Is Sports Rehabilitation a Blue Ocean or a Bitter Sea? Targeting 100 Million Injured Individuals with Offline-Centric Services

Among many sports rehabilitation practitioners, the concept of “integration of sports and medicine” is frequently discussed. Although this term may still be unfamiliar to the general public in China, it embodies the convergence of sports and healthcare. At the national level, both “sports” and “medicine” are indispensable components in efforts to promote the physical fitness and health of the population.

Since State Council Document No. 46 explicitly called for “vigorous development of sports medicine and rehabilitation medicine,” official agencies represented by the General Administration of Sport and the Ministry of Health have successively introduced implementation policies, seemingly providing clear direction for entrepreneurs in sports rehabilitation. However, despite these favorable policy conditions, China’s sports rehabilitation sector remains in a state where it garners acclaim but fails to attract substantial market demand.

Some industry observers believe that the sports rehabilitation sector is an untapped “gold mine,” yet the limited influx of capital reflects its current niche status. VCBeat (WeChat ID: vcbeat) has examined developments in the sports rehabilitation field, compiled policies guiding its growth, and analyzed talent supply and demand as well as corporate strategic layouts to gain insights into the sector’s development trends.

Overview of the Sports Rehabilitation Market

Rehabilitation medicine, together with preventive medicine, clinical medicine, and healthcare medicine, is defined by the World Health Organization (WHO) as the fourth category of medicine. Sports rehabilitation, discussed in this article, is a branch of rehabilitation medicine. Its essence lies in the integration of “sports” and “medicine.” As an interdisciplinary field, it employs various approaches—including equipment-based rehabilitation, manual therapy, and active patient exercises—to repair sports injuries and restore motor function. The target populations include individuals with musculoskeletal injuries and post-orthopedic surgery patients; those with chronic diseases; and the elderly, adolescents, and individuals in a sub-health state.

First, let us examine the traditional rehabilitation industry chain. Overall, the traditional rehabilitation industry chain can be divided into three segments:

Upstream: Rehabilitation equipment manufacturers, rehabilitation drug manufacturers

Midstream: Sports medicine or rehabilitation departments in general hospitals (with a severe shortage of sports rehabilitation service capacity), and specialized rehabilitation institutions

End Users: Consumer Side (C-end) – Competitive Athletes and Public Sports Rehabilitation; Business Side (B-end) – Sports Event Medical Support.

Sports rehabilitation is service-oriented, occupying the midstream segment of the industry chain. Entrepreneurs in this field, whether operating online or offline, primarily focus on service delivery. Although there are providers of rehabilitation equipment, such companies mostly adopt traditional sales models to serve B-end supply and demand and thus fall outside the scope of VCBeat’s analysis. The following section only lists selected equipment/device providers involved in business transformation.

In China, early sports rehabilitation primarily referred to medical services targeted at professional athletes, along with rehabilitative physiotherapy for a very small number of middle- and high-income individuals. However, with the widespread adoption of national fitness initiatives, emphasizing scientific exercise has gradually become a trend. Sports rehabilitation is shifting from a niche market catering to professional athletes toward a mass market serving sports enthusiasts.

The outlook is promising, but the numbers are far from encouraging.

Public data indicates that the number of people in China who regularly participate in physical exercise has reached 500 million. According to conservative estimates by industry experts, approximately 20% of these individuals experience varying degrees of injuries each year, implying that 100 million people require treatment and services for sports-related injuries and conditions. Consequently, the theoretical size of China’s sports rehabilitation market could reach approximately RMB 50 billion.

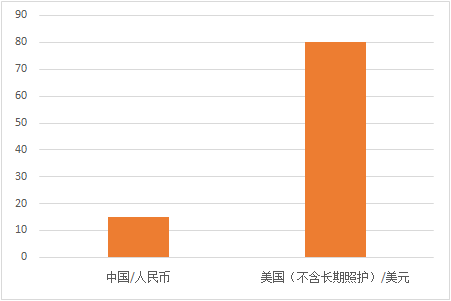

Comparison of Per Capita Costs in the Rehabilitation Markets of China and the United States

In the broader rehabilitation sector, China’s market size amounted to only RMB 20 billion (approximately RMB 15 per capita) as of 2016. In contrast, the U.S. rehabilitation healthcare market also stood at 20 billion, but in U.S. dollars (USD 80 per capita), representing a six-fold difference. When long-term care is included, per capita rehabilitation spending in the United States reaches USD 800, with the overall market totaling USD 200 billion. The imbalance between supply and demand has hindered the opening up of the domestic market.

Policy: A Stepping Stone or a Roadblock?

VCBeat has compiled policies related to sports rehabilitation in the fields of rehabilitative medicine and health management from recent years, aiming to gain insights into the real-world development trends of sports rehabilitation through top-level design.

Among the aforementioned policies, the State Council’s 2014 “Several Opinions on Accelerating the Development of the Sports Industry and Promoting Sports Consumption,” also known as Document No. 46, explicitly called for promoting the integration of healthcare and sports. It emphasized vigorously developing sports medicine and rehabilitation medicine, actively researching and developing sports rehabilitation technologies, and encouraging social capital to establish various institutions focused on healthcare-sports integration, physical fitness assessment, and sports rehabilitation. This policy clearly paved the way for opening up the capital market for sports rehabilitation, serving as a “bible” for enterprises in this sector. In the three years that followed, a large number of startups in the sports rehabilitation field emerged.

Furthermore, relevant directives or indicative trend forecasts have emerged in the speeches and work reports of government officials; although not yet formalized in writing, they have nonetheless brought hope to enterprises in this sector.

In May 2017, Zhao Yong, Deputy Director of the General Administration of Sport of China, emphasized that “the integration of sports and medicine is an urgent necessity for driving the health revolution and addressing public concerns.” The deep integration of sports and medicine has become a key measure to help the general population avoid illness or reduce its incidence. “Sports-medicine integration” has emerged as a critical pathway and developmental direction for sports rehabilitation and rehabilitative medicine.

In August 2017, the National Health and Family Planning Commission (NHFPC) held a regular press conference to report on the progress and effectiveness of its “delegation, regulation, and service” reforms. Jiao Yahui, Deputy Director of the Bureau of Medical Administration and Hospital Management under the NHFPC, announced that five new categories of independently established medical institutions would be added. Relevant standards are currently being drafted for these categories, which include independent rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers. The inclusion of independently established rehabilitation medical centers on the policy agenda may help remove certain obstacles in the approval process for medical qualifications of sports rehabilitation centers.

One of the obstacles is the "Regulations on the Administration of Medical Institutions" (Document No. 149), issued by the State Council in 1994, which stipulates that medical institutions without beds or with fewer than 100 beds must apply to the health administrative department of the local county-level people's government. Currently, nearly all small-scale rehabilitation institutions in China fail to meet the requirement of having at least 100 beds. Furthermore, the local county-level health administrative departments impose specific requirements on drainage systems, disinfection protocols, the number of rehabilitation therapists and assistant therapists, and years of clinical experience. Therefore, it is evidently challenging to obtain the "medical" qualification.

Offline sports rehabilitation startups in the market are basically divided into two camps: those with medical qualifications and those without. Currently, there are no more than six sports medicine centers nationwide that have obtained medical qualifications, such as Hongdao Sports Medicine Clinic in Beijing, Youkan in Hangzhou, Tichuang and Weibao in Nanjing, etc.

Application requirements for medical qualifications vary across different regions. Obtaining such qualifications not only enhances government-backed safeguards but also serves as a critical component of risk mitigation for rehabilitation institutions operating on a studio-based model.

From a long-term perspective, the involvement of future medical insurance and commercial insurance also requires the protection of this "certificate." In terms of payment issues, lacking medical qualifications means that medical insurance cannot be accessed. Taking Beijing Jianxingzhe as an example, the guidance fee of 400 yuan per session has deterred many people, leading them to choose home rehabilitation instead.

Overall, however, policies are supportive of this sector. Some argue that the explicit directive in State Council Document No. 46 to develop sports medicine and rehabilitation medicine may lead to a relaxation of medical qualification approval procedures for establishing sports rehabilitation centers within commercial institutions in the future.

Talent Development in Sports Rehabilitation

The lack of clear understanding about sports rehabilitation is the primary reason why such services fail to gain widespread public acceptance. In China, sports rehabilitation is often perceived as a treatment reserved exclusively for professional athletes. Sports injuries are still not regarded as legitimate medical conditions, and the profession of certified sports rehabilitation therapist remains relatively obscure. When faced with the choice between “I need to treat my illness” and “How can I restore my physical function,” the majority of people still opt for the former.

In the United States, the term "doctor" can refer to both a Ph.D. holder and a physician. This overlap exists because physicians in the U.S. are required to hold a doctoral degree, which stands in stark contrast to China, where medical practitioners may qualify with varying levels of education ranging from associate degrees to doctorates. In China, there are 128 undergraduate programs related to rehabilitation therapy and sports rehabilitation; by comparison, the United States has 219 such programs, Germany has 280, and Japan has 249. At the graduate level (master’s and doctoral), these educational resources are even more scarce.

Sports rehabilitation therapists occupy an intermediate position between physicians and nurses; compared with their counterparts abroad, there is a significant gap in both professional status and income.

Moreover, most sports rehabilitation therapists in China currently graduate from sports universities, as few medical universities offer majors in sports rehabilitation. This relative separation between the two fields reveals a tendency for sports rehabilitation to lean more toward “sports” than “medicine.” The resulting contradiction is that sports colleges lack qualifications for medical education, while medical schools rarely integrate practical sports scenarios into their teaching, creating an undeniably awkward situation.

Regarding professional qualifications, the examination system has become the “Achilles’ heel” for rehabilitation therapists. There are discrepancies in the implementation of policies across China regarding exam eligibility: some provinces only allow students majoring in Rehabilitation Therapy to take the examination, while graduates with degrees in Sports Rehabilitation are not permitted to do so.

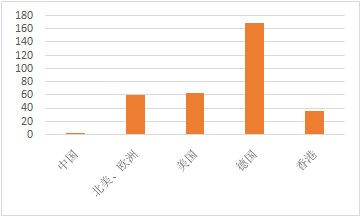

Number of Physical Therapists per 100,000 Population (Persons)

According to publicly available data, China currently has approximately 36,000 rehabilitation therapists with technical qualifications. Calculated according to international standards, there are 2.65 physical therapists per 100,000 population in China, whereas the average in North America and Europe is 60 per 100,000 population. The figure stands at 62.8 per 100,000 population in the United States, 68.7 per 100,000 population in Germany, and 36.4 per 100,000 population in Hong Kong.

The bar chart shows that China’s figure is nearly close to the X-axis, with a gap of more than 30-fold, indicating that the cultivation of rehabilitation professionals still faces a long and arduous journey.

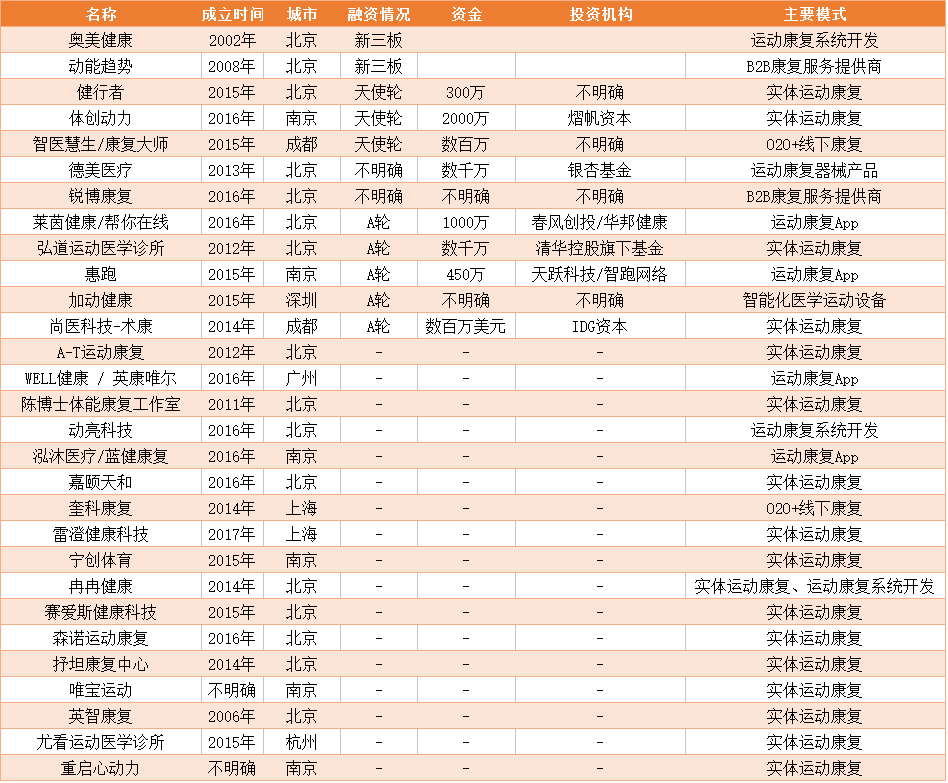

Overview of Sports Rehabilitation Companies

This inventory is incomplete, covering 29 startups in the sports rehabilitation sector (excluding traditional rehabilitation equipment manufacturers). We also welcome companies in the sports rehabilitation field that are not included in this list to contact VCBeat to jointly explore industry trends.

Among the 29 companies surveyed by VCBeat, 12 have received capital investment. The two largest are NEEQ-listed companies, Kinetic Trend and Aomei Health, which operate as a B2B rehabilitation service provider and a sports rehabilitation system provider, respectively. Both adopt business-to-business (B2B) models, delivering rehabilitation services or sports rehabilitation systems to corporate clients. Most of these investments are at the angel or Series A stage, with the prevailing model being offline sports rehabilitation facilities. The remaining 17 companies have not secured any funding.

Hongdao Medical Clinic, Tichuang Dongli, and Demei Medical, which ranked among the top in terms of financing amounts, each secured tens of millions of yuan. Although Shukang, which transitioned from an app to offline sports rehabilitation centers, did not disclose its specific financing amount, its founder Lei Zhen revealed in 2015 that the budget for building a rehabilitation hospital under the Shukang brand was RMB 300 million. Given its relatively ample capital reserves, we speculate that its recent funding round, likely in the range of several million U.S. dollars, represents a significant infusion of capital.

The disclosed investment amounts for the remaining companies ranged from several million to tens of millions, reflecting an overall pattern of small-scale and fragmented operations. Certain sports medicine clinics and rehabilitation studios, such as Jianxingzhe and Youkan, primarily operate on a single-store model without showing signs of expansion, indicating that capital remains in a wait-and-see stance toward sports rehabilitation. No industry “unicorn” has yet emerged.

Patterns can also be identified by examining the establishment dates of companies. China’s sports rehabilitation industry started relatively late, with specialized modern sports rehabilitation institutions beginning to emerge gradually only in 2011. Between 2014 and 2016, there was a concentrated influx of enterprises entering the sports rehabilitation sector, with 18 companies established during this three-year period. This trend indirectly reflects how the recent nationwide fitness boom has heightened public awareness of sports-related injuries.

When scanning the aforementioned companies, another interesting phenomenon emerges: among their founders, four graduated with degrees in Sports Rehabilitation from Beijing Sport University. Without exception, they chose to establish personal rehabilitation studios. At this top-tier sports university in China, Sports Rehabilitation is far from a niche major. Meanwhile, Beijing and Nanjing have become hubs where sports rehabilitation service providers are heavily concentrated.

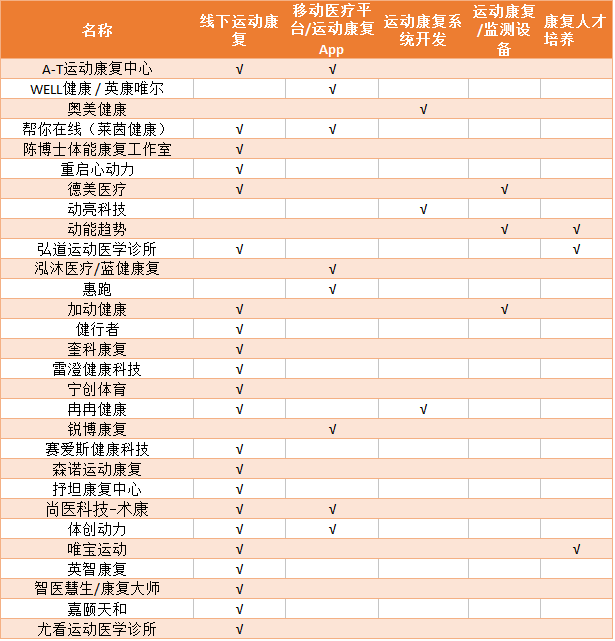

Fields Covered by Sports Rehabilitation Companies

Fields Covered by Sports Rehabilitation Companies (Company Names Listed in Pinyin Order)

Among the aforementioned companies, the largest number—22 in total—have established offline physical rehabilitation and exercise facilities. Eight companies have launched online apps or mobile health platforms. In the remaining three sectors, three companies are engaged in the development of sports rehabilitation systems, while three each focus on sports rehabilitation equipment/devices and the training of rehabilitation professionals (note: several companies operate across multiple business areas simultaneously).

Our observations reveal that among these 28 companies, most have not adopted a dual-channel strategy integrating both online and offline service models; instead, they tend to operate along a single channel. However, a notable trend is emerging: some companies that previously focused primarily on online services or on medical devices and products are now expanding into offline operations. Examples include Bangni Zaixian, Jiadong Health, and Demei Medical. This trend indicates that offline rehabilitation centers will remain the mainstream service providers in the future.

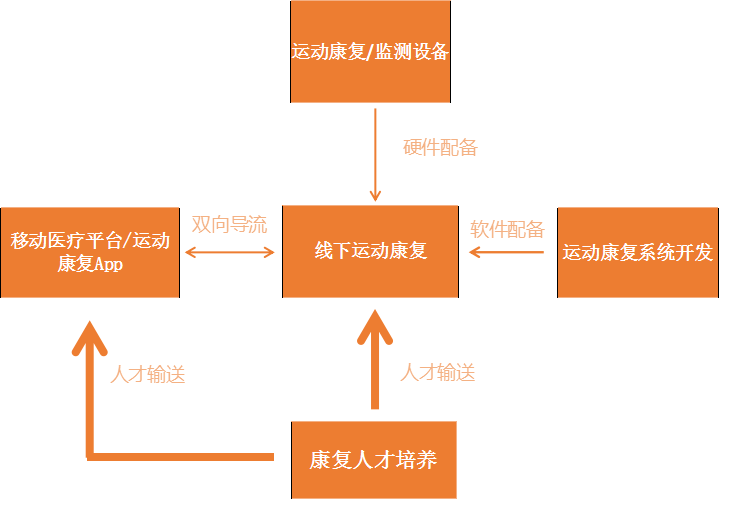

VCBeat has mapped out a demand flow chart to illustrate the connections across different sectors.

It is evident that, whether in talent development, equipment supply, or sports rehabilitation system development, the ultimate goal is to channel resources to offline sports rehabilitation services. Online platforms and apps maintain a bidirectional referral relationship with offline sports rehabilitation providers. Users may first experience online services before transitioning to physical facilities, or they may shift from in-person care to online consultations and customized plans—primarily opting for self-guided rehabilitation—due to cost considerations and other factors.

In fact, there is an additional link following offline sports rehabilitation: various rehabilitation hospitals and the rehabilitation departments of Grade 3A hospitals. Certain physical rehabilitation institutions with medical qualifications will establish referral mechanisms to provide referral services to well-known Grade 3A hospitals. These institutions differ in nature and operational mechanisms from the sports rehabilitation companies discussed in this article; therefore, they will not be elaborated upon here. VCBeat will continue to closely monitor rehabilitation hospitals as a category.

According to the data provided in the National Fitness Plan (2016–2020) issued by the State Council, China’s physically active population is projected to reach 435 million by 2020, with sports consumption reaching RMB 150 million. Meanwhile, the Report on the Output Scale of the Fitness Industry (2009–2014) indicates that the incidence rate of sports-related injuries among regular exercisers exceeds 85%. This implies that, theoretically, the number of individuals suffering from sports-related injuries could reach 370 million by 2020.

From the current state of the industry, sports rehabilitation in China is still in its early stages, with significant market gaps yet to be explored. In this blue ocean of rehabilitation, there is a need for pioneers to emerge. However, unavoidable challenges include a shortage of talent, imperfect medical insurance policies, and high rehabilitation costs, all of which are problems that need to be tackled one by one.

However, as the market remains sluggish, signs of hope are becoming increasingly evident. The “integration of sports and medicine” combined with an “online-offline internet model,” highlighted at the MTT International Symposium on Sports Medicine and Rehabilitation in December 2016, has emerged as one of the predominant business models in the sports rehabilitation sector. With business models growing clearer and concepts gaining wider acceptance, gaps compared to foreign counterparts have been identified. Although China lags behind developed countries by 10–20 years in the field of rehabilitation, this challenging landscape also represents a blue-ocean opportunity. As the base of physically active individuals expands, the prospects are theoretically promising.

Whether sports rehabilitation will develop into a lucrative opportunity or evolve into a barren landscape, VCBeat will continue to monitor this sector and share more insights with its readers.