130 Pharmaceutical Companies' Interim Reports Reveal Three Key Trends: Strong Market Growth, Cooling M&A Activity, and Intensified Transformation Pressures

Listed companies serve as the best window into an industry, with their performance acting as a barometer of sectoral trends.

According to statistics from VCBeat (WeChat ID: vcbeat), as of August 23, 130 listed pharmaceutical companies had disclosed their semi-annual reports. The data shows that the overall performance of listed pharmaceutical companies remained stable with positive trends, and both revenue and net profit experienced significant year-on-year increases.

On the other hand, driven by major pharmaceutical policies implemented in recent years—such as the consistency evaluation, the two-invoice system, and the comprehensive reform of public hospitals—the business environment for the pharmaceutical industry has undergone dramatic changes. Listed pharmaceutical companies are required to adjust their strategies to adapt to the new industrial landscape, and these shifts are also reflected in their semi-annual reports.

Policy-Driven Industry Transformation and Upgrading

Before delving into the semi-annual report, let us first review the major pharmaceutical policies enacted in recent years to establish a foundational understanding of the macro-level pharmaceutical environment.

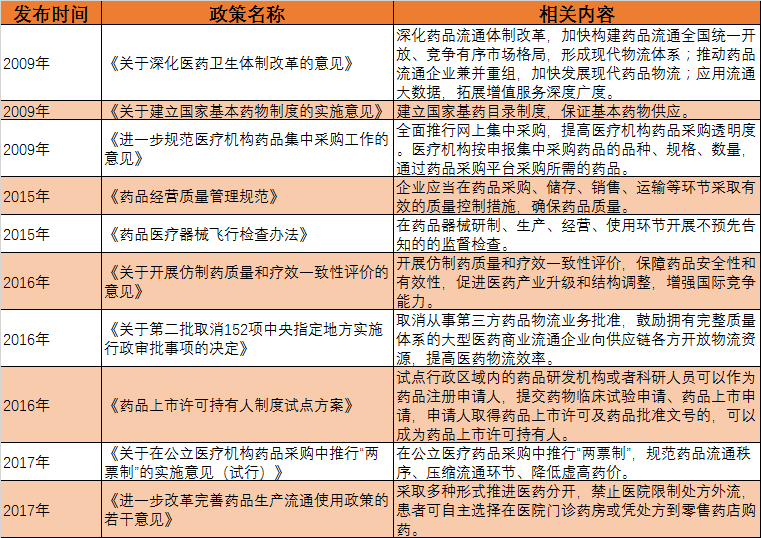

Table 1: Major Pharmaceutical Policies Issued in Recent Years

In March 2009, the State Council issued the “Opinions on Deepening the Reform of the Medical and Healthcare System,” setting forth the overall objectives for deepening healthcare system reform. These objectives included establishing a basic medical care system, improving the public health service system, standardizing drug supply and assurance, and fostering a diversified landscape for healthcare provision, thereby fundamentally defining the framework for healthcare system reform. In the same year, detailed policies were promulgated regarding the essential medicines system, centralized procurement, and reforms of drug and medical service pricing, gradually clarifying the specific implementation measures of the healthcare reform.

In 2015, the introduction of new policies such as the revised Good Supply Practice (GSP), unannounced inspections, and regulations on pharmaceutical distribution directly targeted the standardization of pharmaceutical retail and impacted the structure of pharmaceutical distribution. In 2016, regulatory authorities issued documents including those on consistency evaluation and the Marketing Authorization Holder (MAH) system to adjust the drug supply structure from the perspective of supply-side reform. Since the beginning of this year, the “Two-Invoice System” and Document No. 13 have had a significant impact on the industry. Coupled with the mandate to implement zero mark-up on drugs in all public hospitals by the end of September, pharmaceutical distribution and retail sectors have been further affected.

Overall, since the launch of the new healthcare reform in 2009, China has adopted a comprehensive approach to healthcare system reform. Policies have been progressively refined, the pharmaceutical environment has become increasingly standardized, and the industry has been encouraged to undergo structural adjustment and achieve economies of scale. This constitutes the overarching landscape of the pharmaceutical sector.

The pharmaceutical industry is hailed as an “evergreen sunrise sector,” defying economic cycles with robust endogenous growth momentum. Beyond policy influences, it also benefits from rising national income levels, demographic structural shifts, and heightened public awareness of proactive health management. The confluence of these multifaceted dynamics is clearly reflected in the semi-annual reports.

Semi-Annual Report Conclusion 1: Strong Overall Market Growth

Data shows that the total operating revenue of 130 pharmaceutical companies was RMB 202.512 billion, with a net profit of RMB 20.836 billion.

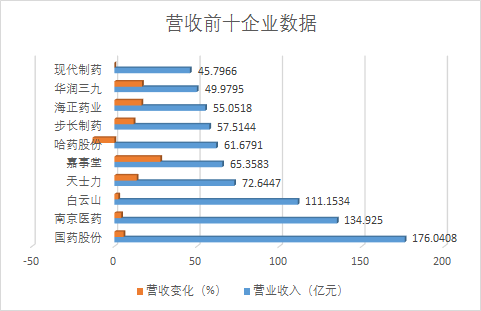

In terms of operating revenue, three companies reported revenues exceeding RMB 10 billion: Sinopharm Co., Ltd., Nanjing Pharmaceutical Co., Ltd., and Guangzhou Baiyunshan Pharmaceutical Holdings Co., Ltd. Among the top ten companies by revenue, eight are pharmaceutical commercial enterprises or derive more than 30% of their revenue from pharmaceutical commerce.

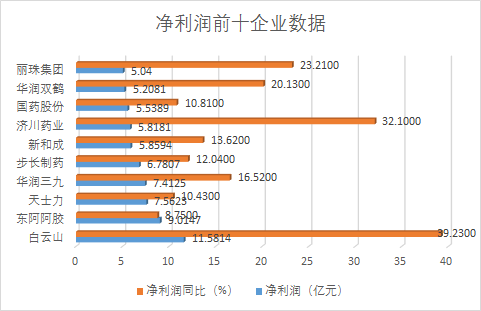

In terms of net profit, Chinese proprietary medicine companies such as Baiyunshan, Dong-E-E-Jiao, Tasly, and China Resources Sanjiu are leading the pack; among the top ten companies by net profit, half are Chinese proprietary medicine enterprises.

In terms of revenue growth rate, companies with a low revenue base demonstrated strong performance. Zhifei Biological Products, Kangtai Biological Products, Chengzhi Share, and Changsheng Biology all achieved year-on-year revenue growth exceeding 100%, three of which had revenues below RMB 1 billion. The top ten companies by revenue growth rate were concentrated in the biopharmaceutical and medical device sectors.

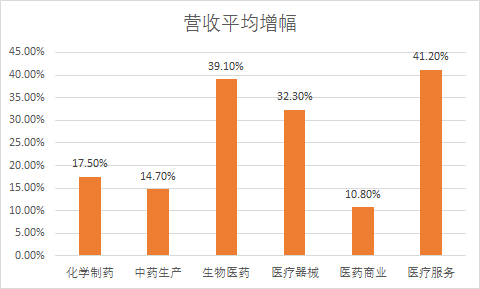

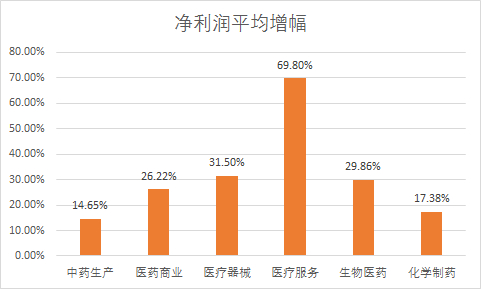

However, revenue data by segment shows that the medical services sector had the highest average revenue growth rate at 41.20%, followed by biopharmaceuticals and medical devices, with average growth rates of 39.10% and 32.30%, respectively. The chemical pharmaceuticals, traditional Chinese medicine (TCM), and pharmaceutical commerce sectors exhibited weaker revenue growth; notably, the pharmaceutical commerce sector recorded the lowest average revenue growth rate at 10.80%.

The average growth rate of net profit also showed a certain correlation with revenue data. By sector, the medical services sector led the industry with an average net profit growth of 69.80%. The medical devices and biopharmaceutical sub-sectors, which ranked high in revenue growth, also maintained high levels of net profit growth, with average rates of 31.50% and 29.86%, respectively. In contrast, the pharmaceutical commerce, chemical drugs, and traditional Chinese medicine (TCM) sectors recorded lower average net profit growth rates. The TCM production segment had the lowest average net profit growth at just 14.65%, approximately one-fourth that of the medical services sector.

According to data from the National Bureau of Statistics, the operating revenue of pharmaceutical manufacturing enterprises above designated size reached RMB 1.451636 trillion in the first half of this year, a year-on-year increase of 12.6%; total profits amounted to RMB 159.63 billion, up 15.9% year on year. In this light, listed pharmaceutical companies that have disclosed their revenue figures have outperformed the macroeconomic averages for the same period published by the Bureau, both in terms of revenue and net profit. This demonstrates the strong growth momentum of listed pharmaceutical enterprises and highlights their leading role within the sector.

In the long term, benefiting from the scaled and structural upgrading of the pharmaceutical market and sustained capital support, listed pharmaceutical companies will continue to maintain rapid growth, thereby feeding back into the industry.

Semi-Annual Report Conclusion II: M&A Trends Decline

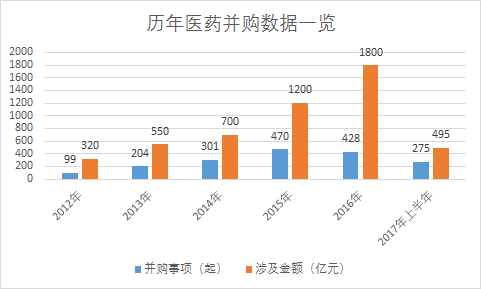

According to data from Choice, as of August 23, a total of 84 listed companies under the A-share pharmaceutical manufacturing sector disclosed 275 mergers and acquisitions (M&A) and restructuring deals, with a total transaction value of approximately RMB 49.581 billion. Previous statistics from VCBeat showed that there were over 400 M&A transactions in China’s pharmaceutical industry in 2016, involving an amount of around RMB 180 billion.

Listed pharmaceutical companies constitute the largest segment within the pharmaceutical manufacturing sector, and these firms essentially represent the full landscape of publicly traded pharmaceutical enterprises. From this perspective, M&A activity in the pharmaceutical industry during the first half of this year reached only about one-quarter of last year’s total, indicating a slowdown in M&A momentum.

Data source: Compiled by VCBeat based on relevant research reports and announcements from listed companies

The decline in M&A activity within the pharmaceutical industry is attributable to the fact that high-intensity mergers and acquisitions in previous years have already identified high-quality targets, thereby reducing available M&A opportunities. Additionally, the resumption of IPOs and the recovery of IPO activity in the pharmaceutical sector have also exerted a certain impact on industry M&A.

VCBeat’s previous statistics showed that IPOs for pharmaceutical companies rebounded in the first half of this year. By the end of July, 25 companies had successfully completed their IPOs, a figure far exceeding the annual totals of the past five years. Disclosure information on initial public offering applications from the China Securities Regulatory Commission (CSRC) also indicated that more than 30 pharmaceutical companies have disclosed their prospectuses, with approximately 10 having already passed the Issuance Review Committee’s approval. It is estimated that the number of pharmaceutical companies listing on the capital market this year will reach 40.

In the first half of the year, the total amount raised by pharmaceutical companies through initial public offerings (IPOs) reached RMB 12.25 billion, surpassing the full-year totals of previous years and representing a twofold increase compared to the RMB 5.818 billion raised in IPOs in 2012. In terms of post-listing performance, the combined market capitalization of these listed companies exceeded RMB 150 billion by the end of July, also surpassing the average levels of previous years, with high-quality stocks such as BGI Genomics, Dashenlin Pharmaceutical Group, and Bio-Kangtai emerging as notable performers.

Based on the progress, among the 275 announced M&A transactions, 131 have been completed, 84 are currently being implemented, and only 17 have been terminated. This indicates a high completion rate for M&A deals announced in the first half of this year, reflecting to some extent the maturity of M&A integration models.

Data also shows that M&A transaction values were highly concentrated in the first half of this year. The top ten M&A deals involved a total amount of RMB 20.809 billion; even after excluding two deals that were terminated, the amount still reached RMB 16.676 billion, accounting for approximately one-third of the total value involved. This further indicates that, amid the recovery trend in M&A activity, both M&A targets and strategic directions have become more concentrated.

Table 2: Top Ten M&A Deals Among Listed Pharmaceutical Manufacturing Companies in the First Half of the Year

Data Source: Choice

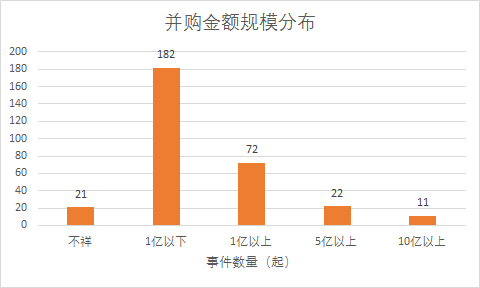

Overall, there were 11 M&A transactions valued at over $1 billion, 22 transactions valued at over $500 million, and 72 transactions valued at over $100 million.

From the perspective of individual companies, Sinopharm Group Co., Ltd. recorded the largest M&A scale in the first half of the year, involving a total of seven companies with a transaction value of RMB 6.144 billion, all of which have been fully completed. The seven companies acquired by Sinopharm Group Co., Ltd. are all Beijing-based subsidiaries of Sinopharm Holdings, engaged in pharmaceutical distribution and retail, imported drug agency services, and hospital channel business, among others. As a company primarily focused on pharmaceutical circulation, this horizontal integration is expected to further expand its operational scale and increase its regional market share.

Livzon Group’s announcement released on July 18 indicated that the industrial and commercial registration changes for the transfer of a subsidiary to Zhuhai Hengqin Weichuang Wealth Investment Co., Ltd., as previously approved by Livzon Group’s shareholders’ meeting, have been completed. The subsidiary was jointly held by Livzon Group and Livzon Pharmaceutical Factory. The transfer, disclosed earlier this year, was executed at a consideration of RMB 4.552 billion. This move represents Livzon Group’s largest external asset disposal in the first half of this year.

Additionally, Humanwell Healthcare’s acquisition of the well-known condom brand “Jissbon” this May has also attracted significant attention. The transaction, jointly funded by Humanwell Healthcare and CITIC Capital, was valued at $600 million. Humanwell Healthcare stated that upon completion of the deal, it would become a global leader in the sexual health sector and the second-largest player in the global condom market, continuing to deepen its presence in the sexual health market.

Concurrently with the acquisition of assets, Humanwell Healthcare divested an 80% equity stake in its wholly-owned subsidiary, Wuhan Zhongyuan Ruide Biological Products Co., Ltd. The transferee was the Asia-Pacific branch of CSL Limited, the world’s largest plasma-derived therapy company, for a transaction consideration of RMB 2.1 billion. This proceeds will significantly improve Humanwell Healthcare’s debt structure and generate cash flow for the company.

Analysis suggests that M&A activities in the pharmaceutical industry will become more prudent in the coming years, driven primarily by horizontal expansion and direct business needs, thereby exhibiting stronger functional orientation. Correspondingly, an increasing number of listed companies will divest assets to focus on their core business scope or to realize investment returns.

Behind the Stabilization of M&A in the Pharmaceutical Industry: Policy Pressures and Industrial Transformation as Key DriversAmid slowing industry growth and significant downward pressure, pharmaceutical mergers and acquisitions (M&A) are approaching an inflection point, driven by policy pressures and the need for industrial transformation and upgrading. The underlying logic of enhancing competitiveness through M&A or asset divestitures remains intact, suggesting that pharmaceutical M&A activity will present new highlights and opportunities.

Analysis of Semi-Annual Report Cases

We selected Sinopharm Group, Baiyunshan Pharmaceutical, and Harbin Pharmaceutical Group as case studies for analyzing semi-annual report performance. These companies were chosen due to their large scale and mature operations, representing the pharmaceutical distribution, traditional Chinese medicine (TCM) manufacturing, and chemical drug manufacturing sectors, respectively. Their annual report data and operational performance provide insights into the general state of the pharmaceutical industry.

Sinopharm Group Co., Ltd. is a subsidiary of Sinopharm Group, with its core business focused on pharmaceutical distribution. Its product portfolio includes Chinese and Western proprietary medicines, narcotic and psychotropic substances, medical devices, and more.

During the reporting period, Sinopharm Group Co., Ltd. achieved operating revenue of RMB 17.604 billion, representing a year-on-year increase of 5.57%. The net profit attributable to shareholders of the listed company amounted to RMB 554 million, a year-on-year growth of 10.81%.

The semi-annual report shows that Sinopharm Group Co., Ltd. has maintained its leading position in the special drug distribution channel for narcotic drugs and Class I psychotropic substances. In the first half of 2017, Sinopharm Group still held more than an 80% market share in the distribution channels for narcotic drugs and Class I psychotropic substances. Following the completion of the company's major asset restructuring in the first half of 2017, key metrics in the Beijing region—including asset scale, sales volume, net profit, market share, and the number of product specifications sold—increased significantly, further strengthening its competitive capabilities.

Sinopharm Group highlighted in its semi-annual report the impact of policies on its performance. The most significant factor was the implementation of Beijing’s Sunshine Procurement Policy for pharmaceuticals, which took effect on April 8. This policy has affected Sinopharm Co., Ltd.’s performance in several ways, including slowed growth in secondary and tertiary hospitals and rapid expansion in community healthcare services.

In the first half of this year, Sinopharm Group Co., Ltd. primarily advanced three key business innovations: promotional services, medical consumables, and e-commerce. In the area of promotional services, represented by entities such as Sinopharm Jiankun, the company intensified its efforts to expand into regional primary healthcare markets. Regarding medical consumables, Sinopharm established Sinopharm Group Beijing Medical Technology Co., Ltd. and obtained a medical device operation license, launching centralized procurement and unified distribution projects for in vitro diagnostics (IVD) and medical consumables with multiple hospitals in Beijing. In terms of e-commerce, the Sinopharm Mall added 1,628 new clients, bringing its total online customer base to 7,844. The platform completed over 10,000 transaction orders this year, representing a 45% year-on-year increase.

Sinopharm Group Co., Ltd. has formulated five strategic development directions for the second half of the year, including expanding business scope, transforming growth models, extending geographic coverage, elongating the industrial chain, and transitioning toward an intelligent model featuring integrated distribution and value-added services.

Sinopharm Group’s performance fluctuations and business adjustments largely reflect the current reality facing domestic pharmaceutical distribution enterprises. Influenced by policies such as the Two-Invoice System and comprehensive reforms of public hospitals, distribution channels and sales terminals are undergoing changes. Consequently, companies are actively pursuing horizontal integration and transitioning from traditional pure-sales distributors to value-added service providers.

Baiyunshan, a subsidiary of Guangzhou Pharmaceutical Holdings Limited (GPHL), operates across four core business segments: the “Greater Southern Pharmaceuticals” segment (pharmaceutical manufacturing), which comprises 26 pharmaceutical manufacturing enterprises and institutions under Baiyunshan, with flagship products including Xiaoke Pills, Huatuo Zaizao Pills, the Kangzhiba antibiotic brand, and anti-inflammatory and antibacterial drugs; the “Greater Health” segment, covering beverages, food, health supplements, and cosmeceuticals, with star products such as Wanglaoji Herbal Tea, Ganoderma lucidum spore oil capsules, and throat lozenges; the “Greater Commerce” segment (pharmaceutical distribution), in which Baiyunshan and its subsidiaries constitute the largest pharmaceutical distribution enterprise in South China; and the “Greater Healthcare” segment, marked by the completion of the acquisition of Guangzhou Baiyunshan Hospital in the first half of this year and the completion and operational launch of the Tibetan-style wellness castle in Nyingchi, Tibet, which was invested in and constructed by the company.

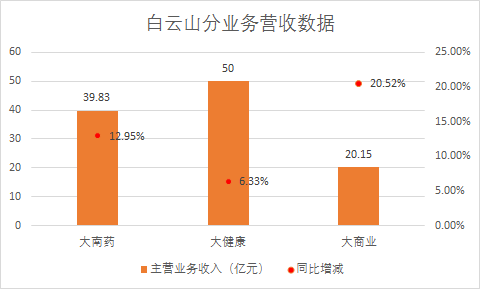

During the reporting period, Baiyunshan achieved revenue of RMB 11.115 billion (unaudited), a year-on-year increase of 2.38%, and net profit attributable to shareholders of the listed company of RMB 1.158 billion (unaudited), a year-on-year increase of 39.23%.

By business segment, the Big Health products segment accounted for the largest share of Baiyunshan’s total revenue, generating approximately RMB 5 billion, a year-on-year increase of 6.33%, with a gross profit margin of 41.17%; the Big Southern Medicine business generated RMB 3.983 billion in revenue, up 12.95% year on year, with a gross profit margin of 46.81%; and the Big Commerce segment recorded revenue of RMB 2.015 billion, a year-on-year increase of 20.52%, with a gross profit margin of 8.45%.

In terms of the Nan Yao brand, Baiyunshan has intensified its efforts in channel development and brand promotion for high-potential products, while closely monitoring key products with sluggish growth and formulating new sales strategies to boost their sales volume. By establishing the concept of “Fashionable Traditional Chinese Medicine,” the sales revenue of related products increased by 50% year-on-year.

Big health products were the focus of Baiyunshan’s operations in the first half of the year. Taking Wang Lao Ji as an example, the brand consolidated and enhanced its market position in the herbal tea industry by expanding channel distribution, advancing modernization, piloting “new-style tea drinks,” implementing differentiated capacity layout, and actively promoting internationalization.

In addition, Baiyunshan’s e-commerce business has also drawn significant attention. Its subsidiary, Caizhilin Pharmaceutical, has officially commenced full operations of its Intelligent Traditional Chinese Medicine (TCM) Decoction Center. Leveraging an efficient “Internet + Internet of Things” model, the center provides TCM decoction services to 16 medical institutions. Baiyunshan Pharmaceutical Sales Company has actively expanded online sales of Baiyunshan Jinge (Sildenafil Citrate Tablets), achieving substantial year-on-year growth in e-commerce channel sales during the first half of the year. Furthermore, its proprietary e-commerce platforms, including Guangyao Jianmin Network and the Guangyao Baiyunshan Tmall store, have seen further development, with sales increasing by more than 30% year on year.

Overall, Baiyunshan’s development path is typical of domestic traditional Chinese medicine (TCM) manufacturers. In its early stages, the company captured market share with exclusive products and secured a stable market position through continuous channel deepening. As growth in pharmaceutical sales stagnated, it actively shifted focus toward health and wellness products, diversifying its business portfolio to adapt to evolving consumer demands. Furthermore, its relatively mature efforts in brand marketing and e-commerce offer valuable lessons for other TCM manufacturers, particularly those producing health and healthcare products.

Harbin Pharmaceutical Group Co., Ltd. listed on the Shanghai Stock Exchange in 1993, becoming the first publicly traded company in China’s pharmaceutical industry and the first listed company in Heilongjiang Province. Its primary business activities include the research, development, manufacturing, wholesale, and retail of chemical pharmaceuticals.

During the reporting period, Harbin Pharmaceutical Group Co., Ltd. achieved operating revenue of RMB 6.168 billion, a year-on-year decrease of 13.31%; and realized net profit attributable to shareholders of the listed company of RMB 348 million, a year-on-year decrease of 8.22%.

Addressing the decline in performance, Harbin Pharmaceutical Group Co., Ltd. stated in its semi-annual report that this was due to several factors: the continued intensification of medical insurance cost containment measures; public hospitals reducing the proportion of drug revenue and abolishing drug markups; diverse forms of drug tendering leading to a continuous decline in winning bid prices; the expansion of bans on outpatient and emergency intravenous infusions to primary healthcare institutions across various regions, alongside further tightening of antibiotic restriction policies; and adjustments to the National Reimbursement Drug List resulting in reduced terminal demand. To ensure the “freshness” of products within the distribution channel, Harbin Pharmaceutical strengthened product expiration date management, increased delivery frequency, and proactively controlled channel inventory, which contributed to the decline in performance.

In the long run, Harbin Pharmaceutical Group’s short-term slump will not persist, as it possesses 69 exclusive products, with 227 varieties and 444 specifications included in the National Essential Medicines List, and 440 varieties incorporated into the National Reimbursement Drug List. Moreover, its flagship products have not experienced a significant decline in market share within their respective niche segments.

In response to the competitive landscape and development trends in the industry, Harbin Pharmaceutical Group Holding Co., Ltd. stated that it would adjust its business operations by focusing on product, management, and marketing initiatives. These efforts include fully mobilizing resources from all parties, accelerating the modular construction at district and county levels, implementing performance indicators at every level, and strengthening refined control over marketing activities; expediting the consistency evaluation process for generic drugs to ensure timely completion of all tasks; intensifying market development efforts while refining and optimizing core markets; and, in the retail sector, using chronic disease management as an entry point to advance such services and pilot a “pharmacy + convenience store” model.

Comprehensive Analysis of the Semi-Annual Report

The above review of the overall performance of listed pharmaceutical companies in the first half of this year, from the perspectives of policy environment, market performance, M&A events, and typical corporate cases, shows that while pharmaceutical companies’ financial results have experienced some fluctuations under the influence of healthcare policies, their overall performance remains robust. Additionally, following the wave of large-scale M&A activity in previous years, M&A transactions in the pharmaceutical market have cooled down, with deals increasingly concentrating on large-sized and high-quality targets. Meanwhile, some companies have begun to divest non-core businesses to sharpen their operational focus and improve cash flow.

From an industry-specific perspective, the pharmaceutical distribution sector is more profoundly affected by policy changes, with its market growth slightly lagging behind other segments. As detailed implementation rules for the “Two-Invoice System” are rolled out across various regions and the zero-markup policy on pharmaceuticals is fully implemented in the second half of this year, pharmaceutical distribution companies will continue to face challenges, which will be directly reflected in their financial performance for the second half of the year.

The chemical drug sector is primarily affected by factors such as health insurance cost containment and channel adjustments. Relevant enterprises need to adjust their marketing strategies, consolidate existing channels while actively exploring new ones, prioritize primary healthcare and out-of-hospital retail markets, and adapt to changes in pharmaceutical consumption channels.

For traditional Chinese medicine (TCM) enterprises, the market competitiveness of exclusive products can provide a certain period of buffer time. Companies can leverage this opportunity to develop big health products—such as healthcare supplements, tonics, cosmeceuticals, and fast-moving consumer goods (FMCG)—thereby capitalizing on the traditional advantages and unique characteristics of TCM to create additional revenue streams and profit sources.

Overall, the pharmaceutical industry is expected to maintain steady growth due to its unique characteristics. Relevant companies should leverage the policy transition window to adjust their operational models and secure long-term growth momentum.