Comprehensive Scan of China's B2B Pharmaceutical E-commerce Industry: Policy Evolution, Market Landscape, Trends, and Product Insights

In 2005, the China Food and Drug Administration (CFDA) issued the Interim Provisions on the Approval of Internet Drug Transaction Services, marking the official emergence of the term “pharmaceutical e-commerce.” This regulation provided detailed stipulations on the classification, implementing entities, and operational procedures of pharmaceutical e-commerce. However, for a long period, the concept of pharmaceutical e-commerce was largely equated with “online pharmacies,” primarily due to their large numbers and extensive brand promotion, which significantly boosted their visibility. In contrast, B2B pharmaceutical e-commerce, or pharmaceutical distribution based on internet platforms, remained much more low-profile, akin to “a hidden gem unknown to the public.”

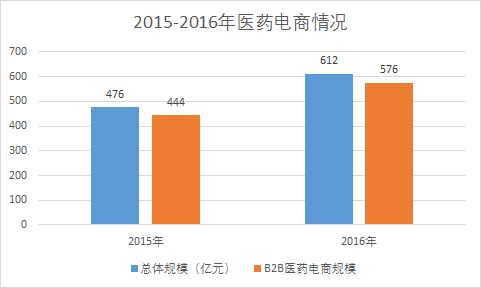

However, according to the "2016 Statistical Analysis Report on the Pharmaceutical Distribution Industry" issued by the Ministry of Commerce, the total sales volume of pharmaceutical e-commerce enterprises with direct reporting reached RMB 61.2 billion in 2016. Among this, B2B (business-to-business) transactions accounted for RMB 57.6 billion, representing 94.2% of the total pharmaceutical e-commerce sales; B2C (business-to-consumer) transactions amounted to RMB 3.6 billion, accounting for only 5.8% of the total.

Large Market Scale, Low Profile: Why Is This the Case for B2B Pharmaceutical E-commerce? In response to this phenomenon, VCBeat (WeChat ID: vcbeat) conducted an industry scan of B2B pharmaceutical e-commerce and engaged in discussions with senior executives from multiple B2B pharmaceutical e-commerce companies. The article provides a comprehensive analysis of the B2B pharmaceutical e-commerce sector from various perspectives, including driving factors, current market status, challenges, and development trends, thereby presenting a clear picture of an industry undergoing rapid transformation.

Policy: First Mover

Adam Smith, the founder of classical economics, proposed in The Wealth of Nations that the market is driven by an “invisible hand,” which allocates resources and structures social division of labor through free competition to achieve optimal output, reflecting the market dynamics of early capitalism. In the early 20th century, neoclassical economists represented by John Maynard Keynes introduced the contrasting concept of the “visible hand,” reflecting government intervention in the socio-economy and emphasizing the role of macroeconomic regulation.

More than a century has passed, yet these two theories remain applicable to China’s pharmaceutical economy. “Strict regulation leads to stagnation, while deregulation results in chaos” is a common assessment among industry insiders regarding the pharmaceutical sector. Even in emerging fields such as pharmaceutical e-commerce, the debate over regulation versus liberalization persists.

Therefore, when asked which factors influence the development of the pharmaceutical e-commerce industry, multiple respondents indicated that policy is the primary driving force for this sector.

He Side, founder of Drug Terminal Network, stated that B2B pharmaceutical e-commerce sparked industry discussion and attention following the introduction of regulations in 2005; however, few players actually entered this field before 2013. From 2013 to the present, B2B pharmaceutical e-commerce has truly entered its growth phase, ushering in a period of rapid development.

He believes that the emergence of B2B pharmaceutical e-commerce can be attributed to three factors. First, the continuous advancement of China’s “New Healthcare Reform” has altered the pharmaceutical business environment, compelling some enterprises to embrace change through innovation. Second, with the inherent growth of the internet and the accumulation of mature operational expertise in other e-commerce sectors, these practices have naturally been extended to the pharmaceutical industry. Third, the “Internet + Healthcare” initiative has sparked a wave of entrepreneurship, fostering synergistic development between the healthcare services and pharmaceutical sectors.

Zhang Yibing, former COO of Haoyaoshi, stated, “The pharmaceutical industry is inherently policy-driven. Given its direct impact on medication safety and public health, regulatory oversight inevitably plays a critical role. In other words, any discussion on the development of B2B pharmaceutical e-commerce cannot be divorced from policy considerations.”

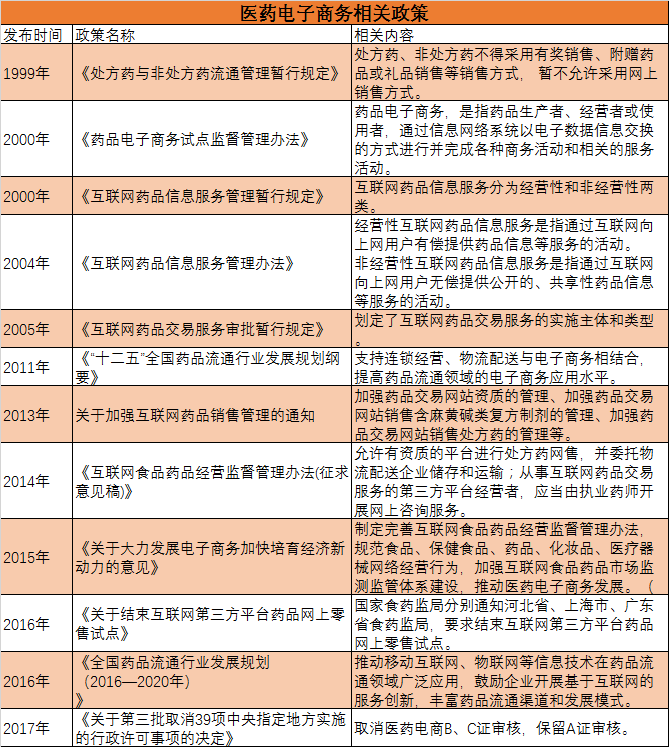

Guided by this framework, we have reviewed the policies issued over the years that have influenced the development of the B2B pharmaceutical e-commerce industry, categorizing them into two major groups: directly relevant and indirectly relevant.

Table 1: Policies Related to Pharmaceutical E-commerce

Here, we will highlight several key points. The first is the "Administrative Measures for Pilot Supervision of Pharmaceutical E-Commerce," promulgated in 2000. Prior to the issuance of this regulation, sporadic online pharmaceutical sales had already emerged; for instance, Shanghai No. 1 Pharmacy launched an online store in 1998, which was later shut down due to the lack of relevant policy support. This notice, issued by the National Drug Administration (later merged into the State Food and Drug Administration) to provinces and municipalities at the forefront of pharmaceutical e-commerce—namely Guangdong Province, Fujian Province, Beijing, and Shanghai—marked the first official "recognition" of the existence of pharmaceutical e-commerce, signaling that regulatory authorities had taken note of this industry.

After a five-year pilot program, in September 2005, the State Food and Drug Administration promulgated the Interim Provisions on the Approval of Online Drug Transaction Services, which clearly defined the scope of transactions, implementing entities, regulatory standards, and other aspects of online drug transaction services, thereby enabling the development of pharmaceutical e-commerce (B2B and B2C).

Another significant event occurred in July 2016, when the China Food and Drug Administration (CFDA) terminated the pilot program for third-party online drug trading platforms, revoking the pilot status of three platforms: 95095, 800 Fang, and Yihaodian. The CFDA cited issues such as “unclear delineation of primary responsibilities between the platforms and physical pharmacies, and difficulties in effectively regulating the sale of prescription drugs and ensuring drug quality and safety.” Although the pilot program was limited to the B2C sector, this move sent shockwaves through the industry, leaving many players apprehensive.

However, in January 2017, the General Office of the State Council issued a document abolishing the review process for Class B and Class C licenses for pharmaceutical e-commerce, which was seen as a positive signal of deregulation in the industry. In mid-May, the China Food and Drug Administration held closed-door meetings with eight pharmaceutical e-commerce companies to further discuss the relaxation of regulatory controls over pharmaceutical e-commerce.

It can be said that since 2000, the pharmaceutical regulatory authorities have maintained a taut “string” in their oversight of e-pharmacy. They must ensure medication safety and public health while also balancing industry development. However, the general trend has been toward deregulation, with e-pharmacy entering a period characterized by “lenient entry, strict exit, and filing-based supervision.”

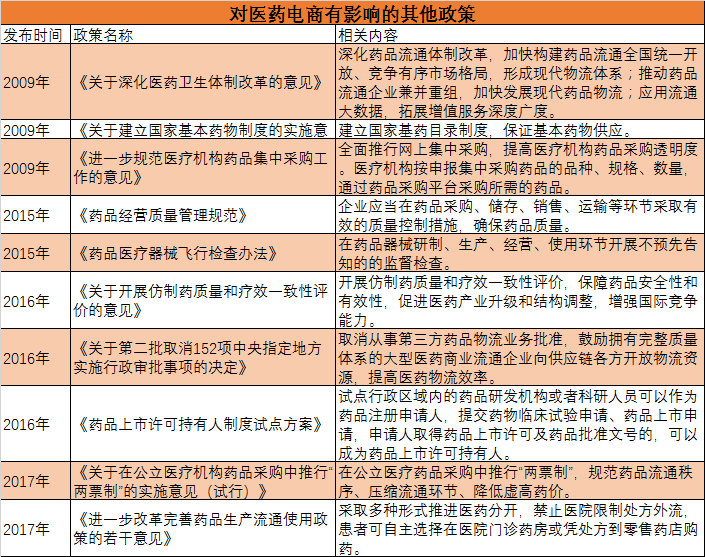

In addition, since the development of pharmaceutical e-commerce is influenced by the overall healthcare environment and the pharmaceutical distribution landscape, we will now examine other policies that impact its growth.

Table 2: Other Policies Affecting Pharmaceutical E-commerce

Of course, the most critical milestone here is 2009, when the “New Healthcare Reform” was officially launched. The “Opinions on Deepening the Reform of the Pharmaceutical and Healthcare System” and related supporting policies were successively promulgated, formally ushering in reforms such as the separation of prescribing from dispensing, control of the drug revenue share, development of a multi-tiered healthcare system, healthcare payment reform, primary healthcare strengthening, the essential medicines system, centralized procurement, and reforms in pharmaceutical circulation.

In the past two years, reforms in the pharmaceutical sector have been progressively refined under the framework of the “New Healthcare Reform.” Policies such as the new Good Supply Practice (GSP), unannounced inspections, consistency evaluation, the Marketing Authorization Holder (MAH) system, and the Two-Invoice System have been steadily implemented, covering all stages of drug development, manufacturing, distribution, sales, and utilization.

Overall, in the broader context of pharmaceutical e-commerce, pharmaceutical manufacturers’ supply, distribution channels, and demand-side dynamics are all undergoing changes. Pharmaceutical e-commerce is adapting to these shifts by leveraging internet-based tools to meet the needs of pharmaceutical distribution and individual consumers’ medication requirements, thereby maintaining a high degree of correlation with the pharmaceutical industry landscape.

Industry Overview: Hundreds of Enterprises, with a Market Size Approaching RMB 100 Billion

Certainly, in addition to policy support, capital investment, industry acceptance, and the willingness of traditional enterprises to participate are also key drivers for the B2B pharmaceutical e-commerce industry. Qiu Zhongxun, founder of Yaodou.com, told VCBeat that starting from 2014, B2B pharmaceutical companies began to attract attention from investors, including top healthcare investors such as Sequoia and Fosun, who started betting on B2B pharmaceutical e-commerce, thereby igniting the industry.

According to statistics from VCBeat, since 2016, B2B pharmaceutical companies such as 360 Health, Drug Terminal Network, Weiming Penguin, Yao Pianyi, and Yaoshibang have secured multiple rounds of financing, with a cumulative total exceeding RMB 1 billion. Investors include prominent firms such as Matrix Partners China, Chengwei Capital, GGV Capital, Ivy Capital, Fosun Pharma, and SoftBank China.

Companies securing such financing are generally internet platform companies. In addition to these, there are traditional distribution enterprises building their own platforms and e-commerce giants entering the market, making the entire B2B pharmaceutical sector “highly dynamic.”

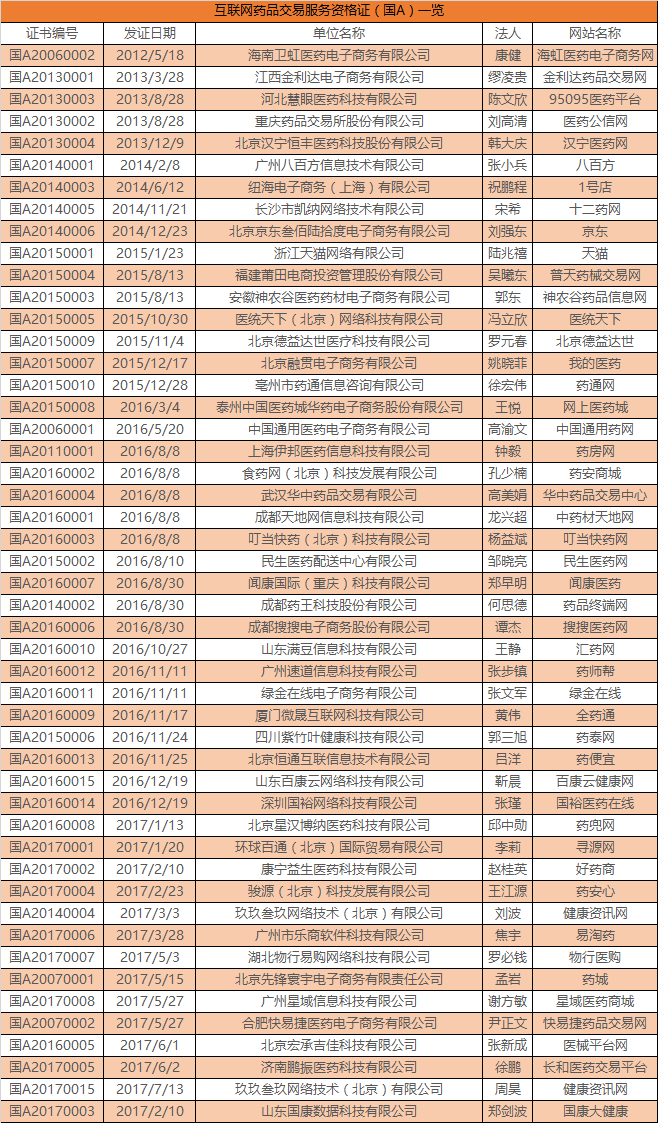

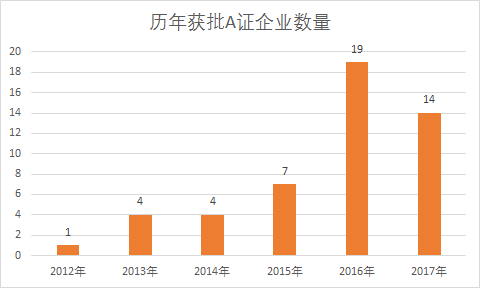

Taking companies holding Class A licenses (platform-based) as an example, data from the National Medical Products Administration shows that there were 48 such enterprises as of August 20. Earlier this year, before the cancellation of Class B licenses, more than 400 companies held Class B licenses; following the cancellation, the number of companies entering this sector may have increased. Combined, the total number of players in the B2B pharmaceutical e-commerce sector could exceed 500.

Table 3: Overview of Information on Enterprises Holding Certificate A

As can be seen from the table above, Haihong Pharmaceutical E-commerce Network was the earliest to obtain the National Class A Certificate for pharmaceutical e-commerce. As one of the earliest providers of pharmaceutical bidding systems and e-commerce platforms in China, it secured a first-mover advantage. Furthermore, an analysis by year of issuance shows that the number of enterprises approved for Class A certificates remained low before 2015, which indirectly corroborates the assessment that B2B pharmaceutical e-commerce has only entered its growth phase in recent years.

How Do These Three Types of Platforms Differ: Traditional Distribution Enterprises Building Their Own Platforms, E-commerce Giants Entering the Market, and Innovative Internet Companies? Qiu Zhongxun, founder of Yaodou.com, told VCBeat that in terms of the number of enterprises, e-commerce websites built by traditional companies are undoubtedly the most numerous, followed by innovative startup internet companies, and then companies established or participated in by e-commerce giants such as Alibaba and JD.com. However, in terms of activity level, innovative startup companies remain the dominant players.

He believes that although the services provided by the three types of enterprises share certain similarities, there are still slight differences. Enterprises with a B-license primarily focus on operating their own product specifications, while those with an A-license serve as comprehensive platforms, holding greater advantages in terms of product offerings. Furthermore, traditional distribution companies enter the B2B pharmaceutical e-commerce sector to sell their own goods, whereas platform-oriented enterprises aim to build industry chains and ecosystems, serving all links of the pharmaceutical supply and demand chain and acting as an adhesive for the industry.

In terms of specific operations, the aforementioned interviewees all agreed that B2B pharmaceutical e-commerce has introduced little innovation compared to the traditional telephone-based procurement model.

“B2B e-commerce itself does not involve disruption; in fact, the concept of disruption does not exist across the entire business landscape. Business progress is driven by incremental innovation. In the context of B2B pharmaceutical e-commerce, it should be viewed in conjunction with the informatization of pharmaceutical distribution enterprises. When individual companies achieve robust informatization, B2B e-commerce breaks down information silos and establishes connectivity—this is where its value lies,” said He Side, founder of Yaopin Zhongduan Wang (Pharmaceutical Terminal Network).

B2B e-commerce is, at its core, an internet-based tool that embodies the characteristic advantages of digital solutions: “cost reduction and efficiency improvement.” It has displaced the traditional model of telephone-based order placement by enabling direct integration with enterprise information systems. Furthermore, as pharmaceutical procurement is not a low-frequency activity, these transformations deliver tangible convenience and economic benefits.

It is precisely this convenience that has led to growing industry acceptance of B2B pharmaceutical e-commerce, with its market size continuing to expand and its share of the overall pharmaceutical distribution sector steadily increasing.

Since 2015, the Market Statistics Department of the Ministry of Commerce has included a dedicated section on “pharmaceutical e-commerce” in its annual report on the pharmaceutical distribution industry, compiling statistics on the number of pharmaceutical e-commerce enterprises, market size, and their proportion within the overall pharmaceutical distribution sector.

According to its data, based on incomplete statistics, the total sales revenue of pharmaceutical e-commerce enterprises with direct reporting reached RMB 61.2 billion in 2016. Among this, B2B business sales amounted to RMB 57.6 billion, accounting for 94.2% of the total pharmaceutical e-commerce sales; B2C business sales totaled RMB 3.6 billion, representing only 5.8% of the total. The number of active users on B2B platforms reached 270,000, with an average order value of RMB 3,652 and an average of 791 customers per transaction. The daily outbound fulfillment rate for B2B operations was 98.4%, and the average expense ratio was 16.5%, significantly exceeding the industry average.

Data Source: Statistical Bulletin of the Ministry of Commerce

Industry insiders have made optimistic projections regarding market growth. The rationale is that B2B pharmaceutical e-commerce platforms currently primarily serve pharmacies, clinics, and private hospitals, which do not yet constitute the main force in end-user pharmaceutical consumption. In the future, if the marketization of the pharmaceutical sector further advances and B2B pharmaceutical e-commerce platforms gain access to public hospital procurement, the market size will expand significantly.

Naturally, there are reasons why B2B pharmaceutical e-commerce has primarily penetrated the aforementioned medication terminals. First, these terminals exhibit high flexibility in procurement and are willing to adopt B2B pharmaceutical e-commerce as a new channel. Second, B2B pharmaceutical e-commerce can address their existing procurement challenges and optimize their pharmaceutical supply chains.

These two factors apply equally to public hospitals. Models such as Sunshine Procurement and Group Purchasing Organizations (GPOs) share significant similarities with B2B pharmaceutical e-commerce platforms. In other words, B2B pharmaceutical e-commerce can fully or partially replace these existing platforms. However, this transition hinges on the deregulation of procurement in public healthcare institutions. Once such restrictions are lifted, the scale of the B2B pharmaceutical e-commerce market is projected to reach hundreds of billions of yuan.

Issues and Concerns: Industry Ecosystem Is the Key to Breaking Through

Of course, in addition to favorable developments, B2B pharmaceutical e-commerce itself faces numerous constraints. He Side contends that the greatest challenge to the growth of B2B pharmaceutical e-commerce lies in industry acceptance. He notes that traditional pharmaceutical companies, driven by vested interests, are prone to path dependency. Moreover, B2B pharmaceutical e-commerce is characterized by high upfront investments and low returns; from a cost-benefit perspective, traditional pharmaceutical enterprises lack the incentive to pursue new business ventures.

He also noted that following the implementation of policies such as the VAT reform (replacing business tax with value-added tax) and the “Two-Invoice System,” many pharmaceutical companies lost access to certain markets, including hospital-based sales, thereby strengthening their willingness to proactively adapt and expand into new business areas. B2B pharmaceutical e-commerce has provided a viable pathway for these companies, either attracting them to join or encouraging collaboration with B2B platforms.

Qiu Zhongxun also noted that industry acceptance remains a significant challenge. Furthermore, B2B pharmaceutical e-commerce platforms must overcome existing resistance in areas such as service implementation and data integration to achieve growth. He stated that while entering the B2B pharmaceutical e-commerce sector is not difficult, those who delve deeper will discover that it requires substantial investment, involves long supply chains, and is fraught with pitfalls, with no guaranteed returns. Although capital markets are currently very enthusiastic about B2B pharmaceutical e-commerce, it is difficult for these platforms to grow solely on venture capital; they need to identify and establish suitable business models on their own.

He even predicted that the number of B2B pharmaceutical e-commerce companies would decline in the future. “Pure B2B services are too challenging. Unless entrepreneurs are fully committed to this venture, many will halt their efforts or pivot to easier business models due to the difficulties of offline implementation and the demands of comprehensive operations.”

Zhang Yibing stated that if offline markets harbor gray-area activities that cannot be migrated online, this will constrain the development of B2B e-commerce. Regulations governing pharmaceutical e-commerce were introduced early on; the industry’s nascent stage can be attributed to this fact. Only in recent years, with the gradual implementation of policies such as the new Good Supply Practice (GSP), the Two-Invoice System, and the separation of prescribing from dispensing, has the industry ecosystem improved significantly, thereby creating fertile ground for the growth of B2B pharmaceutical e-commerce. The development of pharmaceutical e-commerce is directly correlated with the transparency of pharmaceutical distribution: the higher the transparency, the more likely the industry is to enter a window period of rapid growth.

B2B pharmaceutical e-commerce involves the complete supply chain across manufacturers, distributors, and end-users, encompassing information flows, capital flows, and logistics, forming an integrated platform ecosystem. If restrictions or barriers within this system are not removed, the industry will lack the impetus to upgrade through e-commerce, thereby constraining its development. Furthermore, given that pharmaceutical distribution is a high-volume sector critically linked to human life and health, policy pilots tend to proceed slowly and cautiously. Consequently, restrictions on B2B pharmaceutical e-commerce are unlikely to be lifted rapidly.

From the perspective of breaking the deadlock in healthcare reform, the primary issue to be addressed is the practice of subsidizing medical services with drug profits. Once the separation of prescribing and dispensing is implemented, the gray interests attached to drug distribution will disappear. Healthcare professionals will then be able to secure legitimate income through fee structures that better reflect the value of their labor, thereby fostering a healthy and orderly ecosystem for both medical care and pharmaceuticals. Against this backdrop, the open and transparent market competition represented by B2B pharmaceutical e-commerce will also benefit the healthcare system. From another angle, healthcare system reforms, exemplified by the “separation of prescribing and dispensing,” require not only internal breakthroughs but also market forces to drive change from the outside. In this regard, B2B pharmaceutical e-commerce may become a significant catalyst.

Future: Diversified Development Empowers the Upstream and Downstream of the Pharmaceutical Industry

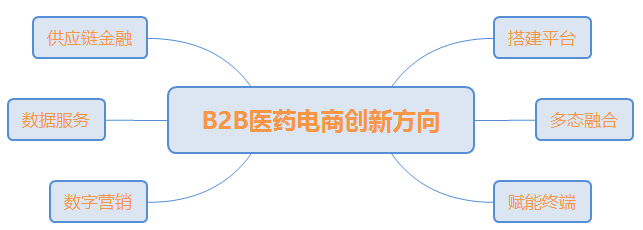

Currently, many B2B pharmaceutical e-commerce companies have launched services such as “data services” and “supply chain finance,” aiming to create more room for growth and strategic focus for the B2B pharmaceutical e-commerce sector. Beyond these two areas, what other development trends can be expected in B2B pharmaceutical e-commerce?

Zhang Yibing stated that supply chain finance and data services are natural extensions for B2B pharmaceutical e-commerce platforms, as both are built upon the foundation of B2B pharmaceutical e-commerce. Once enterprises have transactions and capital flows, they will naturally engage in supply chain finance services; once platforms have sales data, they can use it as a reference for marketing. However, when B2B pharmaceutical e-commerce companies offer these two innovative services, they must be careful not to put the cart before the horse. These services should align with their core business to ensure synergy, enabling the companies to perform well while making client enterprises willing to pay for them.

Qiu Zhongxun proposed several substantive directions and ideas for innovation, which, according to his plan, are what Yaodou.com will implement next. The first is the integration of B2B pharmaceutical e-commerce with pharmacies. By strategically deploying pharmacies within specific regions to serve as last-mile delivery hubs, the supply network of the B2B platform can be enhanced. The second is providing pharmacies with smart terminals. These terminals enable functions such as intelligent cash register operations, order placement, and inventory management (invoicing, sales, and stock control). In the future, they may also offer basic remote medical services, thereby comprehensively empowering pharmacies.

He Side has directed his innovation efforts toward the upstream segment. He believes that while current B2B pharmaceutical e-commerce platforms have significantly improved efficiency and reduced costs, more mature and systematic solutions should emerge now that the necessary infrastructure is in place. For instance, the M2B (Manufacturer-to-Business) model, which connects pharmaceutical manufacturers directly to end-terminals, enables B2B pharmaceutical e-commerce platforms to provide multidimensional services encompassing transactions, marketing, logistics, and financing.

He stated that pharmaceutical manufacturers’ primary objective is to sell their products, while their secondary goal is to expand their sales force. In light of these needs, B2B platforms can provide tools such as online marketing and content marketing to help accelerate the distribution of pharmaceuticals to end-point outlets, including pharmacies.

Currently, B2B pharmaceutical e-commerce platforms should focus on building marketing networks; however, in the future, B2B platforms should revolve around how pharmacies canPutProducts are sold to end consumers. In the future, community clinics and pharmacies will assume greater responsibilities in pharmaceutical services, such as providing chronic disease management for local populations and delivering medical and pharmaceutical services that do not require hospital visits. As a service platform, B2B companies should pay close attention to this shift by offering tools that meet customer needs, thereby helping pharmacies acquire and retain customers. Over the next few years, the pharmaceutical e-commerce industry will trend toward integration, with the boundaries between B2B, B2C, and O2O models becoming increasingly blurred. “Industry leaders will simultaneously possess capabilities across all these models.”

In summary, this article analyzes the B2B pharmaceutical e-commerce industry from multiple perspectives, including policy, current status, challenges, and trends. If one word were to describe this industry, “nascent” would be the most apt characterization. Marked by fluctuations driven by regulatory policies and the persistent exploration of participating enterprises, the industry’s inflection point is quietly approaching amidst the expectations of practitioners.