Does KingMed Diagnostics' IPO Signal the Rise of China's Third-Party Medical Testing and Pathology Industry? Insights from a Review of Nearly 100 Companies

By Luo Mei and Li Yanyu

On September 8, 2017, Guangzhou KingMed Diagnostics Group Co., Ltd. (abbreviated as: KingMed Diagnostics; stock code: 603882) became the third company in the third-party medical testing sector to be officially listed on the Shanghai Stock Exchange, following Daan Gene and Dian Diagnostics.KingMed Diagnostics issued 68.68 million shares in its initial public offering, raising net proceeds of RMB 414 million at an issue price of RMB 6.93 per share; the stock price surged by 44% shortly after market opening.

In fact, KingMed Diagnostics earned its first pot of gold through pathological diagnosis, and has since expanded its business from pathological diagnosis to over 2,400 outsourced testing items and scientific research technical services across six major categories, including physicochemical mass spectrometry testing and genomic testing. It has established a medical laboratory service network covering China, comprising 35 medical laboratories, offering more than 2,400 testing items—far exceeding the capacity of large domestic Grade A tertiary hospitals. The company processes over 40 million test specimens annually, with a compound annual growth rate (CAGR) of its core business exceeding 30%. It collaborates with more than 21,000 medical institutions.

According to the data, from 2013 to 2015, the total operating revenue of China’s third-party medical testing industry increased from RMB 6 billion to RMB 10 billion, and its share of the medical testing market rose from 3% to 5%.However, compared with mature markets in Europe and the United States, China’s third-party medical testing market still lags significantly behind. According to industry data, the share of third-party testing in clinical laboratory services stands at a stable 35% in the United States, 50% in Europe, and 67% in Japan—far exceeding the mere 5% share in China.

As national healthcare reforms continue to deepen and tiered diagnosis and treatment are progressively implemented, measures such as medical consortia, county-level medical communities, specialized alliances, and telemedicine are facilitating the downward flow of high-quality medical resources. Policies also encourage social capital to participate in establishing independent medical institutions, such as clinical laboratory centers and pathology centers. With capital flooding into the sector and growing industry attention, the third-party medical testing industry is poised at a historic turning point, with its market share expected to expand significantly.

In the face of such rapid industry growth, what is the current state of China’s pathology market? Which companies are involved, and what strategies have they adopted to enter the market? What lessons can be drawn from the development of pathology abroad? What are the future trends in the pathology market? To address these questions, VCBeat (WeChat ID: vcbeat) has compiled a list of nearly 100 pathology companies both domestically and internationally, aiming to identify emerging patterns.

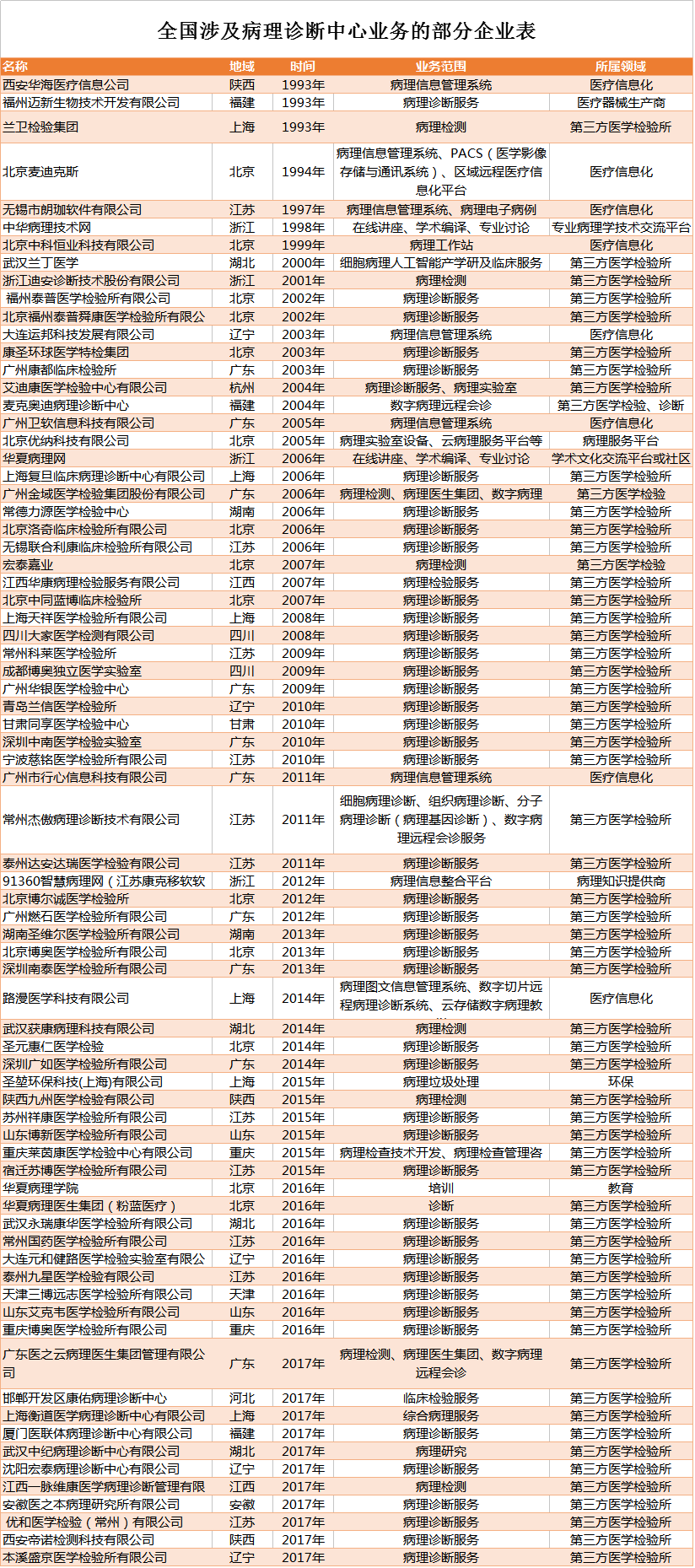

As policies in the pathology sector become increasingly comprehensive, the number of companies involved in pathology-related fields is steadily growing. In terms of their respective domains, these enterprises span medical informatics, third-party clinical laboratories, and education. Regarding their business scope, offerings include pathology information management systems, pathological diagnosis, and educational services. VCBeat has compiled data on the mainstream companies in this industry, as detailed in the figure below:

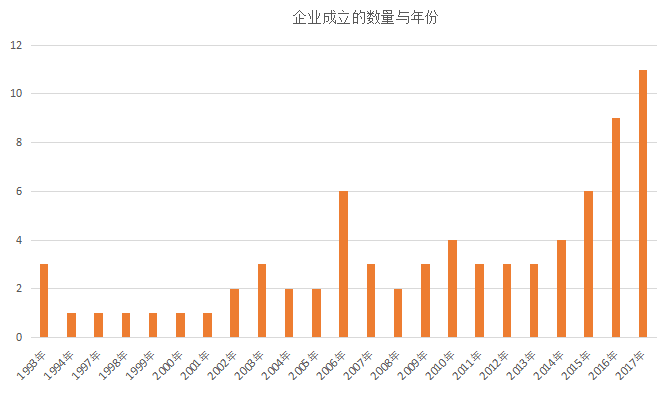

Time vs. Number of Enterprises Established

From a temporal perspective, the first enterprises to enter the pathology field emerged in 1993, with only a modest number of new entrants during the period from 1994 to 2001. After 2011, the Chinese government issued multiple policies related to pathology, leading to a sharp increase in the number of enterprises, particularly with the largest surge occurring in 2017.

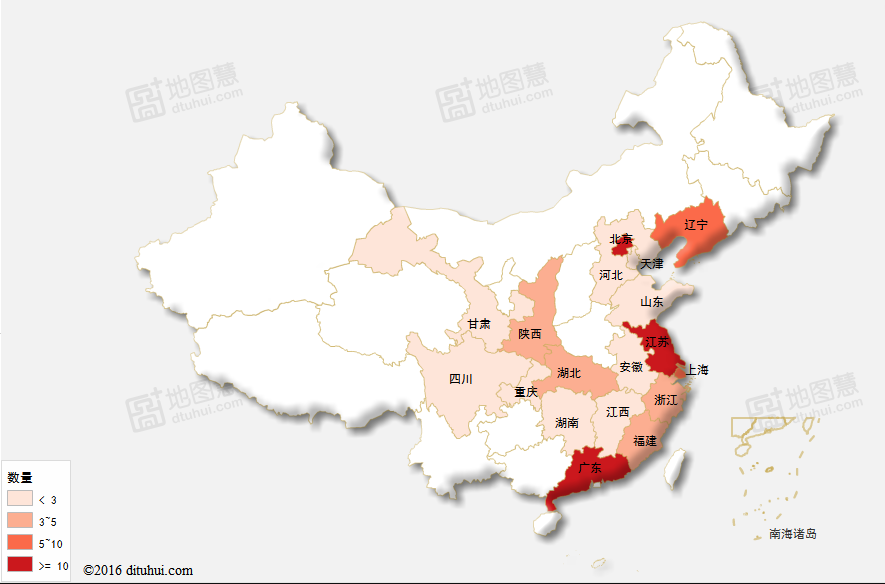

Corporate Geographic Distribution Map

In terms of geographic distribution, companies engaged in pathology-related businesses are spread across 15 provinces and four municipalities directly under the central government, including Beijing, Shanghai, Guangdong, Anhui, Fujian, Gansu, Hebei, Hubei, Hunan, Jiangxi, Liaoning, Shandong, Shaanxi, Sichuan, Tianjin, Zhejiang, and Chongqing. Among these, the highest number of companies have emerged in economically developed coastal regions such as Zhejiang, Beijing, Shanghai, and Guangdong.

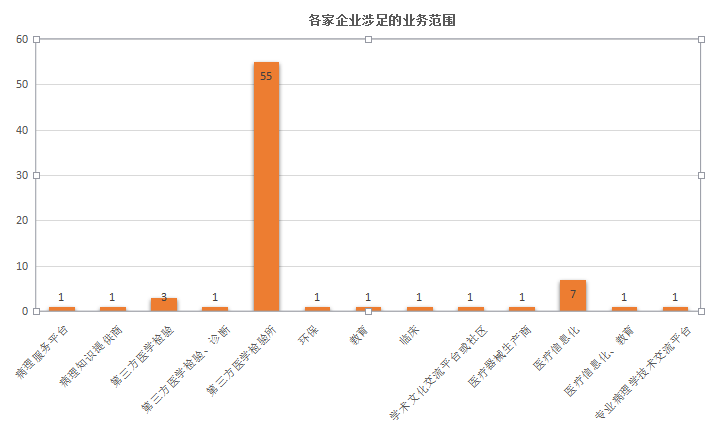

Summary of the Company's Pathology Business

In terms of the pathology sectors involved, these include pathology information management systems, pathology diagnostic services, pathology testing, PACS (Picture Archiving and Communication Systems), regional telemedicine informatization platforms, electronic pathology records, online lectures, academic compilation, professional discussions, pathology workstations, AI-driven cytopathology industry-academia-research and clinical services, and pathology laboratories. Among these, third-party medical laboratory enterprises are the most heavily represented, with 55 companies, followed by seven companies involved in healthcare informatization.

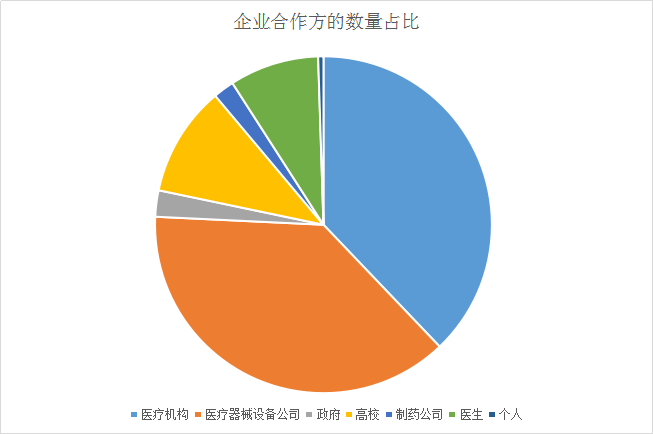

Corporate Partners Overview

From the perspective of corporate partners, collaborations are most frequent with medical institutions and medical device companies, followed by universities and physicians. This indicates that, for enterprises, the primary payers are hospitals. However, pathology diagnostic fees at hospitals are low, and compensation for medical staff is inadequate. Media reports have disclosed that in Shanghai in 2014, the standard fee for pathological diagnosis of a single biopsy specimen was RMB 60, while the actual cost incurred by hospitals exceeded RMB 140. The greater the hospital’s investment, the larger the loss, thereby discouraging further investment. Among more than 100 hospitals in Shanghai, only slightly over 20 had pathology departments of a considerable scale; most other pathology departments were poorly equipped, with some employing merely two or three staff members.

This prevailing situation has spurred the emergence of numerous third-party medical laboratories, such as KingMed Diagnostics, Dian Diagnostics, and Hangzhou Adicon. These enterprises contract with hospitals to provide pathology services and selected testing items, leveraging centralized operations to control costs and enhance testing efficiency.

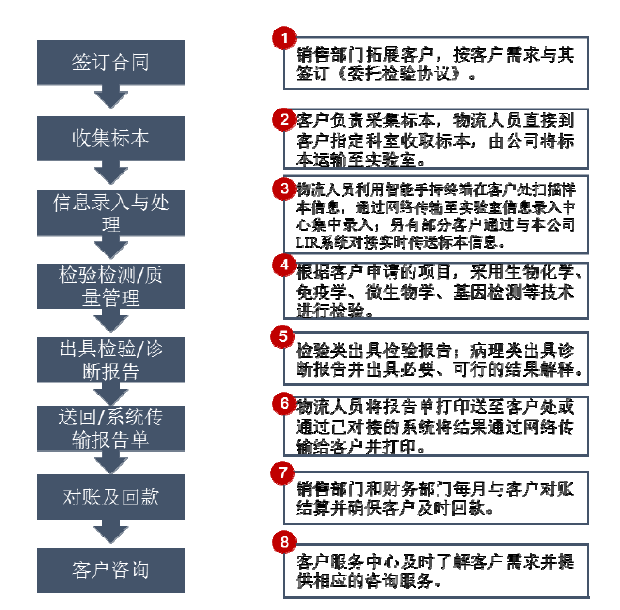

Flowchart of Pathological Diagnosis in Third-Party Medical Laboratory Testing

Among various sectors, third-party medical testing companies are the most numerous. What is the workflow for their pathological diagnostic services? By examining KingMed Diagnostics’ simplified business process, we may find the answer.

As can be seen from the list of images, KingMed Diagnostics’ pathological diagnosis process is mainly divided into contract signing, specimen collection, data entry and processing, testing and quality management, issuance of test/diagnostic reports, return or electronic transmission of report forms, reconciliation and payment collection, and customer consultation.

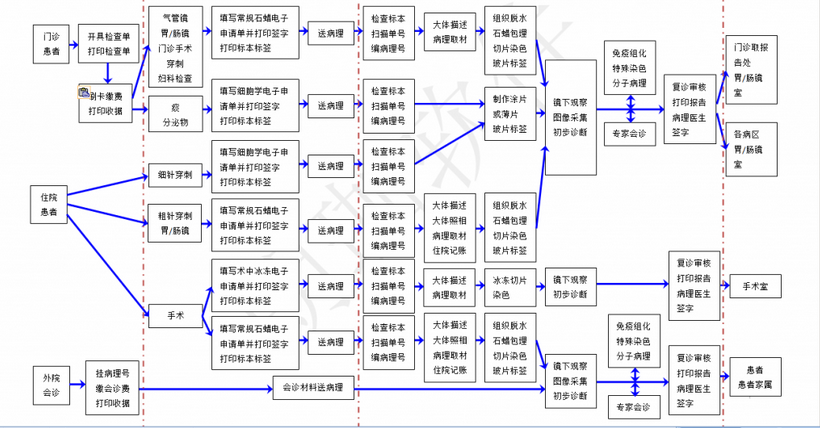

Business Process of Pathology Systems in Medical Informatics

As shown in the figure above, the pathology workflow is more complex compared to other medical technology departments. The implementation of the pathology information system has reduced the manual registration workload for pathologists and minimized the risk of registration errors. It facilitates the acquisition of clinical history, intraoperative findings, and clinical diagnoses, enables the retrieval and verification of details regarding clinical specimens submitted for examination, and ensures the timely feedback of pathology report results or status to clinical departments.

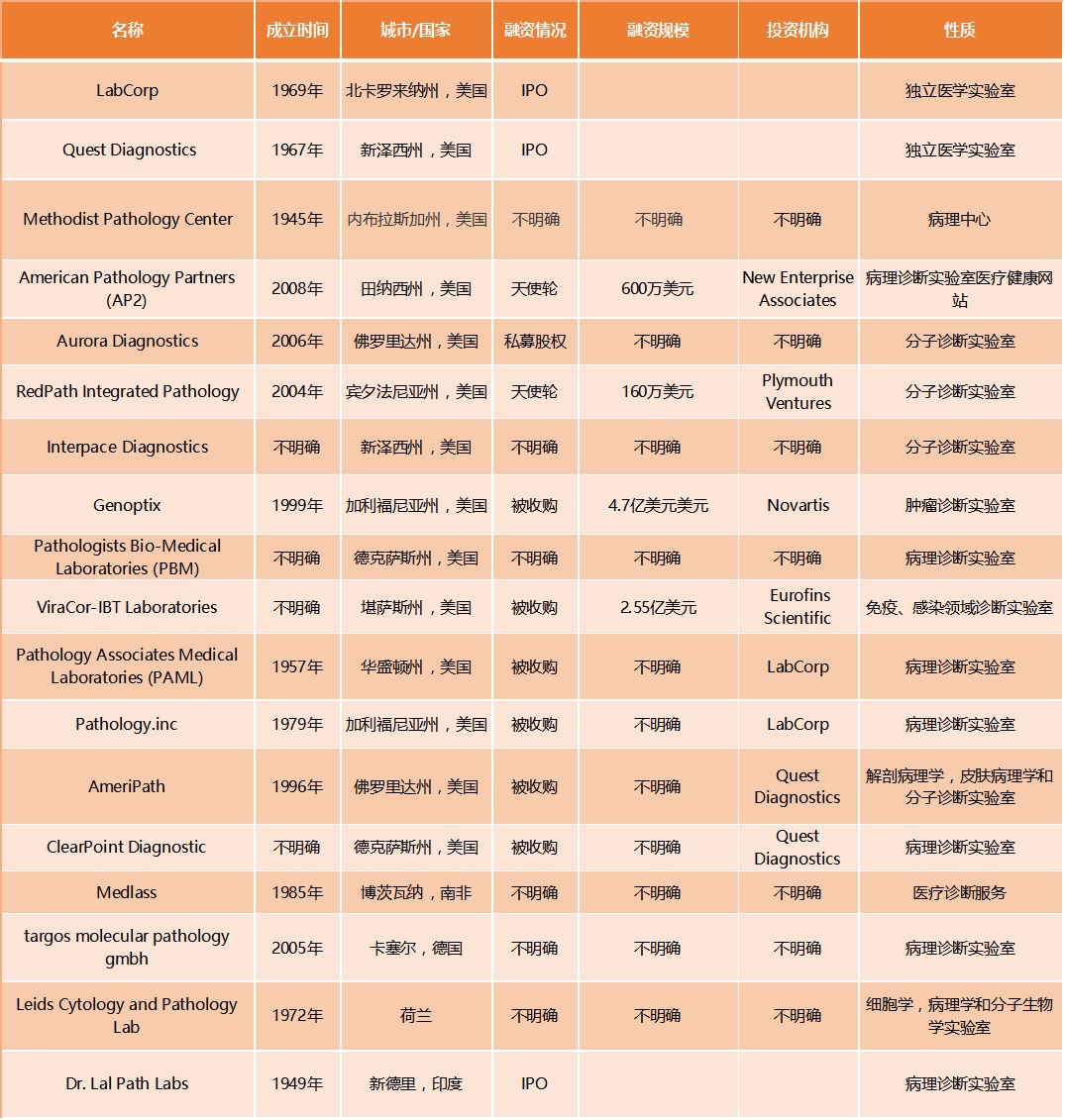

In addition to the domestic market, VCBeat has also compiled data on 18 overseas companies, all of which operate independent clinical laboratories and offer pathology diagnostic services. The majority of these companies are based in the United States and were established relatively early, mostly in the late 20th or early 21st century. For instance, Quest Diagnostics and LabCorp, which hold the largest shares of the third-party clinical testing market in the U.S., were founded in the 1960s and have a history spanning more than five decades.

Among these 18 companies, only the two U.S. giants, Quest and LabCorp, and India’s Dr. Lal Path Labs have achieved IPOs. Dr. Lal Path Labs is a leading diagnostic institution; data released in May 2017 showed that its quarterly consolidated net profit was ₹3.099 billion, with a post-tax profit of ₹15.44 billion for 2016.

Capital penetration in this sector remains limited. In the United States, for example, smaller laboratories are often acquired by industry giants such as Quest Diagnostics and LabCorp, resulting in an oligopolistic market structure. Within this landscape, independent clinical laboratories demonstrate moderate profitability.

From the perspective of the two largest players, Quest and LabCorp, these companies are steadily strengthening their capabilities through continuous mergers and acquisitions to capture greater market share. Currently, in the U.S. independent clinical laboratory market, the two giants, Quest and LabCorp, have essentially formed an oligopolistic competitive landscape.

LabCorp

LabCorp, short for Laboratory Corporation of America Holdings, is the largest third-party clinical laboratory in the United States. As of March 2, 2017, its total market capitalization stood at $14.553 billion, making it the second-largest independent medical testing company in the U.S. The company’s current business offerings include routine clinical testing as well as advanced diagnostic services, such as cancer diagnostics, HIV genotypic and phenotypic testing, and genetic diagnostics. LabCorp operates 36 primary laboratories nationwide, a network of more than 1,600 patient service centers, and an affiliated network that includes STAT laboratories.

In 2016, LabCorp achieved total revenue of $9.6 billion, a year-on-year increase of 11%, with annual net profit reaching $730 million, up 67% year on year. The revenue growth was primarily driven by molecular diagnostics. In July 2016, the U.S. independent third-party laboratory LabCorp announced the acquisition of Sequenom, a molecular testing company, for $371 million.

According to LabCorp’s published business data, testing services are categorized into routine testing (general tests), genetic diagnostics (specialty tests), and pathological diagnostics. Revenue from routine testing grew from $2.778 billion in 2008 to $3.657 billion by the end of 2014 (CAGR = 4.69%), maintaining a stable growth rate. Meanwhile, genomic and specialty testing experienced relatively faster growth, increasing from $1.478 billion in 2008 to $2.026 billion in 2014 (CAGR = 5.40%).

At the end of 2014, LabCorp acquired Covance, the world’s second-largest contract research organization (CRO) for drug development, in a cash-and-stock deal valued at $6.1 billion. This acquisition significantly boosted its total revenue in 2015, surpassing Quest Diagnostics to become the largest clinical laboratory company in the United States.

In May 2017, LabCorp acquired Pathology Associates Medical Laboratories (PAML). Headquartered in Spokane, Washington, PAML is one of the nation’s leading medical diagnostic laboratories and healthcare solutions companies. Following the acquisition, LabCorp gained ownership of PAML’s subsidiaries, including Colorado Laboratory Services (CLS), Kentucky Laboratory Services (KLS), MountainStar Clinical Laboratory (MSCL), PACLAB Network Laboratories (PACLAB), and Tri-Cities Laboratory (TCL).

Quest

Quest, fully known as Quest Diagnostics, is the only third-party laboratory testing company capable of competing with LabCorp. As of March 2, 2017, Quest’s total market capitalization reached $13.398 billion. According to Quest Diagnostics’ 2016 annual report, the company achieved total revenue of $7.5 billion, comparable to the $7.49 billion reported in the same period of 2015. Annual net income was $690 million, representing an 8% year-over-year decline.

As the routine testing market approaches saturation, corporate profitability is primarily driven by high-margin advanced tests, with gene and tissue diagnostics exhibiting a significantly higher compound growth rate than general laboratory testing.

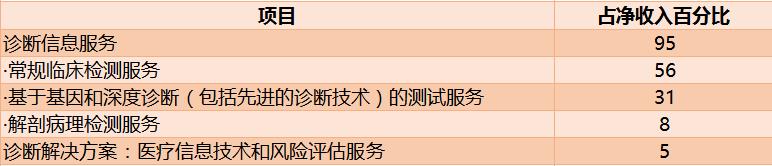

In the Quest 2016 annual report disclosed on the official website of the U.S. Securities and Exchange Commission (SEC), the following data were provided:

2016 Net Income of Quest Diagnostics

Quest comprises two business segments: Diagnostic Information Services and Diagnostic Solutions. As shown in the table above, Diagnostic Services accounted for 95% of Quest’s full-year net revenue in 2016, including routine testing, genetic testing, and anatomic pathology services.

It also provides advanced testing services in fields including endocrinology, immunology, neurology, and oncology, delivering comprehensive diagnostic information to patients, encompassing anatomical pathology and clinical laboratory testing, thereby ensuring complete diagnostic analysis for both patients and clinicians.

Unlike LabCorp, Quest is more inclined to acquire laboratory assets. By acquiring laboratories in different regions across the United States, it strengthens its service capabilities and thereby increases its market share.

On May 31, 2007, Quest acquired AmeriPath, becoming a leading provider of cancer diagnostic testing services. AmeriPath is a supplier of anatomic pathology, dermatopathology, and molecular diagnostic services to physicians, hospitals, clinical laboratories, and surgical centers across the United States. Leveraging a nationwide team of board-certified pathologists and state-of-the-art laboratories, AmeriPath is committed to delivering comprehensive diagnostic solutions, advanced technologies and testing, and superior pathology services to regional and local medical communities. The company employs more than 400 board-certified pathologists and PhDs.

AmeriPath’s subspecialty offerings include: breast pathology, gastrointestinal pathology, genitourinary pathology, gynecologic pathology, hematopathology, and surgical pathology.

Quest operates 31 large regional diagnostic centers, 155 rapid-response laboratories, and more than 2,100 patient service centers in the United States, processing over 100 million specimens annually and offering more than 3,000 diagnostic tests.

A comparison of various segments within the domestic and international pathological diagnosis industries reveals that, driven by supportive national policies, the pathology sector is poised for explosive growth. According to incomplete statistics, since 2017, as many as 11 companies have entered the pathology field.

According to preliminary statistics from the National Health and Family Planning Commission, as of the end of May 2016, a total of six pathology diagnosis centers had been established in Beijing, Zhejiang, and Jiangxi provinces. Among these, four were founded by private capital, and they completed 2.05 million pathology diagnoses.

Under intensive healthcare policies, whether independent pathology centers will become the next major growth opportunity depends on the integration of support services with clinical diagnostics. China’s third-party laboratory and pathology sectors are still in their nascent stages. Based on the current distribution of enterprises operating independent pathology centers in China, tier-3 and tier-4 cities are likely to be the primary battlegrounds for social capital entering the independent pathology testing market, driven by the advancement of tiered diagnosis and treatment. Promoting tiered diagnosis and treatment and facilitating the downward flow of high-quality medical resources align with the original intent of a series of policies issued by the National Health and Family Planning Commission.

Whether China’s pathology industry will evolve into an oligopolistic landscape akin to that of the United States or develop through regional concentration remains to be seen.