 enterprises have applied for trademarks, with 16 of them having obtained China’s Well-Known Trademark recognition. Most of these top 100 chains are regional leaders, demonstrating a strong brand awareness that stands out within the industry. As competition in the retail market intensifies, brand strength will become a critical factor for chain pharmacies in expanding into and capturing new markets.

(7) The Industry’s Journey Toward Innovation Remains Long and Arduous

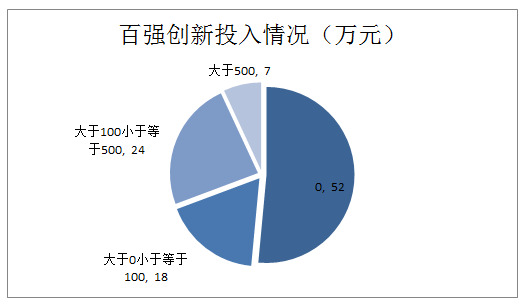

In 2016, 52 of the top 100 chain enterprises made no investment in innovation, reflecting a weak awareness of innovative development; only seven companies allocated more than RMB 5 million to special innovation initiatives. In the face of the new retail wave, the industry has seen a coexistence of proactive exploration, confusion, and sluggish response.

“New Rankings” Highlight the Trend of New Retail in Pharmaceuticals

The wave of new retail is sweeping across the market, and the pharmaceutical retail industry is no exception. However, due to the unique nature of pharmaceutical products, exploring new retail models in this sector presents greater challenges compared to other retail fields.

To this end, the 2016–2017 Comprehensive Competitiveness Ranking of Chinese Pharmaceutical Retail Enterprises established a separate “New List” outside the Top 100 to reflect explorations into new formats and models in pharmaceutical retail.

“New Ranking” primarily brings together two types of enterprises: professional pharmacies operating mainly under the DTP (Direct-to-Patient) model, and new-type pharmacies led by O+O (online-plus-offline) services.

As calls for the separation of prescribing and dispensing grow louder and the outflow of prescriptions continues to intensify, the Direct-to-Patient (DTP) model, as a pioneer in professional pharmacy services, is receiving increasing attention. The practical experience of chain enterprises that primarily operate under the DTP model will serve as a pioneering demonstration for other chains entering this field.

Traditional pharmaceutical e-commerce companies are moving away from relying solely on product sales and striving to build an integrated online-offline healthcare service system. In addition to their first-mover advantage in internet technology application, these companies enjoy greater flexibility in transformation due to the absence of a large number of traditional brick-and-mortar stores. Therefore, their exploratory efforts serve as a pioneering example for chain enterprises primarily reliant on physical stores.

The “new” in new retail is primarily reflected in the construction of a customer-centric service system, which differs fundamentally from traditional models. Specifically, in pharmaceutical retail, the common goal—reached via different paths—is to build a systematic and professional service chain that emphasizes customer experience, based on precise customer profiling and dynamic analysis of customer data. It goes without saying that the pharmaceutical retail industry is still in its infancy in these areas, with a long and arduous journey ahead. The establishment of the “New Retail Ranking” aims to highlight the significant value and strategic importance of such pioneering explorations for the industry. For companies selected for the New Retail Ranking, this recognition serves less as an award and more as encouragement for those who are leading the way in exploring new models of pharmaceutical retail.

The pharmaceutical retail industry is currently undergoing a period of transformation. The restructuring of the industrial ecosystem will profoundly impact the business environment, presenting both opportunities and challenges for large chain pharmacy enterprises. In this era of change, the ability to seize the pulse of the times has become the key to rapid corporate development and future success.