Maternity and Childcare Industry: A Trillion-Dollar Market with Persistent User Acquisition Challenges; Pediatric Clinics and Confinement Centers Set to See Emergence of Leading Brands [2017 Year-End Review]

Excluding public hospitals, the market size of the maternal and infant industry (including pregnancy, infants, and young children) ranges between RMB 2 trillion and RMB 4 trillion. According to projections by the National Health and Family Planning Commission, approximately 3 to 4 million newborns will be added annually in the future, signaling the advent of China’s fourth baby boom and presenting significant opportunities for the maternal and infant sector.

Centered on the needs of mothers and infants, fragmentation has been continuously occurring and boundaries are increasingly converging across various sectors, including women’s and children’s hospitals, brick-and-mortar mother-and-baby stores, e-commerce platforms for maternal and infant products, parenting communities, vertical parenting platforms, as well as assisted reproductive technology (ART) preconception centers, postpartum recovery facilities, and confinement care centers. So, what changes have taken place in the maternal and infant industry in 2017? The following section outlines the key trends observed this year.

The target population for this “maternal and infant industry” review encompasses individuals from pregnancy through age 6, with a particular focus on children under 3 years of age.

First, let’s discuss women’s and children’s hospitals. With consumption upgrading and the relaxation of the two-child policy, people are willing to spend more to ensure the safety of both mothers and infants, and maternal and child healthcare expenditures account for an increasing proportion of household spending. It has become common for hospital outpatient departments to be overcrowded and for bed turnover rates to remain high, while the shortage of pediatric medical resources is becoming increasingly prominent.

According to the China Health and Family Planning Statistical Yearbook, in 2016, there were 690 private specialized obstetrics and gynecology hospitals, the highest number among all types of specialized hospitals, far exceeding others; the number of children’s hospitals also reached 49.

In 2015, the number of private hospitals surpassed that of public hospitals. This indicates that social capital has actively participated in the development of private hospitals as policy barriers have been gradually lowered.

As early as 2013, Warburg Pincus and its partner institutions announced the completion of a $100 million investment in Amcare. In May 2016, Warburg Pincus announced the completion of its investment in U-AiBaby, a chain brand specializing in maternal and infant health services (primarily operating postpartum care centers).

On May 27, 2017, Wintime Energy issued an announcement stating that Chengdu Xinan Gynecological Hospital Co., Ltd., in which its assisted reproductive medical investment fund holds a stake, plans to introduce Warburg Pincus as a strategic investor through a capital increase.

Not only did capital participate, but 2017 was also a year when real estate companies concentrated their transformation and aggressively entered the healthcare sector, with elderly care and maternal and child health being indispensable components.

Following Warburg Pincus’s investment trajectory, the “continuous care” model has demonstrated particular prominence in the maternal and child health sector. Typically, obstetrics-focused hospitals center their operations on obstetric services, which account for 70% of their offerings, while extended women’s and children’s health services make up the remaining 30%. Their development path typically progresses from obstetrics to pediatrics and gynecology, and even expands into synergistic areas such as assisted reproductive technology (ART) and postpartum care centers.

Much like the pediatric clinics that have gained significant popularity this year, those with strong pediatric services naturally expand their offerings to include child health management, general pediatrics, gynecology, and even pediatric massage. Standalone brands specializing in child health management and pediatric massage have also emerged in the market.

In the fields of child developmental behavior and pediatric rehabilitation, Changhe Dayun holds the exclusive agency rights for the Chinese version of the Griffiths Developmental Scales in mainland China. The company currently operates the Beijing Changhe Dayun Pediatric Clinic and the Shenzhen Changhe Dayun Pediatric Rehabilitation Outpatient Department. Additionally, it has acquired the Shanghai Dayun Home Educational Institution and has obtained the license for the Shanghai Changhe Dayun Pediatric Outpatient Department, which commenced clinical operations in November 2017.

Pediatric massage brand Wanpixiong, established in 2016, opened five centers in Beijing within less than two years, with a sixth center currently under preparation. It was also the first in the industry to obtain ISO9000 international quality management system certification.

How profitable are maternal and child health hospitals? A look at Hemei Medical Group, which operates 12 specialized women’s and children’s hospitals. The group primarily provides gynecological, obstetric, and pediatric services, with revenue derived from inpatient and outpatient medical services (including fees for medical services, pharmaceuticals, and medical facilities).

In the first half of 2017, the hospital services segment of Hemei Medical Group generated a profit of RMB 406 million, accounting for 96.3% of the group’s total revenue. The 12 hospitals under the group recorded over 288,205 outpatient visits and 11,000 inpatient admissions. Among them, Beijing Hemei Women’s and Children’s Hospital, the largest facility, reported revenue of RMB 92.62 million in the first half of 2017, with 37,630 outpatient visits and 1,264 inpatient admissions, resulting in an average expenditure of RMB 2,381 per visit.

Why Mention Maternal and Child Health Hospitals? Because they remain the largest and most precise channels for patient acquisition. For instance, maternal and infant science popularization platforms or certain maternal and child health platforms (including online consultations) that rose to prominence during the internet boom still derive their primary customer base from hospitals. Physicians in public hospitals bear heavy workloads, and there is a shortage of personnel and resources for health education. Consequently, hospitals lack the capacity to provide services in out-of-hospital settings, creating opportunities for the emergence of such platforms.

Other service-oriented institutions, such as postpartum care centers and postpartum recovery facilities, also need to channel patient flow from hospitals. Pediatric clinics, serving as a strong complement to hospitals, have been able to advance by leaps and bounds by capitalizing on this opportunity.

Having discussed offline hospitals and their continuous service logic, what is the development path for online maternal and infant platforms? This section will focus on this topic.

The era of leveraging the simple “portal + community + e-commerce” model to build a massive traffic dividend in the maternal and child sector during the early days of the internet has passed.

Currently, the business models of maternal and infant platforms can ultimately be categorized into four types: tools, health education and popularization, community services, and e-commerce (including the currently trending mother-and-baby stores and new retail). These correspond to the four primary needs of mothers (or expectant mothers): tracking, knowledge acquisition, social interaction, and shopping consumption.

“Records” primarily include menstrual cycles, baby photos, and growth calendars, meeting users’ documentation needs. Popular apps in this category include Meiyou, Dayima, BabyTree, and Qinbaobao. For new mothers, each day of their child’s growth is uncharted territory, necessitating access to professional knowledge and even online medical consultations. Therefore, acquiring “Knowledge” is an essential need.

Popular science education platforms (covering topics such as parenting and medical consultations), including Mommy Knows, Sunshine Women and Children, Jia Health, Yue Health, Pocket Parenting, Ai Ying Hui, and Medical Kangaroo, serve a dual purpose. On one hand, they provide users with professional, high-quality health education content to maintain user retention and high engagement. On the other hand, leveraging big data mining models, they build intelligent platforms for curated healthy living solutions, facilitating convenient access to and experience of health services for users. Some of these platforms have also extended their operations offline, aiming to create a comprehensive service closed loop.

Sina’s 2017 Maternal and Infant Self-Media Awards: Content Contribution Rankings. This year, 40 prominent maternal and infant influencers were shortlisted, with no shortage of accounts boasting over one million followers. This trend reflects the substantial demand for parenting knowledge and marks a shift in content format from plain text and images to professionally generated content (PGC) and variety-style short videos.

VCBeat has learned that Meiyou has entered the content sector, leveraging its vast repository of female user data accumulated over more than four years to develop a personalized recommendation system. This system is an optimization of its existing e-commerce and health-care personalized recommendation engines. Currently, content reading has become the most frequently used feature module among Meiyou users.

In 2017, Gong Xiaoming, a renowned obstetrician and gynecologist, founded Fengxinzi and launched “Fengxinzi Health Courses,” a new online channel for knowledge sharing. To date, nearly 100 episodes have been released, with peak concurrent online attendance exceeding 10,000 participants. In addition, Fengxinzi has introduced the “Ask a Doctor at Fengxinzi” program, enabling patients to consult directly with obstetricians and gynecologists across China via its WeChat official account.

In 2017, Lamanbang was committed to building a one-stop maternal and child ecosystem integrating “large-scale communities, robust tools, extensive channels, and major e-commerce.” In February, it completed its Series D financing, exclusively backed by strategic investment from Suning Redbaby. Also in 2017, Lamanbang successfully invested in Changsha Miaoqu New Media Co., Ltd. and Beijing Jiuxiaoshi Cultural Media Co., Ltd., strengthening its focus on content development.

Mothers’ “social” needs are also quite interesting. From the moment pregnancy is confirmed, users enter a brand-new social network, a process that typically lasts until the child is around three years old. Topics such as pregnancy, breastfeeding, and mother-in-law/daughter-in-law relationships are particularly likely to resonate with them.

“Shopping and Consumption”: In addition to physical maternal and infant stores, e-commerce has been booming in recent years. Overall, physical maternal and infant stores remain the primary and preferred channel for consumers, a trend that is even more pronounced among regional maternal and infant stores in second- and third-tier cities.

After several years of development, the maternal and infant e-commerce sector has entered a mature stage. E-commerce platforms such as Tmall Maternal & Infant, JD.com Maternal & Infant, Suning.com, Vipshop, Beibei.com, Mailegou, and Mia.com now command the vast majority of the market share for maternal and infant products.

A visible trend is that some e-commerce platforms, after educating users, lock in their customer base through branded flash-sale models, thereby positioning themselves to target mid-to-high-end consumers. For instance, Mia launched its “Mama’s Choice” initiative in the second half of 2017. Beibei.com focused on distinctive non-standardized products and operated without holding inventory, acquiring a significant user base by leveraging superior customer experience.

In 2017, the emerging content-driven e-commerce platform “Nian Gao Mama” strengthened its supply chain management, enhanced direct collaborations with brand owners, prioritized product quality and end-to-end supply chain integrity, and also launched integrated marketing initiatives leveraging major intellectual properties (IPs) and brands.

The fragmentation of maternal and infant retail has already emerged, particularly under the influence of New Retail. At their core, New Retail and new services represent an online-offline integration driven by technology and data.

Kidswant, a leading brand in maternal and infant retail, reported revenue of RMB 260 million and net profit of RMB 61.45 million in the first half of 2017. As of the first half of 2017, the company had opened 185 stores across 94 cities in 18 provinces nationwide. The cumulative number of mature stores (operating for more than 18 months) reached 111, accounting for 60% of the total store count. This represents a significant increase from the 44% recorded at the end of 2016, enabling the company to achieve profitability for the first time in 2017.

VCBeat has learned that most of Kidswant’s stores are located in popular urban commercial complexes, with an average single-store area of 3,500 square meters.

The stores offer a diverse range of products and services, including retail merchandise, children’s entertainment, early childhood education and training, postpartum recovery, and children’s photography, thereby meeting consumers’ multifaceted needs for shopping, services, and social interaction. Additionally, specialized teams are established to provide customized value-added services such as parenting consultations, nutritional planning, infant massage, baby haircuts, lactation support for new mothers, and confinement meal planning, further strengthening the relationship between customers and Kidswant.

In terms of operations, Kidswant has launched precision marketing strategies based on big data analysis of its membership base to improve the gross profit margin of product sales. Meanwhile, it has implemented an omnichannel strategy integrating online and offline channels, introducing all-scenario scan-to-purchase services and digital in-store online initiatives.

The aforementioned items represent essential needs, and as children grow, mothers’ requirements vary across different developmental stages. Looking ahead, parenting, social interaction, and e-commerce shopping will continue to remain key areas of focus. In particular, social interaction and shopping are inherently enjoyable activities, aligning well with the characteristics of female consumer behavior.

The post-80s and post-90s generations, who grew up during the internet boom, have become the main force driving this baby boom. Consider the characteristics of this demographic: they prefer to learn parenting knowledge and socialize online, and place greater emphasis on the quality and experience of products and services.

Excluding education (which is not covered in this review), investment and financing in the maternal and infant sector are primarily concentrated in healthcare (including childcare, social networking, assisted reproduction, etc.) and commercial monetization (such as e-commerce, advertising, and offline clinics). After accumulating data through sustained operations, major platforms have begun to introduce capital or accelerate their layout in commercial monetization through cross-industry integration.

But for both investors and entrepreneurs, the maternal and infant industry is a slow-burning sector.

Companies that have announced the completion of significant financing rounds this year include:

In February, Anxin Doctor, a mobile health platform specializing in women’s and children’s health, announced the completion of its Series B and B+ financing rounds, raising approximately RMB 200 million. Following this investment, Anxin Doctor will accelerate partnerships and expansion in offline medical services, while also speeding up the optimization and iteration of “Yida,” its professionally generated content (PGC) product focused on women’s and children’s health.

In February, the maternal and infant content e-commerce platform “Xiao Xiao Bao Ma Ma” announced that it had secured RMB 35 million in Series A+ financing at the end of 2016. The round was led by Toutou Shidao Fund, with participation from existing investors Longteng Capital and Lafang Yijian Fund, marking its entry as a new player in the maternal and infant e-commerce sector.

In February, Mami Zhidao secured tens of millions in strategic investment from Chow Tai Fook in its Series B+ round, accelerating the offline expansion of its medical information pediatric services.

In May, the assisted reproductive technology platform Haoyunbang secured tens of millions of RMB in Series B financing. The funds will be primarily allocated to the deployment of physical medical services, including preconception care clinics and brick-and-mortar hospitals, while also strengthening the disease management team to productize condition-specific disease management services.

In July, the mobile maternal and infant community MamaBang announced the completion of a B-round financing round worth hundreds of millions of yuan. It will integrate the multi-channel resources of its investor, TAL Education Group, to focus on technological innovation and the upgrading of intelligent maternal and infant services.

In July, Zhibei Pediatrics secured tens of millions of yuan in Series A financing from Sequoia Capital. Following the investment, Zhibei Pediatrics will accelerate the expansion of its outpatient clinics and deliver closed-loop, evidence-based medical services by integrating offline physical clinics with online internet platforms.

Regardless of its format, the greatest challenge in the maternal and infant industry is customer acquisition. Moreover, this type of acquisition differs from that in other industries, as women who are not pregnant pay virtually no attention to the maternal and infant sector. Therefore, an established maternal and infant platform holds no significant advantage over a new maternal and infant website in terms of user acquisition.

As Mai Tian, founder of Pocket Parenting, put it: “Running a maternal and infant website is like harvesting leeks; it’s an endless cycle where you reap a new crop every year. For maternal and infant platforms, building a moat is a long-term challenge that requires careful consideration. Market trends show that when established parenting apps experience a slump in promotional momentum in any given year, competitors quickly overtake them. This pattern holds across the entire industry, indicating that barriers to entry are remarkably low.”

Another challenge lies in the highly fragmented nature of maternal and infant needs, characterized by a large volume of non-standardized demands. Users exhibit significant segmentation; they are almost exclusively concerned with information, products, or services tailored to their child’s current age group (“same-age-plus”), showing little interest in those intended for earlier developmental stages.

Fragmentation and segmentation have made it extremely difficult for maternal and infant websites to achieve large-scale growth, as the industry suffers from low levels of organic traffic. This necessitates a multi-pronged approach by enterprises, focusing on development strategies, promotional channels, and integration across the upstream and downstream value chain. Driven by strategic considerations, some platforms are making new moves; common practices include expanding into offline services, such as Mama.com’s entry into postpartum care centers, Mommy Knows’ establishment of clinics, and BabyTree’s foray into early childhood education.

The core competitiveness of maternal and infant platforms lies in building sustainable customer acquisition capabilities, transforming into a lifestyle service gateway that connects with diverse consumption scenarios. Leveraging precise big data, these platforms drive the application and monetization of targeted advertising, intelligent parenting assistants, e-commerce, and offline services.

The model of integrating branding and performance, prioritizing user needs by curating highly-rated merchants and charging them only upon successful transactions, has already emerged.

Another trend is that advertising slots on large maternal and infant communities and platforms are becoming increasingly expensive. Since these platforms offer nationwide traffic, offline businesses with a limited geographic service radius—such as postpartum care centers and postnatal exercise rehabilitation providers—experience lower conversion rates. In contrast, regionally focused platforms such as Yuejiankang and Weimai’s Ximai can gain advantages in user acquisition, retention, engagement, and conversion through refined operational strategies.

The profitability models of maternal and infant platforms are currently highly homogeneous, with most relying on a survival strategy based on large user bases and advertising from maternal and infant brands. To become a leader, key barriers to entry include the ability to identify mothers with purchasing power and high-quality merchants, as well as capabilities in data platform infrastructure, content production, merchant curation, and even the planning team’s expertise in designing health services.

Maternal and infant platforms either build bridges connecting doctors with patients, provide health management for maternal and infant groups via mobile devices, or help consumers precisely filter the services they need.

Hu Min, founder of Yue Health, stated in an interview with VCBeat: “In selecting categories of institutions for platform partnerships, we primarily focus on major categories, such as postpartum care centers, confinement nannies, prenatal exercise (yoga and Pilates), postpartum recovery and exercise, early childhood education, and photography. There is also significant untapped potential for collaboration in areas such as postpartum medical aesthetics, high-end medical services, and parent-child entertainment.”

Establishing an offline presence is also a visible trend this year. Owning physical brick-and-mortar stores enables companies to integrate all aspects of healthcare delivery, offering more comprehensive and targeted services, while also helping them build their own brand reputation and credibility.

In terms of expansion and growth momentum, pediatric clinics, postpartum care centers, and early childhood education institutions (typified by BabyTree, etc.) are among the most popular types of offline physical entities this year.

According to data released in the 2015 China Health Statistics Yearbook, the total number of pediatricians in China decreased from 105,000 to 100,000 over the past five years. Currently, there are only 0.43 pediatricians per 1,000 children, a figure significantly lower than the national average of 2.06 physicians per 1,000 people. As public hospitals cannot meet all demands, pediatric clinics have gradually emerged as a supplement to public hospitals, driven by capital investment and policy support.

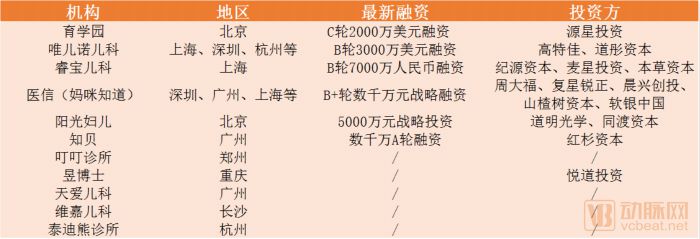

Currently, pediatric clinics in Beijing, Shanghai, Guangzhou, and Shenzhen are undoubtedly the focus of capital attention. Pediatric healthcare institutions that have secured financing, such as Weier Nuo, Ruibao Pediatrics, Yixin, Sunshine Women and Children, and Zhibei, are all located in these regions.

Pediatric Clinic Brand

“Mami Knows” bridges the online and offline service loop. Users can directly connect with renowned specialists from top-tier (Grade 3A) hospitals via the “Mami Knows App” to enjoy online health consultations and preventive care services. For more comprehensive care, users may visit the offline “Mami Knows Pediatric Clinic” for in-person diagnosis and treatment by physicians.

In February 2017, the first self-operated flagship store of “Mommy Knows Pediatric Clinic” officially opened in Tianli Central Plaza, Nanshan District, Shenzhen. On December 12, Mommy Knows announced the completion of its acquisition of Guangzhou You’er Clinic, making it the first pediatric clinic under the Mommy Knows brand to enter the Guangzhou market. The company adopted a physician partnership model, and this innovative management approach attracted pediatricians to join on a full-time basis.

Driven by policy support and the allure of industry prospects, more physicians will leave the public healthcare system to launch their own ventures in this market.

Yihe Health, founded by Dr. Pei Honggang, a pediatrician at Shenzhen Children’s Hospital, has assembled a team of nearly 200 physicians, completed over 160,000 consultations, and delivered online lectures to more than 80,000 listeners. Within one year of its establishment, the company achieved a monthly positive cash flow exceeding RMB 1 million, with future plans to expand into offline clinics.

In addition, major central cities with large populations, rapid economic growth, relaxed household registration (hukou) systems, and strong middle-class purchasing power—such as the Sichuan-Chongqing region, Wuhan, and Zhengzhou—are also likely to see the emergence of large-scale pediatric healthcare chains, such as Yu Boshi and Dingding Clinic.

The rapid development of pediatrics is primarily driven by policy. The “Opinions on Supporting Social Forces to Provide Multi-Level and Diversified Medical Services,” issued in May 2017, explicitly stated the goal to “establish a large number of privately operated medical institutions with strong service competitiveness, form several influential clusters of specialized health service industries, ensure that service supply basically meets domestic demand, and gradually establish a new pattern of multi-level and diversified medical services.”

In August, the National Health and Family Planning Commission issued the “Notice on Deepening the ‘Delegation, Regulation, and Service’ Reform to Stimulate Investment Vitality in the Medical Field,” which stated that the approval process for medical institutions should be further simplified by merging the setup approval and practice registration into a single license for secondary-level and lower-tier medical institutions. Meanwhile, the scope of social investment will be expanded to promote the development of new business models in the health service industry. These are all favorable factors for establishing pediatric clinics.

The successive issuance of national-level policy documents reflects that maternal and infant health has been elevated to a position of high priority. Particularly as a robust complement to public hospitals, and bolstered by strong capital investment, branded pediatric clinics are poised to accelerate their chain expansion efforts.

Assisted reproduction has also been a hot topic this year. In June, VCBeat conducted a comprehensive and detailed industry scan. As of December 31, 2016, there were 451 medical institutions approved to provide human assisted reproductive technologies, and 23 medical institutions approved to establish human sperm banks. The theoretical market size for assisted reproduction reaches RMB 100 billion.

In 2016, approved assisted reproductive technology (ART) institutions in China performed an average of 700,000 ART procedures annually. Given the population of 40 million individuals affected by infertility, this represents a substantial treatment gap.

The assisted reproductive technology (ART) center with the highest number of oocyte retrieval cycles for in vitro fertilization (IVF) nationwide is CITIC-Xiangya Reproductive & Genetic Hospital. In 2016, its cycle volume exceeded 20,000. Approximately five ART centers across China reported over 10,000 IVF oocyte retrieval cycles each, collectively accounting for about 20% of the national total. IVF clinics performing fewer than 800 cycles annually face significant operational challenges.

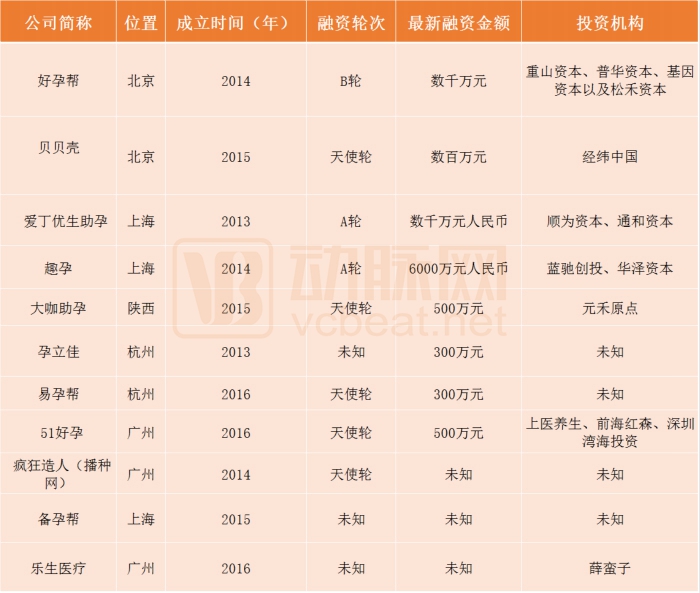

Vertical infertility and sterility service providers, such as Haoyunbang, Beibeike, Aiding Eugenics and Fertility Assistance, Quyun, Bei Yun Bang, and 51 Haoyun, mostly adopt an “Internet + preconception clinic” model to engage in standardized disease course management or enhance service experience, with a focus on success rates and the medical care experience.

Offline traffic gateways, such as health checkup providers like Meinian (including Ciming) and iKang, have already entered or are preparing to enter the assisted reproductive technology (ART) sector. In the overseas ART market, companies such as Youyunxing and Yuehe Jiayi have also joined forces with renowned hospitals and institutions in the United States, Israel, Russia, Thailand, and other countries to capture a share of the market.

Internet + Assisted Reproductive Technology Enterprises

On December 5, 2017, China’s first insurance product specifically designed for in vitro fertilization (IVF) patients—“Zhuyun IVF Insurance”—was officially launched. Couples undergoing IVF at designated medical institutions covered by Zhuyun IVF Insurance are eligible to enroll as long as the female partner is under 35 years of age. Coverage begins upon initiation of the IVF process. If three IVF cycles fail within one year after enrollment, the policyholders can receive insurance compensation of up to RMB 200,000.

This insurance product was developed based on big data accumulated from over 50,000 IVF patients at Chengdu Jinjiang District Maternal and Child Health Hospital during its 17 years of providing in vitro fertilization (IVF) services. After one year of development, the product was successfully completed and filed with the China Insurance Regulatory Commission (CIRC), making the hospital the first medical institution in China to receive insurance approval for integrating IVF technology with insurance coverage.

In October this year, VCBeat conducted a review of the postpartum care center industry. According to the "2016-2022 China Postpartum Care Center Industry Research and Investment Prospect Analysis Report" released by the Industry Information Network, the market size of postpartum care centers in China was approximately RMB 1.02 billion in 2010 and around RMB 4.2 billion in 2014, with a compound annual growth rate (CAGR) of 42.45%. A report from GF Securities projected that the market size would reach approximately RMB 15 billion by 2019.

According to data from the Standardization Administration of China, there are a total of 4,000 postpartum care centers nationwide. The industry emerged over a decade ago and entered a period of rapid growth in 2011. It remains in its early stages, with facilities primarily concentrated in large and medium-sized cities.

Postpartum care centers are growing at an annual rate of over 40%, with their presence now extending even to prefecture-level and county-level cities. However, the current customer base remains primarily concentrated among mid-to-high-end consumers with stronger purchasing power. Brands such as Xin Yue Hui, Ai Di Gong, Xi Yue Ge, Shi Xin, and Yue Lai Yue Mei have emerged as well-established players and have embarked on expansion paths.

A few years ago, staying at a postpartum care center was considered a luxury experience; today, Chinese mothers no longer view it as an unaffordable expense. Overall, the postpartum care center industry is shifting from high-end luxury toward the mid- and low-end markets.

Furthermore, the asset securitization level of the postpartum care center industry remains low, with only four companies listed on the National Equities Exchange and Quotations (NEEQ) in China: XiXi Maternal & Infant Care, XiZhiJia, FuZuo Maternal & Infant Care, and DaMei Maternal & Infant Care. There is significant room for improvement in terms of profitability.

For the majority of postpartum care centers, which are typically small-scale and fragmented, industry consolidation and expansion into lower-tier cities will become the dominant trends. Leading brands will enjoy significant premium advantages. Regardless of whether the Taiwanese or Korean model is adopted, it is essential to efficiently integrate management, maternal and infant care, and postpartum meal services to establish cost advantages and build a strong reputation.

To achieve profitability, postpartum care centers must address high costs associated with rent, labor, and marketing, as well as control renovation expenses. As an industry with substantial growth potential that meets the essential needs of postpartum women, postpartum care centers are generally viewed favorably by investors.

From the perspective of market capacity, the relaxation of the two-child policy, the increase in per capita disposable income of urban residents, the upgrading of consumption concepts for postpartum care, and the improvement of industry standards and regulatory policies have created a theoretically vast market space for confinement centers, given the current low penetration rate, with the competitive landscape yet to be determined.

On December 5, China’s first fund focused on maternal and child health—the Fuyou Fund—was established in Shanghai. With a total size of RMB 1 billion, the fund will primarily invest in growth-stage companies within China’s maternal and child healthcare sector. Professor Duan Tao, former director of Shanghai First Maternity and Infant Hospital and founder of Shanghai Chuntian Hospital Management Co., Ltd., has joined the fund as a partner.

Duan Tao stated, “In the maternal and child healthcare market—whether hospitals, clinics, postpartum care centers, or other service types—there are some strong regional brands, but a unified national market and brand landscape have not yet fully taken shape. This is particularly evident in the postpartum care center sector.”

Postpartum care centers are most densely distributed in Beijing, Shanghai, Guangzhou, and Shenzhen; however, each of these cities has no more than 10 brands that have achieved significant brand recognition. In other second- and third-tier cities, the number of branded postpartum care centers ranges from a high of five to a low of two or three, resulting in low market concentration and difficulties in cross-regional customer acquisition.

Postpartum care centers that possess advanced maternal and infant care concepts, superior property assets, founders with industry insights and a vision for future expansion, comprehensive service systems, and significant local influence or market share are well-positioned to become leading institutions through branding and capitalization strategies.