The $15 Trillion Supply Chain Finance Market: Healthcare Emerges as a Key Battleground with Alibaba and JD.com Intensifying Competition

Across various industries, the business ecosystem often features several small and medium-sized enterprises (SMEs) conducting business around a core enterprise. This core enterprise holds a dominant market position and leverages this dominance to exert pressure on SMEs in terms of cash flow, imposing significant financial strain on them.

In the realm of financial services, banks and other financial institutions tend to favor providing lending services to large enterprises with strong repayment capabilities and comprehensive credit records. In contrast, small and medium-sized enterprises (SMEs) often fail to secure loans due to issues such as incomplete credit histories and a lack of robust risk control models, leaving them with no recourse to alleviate their financial pressures.

However, as commercial competition has matured, the preference of financial institutions for large enterprises has gradually revealed its drawbacks. In a fully competitive market, competition is no longer solely the concern of core enterprises; instead, upstream and downstream companies in the industrial chain must cluster around these core enterprises to build stronger competitiveness. At this stage, providing financial services to small and medium-sized enterprises (SMEs) beyond the core enterprises becomes particularly important, enabling the supply chain to operate more healthily and efficiently. Thus, supply chain finance has emerged.

In the era of “Internet Plus,” supply chain finance has witnessed new developments. By leveraging internet technologies to provide trading platforms and solutions for core enterprises and their upstream and downstream partners, it can effectively enhance the efficiency of supply chain finance. With the introduction of innovations such as big data credit scoring and inclusive finance, supply chain finance is gradually revealing a new landscape of development.

In the healthcare sector, supply chain finance services have also seen significant development. Listed company Huaye Capital, internet companies Feiyi Wang, Yijia Yi, and Yilian, along with a number of B2B pharmaceutical e-commerce firms, have all entered the field of medical supply chain finance, offering diversified healthcare supply chain financial services.

VCBeat (WeChat ID: vcbeat) has surveyed the medical supply chain finance services market, aiming to clarify which companies are engaged in this sector, what their specific business processes entail, what bottlenecks they have encountered in their development, and what the future trends will be.

The article is structured according to the following framework, with a total length of approximately 7,000 words and an estimated reading time of 15 minutes.

Part1

1. What is Supply Chain Finance?

2. The Development History of Supply Chain Finance in China and Abroad

3. Current Status of the Domestic Supply Chain Finance Market

Part2

1. Current Status of the Medical Supply Chain Finance Market

2. Pain Points and Development Trends in Healthcare Supply Chain Finance

What is Supply Chain Finance?

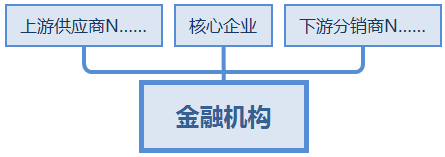

Supply Chain Finance: In simple terms, it is a financing model in which financial institutions such as banks link core enterprises (large enterprises with significant bargaining power in the industrial chain) with their upstream and downstream partners to provide financial products and services.

Generally, the supply chain for a specific product spans from raw material procurement to the production of intermediate and final goods, and ultimately involves the distribution network delivering the products to consumers, thereby integrating suppliers, manufacturers, distributors, retailers, and end users into a cohesive whole.

In this supply chain, core enterprises with strong competitiveness and large scale often impose stringent trade conditions—such as delivery schedules, pricing, and payment terms—on upstream and downstream supporting companies due to their dominant position, thereby exerting significant pressure on these firms.

Moreover, the majority of upstream and downstream supporting enterprises are small and medium-sized enterprises (SMEs) that struggle to secure bank financing, ultimately resulting in severe cash flow constraints and an imbalance across the entire supply chain.

“Supply chain finance” is characterized primarily by identifying a large core enterprise within the supply chain and leveraging it as the focal point to provide financial support to the entire supply chain.

On one hand, it effectively injects capital into upstream and downstream small and medium-sized enterprises (SMEs) that are in a relatively weaker position, thereby addressing the difficulties SMEs face in securing financing and correcting supply chain imbalances. On the other hand, it integrates bank credit into the procurement and sales activities of upstream and downstream enterprises, enhancing their commercial creditworthiness, fostering long-term strategic synergy between SMEs and core enterprises, and ultimately boosting the competitiveness of the supply chain.

By role, supply chain finance involves several types of participants—financial institutions, core enterprises, small and medium-sized enterprises (SMEs), and supporting enterprises—each with distinct functions.

The role of financial institutions is to identify core enterprises within the supply chain, design supply chain finance models based on these entities, and provide financial support. Supporting enterprises primarily offer services such as resource matchmaking, document verification, and credit endorsement.

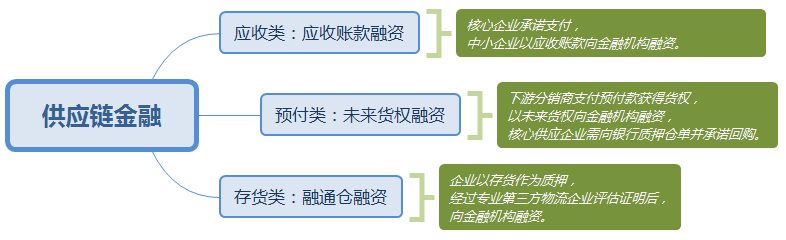

From the perspective of financing models, supply chain finance primarily includes three types: accounts receivable financing, prepayment-based financing, and inventory-based financing.

Accounts Receivable Financing refers to a financing model in which small and medium-sized enterprises (SMEs) upstream and downstream in the supply chain can obtain loans from financial institutions using their unmatured accounts receivable, contingent upon the core enterprise’s commitment to payment.Accounts receivable financing can address the short-term funding needs of small and medium-sized enterprises (SMEs) and facilitate efficient supply chain operations.

Prepayment financing is also known as confirmed warehouse financing.Targeting core suppliers+Multi-downstream Buyer Supply Chain Model: In this structure, downstream buyers often do not receive physical goods immediately after payment but have already acquired ownership of the goods. When such enterprises require financing, they pledge their future ownership rights as collateral to obtain loans from financial institutions. Meanwhile, the core supplier pledges warehouse receipts to the financial institutions and commits to repurchasing the goods if the downstream buyers fail to make payments, thereby reducing the risk of debt default for the financial institutions.

Inventory-based financing targets enterprises that lack accounts receivable and other forms of corporate credit guarantees. When such enterprises have financing needs, they pledge their inventory as collateral and, after assessment and certification by professional third-party logistics providers, obtain loans from financial institutions.

In practice, the aforementioned financing models can be integrated to create comprehensive financing solutions involving multiple enterprises across the supply chain. For instance, accounts payable financing can be selectively incorporated into inventory-based financing models to mitigate the risks associated with relying on a single financing approach.

In summary, the hallmark of supply chain finance is the shift from serving individual enterprises to considering the supply chain as a whole. Upstream and downstream companies form a community of shared interests, addressing creditworthiness challenges for financing entities through mutual guarantees and credit extensions. This approach allows capital to act as a solvent within the supply chain, thereby facilitating its efficient operation.

The Evolution of Supply Chain Finance

Let us first examine the development trajectory of supply chain finance abroad. Its evolution has roughly undergone three stages. The first stage was characterized by loan businesses primarily based on single-commodity inventory pledges, which originated relatively early, dating back to the 19th century. After the mid-19th century, financing models such as accounts receivable financing began to emerge, enriching the service offerings of supply chain finance. Since the 1980s, supply chain finance has progressively flourished, with the introduction of financing products including prepayment financing, settlement services, and insurance. Meanwhile, given that supply chain finance largely serves commodity trading, logistics enterprises have played a pivotal role. Following the high concentration of logistics operations, capable logistics companies began to participate in supply chain finance services, providing additional services to banks and small and medium-sized enterprises (SMEs), such as collateral assessment, supervision, disposal, and credit guarantees. Consequently, an operational philosophy of “logistics as the core, finance as the supplement” emerged in supply chain finance.

Domestic supply chain finance services emerged in the late 1980s. After 2000, the logistics industry underwent major consolidation, with large logistics enterprises partnering with financial institutions to launch supply chain finance services centered on logistics.

A notable case in retrospect is that in 2005, Shenzhen Development Bank successively signed “headquarters-to-headquarters” strategic cooperation agreements with China National Foreign Trade Transportation (Group) Corporation, China National Materials Storage and Transportation Corporation, and China Ocean Logistics Co., Ltd. In that year, Shenzhen Development Bank’s “1+N” supply chain finance model achieved a credit facility of RMB 250 billion, contributing approximately 25% of the bank’s business profits, with a non-performing loan ratio of 0.57%.

Feng Lei, General Manager of Beijing Xingde Technology Development Co., Ltd., introduced to VCBeat that supply chain finance in China has roughly gone through several stages.

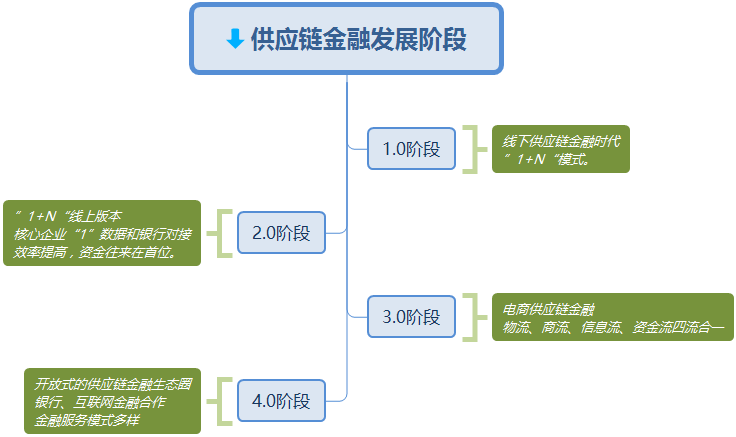

Supply Chain Finance 1.0: The Era of Traditional Offline Supply Chain FinanceThe model of supply chain finance is broadly summarized as “1+N,” where banks provide financing and credit support to a cluster of small, micro, and medium-sized enterprises (“N”) based on the credit backing of the core enterprise (“1”). There are two major risk challenges in offline supply chain finance: first, banks struggle to verify the authenticity of inventory quantities and find it difficult to detect duplicate collateralization; second, there are operational risks arising during business operations.

Supply Chain Finance 2.0 Stage. This is the online version of the “1+N” model, where traditional offline supply chain finance is migrated online. It enables the core enterprise (“1”) to integrate its data with banks, allowing banks to access real-time, authentic operational information—such as warehousing, procurement and sales, and settlement data—of both the core enterprise and its upstream and downstream partners in the industrial chain. Online supply chain finance facilitates efficient multi-party online collaboration and improves operational efficiency. However, its core remains bank-centered financing, with fund flows prioritized by default.

Supply Chain Finance 3.0: E-commerce Supply Chain Finance (Integration of the Four Flows). Supply Chain Finance 3.0 is finance based on the e-commerce model, summarized as the online “M+1+N” model. Its main feature is the e-commercialization of financial services, wherein logistics tightly integrates cargo ownership with capital flows, thereby financializing logistics. The establishment of e-commerce cloud service platforms has disrupted the previous supply chain model centered on financing, shifting the focus to the enterprise’s transaction process. Banks are also gradually changing their approach by building e-commerce cloud service platforms that host SMEs’ operational activities—such as order processing, waybill management, payment acquisition, financing, and warehousing—while introducing logistics providers and third-party information services to offer supporting services. In this system, core enterprises play a role in credit enhancement, making various transaction data more credible.

The Era of Supply Chain Finance 4.0. The 4.0 era is characterized by an open ecosystem for supply chain finance, which comprises two segments. The first involves large e-commerce players integrating their platforms with proprietary financial services for supply chain finance. The second pertains to small and medium-sized e-commerce enterprises (SMEs). As these SMEs are unable to build their own financial systems, opportunities for collaboration with banks and internet finance providers have emerged. In particular, peer-to-peer (P2P) lending, third-party payment platforms, and crowdfunding models within the internet finance sector can all partner with e-commerce businesses. Cross-industry win-win cooperation is a distinctive feature of internet finance, primarily involving mutual integration and support. The advent of Supply Chain Finance 4.0 has brought an end to the era of relying exclusively on traditional bank financing. Now, thanks to the well-developed ecosystems formed by internet finance service platforms, small and medium-sized e-commerce enterprises can gradually reduce their dependence on funding from traditional financial institutions.

“From an evolutionary perspective, Supply Chain Finance 4.0 is an inevitable trend; only a fully open, integrated, ecosystem-based supply chain finance model is best suited to current and future markets,” said Feng Lei. He believes that future supply chain finance models will become more open and integrated, with more diverse service offerings. The integration of information, logistics, commercial, and capital flows will enable coordinated efforts with financial institutions to enhance supply chain finance services, address financing challenges for small and medium-sized enterprises (SMEs), optimize capital allocation within supply chains, and boost competitiveness.

Current Status of the Supply Chain Finance Services Market

Due to the large number of industries and companies involved, as well as the diverse business models, there is currently no precise data on the market size of supply chain finance in China.

However, according to forecasts by the Qianzhan Industry Research Institute, the market size of China's supply chain finance services was RMB 15 trillion in 2015. At an annual growth rate of 5%, the market size is projected to reach approximately RMB 15 trillion by 2020.

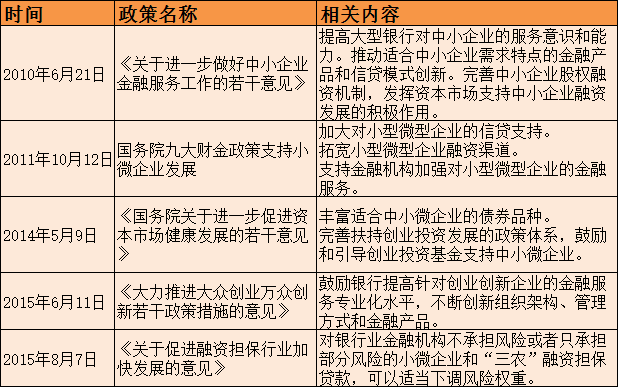

From a policy perspective, the development of supply chain finance services is also highly favorable. First, policies encouraging the growth of small and medium-sized enterprises (SMEs) have significantly promoted their development; second, policies related to financial service innovation have paid considerable attention to supply chain finance services.

Here, we have selected several relevant policies, which illustrate the regulatory authorities’ orientation toward small and medium-sized enterprises (SMEs) and supply chain finance services.

Currently, entities providing supply chain finance services in China mainly include commercial banks, e-commerce platforms, factoring institutions, and P2P lending platforms. Taking factoring institutions as an example, according to statistics from the Commercial Factoring Professional Committee of the China Association of Trade in Services, the number of registered commercial factoring companies in China reached 5,593 by the end of 2016, with 2,757 newly added during the year, representing a 92% year-on-year increase compared to 2015.

Among A-share listed companies, Hand Enterprise Solutions, Huaye Capital, Hongda Xingye, Ruimao Tong, Xiamen ITG Group, and China Light & Textile Industrial City are engaged in supply chain finance-related businesses, covering sectors including mining, international trade, healthcare, and supermarket retail.

Of course, the companies with the most prominent voice in supply chain finance services are still those that originated from e-commerce, such as Alibaba and JD.com.

Let’s start with Alibaba. Since 2002, Alibaba has been building credit models for small and medium-sized enterprises (SMEs). By 2007, Alibaba partnered with China Construction Bank and Industrial and Commercial Bank of China to provide credit services to SMEs. In 2011, Alibaba established Alibaba Microfinance in Chongqing, independently offering supply chain financial services to merchants on its platform. In 2014, Ant Financial was officially founded, and the following year, MYbank, initiated by Ant Financial as the majority shareholder, formally commenced operations, with serving micro and small enterprises as its core mission. According to MYbank’s 2016 annual report, by the end of 2016, MYbank had cumulatively issued RMB 87.9 billion in loans to micro and small enterprises, serving 2.77 million such enterprises, with an average loan balance of RMB 15,000 per enterprise.

Where Alibaba has a presence, JD.com naturally follows suit. JD.com’s foray into supply chain finance began in 2012, initially adopting a model of collaboration with banks. In 2013, JD.com started providing supply chain finance services independently.

JD.com’s flagship supply chain finance product is “Jingbao Bei,” a service developed based on JD.com’s accumulated expertise in supply chain financing. Platform suppliers of JD.com can obtain automated approval by leveraging their procurement, sales, and financial data, with the entire process from application to disbursement taking as little as three minutes, thereby enabling truly rapid financing. According to official data from JD Finance, as of March 2017, JD Finance’s supply chain finance services had cumulatively served over 100,000 enterprises, providing RMB 250 billion in loans, the vast majority of which were extended to micro, small, and medium-sized enterprises (MSMEs).

In the healthcare sector, JD Finance has also made strategic inroads. According to the official website of Yaojingcai, JD Health’s pharmaceutical procurement platform, JD Health offers “Baitiao” financial services to purchasers. Promotional materials for “Pharma Baitiao” state that it provides exclusive buy-now-pay-later options for drug procurement, with a maximum credit line of RMB 500,000 and interest-free repayment within 30 days.

Current Status of the Medical Supply Chain Finance Services Market

Broadly speaking, the market for healthcare supply chain finance services has not yet achieved significant scale or a systematic structure, with limited corporate participation and relatively small transaction volumes.

Addressing this phenomenon, Sean Daxia, Managing Director of Huagai Medical Fund, stated that due to the lengthy industry chain, bargaining power varies among different institutions and enterprises.Many enterprises across the medical industry supply chain face financing difficulties, such as insufficient collateral and guarantees, information asymmetry in credit data, and weak risk resilience.

Healthcare enterprises (including hospitals, particularly government- and enterprise-affiliated hospitals) urgently require the participation of capital from various sectors. In recent years, the rapid liberalization of policies and market competition have alleviated some of these issues to a certain extent, while new financing models and technological approaches have also provided multifaceted support.

One emerging financing model is healthcare supply chain finance, a financial service framework tailored to the actual funding needs of individual enterprises within the supply chain. Alternatively, it involves providing pledge-based financing against accounts payable and receivable, inventory, and other assets of small and medium-sized upstream and downstream enterprises, based on assessments of their payment capacity and credit support, thereby delivering comprehensive financial services to one or multiple pharmaceutical companies across the supply chain.

Xiaoda Xia said,Currently, some domestic trade-oriented (circulation) listed companies have made beneficial explorations in supply chain finance business.Given their long-term involvement in the logistics of medical equipment and pharmaceutical distribution, these entities serve as a critical link between numerous pharmaceutical manufacturers and hospitals. In some cases, trading companies even act directly as distributors of pharmaceuticals and medical devices for certain hospitals, participating directly in bidding processes. They possess an in-depth understanding of hospital payment cycles and manufacturers’ collection policies, thereby naturally positioning them to establish financing channels that address funding gaps arising from manufacturers’ advance payments and hospitals’ accounts receivable.

Meanwhile, by having access to information on hospital fundraising, fund disbursement, and patient volume, it can forecast hospitals’ repayment capacity. When providing financing services to small and medium-sized enterprises (SMEs), it is able to assess financing risks. Furthermore, as a listed company, it has diverse financing instruments, ensuring ample capital support for its lending activities. In short, it “has the financial strength and capability to control risk.”

The financing models offered by such trading enterprises fall into two categories: transaction-based financing and financial financing. Transaction-based financing includes three types: providing short-term loans to manufacturers’ distribution agents to support inventory procurement, factoring distributors’ accounts receivable from hospitals, and offering credit sales to hospitals on an installment basis. Financial financing refers to financing methods such as financial leasing and microloans provided by traders with partial financial licenses to agents and private hospitals. Currently, the number of traders engaging in financial services through this approach is gradually increasing.

In addition to the aforementioned models, there are also supply chain models for pharmaceutical procurement involving multiple pharmaceutical companies and hospitals; financial leasing models tailored to the medical device industry; online B2B models for pharmaceutical distribution; models for hospitals such as leasing instead of financing and joint investment-financing-lending schemes; and systematic business models for (pharmaceutical or hospital) group corporations, among others.

Here, we use the case of Huaye Capital to interpret the specific operational model of medical supply chain finance.

Huaye Capital was previously a second-tier real estate developer, with business operations distributed across six core cities including Beijing and Shenzhen. In June 2015, Huaye Capital acquired Chongqing Jieer Medical Equipment Co., Ltd. for RMB 2.15 billion using its own funds. Jieer Medical’s core businesses are the distribution of pharmaceuticals and medical devices, as well as healthcare services. After Huaye Capital took control, it began expanding into the healthcare sector and healthcare supply chain financial services.

From a business model perspective, Huaye Capital provides medical supply chain financial services by purchasing accounts receivable from suppliers of Grade A tertiary hospitals at a discount, thereby offering financing to upstream suppliers. It then collects payments from the hospitals upon maturity of these receivables or sells them to financial institutions through asset securitization.

Huaye Capital’s 2017 semi-annual report showed that the total scale of its medical finance platform reached nearly RMB 9 billion, and its subsidiary Guorui Minhe, together with Tibet Huashuo, recognized RMB 385 million in investment income from investments in medical supply chain finance.

Pain Points and Development Trends in Medical Supply Chain Finance

The case of Huaye Capital demonstrates that medical supply chain finance can generate substantial investment returns. Consequently, capital has begun to flock to the medical supply chain finance services market. In addition to traditional financial service models, “Internet+” medical supply chain finance has emerged as a critical entry point, with participants including B2B pharmaceutical e-commerce platforms, as well as information technology platforms and solution providers specializing in supply chain finance services.

Feng Lei, General Manager of Beijing Xingde Technology Development Co., Ltd., believes that while different supply chain finance service models are essentially designed to address corporate financing challenges, there are variations in their practical application depending on the source of funds and the identity of the operator.

For example, the “e-commerce + supply chain finance” model is closed-loop within the industrial chain, conducting business exclusively with its own upstream and downstream partners. Its advantages include facilitating the integration of the four flows (information, capital, goods, and documents), as enterprise data verification is conducted on the company’s own e-commerce platform, making it easier to control and operate. Furthermore, supply chain finance operations help stabilize relationships with upstream and downstream partners.

In terms of funding sources, one approach relies on the operator’s own capital with full self-investment, akin to the well-capitalized e-commerce models of Alibaba and JD Finance; the other involves introducing external capital or collaborating with third-party supply chain finance platforms. Small and medium-sized e-commerce enterprises generally adopt the latter approach. The “Trading Platform + Supply Chain Finance” model is similar to this.

Ou Jianxiong, co-founder of Feiyi.com, stated in an interview with VCBeat that medical supply chain finance is not a new business sector; previously, some companies had already been engaged in this area, including traditional factoring and accounts receivable financing.However, traditional businesses face challenges such as difficulties in customer acquisition, cumbersome processes, and complex risk control, making it difficult to achieve scalability.

“In traditional business practices, many institutions rely on static data and must conduct on-site inspections to verify operational conditions, transaction records, and other metrics. However, such offline inspections leave room for manipulation, posing significant risks and entailing high verification costs for banks and other financial institutions,” he stated.

Therefore, Feiyi.com has adopted a strategy of entering the market by building an electronic trading platform. It provides a transaction platform for hospitals and upstream suppliers, accumulating transaction data as the foundation for financial services.

“The supply chain finance services we refer to are based on big transaction data. We do not launch such services outright; instead, by leveraging the massive volume of transaction data accumulated in the early stages, we can provide decision-making support for financial services, including credit enhancement, verification of transaction authenticity, and risk control.”

However, the development of medical supply chain finance services currently faces significant constraints. A securities analyst told VCBeat that, compared to other sectors,The main challenge in implementing medical supply chain finance services lies in the difficulty of gaining access to hospitals.Hospitals are not enterprises; they inherently lack motivation in financial services, and supply chain finance does not bring them substantial benefits. However, processes such as confirmation of rights require hospital cooperation, making implementation quite challenging.

Furthermore, the “Internet+” supply chain finance model imposes certain requirements on hospital informatization, including the digitalization of material management and the electronic processing of financial operations; however, hospitals still lack sufficient investment in these areas.

As public hospital reforms are gradually advanced, these restrictive factors are being progressively dismantled. For instance, the "Guiding Opinions of the General Office of the State Council on Pilot Comprehensive Reforms of Urban Public Hospitals" stipulates that hospitals should promote refined management. Coupled with the implementation of policies such as the "Two-Invoice System" and "Zero Markup," pharmaceuticals and other medical supplies have increasingly become cost items for hospitals. This creates an incentive for hospitals to control costs in material procurement and financial management. The information management tools and financial services provided by "Internet Plus" supply chain finance have alleviated cost pressures on hospitals.

So, how large is the medical supply chain finance market? Reference can be drawn from data on hospital material expenses. According to the China Health Statistics Yearbook, there were 12,897 public hospitals nationwide in 2014, with an average revenue of RMB 146 million and material expenses of RMB 122 million. Based on a projection assuming the same growth rate as that observed from 2014 to 2016, national hospital procurement spending on materials was expected to reach RMB 1.3–1.5 trillion in 2017. Assuming that 20%–30% of this amount requires financial services,The market size of medical supply chain financial services is expected to reach RMB 300-500 billion in the long term.

Based on the above information, it can be concluded that supply chain finance, as an emerging financing model, boasts substantial market potential and has attracted significant attention from financial institutions (including banks), logistics companies, and core enterprises. Against the backdrop of the “Internet Plus” initiative, e-commerce giants such as Alibaba and JD.com have leveraged their platform advantages to provide extensive and in-depth supply chain finance services across various industries. In vertical sectors, the healthcare industry, driven by its high growth trajectory and policy-supported reforms, offers a highly fertile ground for supply chain finance solutions. Healthcare supply chain finance is still in its early stages—akin to “a young lotus just revealing its tip”—and holds immense potential for future development.

References:

Supply Chain Finance - MBA Wiki

http://wiki.mbalib.com/wiki/%E4%BE%9B%E5%BA%94%E9%93%BE%E9%87%91%E8%9E%8D

Logistics Finance - MBA Wiki

http://wiki.mbalib.com/wiki/%E7%89%A9%E6%B5%81%E9%87%91%E8%9E%8D

Trillion-Dollar Blue Ocean: A Comprehensive Analysis of Supply Chain Finance Essentials

http://www.gold678.com/dy/A/2847874

Supply Chain Finance Market Analysis Report