Strategic Layout of the Top 10 Global IVD Giants in China Over the Past Two Decades and Emerging Opportunities for Domestic IVD Companies

In Vitro Diagnosis (IVD) refers to products and services that obtain clinical diagnostic information by testing human samples (such as blood, body fluids, and tissues) outside the human body, thereby assessing diseases or physiological functions.

According to Roche Diagnostics’ statistics, in vitro diagnostics (IVD) influence 60% of clinical treatment decisions, yet account for only 2% of total healthcare costs. IVD has become an increasingly vital component in the prevention, diagnosis, and treatment of human diseases, playing a growing role in safeguarding public health and building a harmonious society.

Based on different detection principles and methods, in vitro diagnostics (IVD) can be categorized into clinical chemistry diagnostics, immunoassay diagnostics, molecular diagnostics, microbiological diagnostics, urinalysis, coagulation diagnostics, hematology and flow cytometry diagnostics, among others. Currently, the predominant IVD methodologies in China are clinical chemistry diagnostics, immunoassay diagnostics, and molecular diagnostics.

Global In Vitro Diagnostics (IVD) Market Size & Competitive Landscape

In recent years, the global incidence and prevalence of infectious diseases have been on the rise, while the number of individuals suffering from chronic diseases continues to grow, driving the continuous expansion of the in vitro diagnostics (IVD) market. As the largest segment within the global medical device industry, the IVD sector, a highly lucrative market, has attracted significant attention from industry insiders.

Data sources: Wind, Global In-Diagnostics Market Forecast to 2018, Fencun Capital

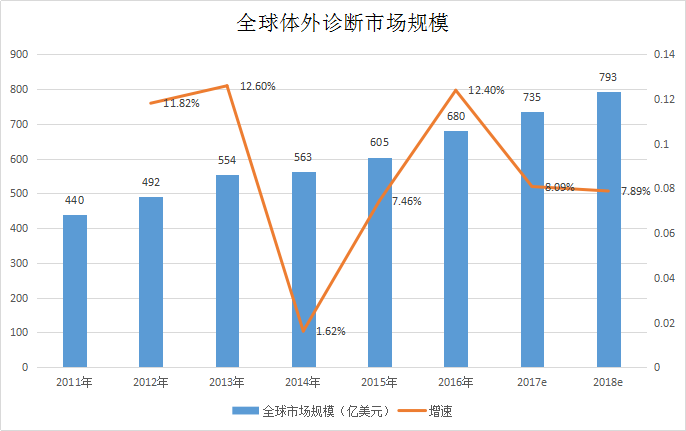

According to statistics from authoritative institutions, the global in vitro diagnostics market was valued at $60.5 billion in 2015 and is projected to potentially exceed $80 billion by 2018.

Data Source: China Industry Insight Network, Fencun Capital

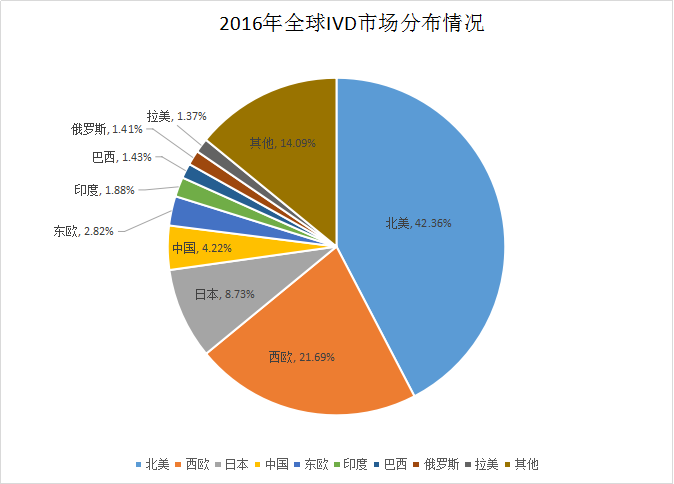

Geographically, North America is the largest in vitro diagnostics (IVD) market globally. In 2016, the North American IVD market accounted for 42.36% of the global share, while Europe represented 24.51%. Together, these two major markets comprised over 65% of the global market. However, due to slowing population growth and price reductions for IVD products in Europe and North America, the overall market has been experiencing slow growth.

In the Asian in vitro diagnostics (IVD) market, Japan holds the largest share, accounting for 8.73% of the market. Other emerging markets in Asia, such as China and India, are witnessing rapid growth in the IVD sector, driven by their large populations, rapid economic development, and increasing healthcare investments. In 2016, China accounted for 4.22% of the global IVD market share.

From the perspective of the competitive landscape, leading companies continue to demonstrate outstanding performance. The top ten in vitro diagnostics (IVD) companies account for 80% of the global market share. Among them, the top five—Roche, Danaher, Siemens, Abbott, and Thermo Fisher Scientific—possess resources and core technologies spanning the entire IVD industry chain, giving them a particularly pronounced advantage.

VCBeat (WeChat ID: vcbeat)A Top 10 Ranking of Global IVD Device Companies Based on Their 2016 Diagnostic Business Revenue

★ The ranking is limited to companies that disclosed their 2016 diagnostic business sales revenue; therefore, companies that did not disclose such information are excluded from consideration.

As shown in the chart, the global in vitro diagnostics (IVD) market is highly competitive. Among the top ten IVD device giants, nine are from Europe and the United States, with the United States alone accounting for six spots. Japan’s Sysmex is the only Asian company to rank among the top ten. In 2016, the total diagnostic sales revenue of these top ten IVD device giants reached $38.641 billion, with Roche Diagnostics leading the list at $11.473 billion in revenue.

China's In Vitro Diagnostics (IVD) Market Size & Competitive Landscape

Compared with the total size of the international IVD market, China’s share is relatively small (accounting for only 4.22% in 2016). However, driven by rising household incomes, growing demand for disease diagnosis, prevention, and health management, and strong government support, China’s IVD industry has expanded rapidly in recent years. It has become one of the fastest-growing segments within China’s healthcare system, offering substantial growth potential and attracting significant interest from capital markets.

Data Source: China Investment Advisor Industry Research Center

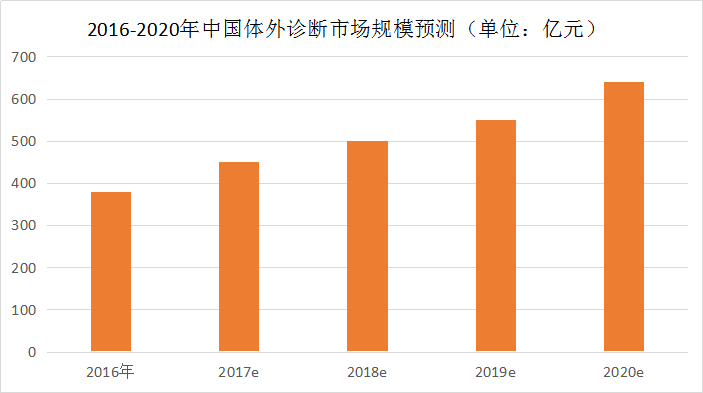

According to projections by the Industry Research Center of China Investment Advisor, the in vitro diagnostics (IVD) sector is expected to maintain a compound annual growth rate of 15% over the next five years, with the Chinese IVD market size projected to reach approximately RMB 64 billion by 2020. Given that diagnostic reagents account for 80% of the Chinese IVD market and diagnostic instruments constitute the remaining 20%, the market size for IVD instruments in China is estimated to reach RMB 13 billion by 2020.

In terms of the competitive landscape, the current Chinese in vitro diagnostics (IVD) market is primarily dominated by two major groups: multinational corporations and domestic enterprises. Overall, there remains a certain gap between Chinese IVD manufacturers and multinational companies.Multinational corporations, leveraging their advanced technology, brand advantages, and consistent quality, account for 56% of China’s in vitro diagnostics (IVD) market.It holds a monopoly in the high-end market of Grade 3A hospitals, with prices ranging from one to five times those of similar domestic products.

Data Source: China Industry Information Network

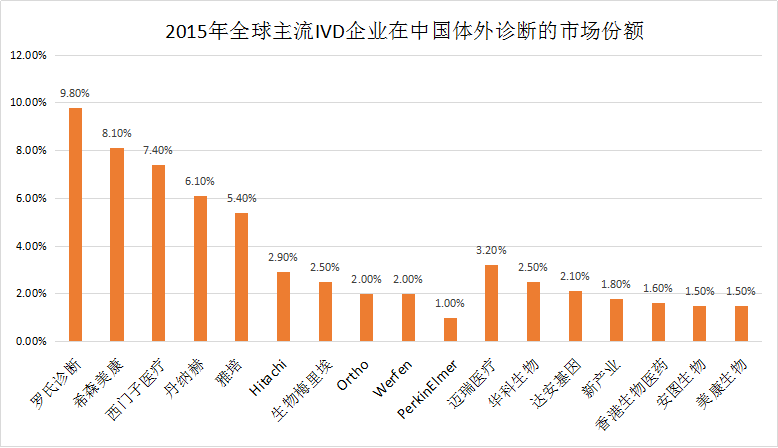

In 2015, the top five multinational IVD companies accounted for 36.8% of China’s in vitro diagnostics market share. Among them, Roche held a leading position with a 9.8% market share; Sysmex, Siemens, Danaher (which has acquired Beckman), and Abbott had market shares of 8.1%, 7.4%, 6.1%, and 5.4%, respectively.

Chinese IVD companies started relatively late and still lag significantly behind internationally renowned diagnostic firms in terms of scale, strength, technology, and product quality. However, leveraging their cost-effective products and closer proximity to the local market, domestic enterprises have been continuously gaining market share. A number of strong local players have emerged, primarily concentrated in the three major sectors of clinical chemistry, immunoassay, and molecular diagnostics.

Domestic IVD companies are characterized by small scale and large numbers. According to statistics, there are currently 300–400 manufacturers of in vitro diagnostics in China, most of which are small and medium-sized enterprises. Their product coverage is relatively narrow, mainly consisting of mid-to-low-end products in a single field, with users concentrated in municipal hospitals and primary healthcare institutions, resulting in a relatively fragmented market landscape. Moreover, the sales revenue of domestic IVD companies is generally concentrated in the range of RMB 10 million to 50 million, with few companies exceeding RMB 100 million in revenue. The top ten companies account for only about 30% of the market share.

How Are the Top 10 IVD Device Giants Strategizing in China?

Although the monopoly of multinational IVD companies in China has been slightly weakened in recent years with the rise of domestic brands, there is still a long way to go to truly achieve “import substitution.” VCBeat has attempted to analyze the current development status of the top ten global IVD device companies and their strategic layouts in China over the years, which may help domestic IVD companies find new breakthroughs.

Roche is a global leader in the pharmaceutical and diagnostics sectors. Founded in 1896 and headquartered in Basel, Switzerland, the company operates in more than 100 countries worldwide. The Group’s core businesses comprise two divisions: Pharmaceuticals and Diagnostics, with the latter accounting for 23% of its operations. Roche Diagnostics’ products are primarily used to test blood, tissues, and other bodily fluids, providing healthcare professionals with essential information for diagnosis and treatment. In 2016, Roche Diagnostics generated revenue of CHF 11.5 billion (approximately USD 11.5 billion), ranking first in the global in vitro diagnostics (IVD) market.

Within Roche’s Diagnostics division, Core Laboratory and Point-of-Care (POC) Testing (formerly Professional Diagnostics) account for 58%, Diabetes Care for 18%, Molecular Diagnostics for 16%, and Tissue Diagnostics for 8%. Among these, the clinical chemistry and immunoassay business (the largest in volume) demonstrates the most stable growth, while molecular diagnostics is the fastest-growing segment.

In 2000, Roche Diagnostics officially entered the Chinese market and established its headquarters in Shanghai. Over the past decade and more, Roche has set up branches or representative offices in Beijing, Guangzhou, Shenyang, Xi’an, Wuhan, Chengdu, Nanjing, and Hangzhou. Roche Diagnostics employs over 2,000 people in China. Today, China has become Roche Diagnostics’ second-largest market globally, after the United States. The company’s average annual growth rate in the Chinese market has remained steady at approximately 25%.

● In 2000, Roche Diagnostics officially entered China;

● In 2008, Roche Diagnostics established its Guangzhou and Beijing branches, respectively;

● In 2009, Roche Diagnostics established its branch offices in Shanghai Xuhui, Nanjing, and Hangzhou, respectively;

● In November 2014, Roche Diagnostics invested approximately USD 2.5 billion to establish its Asian production base in the Suzhou Industrial Park (its eighth largest production base globally).

Danaher is a global leader in the design and manufacture of science and technology innovation products and services. Headquartered in Washington, D.C., United States, its business spans multiple technological fields, including electronic testing, power systems, machine tools, environmental controls, product identification, and medical devices. Danaher ranked 267th on the 2017 Fortune Global 500 list.

The company primarily operates five business segments: Test & Measurement, Environmental, Dental, Life Sciences & Diagnostics, and Industrial Technologies. Danaher’s in vitro diagnostics business (including Beckman Coulter Diagnostics, Leica Diagnostics, Radiometer, and Cepheid) accounts for 30% of the group’s total business, second only to Life Sciences, with a mere one-percentage-point difference between the two.

Danaher’s full-year 2016 revenue reached $16.88 billion, representing a 17% increase from the $14.43 billion recorded in 2015. Diagnostic revenue rose by 4%, from $4.83 billion to $5.04 billion. This growth was primarily driven by Danaher’s $4 billion acquisition of Cepheid, a global leader in molecular diagnostics, on September 6 of the previous year, which expanded its diagnostics portfolio. In terms of global business distribution, Danaher maintained its leading market share in China and India. Latin America, the Middle East, and Russia saw a gradual return to growth, while core revenue growth in developed markets remained in the low single digits, driven by increases in the United States and Western Europe.

Danaher’s presence in China was primarily established in 2011 through its $6.8 billion acquisition of Beckman Coulter, which secured Beckman’s position in the Chinese diagnostics market. Beckman Coulter was the first foreign IVD company to enter China and the first to build a manufacturing facility in the country. In China’s in vitro diagnostics (IVD) market, Beckman ranks second, trailing only Roche.

● As early as 1983, Beckman began establishing representative offices and service centers in Chinese cities such as Beijing, Shanghai, Guangzhou, and Fuzhou;

● In 1997, Beckman established a reagent manufacturing plant in Suzhou, Jiangsu Province, to supply the entire Chinese market, Southeast Asia, and Japan. The facility is named Beckman Coulter Experimental Systems (Suzhou) Co., Ltd., with an initial investment of US$5 million;

● In 2011, Danaher acquired Beckman Coulter for $6.8 billion;

● In 2015, Beckman Coulter, led by Danaher, established a research and development center in Suzhou and expanded the scale of its original manufacturing facility. This marked the official commencement of competition among the three giants—Roche, Beckman Coulter, and Siemens—in the localization of reagents within China’s IVD market.

Siemens AG is a global technology leader founded in 1847, with operations in more than 200 countries and a focus on electrification, automation, and digitalization. In 2015, Siemens Healthineers was spun off from the group and has since maintained its strengths in diagnostic imaging and in vitro diagnostics, continuously introducing innovative products while vigorously expanding into areas such as point-of-care testing and molecular diagnostics.

Siemens Healthineers boasts the most comprehensive IVD product portfolio, encompassing immunoassay, clinical chemistry, molecular diagnostics, hematology, coagulation, and POCT, making it the manufacturer with the most extensive footprint in the IVD sector. In 2016, Siemens AG reported total annual revenue of €13.5 billion, a 4.8% increase from 2015. Siemens Healthineers’ IVD business generated approximately $4.9 billion in sales in fiscal year 2016, ranking third globally in the IVD market. Meanwhile, Siemens’ total revenue in China reached €6.44 billion in 2016.

Siemens’ presence in China dates back to 1985, when it signed a memorandum of understanding with the Chinese government, becoming the first foreign enterprise to engage in in-depth cooperation with China. Subsequently, it established a medical devices subsidiary and a medical diagnostics products subsidiary in Shanghai in 1992 and 2000, respectively. In 2016, Siemens Healthineers announced that its first diagnostic reagents manufacturing plant in the Asia-Pacific region would be located in Shanghai. To date, Siemens Healthineers employs more than 5,000 people in China.

● In 1985, Siemens signed a memorandum of cooperation with the Chinese government, becoming the first foreign enterprise to engage in in-depth collaboration with China;

● 1992: Shanghai Siemens Medical Devices Co., Ltd. was established;

● In 2000, Siemens Medical Diagnostics Products (Shanghai) Co., Ltd. was established;

● In October 2015, Siemens spun off its healthcare business into a new company within the Siemens Group, establishing separate legal entities in China and globally;

● In 2016, Siemens Healthineers announced that its first diagnostic reagent manufacturing plant in the Asia-Pacific region would be established in Shanghai.

Abbott is a global, diversified healthcare company founded in 1888 and headquartered in Illinois, USA. In 2017, Abbott had approximately 94,000 employees worldwide, with operations in more than 150 countries and regions.

Abbott’s healthcare business is primarily divided into three segments: pharmaceuticals (28%), medical devices (38%, including cardiovascular, ophthalmology, and diabetes care), and in vitro diagnostics (IVD) (34%). Abbott Diagnostics focuses on the entire continuum of disease management, from early detection and diagnosis to therapeutic monitoring, providing laboratories with comprehensive solutions encompassing pre-analytical processing, automation, clinical chemistry, immunoassay, hematology, and informatics products. In fiscal year 2016, Abbott Diagnostics recorded sales of approximately $4.65 billion, ranking fourth in the global IVD market.

Abbott has been operating in China for nearly 20 years, providing Chinese consumers with a wide range of nutritional products, pharmaceuticals, and medical devices. Currently, in addition to establishing its China headquarters in Shanghai, Abbott has set up 10 offices, three manufacturing plants, and two research and development centers, employing more than 4,000 people.

● In 1995, Abbott established offices in Beijing and Shanghai, officially entering the Chinese market, and subsequently set up additional offices in Guangzhou and Shenzhen;

● 1998: Established Shanghai Abbott Pharmaceutical Co., Ltd.;

● In 2000, Abbott's Shanghai plant obtained GMP certification;

● In September 2016, Abbott’s China R&D Center was officially inaugurated. Comprising the Abbott Nutrition China R&D Center and the Abbott Diagnostics China R&D Center, it is Abbott’s only global R&D center that integrates both nutrition and diagnostics businesses.

To date, Abbott remains the only one among the “Big Four” IVD companies that has not yet established a diagnostics manufacturing facility in China. Given China’s vast potential as an IVD market, localizing production and services by foreign enterprises is an inevitable future trend.

Thermo Fisher Scientific, a Fortune 500 company in the United States, is a global leader in scientific services. Headquartered in Massachusetts, USA, the company traces its roots to Thermo Electron Corporation, which was founded in 1956. In 2006, Thermo Electron Corporation merged with Fisher Scientific International Inc. to form Thermo Fisher Scientific Inc.

The company’s core businesses include instrument manufacturing, laboratory construction, and biotechnology products. In 2016, the group’s total revenue reached $18.274 billion, with its professional diagnostics segment accounting for 18% and generating approximately $3.339 billion in revenue, a 3% increase from 2015, ranking it fifth globally in the in vitro diagnostics (IVD) sector. Geographically, Thermo Fisher Scientific’s operations are distributed as follows: North America accounts for 53%, Europe for 25%, Asia-Pacific for 18%, and other markets for 4%.

Thermo Fisher Scientific has been operating in China for over 30 years. Its China headquarters is located in Shanghai, with branch offices established in Beijing, Guangzhou, Hong Kong, Taiwan, Chengdu, Shenyang, Xi’an, Nanjing, Wuhan, and Kunming, employing approximately 3,700 people. To meet the demands of the Chinese market, the company currently operates eight manufacturing facilities in Shanghai, Beijing, and Suzhou.

Unlike most foreign enterprises, which rely almost entirely on agency models, Thermo Fisher Scientific has adopted a strategy for the Chinese market that emphasizes the deployment of R&D teams and strengthened collaboration with Chinese clients. Currently, Thermo Fisher Scientific has established six application development centers across China and forged partnerships with medical institutions in various sectors. These include co-establishing a Joint Research Platform for Precision Medicine with West China Hospital of Sichuan University; jointly launching a Center of Excellence for Precision Medicine in Tianjin with Novogene; collaborating with The First Affiliated Hospital of Sun Yat-sen University in Guangzhou to establish a Center for Precision Medicine and Molecular Diagnostics; and partnering with the Molecular Diagnostics Center of Beijing Fuwai Hospital to create a Joint Training Center for Precision Medicine.

● In 1982, Thermo Electron established a sales office in China, officially entering the Chinese market;

● In 2000, the thermoelectric company established a production base in China, with the factory on Jinmin Road in Pudong, Shanghai, being founded;

● In 2005, Thermo Fisher Scientific established an advanced customer experience center in China and simultaneously founded its Beijing manufacturing facility;

● In 2006, the third factory in Shanghai was established in Jinqiao, Pudong;

● In 2010, Thermo Fisher Scientific established its China Technology Center in Shanghai;

● In 2011, China's service footprint expanded to second- and third-tier cities, with the establishment of branch offices in Shenyang and Chengdu;

● In 2012, the service footprint continued to expand into central and western China, with the establishment of branch offices in Wuhan and Xi’an, and the Suzhou manufacturing facility was completed and commenced operations.

● In 2013, Thermo Fisher Scientific established its China Innovation Center in China, and the Thermo Fisher Scientific Wuhan Office was officially launched.

Alere is the dominant player in the point-of-care testing (POCT) sector, dedicated to empowering individuals to proactively improve their health and quality of life at home by developing new capabilities in point-of-care diagnostics (POCT), monitoring, and health information technology. It helps diverse populations worldwide manage challenging diseases, including infectious diseases, toxicological conditions, cardiovascular diseases, and diabetes.

QuidelOrtho is headquartered in Waltham, Boston, USA. It has more than 50 branches worldwide, nearly 20,000 employees, and an R&D team of over 800 people. The company’s overall business is divided into two sectors: professional diagnostics and consumer diagnostics, with professional diagnostics accounting for 97% of its total business. Cardiac markers, infectious diseases, and toxicology diagnostics have always been QuidelOrtho’s core businesses.

In 2016, Alere’s revenue was approximately $2.38 billion, representing a 3% increase from 2015. It accounted for over 40% of the global POCT market share and ranked sixth in the global IVD sector.

Since entering the Chinese market in 2005, Alere has provided a diverse range of diagnostic tests and platforms in China, covering areas such as acute cardiovascular disease diagnosis, chronic disease management (including diabetes), infectious disease diagnosis, toxicology testing, women’s health, and oncology, spanning over one hundred disease categories. In 2006, Alere acquired Hangzhou Aibo, establishing it as its regional headquarters in China. In 2007, Inverness Medical Devices (Beijing) Co., Ltd. was established, and it was officially renamed Alere Inc. in 2010. Additionally, Alere places significant emphasis on talent development in China by introducing management courses from CEIBS (China Europe International Business School) and creating the “SHINE” manager training program and the “HPM” senior manager development program.

● In 2005, established Shanghai Imbicon Med-Biotech Co., Ltd., primarily engaged in the development of rapid diagnostic test kits for women's health (pregnancy and ovulation) and infectious diseases.

● 2006: Acquired Hangzhou Aibo to serve as its China headquarters;

● In 2007, Invilis Medical Devices (Beijing) Co., Ltd. was established, integrating marketing and sales functions;

● In 2010, the company was officially renamed Alere Inc. Alere (China) serves as the China regional management headquarters for the Alere Group, established in China with management and strategic planning functions.

● In 2012, established Meiai'er (Biological) Technology Co., Ltd. in Shanghai;

● In 2014, MyAir (Shanghai) Health Management Co., Ltd. was established in Shanghai.

Sysmex Corporation, formerly known as Toa Medical Electronics Co., Ltd., is headquartered in Kobe, Japan. With more than 40 branches across China, Europe, the Americas, and the Asia-Pacific region, its products are distributed in over 170 countries worldwide.

Currently, Sysmex holds a world-leading position in the fields of hematology analysis, coagulation analysis, and urine sediment analysis. The hematology business accounts for 65% of Sysmex’s total revenue, followed by the coagulation business at 14%, and the urinalysis business at 8%, with other businesses comprising smaller shares. Sysmex commands over 45% of the market share in the hematology sector. In 2016, its revenue reached JPY 253.1 billion (approximately USD 2.29 billion), ranking seventh in the global IVD market. It is the only Japanese company among the top ten IVD companies worldwide.

Sysmex’s revenue from the Japanese domestic market has been steadily declining. In fiscal year 2016, Japan accounted for only 15.7% of total revenue, while overseas markets contributed 84.3%. Among these, China ranked second with a 25.8% share, just behind emerging markets (including Europe, the Middle East, and Africa) at 26.9%, while the Americas accounted for 23.6%.

In fiscal year 2016, Sysmex’s revenue in the Chinese market increased by 30.7% year-on-year, primarily driven by growth in its hematology and coagulation businesses. However, Sysmex relies heavily on an agency-based distribution strategy in China, with distributors accounting for as much as 98.7% of its sales. This has increasingly eroded Sysmex’s control, to the extent that local distributors can even “dictate” its business direction. Should these distributors choose to compete directly (as Mindray has done), they could significantly squeeze Sysmex’s market share.

January 2000,Sysmex Medical Electronics (Shanghai) Co., Ltd. was established. Currently, Sysmex has a Beijing office in China and has set up liaison points in multiple provinces and cities, with sales support and customer service outlets covering the entire country.

● In June 1995, a Sino-foreign joint venture, Jinan Dongya Medical Electronics Co., Ltd. (now Jinan Sysmex Medical Electronics Co., Ltd.), was established for the purpose of reagent production; it was converted into a wholly foreign-owned enterprise in 2000;

● In 1996, the Shanghai Representative Office of Sysmex Corporation was established to support business operations across China;

● In December 1999, Sysmex Hong Kong Limited was established;

● In January 2000, Sysmex Medical Electronics (Shanghai) Co., Ltd. was established to oversee marketing and service management for the Hong Kong and mainland China regions;

● In July 2000, Sysmex Infosystems (Shanghai) Co., Ltd. was established to provide Chinese-language data management systems compatible with original equipment manufacturer (OEM) instruments, as well as professional information management software;

● In August 2003, established the second reagent manufacturing facility in China, Sysmex Biotechnology (Wuxi) Co., Ltd.

BioMérieux, founded in Lyon, France, is dedicated to the development of diagnostic products for clinical medical and industrial applications. As the largest in vitro diagnostics (IVD) company in France and the world’s largest IVD company specializing in microbiology, BioMérieux holds the number one global market share in clinical and industrial microbiology. It ranks third worldwide in the infectious disease diagnostics sector, with particular expertise in the diagnosis of HIV/AIDS and tuberculosis.

Currently, the Group operates three global headquarters in Lyon (France), Boston (USA), and Shanghai (China), with 41 subsidiaries, branches in 150 countries, 19 production bases, and 20 R&D centers, employing over 10,000 people.

BioMérieux’s business is divided into two segments: clinical diagnostics, which accounts for 80%, and industrial diagnostics, which accounts for 20%. The company’s product portfolio primarily focuses on microbiology, immunology, and molecular biology, encompassing instruments, reagents, and other services. As a leader in the microbiology niche, BioMérieux holds a market share of up to 40%, with 80% of its revenue derived from reagents. In 2016, the BioMérieux Group reported total revenue of €2.103 billion, of which the clinical diagnostics segment generated €1.678 billion (approximately $2.006 billion).

The ties between bioMérieux and China can be traced back to the ancestors of its founder, Mr. Mérieux. During the early stages of China’s reform and opening-up, members of the Mérieux family had already engaged with Chinese national leaders, subsequently paving the way for the company’s gradual entry into the Chinese market. In 2011, bioMérieux completed its new Shanghai Pudong facility, which became its third-largest base globally, following those in France and the United States. Currently, bioMérieux China has established an R&D team dedicated to the localization and development of its full product portfolio. The company has maintained double-digit revenue growth in China for over a decade, with an average annual growth rate exceeding 25% prior to 2015.

● In 1978, Mr. Mérieux visited China for the first time and established cooperation with the Chinese Ministry of Health in the field of public health;

● In 1985, the first VITEK instrument was installed at Beijing Hospital of the Ministry of Health;

● 1992–2001: Offices were successively established in Beijing, Shanghai, Chengdu, and Guangzhou;

● In 2004, the headquarters of China and ASPAC were relocated to Shanghai;

● In 2011, bioMérieux established its China Campus in Pudong, making it the Group’s third-largest global headquarters (the other two are located in Boston and Lyon).

Bio-Rad, established in 1952 and headquartered in Hercules, California, has evolved over more than six decades into one of the few leading high-tech companies in the life sciences and clinical diagnostics sectors. Its Life Science Group ranks among the top five globally, while its Clinical Diagnostics Group is ranked within the top ten worldwide. Currently, Bio-Rad operates more than 30 subsidiaries across the globe, employs over 8,250 people, and conducts business in more than 150 countries.

Bio-Rad’s primary business is divided into two segments: Life Sciences and Clinical Diagnostics, which account for 35% and 64% of the group’s total business, respectively. Its main products include ELISA instruments and assay kits, gene mutation analysis products, HbA1c analyzers and reagents, among others.

In 2016, Bio-Rad’s total revenue reached $2.07 billion, representing a 2.4% increase from $2.02 billion in 2015. The Life Science segment generated $731 million in revenue, a year-on-year growth of 5.1%, while the Clinical Diagnostics segment recorded $1.32 billion, up 1% year on year, with the fastest growth seen in immunoassay, blood typing, and diabetes care businesses. Geographically, 37% of the company’s revenue came from the United States, with the remaining 63% derived from overseas markets.

As China is one of the major markets for in vitro diagnostics (IVD), Bio-Rad naturally places significant emphasis on this region. Currently, Bio-Rad has established offices in Shanghai (headquarters), Beijing, Guangzhou, and Hong Kong, and set up a bonded warehouse in Waigaoqiao, Shanghai. These locations are staffed with technical support, customer service, maintenance, and commercial personnel, forming a specialized and localized team.

In 2009, Bio-Rad Laboratories (Shanghai) Co., Ltd. was officially established in Zhangjiang, Shanghai. This marked the formal establishment of the Bio-Rad (Shanghai) R&D Center as Bio-Rad’s first research and development base in the Asia-Pacific region, laying the foundation for Bio-Rad’s manufacturing operations in China and facilitating its further growth in the Chinese market.

Becton, Dickinson and Company (BD) is a globally renowned supplier of disposable medical products. Founded in 1897 and headquartered in Franklin Lakes, New Jersey, USA, the company has acquired more than ten related medical device and equipment manufacturers over its century-long history, establishing itself as one of the world’s largest medical technology and equipment corporations. Currently, BD maintains branch offices, research and development centers, and manufacturing facilities in over 50 countries and regions worldwide. Its business operations span six continents, and it employs more than 45,000 people.

BD’s operations are divided into two major segments: BD Medical and BD Life Sciences, with its diagnostics business falling under the Life Sciences segment. In 2016, BD’s total revenue reached $12.5 billion, of which $1.301 billion came from the diagnostics business. Notably, by fiscal year 2014, BD had achieved annual growth rates exceeding 20% in the Chinese market for several consecutive years, surpassing Japan to become its second-largest market after the United States.

From medical consumables to in vitro diagnostics (IVD), and further to pre-analytical specimen processing, BD is expanding into second- and third-tier markets leveraging its extensive product portfolio and actively seeking more partners of this kind. In recent years, BD has achieved significant success in the Chinese market by expanding its collaboration with Sinopharm’s distribution channels and through mergers and acquisitions. Currently, BD has established a business footprint in China with its headquarters in Shanghai and 16 branch offices in cities including Beijing and Guangzhou, employing a total workforce of 3,000.

● In 1994, BD officially dispatched personnel to register and establish a representative office in China, commencing its business operations in the Chinese market;

● In August 1995, BD invested US$25 million to establish a manufacturing entity, Suzhou Becton Dickinson Medical Devices Co., Ltd., in the Suzhou Industrial Park;

● Since 2005, BD has invested a total of US$48 million to establish Becton Dickinson Rapid Diagnostic Products (Suzhou) Co., Ltd. in the Suzhou Industrial Park;

● At the end of 2008, BD made an additional investment of $44 million in the company; upon completion, it will become BD’s largest medical device manufacturing base in Asia.

● In 2012, BD invested $300 million to launch its wholly-owned manufacturing facility—the Phase II project of Suzhou Becton Dickinson Medical Devices Co., Ltd.—in the Suzhou Industrial Park.

In June 2016, BD’s R&D Center for Greater China was officially completed and inaugurated, while construction of the pre-filled syringe production line for BD Pharmaceutical Systems commenced. This milestone marked BD’s establishment of a comprehensive industrial chain in China, encompassing R&D, manufacturing, marketing, and sales. With the establishment of the new Greater China R&D Center, BD China has formed a “dual-center” R&D structure, with Shanghai serving as the innovation and design hub and Suzhou as the experimental center.

Finally, we observe that foreign IVD companies have been operating in China for over two decades, far longer than many domestic enterprises. The competitive landscape of China’s in vitro diagnostics (IVD) market has become quite stable, with clearly defined industry barriers that are currently difficult to breach. For domestic IVD companies to successfully break through in this competition, opportunities may still exist in more specialized niche segments.