CBCT: The Pivotal Device Driving Dental Digitization Set to Become the Third-Largest Segment in Global Dental Imaging Market

“The watershed moment in dental digitalization is the emergence and adoption of CBCT devices,” a senior expert who has studied orthodontic systems for many years told VCBeat. Oral imaging is currently undergoing comprehensive digital transformation, with two key devices driving this shift: intraoral scanners and CBCT.

Oral CT equipment is an X-ray imaging system specifically designed for the characteristics of the oral and maxillofacial region. With the aid of CT, dentists have detected and treated various oral diseases and performed surgeries that were previously impossible. It can be said that oral CT equipment is a revolutionary tool in dentistry.

Building upon traditional spiral CT, cone-beam CT (CBCT) features upgraded scanning and data acquisition methods. Its principle involves the X-ray generator performing circular digital radiography (DR) around the subject at a lower radiation dose (typically with a tube current of approximately 10 mA). Subsequently, multiple digital projections (ranging from 180 to 360, depending on the specific product) are acquired around the subject. The data obtained from the overlapping projections are then reconstructed by computer algorithms to generate three-dimensional images.

Approximately two years after the emergence of dynamic flat-panel detectors in 1995, the world’s first cone-beam computed tomography (CBCT) system was introduced. Since then, spiral CT and CBCT have evolved along separate trajectories. The data acquisition principle of CBCT differs from that of traditional fan-beam CT; however, the principles underlying the subsequent computational reconstruction algorithms share certain similarities. As CBCT technology and related reconstruction algorithms become increasingly precise, its advantages over traditional fan-beam CT will continue to widen.

The advent of CBCT devices has transformed the landscape of global dental radiology, making digital dentistry a reality. So, what is the current state of the oral CBCT market? Who are the key players, and what does the competitive landscape look like? VCBeat (WeChat: vcbeat) has conducted a detailed analysis.

Initially, dentists could only study hard tissues using dry skulls, with research on hard and soft tissues conducted separately.

In 1895, Röntgen discovered X-rays, a technology that was rapidly applied in the medical field; specifically in dentistry, this led to the invention of intraoral dental X-ray machines and panoramic radiography units.

In 1931, Broadbent and Hofrath proposed a new cephalometric radiography technique and invented the cephalostat, which ensured consistent head positioning across all radiographs and standardized image size.

This technology ensures the comparability of study subjects before and after treatment, playing a pivotal role in elucidating the anatomical basis of dentofacial deformities, diagnosing and analyzing malocclusion types, and predicting craniofacial growth and development. It also provides a scientific basis for establishing clinical diagnostic and therapeutic standards and formulating treatment plans.

In the 1970s, cephalometric analysis began to evolve from two-dimensional planar measurements toward integrated systems combining three-dimensional spatial analysis with stereophotogrammetry. In the 1990s, the first dental-specific cone-beam computed tomography (CBCT) scanner, the NewTom 9000, was introduced, providing precise and clear three-dimensional facial images and enabling clinicians to obtain intuitive 3D surface representations of patients' faces.

The device entered the European market in 1996 and the U.S. market in 2001. In 2013, at the Festival della Scienza in Italy, Attilio Tacconi, Piero Mozzo, Daniele Godi, and Giordano Ronca received the Cone Beam CT Invention Award, honoring the inventors of this revolutionary technology that has transformed panoramic dental radiology worldwide.

Axial Images Obtained from the First Cone-Beam 3D Scan

Due to the high radiation dose, high procurement cost, and lack of dedicated dental post-processing software associated with spiral CT, dental medical institutions primarily procure CBCT systems. Spiral CT is used only in large public dental institutions when there is a need for maxillofacial surgical diagnosis and treatment.

For instance, in orthodontic surgery, by integrating 3D reconstruction imaging technology with orthodontic parameters and application software, CBCT equipment can generate three-dimensional images of the subject. This approach overcomes the limitations of cephalometric X-ray systems, such as unclear visualization of facial soft tissues, susceptibility to distortion in orthodontic parameter localization, and insufficient understanding of the patient’s facial three-dimensional spatial anatomy by clinicians. Consequently, it facilitates more effective formulation of treatment plans and analysis of treatment outcomes.

It can be said that without the application of CBCT in dentistry, digital orthodontics and dental implantology would not have been able to achieve their current rapid adoption.

A dental medical device manufacturer revealed to reporters: “The emergence of CBCT represents the evolution of medical imaging from two-dimensional to three-dimensional. CBCT has elevated scanning resolution to levels unattainable by spiral CT, and even Micro-CT has emerged. Meanwhile, the radiation dose associated with CBCT has been reduced to a new low.”

The primary difference between CBCT and conventional CT lies in the scanning method: CBCT employs a three-dimensional cone-beam X-ray scan to acquire nearly 600 distinct images, which are then reconstructed directly into a three-dimensional image with reduced metal artifacts. In contrast, conventional CT uses a two-dimensional fan-beam scan, generating two-dimensional image data after reconstruction, which is associated with more pronounced artifacts. CBCT is widely utilized in fields such as oral and maxillofacial surgery, endodontics, orthodontic treatment, and dental implantology.

Specifically, CBCT delivers a low effective dose, with an exposure dose of 19.0–464.0 μSv per scan, equivalent to approximately 1–30 panoramic radiographs and about 1/56 to 1/5 of the dose from spiral CT. Due to the short exposure time and ease of patient positioning, image degradation caused by patient movement is less likely. With high resolution, minimal metal artifacts, and clear images, CBCT offers superior capability in resolving fine anatomical structures, thereby facilitating physician diagnosis.

Furthermore, for physicians, the associated software operations are relatively straightforward, and 3D reconstruction is both rapid and comprehensive; after training, even general technicians can operate the system. For patients, the examination costs are correspondingly lower, making it more acceptable to them.

CBCT hardware currently meets clinical requirements in general, although there remains significant room for improvement.

An attending orthodontist in the industry revealed to reporters, “When integrated with orthodontic software such as 3Shape and ExoCAD, CBCT enables clinicians to pay closer attention to the thickness and height of the labial and lingual bone plates, as well as functional remodeling during orthodontic treatment. This is crucial for achieving high-quality orthodontic outcomes, ensuring long-term post-treatment stability, and maintaining periodontal health. Additionally, orthodontists are now placing particular emphasis on the temporomandibular joint (TMJ), where CBCT plays a significant role in assessing condylar morphology and joint space.”

New software functionalities have been realized with the support of further hardware advancements. For instance, the emergence of ultra-low-dose cone-beam computed tomography (CBCT) enables orthodontic software to acquire patients’ actual dental information and derive occlusal data from CBCT scans. This progress allows orthodontists to obtain more precise data, thereby delivering more professional orthodontic services to patients more quickly and effectively.

In dental implantology, prior to surgery, it is essential to assess the patient’s jawbone quality and volume, as well as to identify the locations of critical anatomical structures such as the inferior alveolar nerve canal and the maxillary sinuses. Based on this evaluation, the feasibility of the implant procedure is determined, along with key parameters including the type, dimensions, insertion site, surgical approach, and depth of the dental implants.

With the assistance of implant planning software such as Simplant, Nobel Clinician, and 3Shape, CBCT devices can facilitate the design of implant surgeries and the fabrication of surgical guides. They enable precise control over implant position, angulation, length, and diameter, thereby ensuring the success of both the surgical procedure and subsequent prosthetic restoration. Consequently, minimally invasive implant techniques have recently gained significant popularity. Furthermore, the sensitivity, speed, and accuracy of CBCT have been validated in the analysis of impacted teeth, as well as in the diagnosis of endodontic-periodontal diseases and temporomandibular joint disorders.

Following immediate intraoral scanning, dentists integrate CBCT data to design digital implant surgical guides, enabling efficient and convenient preoperative planning. However, CBCT devices have certain limitations, such as the lack of a standardized scaling system for reconstructing dental dimensions and the inability to assess bone density.

Cone-beam computed tomography (CBCT) commonly used in dentistry continues to evolve toward higher spatial resolution, improved soft-tissue resolution, and lower radiation dose.

“Panoramic X-ray machines have very limited functionality. Nowadays, virtually all orthodontic patients at the dental hospital where I work routinely undergo CBCT scans,” said the attending orthodontist.

CBCT image detectors determine imaging quality. Currently available types include amorphous silicon flat-panel detectors, CCDs coupled with image intensifiers, CMOS flat-panel detectors, and CsI flat-panel detectors, with amorphous silicon flat-panel detectors being relatively superior. Parameters such as exposure field size, exposure time, image reconstruction time, and voxel size vary. At present, flat-panel detector types remain the mainstream.

Based on the field of view, large-field-of-view CT detectors have dimensions greater than 130 mm × 150 mm; medium-field-of-view detectors have dimensions greater than 70 mm × 80 mm but less than 130 mm × 150 mm; and small-field-of-view detectors have dimensions less than 70 mm × 80 mm.

In short, both excessively long and excessively short scan times are undesirable, whereas shorter reconstruction times are preferable. A smaller spatial resolution value indicates higher image clarity but poses greater challenges for storage and transmission. Additionally, in terms of footprint and design, vertical and seated systems require less space than horizontal systems. The accompanying software is also crucial, as it significantly influences the user experience to a certain extent.

The X-ray tube is also critical. It is mainly categorized into pulsed and continuous exposure types. To some extent, the pulsed type is superior to the latter; however, the latter features a highly effective cooling system, making it suitable for clinics with high usage frequency. Rotating anode X-ray tubes are superior to fixed anode tubes, with a significant price difference between them. Currently, the focal spot size of mainstream CBCT systems ranges from 0.3 mm to 0.7 mm; a smaller focal spot yields higher image clarity. The rotation angle also affects image clarity.

From the perspective of user needs alone, small clinics may consider digital panoramic X-ray machines. For practices primarily focused on dental implants or endodontics, small- to medium-field-of-view CBCT is sufficient. If orthodontic and orthognathic surgical applications are required, a large-field-of-view CBCT should be selected; most specialized comprehensive stomatological hospitals and large tertiary Grade-A general public hospitals are equipped with large-field-of-view CBCT systems.

Finally, it is important to note that CBCT is an expensive and sophisticated instrument; reliable after-sales service is essential to ensure its proper operation, and the presence of a registration certificate must also be taken into consideration.

Regarding CBCT, the hardware technology is already quite mature. In an interview, a senior dental professional stated, “There is still room for improvement in hardware, particularly in terms of scanning speed per rotation, resolution, image clarity, and low-dose performance. Imaging of hard tissues is no longer a significant issue; the more challenging aspect lies in soft tissue visualization to better support clinical diagnosis. Furthermore, supporting software such as surgical guide design and orthodontic planning tools are continuously being iterated, with substantial opportunities remaining for further development and enhancement.”

As for the supporting software, 3D post-processing software is mature and its functions fully meet clinical needs. Although the core image reconstruction algorithm software, representing the current mainstream technology, basically meets clinical requirements, it still requires further improvement in reducing radiation dose, removing metal artifacts, enabling ultra-fast scanning, and expanding the effective field of view.

An expert in digital dental software also revealed to reporters, “Open systems are technically very easy to implement; they simply require the use of universal data formats, namely DICOM and STL. Openness is the trend. The current prevalence of closed systems is due to insufficient competitive pressure among manufacturers, who can still generate profits through consumables.”

However, commonly bundled consumables such as film and developer solutions are low-priced, generic products. Coupled with the ongoing transition to digitalization, it is increasingly difficult to generate profits from the sale of these consumables.

Previously, closed systems operated in a market with limited competition. To maximize profits, manufacturers not only generated revenue from equipment sales but also charged fees based on the number of scans performed. They even secured additional income through exclusive supply agreements for materials used in subsequent 3D printing integration.

He stated that closed and open systems are relative concepts. During the development of a technology or product, it will inevitably undergo a cyclical process alternating between closed and open phases. A closed approach fosters focus and depth, while an open approach facilitates broader application and widespread adoption.

This depends on the business model chosen by the manufacturer. If selling equipment directly, an open system with a one-time fee can be adopted; if selling services or even engaging in the sharing economy, a closed system with per-scan charges may be used.

Open systems require the establishment of interface standards at the hardware level and data standards at the software level. To some extent, cloud computing and big data technologies are more conducive to building open systems.

Closed systems can theoretically provide more stable product quality. However, judging from current market developments, the advantages of closed systems are gradually diminishing. The superiority of open systems is manifested in lower prices, better compatibility, and more upgrade options.

With industry development, expansion of market scale, and an increasing number of suppliers, the foreseeable future will likely see the emergence of globally unified industry standards, similar to those in the home appliance and telecommunications sectors. This will help reduce R&D costs, minimize unnecessary duplication and waste across various stages, accelerate the deployment of new technologies, lower production costs for new products, and avoid waste caused by equipment incompatibility.

Panoramic X-ray machines, CT scanners, and CBCT systems coexist in the market; what is their actual level of product acceptance? A study by the Research Department of Guotai Junan Securities indicates that CBCT currently accounts for a small share, representing less than 5% of the combined total in both public and private institutions. At present, most better-equipped public hospitals invariably use CBCT devices, typically procured through centralized bidding processes, and rarely employ spiral CT scanners.

In the future, it is unlikely that spiral CT will be used in teaching, diagnosis, or clinical practice, as spiral CT scanners are large-scale devices requiring operation by specialized personnel. Moreover, they offer low resolution for soft tissues, which constitute the main components of the oral cavity, and the accompanying dental diagnostic software still requires improvement. Given that CBCT holds significant advantages in the dental market, why is its current penetration rate still low?

First, not all private clinics will purchase CBCT. Small dental clinics consider the upfront investment costs; if they cannot recoup their costs within 1–3 years, their willingness to buy is very low. Dentists who have already purchased panoramic X-ray machines are unlikely to replace them with dental CBCT systems.

Previously, due to the high cost of panoramic X-ray machines and CT scanners, small and medium-sized clinics struggled to equip themselves with these devices. As the dental market is predominantly composed of private small and medium-sized clinics, the adoption volume of dental CT scanners remained low. However, domestically produced products have now driven prices down by half or even to one-third of their original levels.

Panoramic radiography produces two-dimensional images with limited clarity. Most dentists lack expertise in interpreting panoramic radiographs, and even the most distinguished authorities in radiology cannot detect all pathologies using this modality.

However, CBCT 3D imaging enables precise diagnosis and treatment, offering significant advantages. Therefore, dental CBCT represents a future development trend, with its penetration rate expected to continue rising.

In terms of pricing, large-field-of-view CBCT systems range from 1.5 million to 3.5 million yuan, medium-field-of-view models from 600,000 to 1.5 million yuan, and small-field-of-view units from 400,000 to 600,000 yuan.

A dental clinic operator revealed to reporters: “CBCT is an essential adjunct to implantology services; any practice offering dental implants must be equipped with CBCT. Introducing new services will create additional revenue streams for clinics and hospitals, so adoption is certainly expected. However, decisions still depend on brand reputation, quality, cost-effectiveness, and after-sales support. In addition, there is market demand for accompanying software solutions, which are currently either underdeveloped or prohibitively expensive if well-executed. Software systems will ultimately need to be open, and a robust platform is sure to emerge.”

Moreover, digital equipment and technologies serve as marketing gimmicks for clinics and hospitals, demonstrating and validating their technical capabilities; consequently, stakeholders are willing to invest heavily in this area.

A representative from Byondent stated, “The upgrade cycle for CBCT systems depends on technological breakthroughs in key components such as X-ray detectors, averaging around five years, while supporting software is updated more frequently, typically every two years or so. Cost remains one of the primary barriers preventing small clinics from purchasing digital equipment and software.”

The official told reporters that doctors, clinics, and hospitals have now widely and fully accepted CBCT and its accompanying software. The three-dimensional perspective and tissue density analysis capabilities provided by CBCT enable physicians to obtain diagnostic results more conveniently and with greater confidence. The key challenges to be addressed in promoting adoption are, first, the cost of purchase, and second, training in software operation and imaging-based diagnostic techniques.

The decline in costs will undoubtedly significantly boost the demand for digital equipment and software among small clinics. Meanwhile, the technological promotion of such digital tools is also a critical influencing factor; accessibility and ease of use are equally important.

A medical device manufacturer shared its perspective on the CBCT industry with reporters: “It has been only a little over a decade since CBCT equipment was first introduced to the market. The current wave of product iterations is driven primarily by limitations in field of view (FOV). In the future, we may see product updates necessitated by certain brands’ insufficient consideration of upgradability during the design phase. The cycle of such updates could depend on the intensity with which major CBCT manufacturers promote new technologies, as well as the rigor of regulatory oversight regarding issues that have not yet been identified.”

Reporters learned from multiple interviewees that the most commonly cited issues are the current lack of high-quality training and after-sales support, as well as uncertainties regarding how to handle data generated through digitalization, where such data should be sent, and who can provide supporting services for digital transformation.

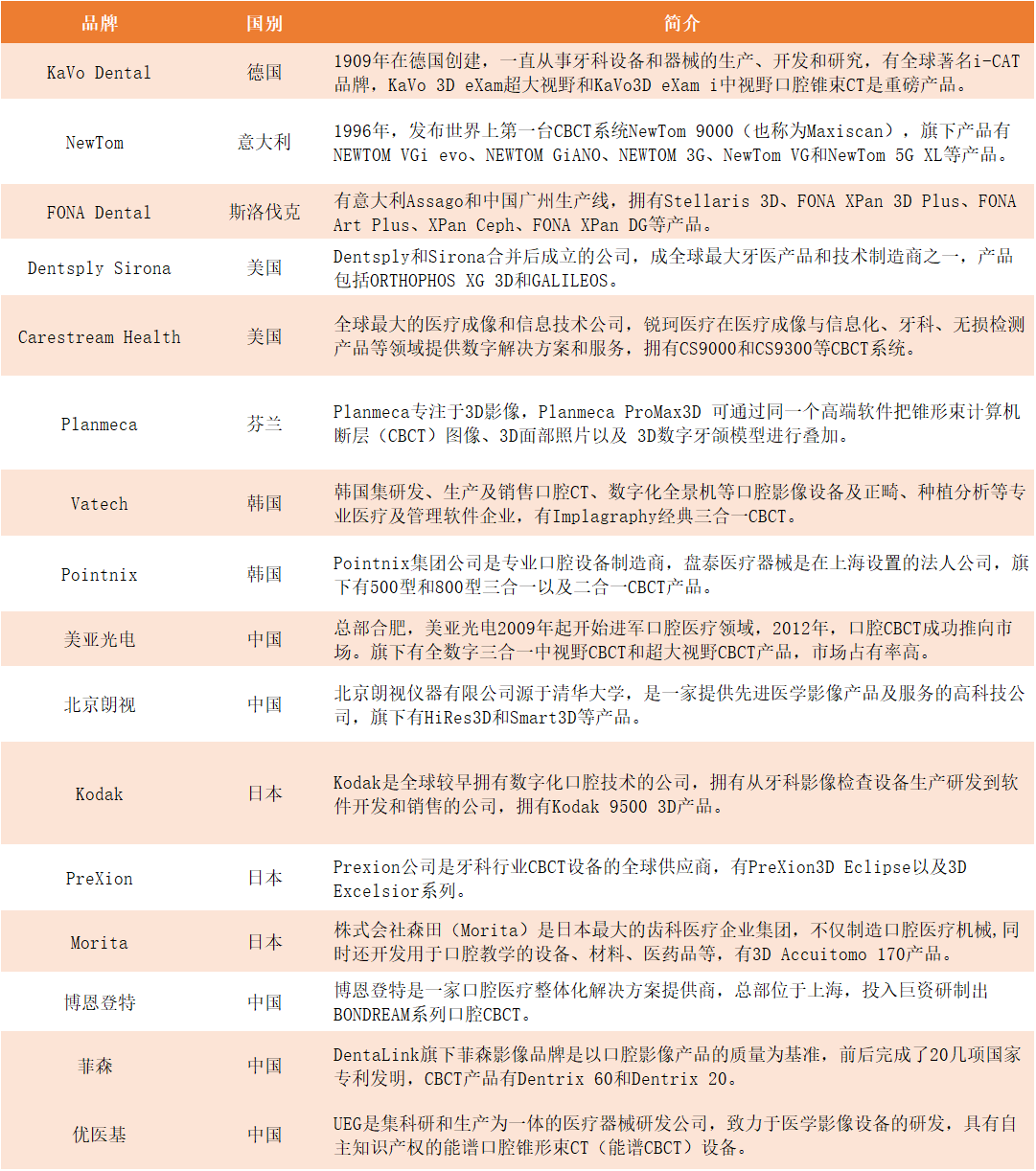

According to research by the Research Department of Guotai Junan Securities, the estimated sales volume of CBCT units across the entire industry in 2016 was approximately 2,000. An investor who requested anonymity disclosed to reporters that the installed base of dental CT scanners of various specifications in the domestic market exceeded 23,000 units, with around 4,000 CBCT units in the overall market. In addition to foreign brands such as Sirona, KaVo, Morita, Planmeca, and Newtom, Meyer Optoelectronic, LargeV, Shenzhen Fussen, and Byntec are all Chinese manufacturers possessing independent intellectual property rights for CT technology.

Currently, three companies in China—Meyer Optoelectronic, Beijing LargeV, and Shenzhen Fussen—have obtained registration certificates and are commercially selling their products. The technologies of these three enterprises are largely derived from extensions of optoelectronic and image-processing product technologies. Meyer Optoelectronic rapidly captured market share by introducing financial leasing and equipment placement models. Domestic brands hold significant price advantages, making them highly attractive to small clinics and hospitals.

Overview of CBCT Companies in the Market

Since 2009, Meyer Optoelectronic has been expanding into the field of dental healthcare. In 2012, it successfully launched its dental cone-beam computed tomography (CBCT) system to the market, thereby becoming the first enterprise in China with the capability to develop and manufacture medical CBCT systems, filling a domestic gap in this field.

In addition to its fully digital all-in-one mid-field-of-view CBCT, Meyer Optoelectronic launched an ultra-large field-of-view CBCT product in September 2014 during the CDS International Dental Show in Shanghai. Equipped with a state-of-the-art ultra-large flat-panel detector, this device captures full-head 3D images in a single scan, with an effective field of view measuring 23×19 cm, and has obtained registration certification from the China Food and Drug Administration (CFDA).

In 2016, Meyer Optoelectronic sold 600 CBCT units, representing a year-on-year increase of nearly threefold, which clearly indicates robust market growth. According to its semi-annual report for the first half of 2017, dental X-ray CT diagnostic devices accounted for 23.82% of total revenue, with a gross profit margin reaching 56.97%. The gross margins for this product category remain relatively high, generally stabilizing between 50% and 60%.

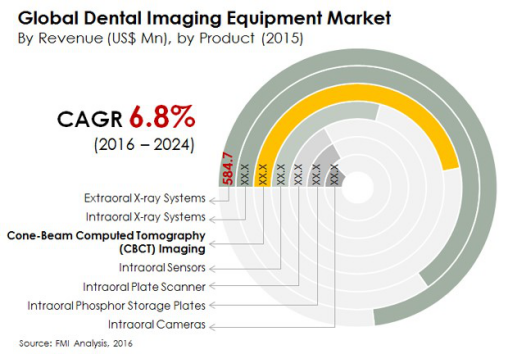

What about the international market? According to data from FMI Analysis, the global market size for dental imaging equipment was estimated at $208 million in 2015, with cone-beam computed tomography (CBCT) accounting for 18% of this market. Flat-panel detectors comprised 88.3% of the dental CBCT market.

In 2015, intraoral X-ray systems accounted for the largest share of the global market, followed by extraoral X-ray systems and cone-beam computed tomography (CBCT). During the period from 2016 to 2024, with an estimated compound annual growth rate (CAGR) of 7.5%, CBCT is projected to become the third-largest product category in the global dental imaging equipment market.

According to a research report by China Securities Co., Ltd., Taiwan, with a population of 23.5 million, has more than 6,000 private clinics. In contrast, China’s urban population of 790 million would require 205,000 such clinics, indicating a shortfall of at least 120,000 private clinics. Assuming a penetration rate of 30%, this would translate to a demand for 36,000 dental CT scanners, suggesting significant market growth potential and a future market valued at tens of billions of yuan.

Compared with other departments, dentistry is the industry most easily privatized and replicated across different regions. Currently, there are about 80,000 private dental clinics in China, which constitute the main growth point for CBCT.

Although the competitive barriers in the CBCT sector are relatively high, making significant short-term shifts in the market landscape unlikely, the trends toward dental digitalization and system openness are largely irreversible. Consequently, medical device manufacturers must transition from being mere “equipment manufacturers” to becoming “equipment solution providers.”

Additionally, we are optimistic about the domestic substitution of panoramic X-ray machines and dental CT scanners. Against the backdrop of an aging population and consumption upgrades in China, coupled with the current low penetration rates of dental implants and orthodontics, the CBCT market is poised to maintain rapid growth.