China's $60 Billion Pet Healthcare Market Sees Rise of Domestic Leaders as Foreign Players Lack Edge

Recently, Guotai Junan released a research report titled “The Pet Market’s Trillion-Yuan Blue Ocean: Prioritizing Healthcare, Then Snacks.” The report stated that the domestic pet market size had reached RMB 122 billion in 2016 and is projected to reach RMB 257.1 billion within five years.

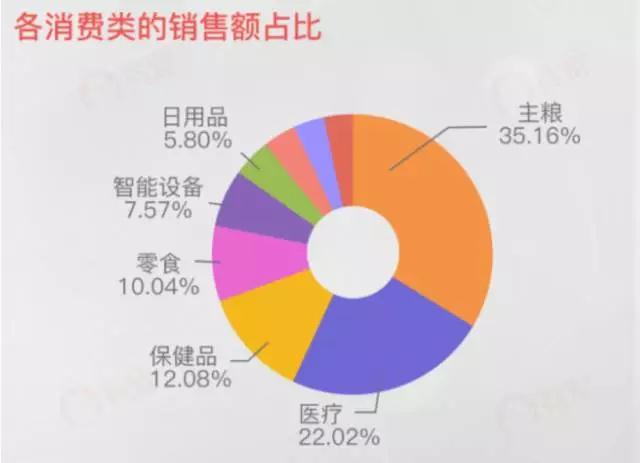

The report indicates that pet healthcare, as the most critical segment of pet services, ranks second in market size within the industry chain.

Pet Healthcare Market to Reach RMB 60 Billion in Five Years; Foreign Firms Hold No Advantage

Driven by factors such as the growth in per capita disposable income of urban residents, population aging, and the rising number of young people living alone, consumer attitudes toward pets have shifted, creating substantial market growth prospects for China’s pet industry. Currently, the Chinese pet market is in a phase of rapid development, with a compound annual growth rate (CAGR) of 43.45% over the past six years.

According to data from the Pet Diagnosis and Treatment Industry Association, in 2016, nearly 8% of households in China’s first- and second-tier cities owned pets, while the national pet-owning household rate was approximately 5%.

In the United States, where the pet market is relatively mature, pet healthcare constitutes the largest segment of the pet industry, accounting for approximately 40%–50% of the market share. According to data from the American Pet Products Association, China’s pet healthcare sector accounts for 22.88% of the pet industry’s segmented market; specifically, the market size of China’s pet healthcare industry was RMB 27.914 billion in 2016, and it is projected to reach RMB 60 billion within five years.

As pet consumption services upgrade, the market share of China’s pet healthcare sector is expected to gradually increase.

According to the conservative estimates in the Goumin.com White Paper, China’s total pet industry consumer market size is projected to reach RMB 132 billion in 2017. The Chinese pet industry is expected to maintain a high average annual growth rate of 30.9% during the period from 2010 to 2020.

Although foreign giants have nearly monopolized the domestic pet staple food market, due to the high barriers to entry in veterinary care, foreign companies lack a first-mover advantage in China. Consequently, the pet healthcare sector is the sub-industry within the pet market most likely to give rise to several leading domestic players.

Compared with the upstream segment of the pet industry, which is characterized by low entry barriers and intense competition, the downstream sector—pet healthcare—offers a more favorable entry point into this niche market. Due to its high technical barriers and status as an essential service, it possesses the scalability needed to integrate both upstream and downstream segments of the industry chain.

Leading Enterprises with Scale and Brand Recognition Poised to Rise

The report suggests that pet healthcare is the most promising sub-sector, with several leading enterprises expected to emerge.

Currently, there are approximately 11,000 animal diagnosis and treatment institutions in China, with about 70% being small-scale clinics. Chain pet hospitals account for less than 10% of the market share, which is significantly lower than the 25% share seen in the United States.

Due to the limited service radius of individual offline stores and the fragmented nature of the market, several leading companies with significant investment value are expected to emerge in the future. The report cites the following reasons:

1) The Chinese pet healthcare market is still in its early stages, with substantial room for future growth. Compared with the large chain giants in the United States, Chinese enterprises are currently smaller in scale, indicating significant market potential and a high likelihood of emerging industry leaders in the future.

2) Veterinary care for pets is an essential, irreplaceable need. It is deeply integrated with offline services such as pet grooming, and also serves as a key offline channel for driving pet food sales.

3) The industry has high entry barriers, with stringent professional and technical requirements for profitability. Enterprises that establish brand advantages early are well-positioned to consolidate the entire pet services market, while also serving as a key sales channel for pet food and supplies.

4) The pet healthcare market lacks a first-mover advantage for foreign companies, placing Chinese enterprises on a nearly level playing field.

5) The industry is currently highly fragmented, with most players operating as sole proprietors lacking economies of scale and brand recognition. Should scaled, branded enterprises emerge, they are likely to rapidly capture market share.

Large-scale veterinary hospitals primarily adopt a chain-store model, leveraging pet healthcare as the entry point to establish a presence across the entire industry value chain.

In the veterinary healthcare industry, large-scale pet hospitals typically operate under a chain model, integrating services such as disease prevention, diagnosis and treatment, wellness care, grooming, and the sale of pet food and supplies.

Although several large-scale chain pet hospitals differ in their geographic distribution, they share a business model that uses high-barrier healthcare services as an entry point to develop an integrated full-industry-chain approach encompassing the sales of pet food, supplies, and health supplements, as well as grooming, boarding, training, and live animal trading. The report suggests that domestic companies can leverage the inelastic demand for pet medical care to drive integration across the industry chain, while simultaneously entering service markets such as pet grooming and retail markets for pet food, supplies, and pharmaceuticals.

With the involvement of industrial capital, the pet industry is accelerating its consolidation. Veterinary hospitals with slightly larger market shares are expanding their operations geographically and in scale, with chain operations beginning to take shape. Representative chain veterinary hospitals include New Ruipeng Group, Ruipai Pet Hospital, Barbie Tang Animal Hospital, Medlinket Animal Hospital, Pet Pet, Aibeier, and Wo Chong Wo Ai.

Veterinary medical institutions generally require comprehensive hardware and medical equipment, as well as adequate operational premises, with high standards for physical infrastructure. Consequently, the predominant business model for veterinary hospitals in China is chain operations. The corporate-owned chain model more readily facilitates standardization and brand development. This also makes capital availability a critical factor in the expansion of veterinary hospitals.

Currently, there is a significant disparity in the scale of direct operations among the top ten companies in China’s pet healthcare market. These companies are primarily located in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen, as well as selected second- and third-tier cities. Among them, Ruipeng Group, the largest chain operator, operates hospitals mainly in these first-tier cities and some second- and third-tier cities. With over 180 pet hospitals nationwide, its business model is predominantly based on directly operated chains.