Six-Dimensional Analysis and Four Case Studies: A Comprehensive Deconstruction of Collaborations Between Foreign Medical Institutions and Chinese Real Estate Developers

By Luo Mei and Li Yanyu

From any perspective, the collaboration between Chinese real estate developers and overseas medical institutions is a particularly cost-effective deal.

For real estate developers, rashly investing in or transitioning to the healthcare industry carries significant risks. Although the sector boasts advantages such as high gross profit margins and supportive national policies, its high level of specialization and monopolistic characteristics deter most entrepreneurs.

For overseas medical institutions, the path to entering China’s healthcare industry has been exceedingly arduous. According to a report by the research team of the Chinese Hospital Association’s project on “The Status of Medical Institutions Established by Foreign Capital in China,” as of the end of 2014, there were only 92 foreign-funded hospitals, and the total number of broad-sense healthcare institutions established by foreign capital merely exceeded 200.

It is evident that the number of foreign-funded medical institutions in China is not only orders of magnitude lower than that of public and private medical institutions, but also falls far short of the booming landscape of Foreign Direct Investment (FDI) in the country.

According to data from the Ministry of Commerce, by the end of 2014, within the industrial structure of foreign direct investment (FDI), enterprises in the health, social security, and social welfare sector accounted for only 0.17% of the total number, while the actual amount utilized in this sector was merely USD 7.688 billion, representing 0.23% of the total FDI amount.

Thus, the collaboration between the two parties can be regarded as a typical case of “providing timely assistance in times of need.”

What are the advantages of foreign capital? What challenges do they face when entering the Chinese market? What forms of collaboration exist with domestic real estate developers? Which foreign investors are keen to enter China? In which medical sectors are these foreign healthcare institutions most active?

Driven by these questions, VCBeat (WeChat ID: vcbeat) has compiled a list of 23 overseas healthcare institutions, providing an in-depth analysis of their collaboration models with Chinese real estate developers, market entry timelines, and other key dimensions.

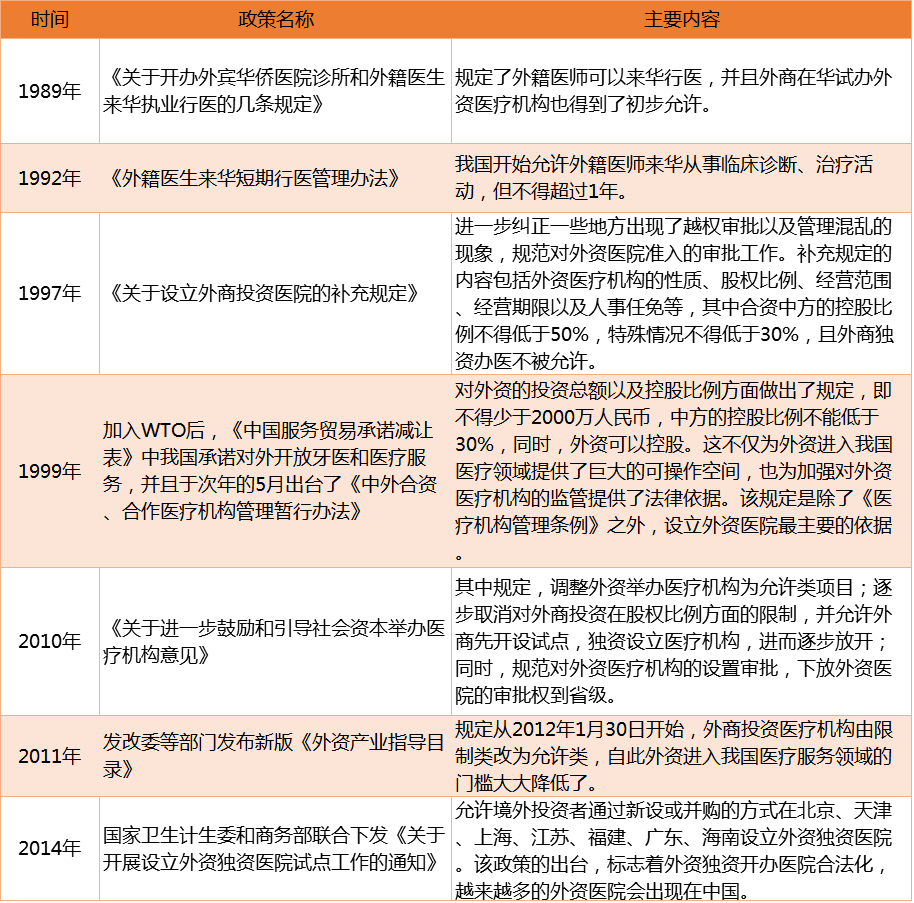

China’s earliest legal document concerning market access in the healthcare industry was issued in 1989, stipulating that foreign physicians could practice medicine in China and preliminarily permitting foreign investors to pilot foreign-funded medical institutions in the country.

Following China’s accession to the WTO, the entry of international medical services into China became part of global integration, creating favorable conditions for foreign investment in the Chinese market. At that time, the Chinese government committed to opening up two sectors: dental services and medical services. While no restrictions were imposed on cross-border supply, consumption abroad, or national treatment for these two sectors, limitations were placed on commercial presence and the movement of natural persons.

At that time, China permitted overseas medical institutions to establish Sino-foreign joint venture hospitals and clinics with foreign majority ownership, although the country would impose quantitative restrictions based on actual needs. It also allowed foreign physicians holding professional certifications issued by their home countries to provide short-term medical services in China upon obtaining approval from Chinese health authorities.

Detailed Policy List

Although China’s policies have provided numerous conveniences for foreign-funded medical institutions, they still face a multitude of challenges. These include restrictions on the procurement of medical equipment, incomplete coverage by basic medical insurance and low penetration of commercial health insurance, competition from public hospitals entering the high-end healthcare sector, challenges in localizing human resource management, difficulties in domestic financing, as well as inadequate tax policies and supporting measures.

The turning point for foreign-funded medical institutions emerged in 2013, when China began to regulate the real estate sector. On February 20, 2013, the State Council’s executive meeting introduced the “New Five National Measures” for property market regulation. These measures reaffirmed the steadfast implementation of regulatory policies centered on purchase restrictions and mortgage limits, vowed to crack down firmly on speculative and investment-driven property purchases, and required local governments to publish annual targets for controlling housing prices.

The General Office of the State Council issued the "Notice on Continuing to Carry Out Real Estate Market Regulation and Control," introducing stricter and more detailed measures such as "increasing the down payment ratio and loan interest rates for second-home mortgages in cities where housing prices are rising too rapidly" and "conducting regulatory interviews and holding accountable local governments that have failed to effectively implement housing purchase restriction policies."

“The Five New National Measures” stipulate that individual income tax on second-hand housing transactions shall be levied at 20% of personal gains. This provision will curb investment demand and affect transaction volumes, representing a positive outcome of real estate market regulation. However, it will inevitably suppress residents’ demand for upgrade-oriented home purchases.

In response, real estate developers have begun to seek transformation. According to incomplete statistics, two-thirds of the top 100 real estate companies have already entered the cultural and tourism real estate sectors.

Vanke’s foray into commercial real estate, Wanda’s pivot to cultural industries, Poly’s expansion into the elderly care sector, and Evergrande’s venture into bottled water—every major move and significant investment by these benchmark property developers in 2013 drew intense attention from both within and outside the industry.

Industry insiders unanimously agree that after a golden decade of rapid growth, the real estate sector is now poised to confront new challenges in its development. In response, leading property developers have concurrently begun expanding into non-real estate businesses, clearly signaling their proactive efforts to chart new strategic directions for corporate growth.

After exploring numerous transformation strategies, real estate developers found that industries such as tourism and beverages did not perform as expected. At that time, mobile health projects were booming, while continuous innovations in healthcare reform policies further propelled the development of the medical industry.

For years, the healthcare industry has been perceived as a high-margin sector with inherent patient traffic, where patients eagerly compete for appointments and readily pay for services. Consequently, real estate developers have come to view healthcare as a potential successor to the real estate industry—a new frontier poised for rapid growth.

On the surface, the healthcare industry appears to be a sunrise sector; in reality, however, it is akin to Mount Everest—an insurmountable challenge for real estate developers. Given the stringent requirements of high monopoly, advanced technology, and top-tier talent, collaboration with an institution that possesses both deep healthcare industry expertise and technical proficiency is essential.

However, most high-quality medical resources in China are concentrated within the public system, with few medical institutions partnering with real estate developers. This presents a favorable opportunity for overseas medical institutions to enter the Chinese market.

Consequently, real estate developers have entered into partnerships with overseas medical institutions, as detailed below:

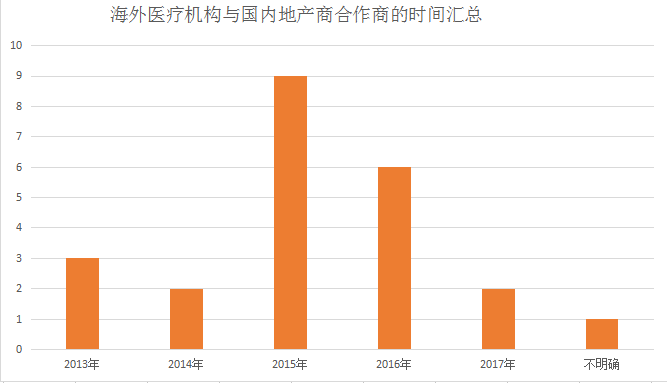

From a temporal perspective, among the statistical sample, the highest number of institutions—nine in total—entered the Chinese market in 2015, followed by six in 2016. Taiwan’s Meizhao Group also established its presence in the Country Garden Forest City project in 2016. This indicates that the entry of medical institutions into the mainland China market experienced explosive growth, concentrated primarily in 2015 and 2016.

Why these two years? This is primarily related to the overall trend of the real estate sector. In 2015–2016, the real estate industry was in a downturn, with the market cooling overall and many property developers facing significant survival pressures. According to VCBeat’s previous report, “What Are the 15 Real Estate Companies Venturing into Healthcare Doing? Mainly Layouts in Four Major Areas,” the proportion of residential investment in total real estate development investment showed a gradual decline. Between 2008 and 2014, the share of residential investment dropped by 4.5 percentage points.

In 2016, coinciding with the launch of the 13th Five-Year Plan, it was proposed to elevate “Healthy China” to a national strategy. This move unlocked a trillion-yuan market, positioning China’s healthcare industry as a new engine for economic growth. In 2014, the healthcare industry generated total revenues of RMB 684.636 billion, a year-on-year increase of 13.57%, and operating profits of RMB 63.386 billion, up 17.71% year on year. Its counter-cyclical nature and high returns have attracted significant attention from real estate developers.

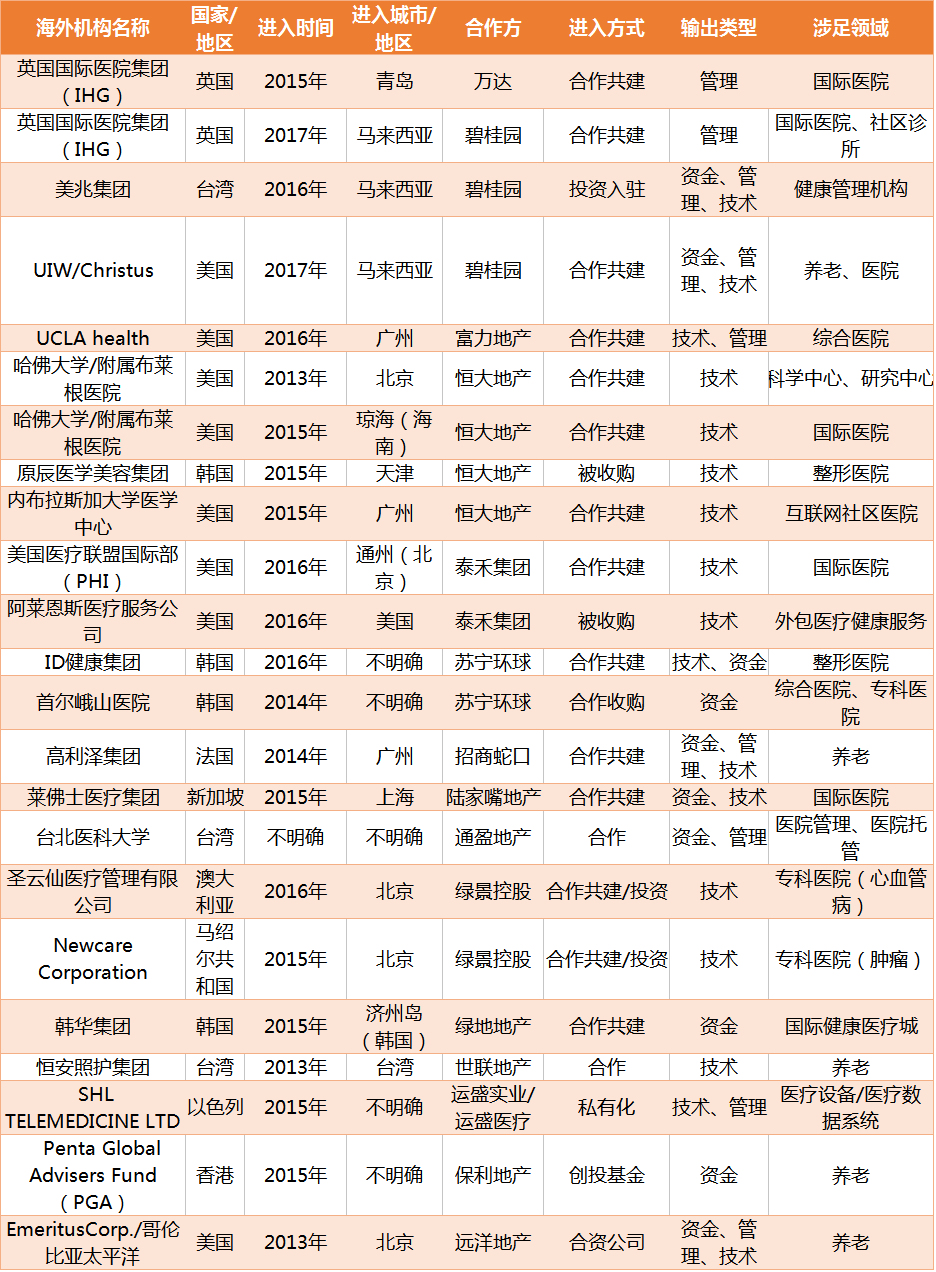

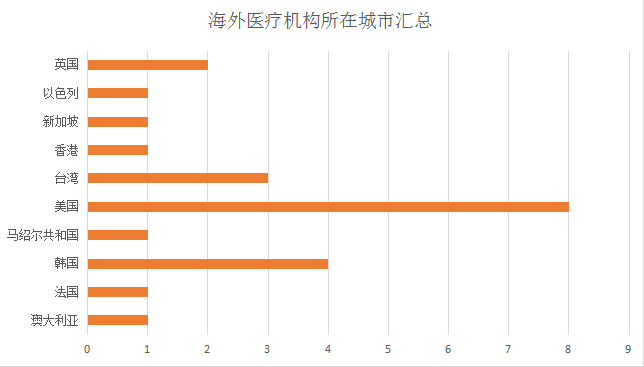

Overseas medical institutions partnering with Chinese real estate developers originate from a total of 10 regions, primarily including the United Kingdom, Israel, Singapore, Hong Kong, Taiwan, the United States, the Republic of the Marshall Islands, South Korea, France, and Australia. Among these, the United States has the highest number with eight institutions, followed by South Korea with four. Most partnerships are established through one-on-one agreements with Chinese real estate developers.

Most collaborations with the United States focus on co-developing hospital operations. As one of the world’s leading hubs for advanced medical resources, the U.S. has clearly chosen to partner with Chinese real estate developers in recognition of China’s vast healthcare market.

South Korea is one of the most developed countries in medical aesthetics. Among the four Korean medical institutions with ties to Chinese real estate developers, two are involved in cosmetic surgery and plastic surgery. Wonjin was acquired by Evergrande, which subsequently established Tianjin Evergrande Wonjin Medical Aesthetic Hospital. Suning Universal and ID Health Group have also collaborated through a joint venture to expand into the cosmetic and plastic surgery market.

In addition, Country Garden, Tongying Real Estate, and World Union Properties have chosen to collaborate with renowned healthcare institutions in Taiwan, focusing on health management, hospital management, and elderly care.

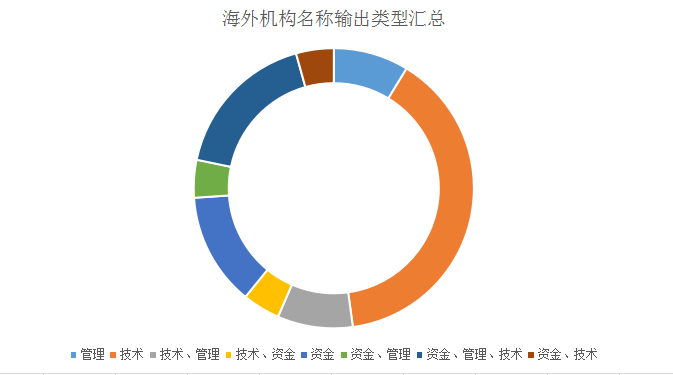

Among the types of services exported by overseas healthcare institutions, three categories are identified: management, technology, and capital. Technological collaboration is the most prevalent, followed by capital investment. This indicates that overseas medical technology surpasses domestic capabilities, particularly in medical theory and pharmaceutical equipment. Furthermore, foreign-funded hospitals investing in China can more conveniently introduce advanced medical technologies.

For example, Cilin Hospital in Cixi, Zhejiang Province, was jointly funded and built by Cixi Health Development Investment Co., Ltd. and the U.S.-based Hospital Corporation of America (HCA). For complex and difficult cases, a team comprising international and local physicians can conveniently conduct remote consultations with U.S. experts using in-operating room cameras, electronic screens, and other equipment.

Therefore, medical technology has become the core resource most favored by real estate developers, with the construction of specialized hospitals being the most typical example. This includes plastic surgery hospitals; South Korea’s long-accumulated resources in the medical aesthetics industry have been introduced into China, naturally commanding strong brand recognition and regarded as representatives of advanced technology.

In summary, the healthcare and pharmaceutical industry is characterized not only by significant policy risks but also by the need for long-term accumulation to build brand recognition, renowned departments, and expert resources. Furthermore, with regard to medical services themselves, brand reputation is one of the key factors influencing patients’ choice of healthcare providers.

Lacking in-house medical resources and seeking to address weaknesses such as brand recognition, real estate companies unfamiliar with the healthcare sector typically seek out superior medical resources from overseas or from Hong Kong, Macao, and Taiwan. This strategy aims to acquire successful operational expertise and facilitate the effective deployment of these resources. The peak volume of collaborations with U.S.-based medical institutions serves as the strongest testament to this trend.

Furthermore, healthcare institutions from overseas and the Hong Kong, Macao, and Taiwan regions are optimistic about the mainland China healthcare market and the substantial strength of real estate developers, leading to frequent collaborations.

However, whether overseas models are suitable for implementation in China remains debatable. Vanke, another real estate giant, had already abandoned opportunities with overseas medical institutions as early as 2014. Vanke’s initial plan was to establish a children’s hospital, with the Children’s Hospital of Philadelphia or the Children’s Hospital of Pittsburgh as its preferred partners. However, the high management fees charged by foreign medical institutions posed a practical challenge. An insider close to the negotiations revealed to the media, “The management fee alone started at tens of millions of U.S. dollars. In China, who can afford that?” Consequently, Vanke shifted its partnership to the Children’s Hospital of Fudan University and adopted a cooperation model combining management fees with revenue sharing.

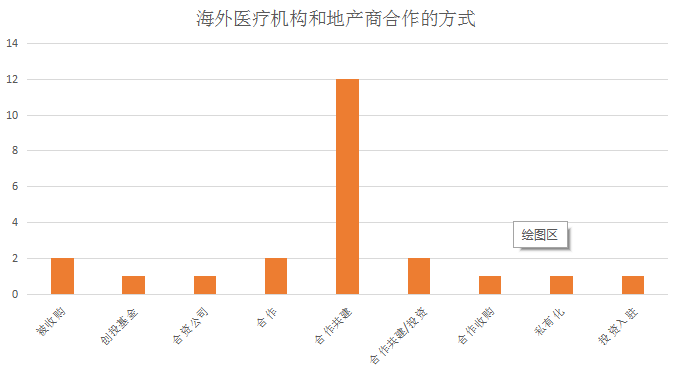

From the perspective of cooperation models, there are a total of nine types, including acquisitions, venture capital funds, joint ventures, partnerships, co-development, investments, collaborative acquisitions, privatization, and investment-based entry. Among these models, co-development is the most prevalent form of collaboration between real estate developers and overseas medical institutions, with a total of 12 cases.

It is evident that for real estate enterprises to diversify into the healthcare industry, they require not only financial support but also mature operational expertise and abundant medical resources. Among the pathways for sharing complementary advantages, cooperative joint development is the most suitable approach.

Although real estate developers adopt similar approaches when partnering with overseas medical institutions, the sectors they enter post-collaboration vary significantly. The primary consideration is synergy with their core businesses; consequently, areas closely related to real estate development, such as hospitals and senior living properties, have become key investment focuses for the “real estate + healthcare” model. Investment in other sectors is determined by their growth prospects and industry characteristics.

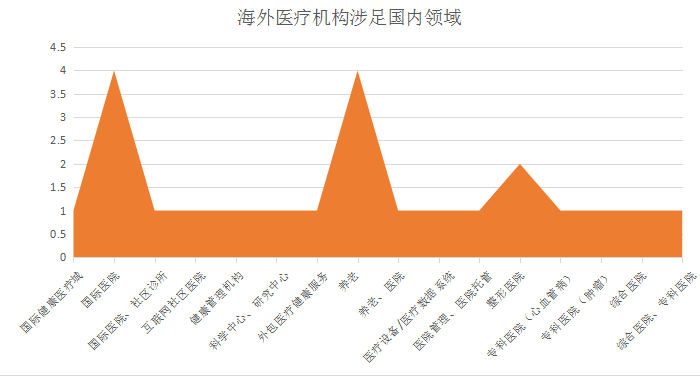

Primarily international hospitals, community clinics, health management organizations, elderly care, hospitals, general hospitals, science centers, research centers, plastic surgery hospitals, internet-based community hospitals, outsourced healthcare services, plastic surgery hospitals, specialized hospitals, elderly care, hospital management, hospital trusteeship, specialized hospitals (cardiovascular diseases), specialized hospitals (oncology), international health and medical cities, elderly care, medical equipment/medical data systems.

Among these, elderly care facilities and international hospitals are the most prevalent. The prominence of elderly care indirectly reflects efforts to cater to China’s rapidly aging population by providing healthcare services centered on seniors, as exemplified by Shilian Real Estate. Meanwhile, international hospitals typically represent high-end medical care; for instance, Wanda Group has partnered with IHG to introduce top-tier comprehensive international hospitals. Wang Jianlin aims not only to meet the growing demand for premium health and medical services but also to drive improvements in the overall standard of high-end healthcare in China.

Among the various possibilities for collaboration between medical institutions and real estate developers, priority has been given to medical sectors with strong synergies with both real estate and healthcare operations. For instance, in the development of international hospitals, companies such as Wanda, Evergrande, Country Garden, and R&F have opted to partner with renowned medical institutions from overseas or Taiwan to co-establish hospitals.

There are three reasons for this: First, real estate developers lack medical resources, and established medical resources require long-term accumulation. Overseas brands such as IHG, Brigham and Women’s Hospital (affiliated with Harvard), and UCLA Health can successfully enter the domestic healthcare services market by leveraging their high brand recognition and leading technologies, positioning themselves in the premium healthcare segment. Their years of accumulated medical expertise are precisely what real estate developers need.

Second, during the co-development process, in addition to providing necessary technology, most medical institutions, such as IHG, primarily contribute costs related to hospital management and operations. This approach breaks away from China’s traditional hospital management model by introducing advanced international management concepts.

Third, policy support in land acquisition. Given the significant price disparity between medical land and residential land, public data shows that in Wanda’s Qingdao Oriental Movie Metropolis project in 2015, the floor price for land designated for medical, health, and charitable purposes was RMB 150 per square meter, for scientific and educational use it was RMB 219 per square meter, while for residential use it reached as high as RMB 2,083 per square meter.

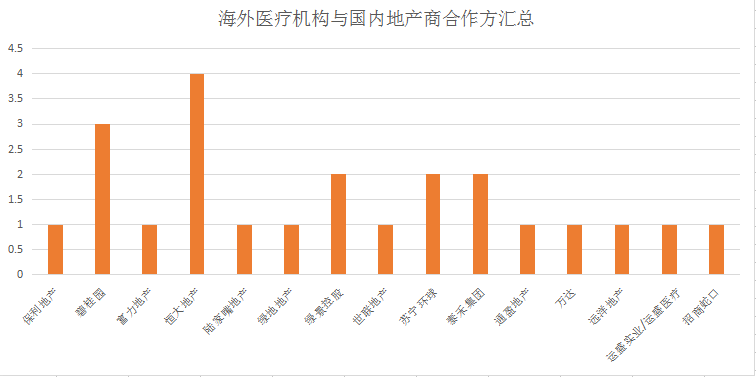

From the perspective of signed real estate partners, the list includes Wanda Group, Country Garden, R&F Properties, Evergrande Real Estate, Taihe Group, Suning Universal, China Merchants Shekou, Lujiazui Real Estate, Tongying Real Estate, Greenview Holdings, Greenland Real Estate, WorldUnion Real Estate, Winshare Industrial/Winshare Medical, Poly Real Estate, and Sino-Ocean Land. Among them, Evergrande Real Estate has collaborated with the highest number of overseas medical institutions, reaching four, followed by Country Garden with three.

As overseas medical institutions deepen their collaboration with real estate developers, an increasing number of such entities may enter the Chinese market in the future, sparking a wave of international healthcare services.

Nevertheless, amidst this wave, the predominant mode of entry for foreign-funded medical institutions into China remains joint ventures and collaborations, although wholly foreign-owned enterprises are emerging as a trend. For instance, Amcare Hospital was jointly established by Warburg Pincus and Lenovo Group; United Family Healthcare was founded in Beijing through a partnership between Chindex and the Chinese Academy of Medical Sciences; Cilin Hospital, the largest Sino-foreign joint venture tertiary hospital in China, was jointly established by Hospital Corporation of America (HCA) and Cixi Health Development Investment Co., Ltd. of Zhejiang Province.

Currently, there are only two wholly foreign-owned hospitals in China: Shanghai Hexin Hospital, which is solely funded by Taiwanese capital, and Shenzhen C-MER Dennis Lam Eye Hospital, which is solely funded by Hong Kong capital.

Furthermore, while introducing foreign-funded medical institutions, China has also imported their advanced management concepts and operational models characterized by clearly defined property rights and responsibilities. Most foreign-funded hospitals are essentially for-profit medical institutions with advanced management systems and flexible operational mechanisms, giving them a comparative advantage over public hospitals in human resource management and allocation.

Most foreign-invested hospitals implement a director responsibility system under the leadership of a board of directors, emphasizing internal management and enabling the establishment and refinement of corporate governance structures. Furthermore, these hospitals feature clear property rights systems, creating positive incentives for owners to preserve and increase asset value. Hospital executives holding equity or stock options are motivated to reduce operational costs and enhance efficiency, thereby achieving superior operational performance.

On the other hand, foreign-funded medical institutions place great emphasis on brand building and the provision of specialized, patient-centered healthcare services. The model for building brand equity in hospitals differs from that in the food and beverage and fast-moving consumer goods (FMCG) sectors, as it entails higher costs and a longer development cycle. Compared with private domestic hospitals, foreign-funded hospitals possess greater experience and patience in brand building; compared with public hospitals, they demonstrate more targeted and distinctive approaches to brand development.

Foreign-funded hospitals possess advanced medical technologies and provide more specialized training for medical staff, enabling them to deliver humanized, high-quality services tailored to mid-to-high-end clientele who prioritize service quality. For instance, BenQ Hospitals in Nanjing and Suzhou emphasize Taiwanese-style medical service models such as the “outpatient consultation accompaniment system,” “attending physician full-responsibility system,” “primary nurse care system,” and “pharmacist medication guidance system,” thereby building a humanistic healthcare brand centered on the philosophy of “starting from the patient’s perspective and serving the patient.”

The introduction of these high-quality services and advanced technologies into medical institutions is bound to promote the progress of China’s healthcare industry!

Take the UK-based IHG (International Hospitals Group) as an example; it has gained increasing recognition through strategic partnerships with leading real estate developers such as Wanda Group and Country Garden.

IHG officially entered the Chinese market in 2015 and, within approximately two and a half years, successively reached strategic cooperation agreements with real estate giants such as Wanda Group and Country Garden. For instance, in January 2016, IHG signed a 20-year strategic partnership with Wanda Group to build and operate ten mid-to-high-end hospitals under the Yingci brand in China. Under this arrangement, Wanda serves as the project owner, while IHG acts as the hospital operator. IHG will ensure that three of these hospitals obtain accreditation from international healthcare organizations, such as the Joint Commission International (JCI).

Wanda’s selection of IHG stems from its historical ties with the NHS (National Health Service, the UK’s National Health Service). In the decades following its privatization—having originated as a joint venture with the UK government—IHG has maintained collaborative relationships with various healthcare organizations within the NHS system. This has enabled IHG to accumulate extensive experience in participating in the development of national healthcare systems. Indeed, against this backdrop, approximately half of IHG’s international business involves assisting governments worldwide in establishing or improving public healthcare service systems.

Under this collaboration, UK-based IHG and China’s Wanda Group have signed a 10-year exclusive partnership agreement for global international hospital projects. The two parties will establish and operate a 200-bed international hospital in Qingdao, with plans to build two additional international hospitals in Shanghai and Chengdu. It is reported that Wanda will invest more than RMB 15 billion in these three projects, which will generate at least RMB 3 billion in revenue for IHG.

The first project to launch is located within the Wanda Cinema in Huangdao District, Qingdao City, with the hospital scheduled to open in 2018. The two parties have established a joint venture for this purpose, in which IHG holds a 70% stake and Wanda holds a 30% stake, aiming to achieve RMB 2.5 billion in revenue within five years after the hospital becomes fully operational. In addition, the collaboration includes IHG introducing training programs from the University of Cambridge’s Judge Business School, designed to cultivate managerial talent for healthcare institutions.

Wang Jianlin, Chairman of Wanda Group, stated, “IHG possesses extensive hospital management expertise worldwide, and we are honored to partner with them. We aim to leverage the UK’s professional strengths in healthcare to create more opportunities for China and other countries. By introducing top-tier comprehensive international hospitals, Wanda not only meets the growing demand for premium health and medical services but also drives the advancement of high-end medical standards in China.”

In 2013, Evergrande’s attempt to partner with a “Harvard-affiliated” hospital was rejected; three years later, it finally achieved its goal. On December 15, 2016, Evergrande Health, a wholly-owned subsidiary of Evergrande Group, announced that Evergrande Group had signed a licensing agreement with Brigham and Women’s Hospital of Harvard to establish Evergrande International Hospital in Boao, Hainan.

Brigham and Women’s Hospital, an affiliate of Harvard Medical School, has been consistently ranked among the best hospitals in the United States for many consecutive years. It is one of the hospitals worldwide with the highest number of Nobel laureates affiliated with it, and it maintains a world-leading position in multiple medical fields, including cancer, cardiology, diabetes, nephrology, rheumatology, endocrinology, and gynecology.

It is reported that in June 2015, Brigham and Women’s Hospital of Harvard Medical School collaborated with Evergrande to conduct site visits in Shenzhen, Sanya, and Guangzhou for the purpose of selecting a location to jointly establish a new type of international hospital in China. Observers have pointed out that both parties may leverage this collaboration to significantly advance the development of such a facility.

Tan Zhaohui, Executive Vice President of Evergrande Group and Chairman of the listed company Evergrande Health, stated that through this collaboration, Harvard-affiliated Brigham and Women’s Hospital will provide guidance to Evergrande Health’s operations in terms of medical philosophy, talent, technology, and management models.

Stephen Thomson, Senior Vice President and Chief Development Officer of Brigham and Women’s Hospital, an affiliate of Harvard Medical School, stated, “We are delighted to have the opportunity to forge this significant partnership, which will enable the global dissemination of Brigham and Women’s Hospital’s advanced medical technologies and highly efficient healthcare services.”

Boao Evergrande International Hospital is positioned as “a specialized oncology hospital built in accordance with international professional standards” and is expected to commence official operations in the first half of 2017. Evergrande stated that Boao Evergrande International Hospital will benefit from nine special preferential policies implemented by the state, including streamlined approval processes for the import of foreign medical devices and pharmaceuticals. Precision medicine initiatives, such as genetic testing, hybrid integrated operating rooms, and particle beam radiotherapy, will also be progressively introduced. Evergrande will collaborate with Brigham and Women’s Hospital of Harvard University to conduct clinical research leveraging the latest international technologies, pharmaceuticals, and clinical protocols, and will engage in translational medicine in partnership with the Evergrande Research Center for Immune Diseases.

In addition to Brigham and Women’s Hospital of Harvard, Evergrande announced that it has successively established strategic partnerships with medical institutions such as Wonjin in South Korea, Theresa in the Netherlands, and Xiaoer in the United Kingdom. Its primary layout encompasses three core service areas: high-end hospitals and tiered healthcare, community healthcare and elderly care, and medical aesthetics and anti-aging.

Currently, Evergrande Health has established a network of micro medical aesthetic clinics in key cities such as Beijing and Guangzhou, with the Evergrande Wonjin Medical Aesthetic Hospital serving as its central hub. On November 28, 2016, Evergrande Health’s wellness real estate project, “Evergrande Wellness Valley,” was unveiled in Sanya. As planned, the Wellness Valley will offer a comprehensive range of health and wellness services, including health education and prevention, medical services, elderly care and rehabilitation, medical aesthetics and anti-aging treatments, and health insurance coverage.

On November 2, 2016, R&F Properties and UCLA Health signed a consulting services agreement at the Park Hyatt Guangzhou, announcing their joint venture to develop a new international hospital in Guangzhou.

UCLA ranks third among hospitals nationwide, with 15 adult specialties and 8 pediatric specialties ranking among the best in the United States. According to the U.S. News & World Report’s 2015–2016 Best Hospitals rankings, UCLA Medical Center rose two spots from its fifth-place ranking in 2014–2015, demonstrating that the comprehensive medical strength of the University of California, Los Angeles Medical Center has gained professional recognition.

The center comprises four hospitals: Ronald Reagan UCLA Medical Center, UCLA Mattel Children’s Hospital, Stewart and Lynda Resnick Neuropsychiatric Hospital, and UCLA Medical Center, Santa Monica. It has 2,000 faculty members (including physicians and non-physicians), 3,350 nurses, and 1,010 residents and fellows. Each year, 1.5 million patients visit the hospitals, and more than 40,000 patients are hospitalized.

This strategic partnership between R&F and UCLA Health was finalized after two years of extensive in-depth discussions and negotiations. Representatives from UCLA Health made multiple visits to China for on-site inspections, to finalize cooperation details, and to discuss hospital site selection, with Guangzhou ultimately chosen as the location. The planned hospital, part of a real estate development, will have a gross floor area of 100,000 square meters and 501 beds, including 400 premium beds and 101 rehabilitation beds.

They are optimistic about the real estate market in the Guangzhou area. By the end of 2015, Guangzhou’s permanent resident population had reached 13.5011 million; however, the total supply of high-quality medical resources was insufficient and unevenly distributed. With the commencement of construction on the new international hospital jointly developed by R&F Properties and UCLA, Guangzhou’s urban healthcare service system is expected to be further improved, thereby enhancing the overall standard of healthcare services.

During the collaboration, R&F will primarily provide hardware services and financial support, with the initial construction phase planned to be managed by its subsidiary hotel management company. In the medical specialty domain, UCLA Health will provide support in technology, equipment, consulting, and management. Ultimately, R&F will establish a professional management team to oversee the operations of the healthcare segment.

Regarding this collaboration, Zhang Li, Chairman and President of R&F Properties, stated: “As an enterprise that has led China’s real estate industry for over two decades, R&F Properties is well aware that responsibility grows with achievement. Our emphasis on corporate social responsibility has guided us to partner with UCLA Health, a leader in the medical community dedicated to the mission of patient care. We need a hospital at the forefront of medical innovation, providing the highest quality of care, and UCLA Health is the ideal partner to help us operate this hospital.”

As early as 2012, Sino-Ocean Land, Emeritus Corp., and CPM, through their respective affiliates, entered into a partnership to establish Beijing Yuanjian Elderly Care Service Co., Ltd., the first operational Sino-foreign joint venture elderly care enterprise in Beijing.

On August 21, 2013, Chunxuanmao Kaijian Senior Living Apartment, jointly invested and operated by Sino-Ocean Land, CPM, and Emeritus Group, officially commenced operations. As Sino-Ocean Land’s first implemented elderly care project, it is a high-end senior care facility spanning nearly 6,000 square meters, located within the Sino-Ocean Tianzhu premium residential complex in Yizhuang, southeastern Beijing.

Emeritus Corp. is a national senior care operator in the United States and one of the largest and most experienced operators of assisted living communities for the elderly. These communities offer a new lifestyle for seniors who require assistance with activities of daily living, focusing on personal care services to support the aging resident population.

Emeritus Corp. currently operates more than 518 communities, serving over 50,000 residents across 45 states. The company is listed on the New York Stock Exchange under the ticker symbol ESC.

Chunxuanmao (Yizhuang) Senior Living, a Sino-US collaborative venture, primarily provides high-quality care services for semi-disabled and disabled elderly residents. It is the premier senior living facility to have received LEED-CS pre-certification from the U.S. Green Building Council (USGBC).

In building professional elderly care services, Chunxuanmao has introduced U.S. concepts of eldercare, operational systems, and caregiving expertise. Through a rich array of cultural, recreational, and social activities, as well as psychological support services, it helps seniors maintain normal functioning in psychological, physiological, and social domains, while preserving the continuity of their social roles.

Emeritus Group’s collaboration with Sino-Ocean Land includes the establishment of joint ventures and technology transfer, leveraging the export of U.S.-based professional care and elderly care philosophies.

Currently, Sino-Ocean’s elderly care industry has successfully entered key cities such as Beijing, Shanghai, Guangzhou, and Wuhan, as well as coastal cities like Dalian. Its strategic development layout in key cities and along the coast and major rivers has begun to take shape, with six projects expected to open in 2017. The first Sino-foreign joint venture in elderly care real estate holds obvious significance for Sino-Ocean’s subsequent strategic layout.

With the management and operational experience gained from its first Chunxuanmao facility, the three senior living real estate projects subsequently launched by Chunxuanmao in Beijing inevitably bear some imprint of American senior living models.

Currently, Chunxuanmao’s product offerings are categorized into three types: small- to medium-sized CB Senior Living Apartments (Care Building), large-scale CLRC Senior Living Communities (Continuing Living Retirement Community), and the newly added Care Centers.

Sino-Ocean Land’s asset-light elderly care business model is characterized by its distinctive approach, primarily involving investment, leasing, or entrusted management of such properties to provide comprehensive, end-to-end elderly care services. These services include independent living, personal care, dementia care, rehabilitation services, adult day care, and home-based care. The Yizhuang, Shuangqiao, and Qingta Chunxuanmao projects are all operated under an asset-light model, involving the leasing and subsequent renovation of properties for operational purposes. Notably, the property leased for the Yizhuang project is Sino-Ocean Land’s own development, Sino-Ocean Tianzhu.

Here is a set of data: In the United States, the current cash-on-cash return rate for the senior living community industry stands at 8%-11%, with an internal rate of return (IRR) ranging from 10% to 20%, and an investment horizon of 8 to 10 years. Meanwhile, as of 2016, the Yizhuang project had achieved an occupancy rate of 80%.

Industry experts in the elderly care sector have revealed to the media that a senior living project needs an occupancy rate of over 70% to achieve profitability. By 2016, Sino-Ocean Land’s Chunxuanmao had already reached an occupancy rate of 80%.

In addition, dementia care is a major specialty of Chunxuanmao. In 2015, by introducing the dementia care program of MERIDIAN, the third-largest dementia care operator in the United States, Sino-Ocean Group established “Yi Lu Tong Xing” (Walking Together on the Path of Memory), China’s first internationally benchmarked dementia care program rooted in Chinese culture. Its distinguishing feature lies in recreating life scenes from the eras familiar to older adults with dementia, thereby helping to slow the progression of memory decline.