China Leads in Medical AI Applications Across Multiple Segments, Yet Lags in Talent and Data Standardization

In June 2014, the UK-based artificial intelligence company BenevolentAI announced that it would sell two Alzheimer’s disease drug candidates under development to a U.S. pharmaceutical company for $800 million;

In July 2017, IBM publicly released data showing that IBM Watson Oncology had been deployed in more than 50 hospitals worldwide, served nearly 40,000 patients and physicians in the first half of 2017, and covered seven types of cancer.

In September 2017, Yitu Healthcare stated that Zhejiang Provincial People's Hospital, as one of its first partner hospitals, had utilized the AI system to assist physicians in reviewing imaging data for 17,000 patients since its launch, with an adoption rate of 90%.

Around the world, medical artificial intelligence has evolved beyond a mere innovative concept; various products developed based on AI technologies are now tangibly serving doctors, patients, enterprises, and healthcare institutions.

Recognizing the immense potential of artificial intelligence (AI), countries and regions around the world have successively introduced policies and invested capital to accelerate their strategic deployment. This has led some to jokingly refer to the quiet onset of an AI “arms race.” Among all global regions, the United States, China, and Europe stand out as the three most prominent players in medical AI.

“In literature, there is no first place; in martial arts, there is no second.” VCBeat (WeChat ID: vcbeat) reviews the current state of medical AI development in these three regions from the perspective of clinical applications to determine who is leading the field of medical artificial intelligence.

Not long ago, CSRankings.org released global, Asian, U.S., and European university rankings based on the number of papers published by institutions in top-tier computer science conferences. Among the top 25 universities worldwide, Tsinghua University ranked fourth, The Hong Kong University of Science and Technology ranked tenth, and Carnegie Mellon University (CMU) topped the list. The University of Edinburgh and University College London from Europe made it onto the list, while 18 U.S. universities were included.

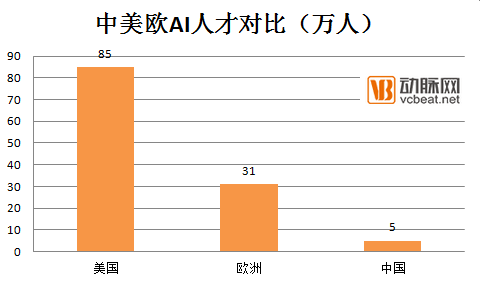

The United States holds an insurmountable advantage in talent. The recently viral “LinkedIn Talent Report” also pointed out that the U.S. has 850,000 AI practitioners, Europe has a combined total of over 310,000, while China has just over 50,000.

U.S. researchers place greater emphasis on basic research, supported by a robust talent development system for artificial intelligence, which confers significant advantages to research-oriented professionals. Specifically, the United States holds distinct advantages in key areas such as foundational discipline construction, patent and publication output, high-end R&D talent, venture capital investment, and leading enterprises.

In the era of artificial intelligence, Europe’s development is rarely mentioned; however, the continent boasts 310,000 AI practitioners, six times the number in China. Notable institutions include the University of Edinburgh, University College London, the University of Hertfordshire, the University of Montreal, and the University of Oxford, as well as Sweden’s Dalle Molle Institute for Artificial Intelligence, EPFL (École Polytechnique Fédérale de Lausanne), and the University of Basel.

Data Source: McKinsey

In recent years, China has maintained rapid growth in the number of academic papers and patents in the field of artificial intelligence, securing its position among the top tier globally. In comparison, China needs to sustain its investment in R&D expenditure and the size of its research workforce. Although its talent cultivation still lags behind that of Europe and the United States, many overseas-educated Chinese professionals are choosing to return home to start businesses or seek employment, driven by domestic policy support and data advantages. This trend has, to some extent, helped mitigate the shortage of skilled personnel.

The primary data source available for artificial intelligence research and development is electronic medical records (EMRs). With the advancement of computer technology, traditional paper-based medical record-keeping has been replaced by EMRs, which have demonstrated practical application effects and utility in hospital operations. In terms of health data, China’s foundational data volume far surpasses that of Europe and the United States, particularly due to the vast amount of medical and health data derived from its large population. However, this massive dataset lacks a unified standard and an ecosystem for cross-platform sharing; most data remain isolated in silos, resulting in low utilization rates and limited practical value.

The Development of U.S. Healthcare Data Has Undergone Three Stages:

Phase of Unrestricted Development (1991–2003)

Phase of Unregulated Development (1991–2003): As early as 1991, the U.S. Institute of Medicine (IOM) released a research report on electronic medical records. Subsequently, the U.S. government, academia, and the medical community successively issued policies, reports, and technical standards to promote the development of electronic medical records.

Formation of National Policies and Government-Driven Phase (2004–2008)

![2{I2DO]4ZZOO8XNHNCU)5Z4.png](https://cdn.vcbeat.top/upload/image/10/09/14/10/1505383857359565.png)

Leveraging Economic Incentives to Drive Growth (2009–Present)

To facilitate the implementation of the Health Information Technology for Economic and Clinical Health (HITECH) Act, President Obama mandated that physicians adopting electronic health record (EHR) systems in their practices by 2015 would receive Medicare incentives ranging from $44,000 to $64,000. It was precisely through the implementation and adoption of these EHR policies that the United States accumulated vast amounts of medical data, laying the foundation for the third wave of artificial intelligence development.

The development of electronic medical records (EMR) in mainland China started somewhat later. Relatively more developed regions such as Hong Kong and Taiwan embraced EMR more rapidly. In 2005, Hong Kong began fully implementing the world’s largest EMR system across more than 40 public hospitals within the territory. Although mainland China lagged behind in the early stages of EMR development, continuous domestic efforts and progress have enabled hospitals to gradually establish information systems. Starting in 2010 and in the subsequent years, multiple regulations and notices concerning EMR were issued, albeit at a low frequency.

For instance, on February 22 of this year, the National Health and Family Planning Commission promulgated the new “Administrative Specifications for the Application of Electronic Medical Records (Trial).” Seven years have passed since the issuance of the “Basic Specifications for Electronic Medical Records (Trial)” in 2010.

The UK’s National Health Service (NHS) has long shouldered the critical responsibility of providing publicly funded healthcare to all British citizens. Under the impetus of Jeremy Hunt, the UK Secretary of State for Health, all primary care and hospital services within the NHS were required to implement electronic health records by 2020; failure to do so would result in the loss of authorization to treat patients.

Overall, legislation governing medical data in Europe and the United States is largely comprehensive, with a particular emphasis on privacy protection. The collaboration between DeepMind and the NHS was once stalled due to a “privacy scandal.” Meanwhile, data costs in these regions are significantly higher; IBM once planned to acquire the healthcare data company Truven for $2.6 billion.。

Compared with Europe and the United States, although China’s medical data is vast in volume, there are no detailed legal provisions governing the ownership, usage rights, storage rights, and trading rights of such data. Current policies merely require the entities managing these data—namely hospitals and government agencies—to safeguard privacy and permit the use of this data for scientific research purposes.

The "Development Plan for the New Generation of Artificial Intelligence" points out that the state will establish preliminary legal regulations to standardize various rights related to medical data by 2025. Prior to this, domestic artificial intelligence companies can leverage this period of legal vacuum to train their models using medical data.

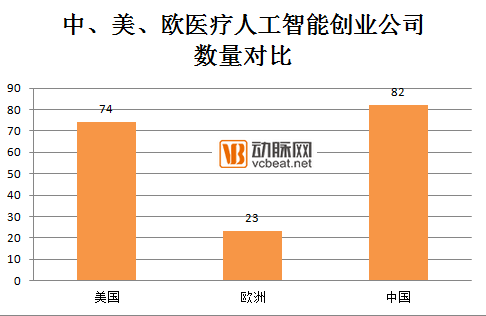

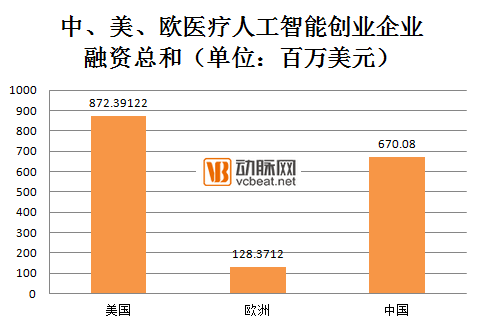

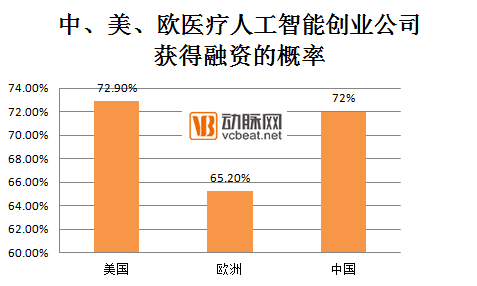

After several years of development, the total number of healthcare AI startups in China, the United States, and Europe has approached 200, with 82 in China, 74 in the United States, and 23 in Europe. The financing rates for healthcare AI companies in these three regions reached 72%, 72.9%, and 65.2%, respectively, with total funding amounts of $670 million, $872 million, and $128 million, respectively.

Among these, the largest financing round in China was iCarbonX’s RMB 1 billion Series A funding. In the United States, the largest single financing round went to Flatiron Health, a company specializing in multi-source heterogeneous data mining, which raised $175 million in a single round in 2016. In Europe, the largest financing round was secured by BenevolentAI, a company leveraging AI for drug discovery and development, with its largest single funding amounting to $140.6 million.

The investment success rates in the United States and China are remarkably close, with an average rate of 72.90% for U.S. medical AI companies compared to 72% in China. Europe’s rate is relatively lower, at just 65.2%. Additionally, according to VCBeat, some companies maintain a low profile; even after securing funding, they focus on development without public announcements, suggesting that China’s actual investment success rate is likely higher. The data indicates that capital markets currently hold an optimistic outlook on medical AI projects, as investors are eager not to miss this emerging opportunity.

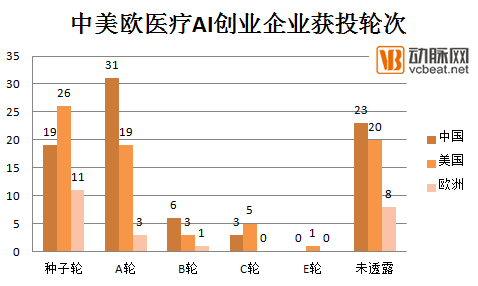

Most healthcare startups in China, the United States, and Europe are still in their early stages. Only one U.S. company, Pathway Genomics, has secured Series E funding, while all others remain at Series C or earlier. Notably, there are 12 more Chinese companies at Series A than their U.S. counterparts, whereas the U.S. has seven more companies at the seed stage than China. European companies lag behind both China and the U.S. across all funding rounds. These data suggest that Chinese medical AI companies find it easier to secure subsequent financing compared to those in Europe and the U.S.

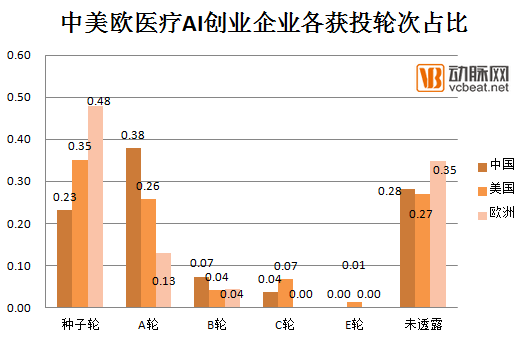

If the number of companies only indicates scale, then the proportion of firms at each funding round can reflect the development status of medical artificial intelligence (AI) in China, the United States, and Europe. Seed-stage companies account for 23% of all medical AI companies in China, compared to 35% in the United States and 48% in Europe, indicating that most European companies are still in the early stages of development.

In China, 38% of all medical AI companies are at the Series A stage, compared with 26% in the United States and 13% in Europe. This indicates that the majority of Chinese companies have survived the seed stage, gained investor recognition, and entered the next phase of development. The proportion of companies that have reached Series B and Series C remains in the single digits, suggesting that AI companies worldwide are still in the early stages of development and remain some distance from an initial public offering (IPO).

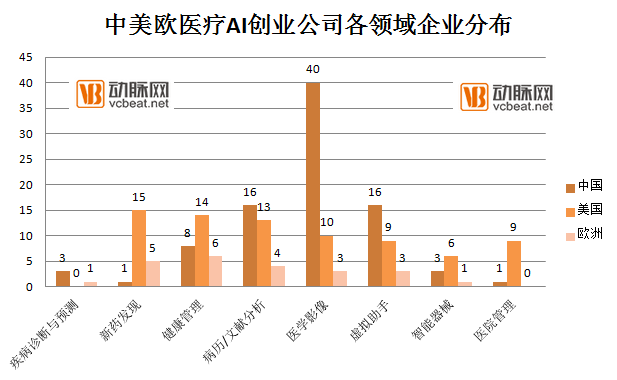

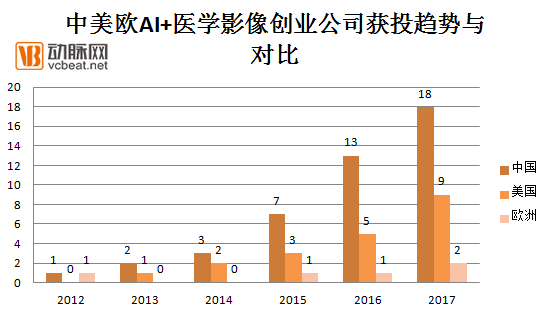

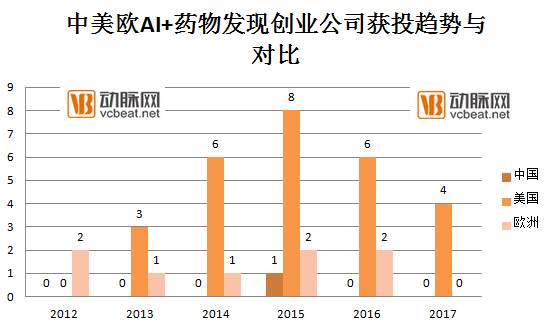

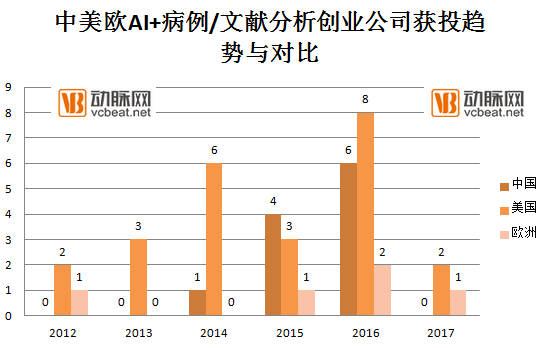

In addition to its applications in familiar areas such as medical imaging, artificial intelligence can also be utilized in drug discovery, health management, hospital administration, smart medical devices, disease diagnosis and prediction, medical record/literature analysis, and virtual assistants. Within these fields,It is intuitively evident that China holds a distinct advantage in the field of medical imaging; however, in drug discovery, Europe and the United States remain far ahead of China.。

In the field of artificial intelligence plus medical imaging, China holds an absolute advantage in terms of the number of enterprises, their scale, and their development progress. A cohort of outstanding companies has emerged; for instance, Yitu Technology raised RMB 380 million in its Series C financing round, with nearly all funds allocated to the healthcare sector. As one of the first partner hospitals of Yitu Medical, Zhejiang Provincial People's Hospital has seen its AI system assist physicians in interpreting images for 17,000 patients since deployment, achieving a report adoption rate of 90%.

Infervision Founder and CEO Chen Kuan delivered a speech at the GTC AI Summit in Silicon Valley as the sole representative of Chinese medical AI companies invited to the event, garnering coverage from Forbes and other major international media outlets.

Moreover, according to Chen Kuan, Infervision’s Japan office has been officially established in Chiyoda Ward, the political and economic core of Tokyo and a key hub for the medical imaging market in the Asia-Pacific region. The company has also begun expanding into the U.S. market, with its products undergoing clinical trials at hospitals such as the University of Chicago Medical Center and Massachusetts General Hospital. Chinese products are beginning to make their mark on the global stage.

Companies operating at the intersection of artificial intelligence and medical imaging are not only numerous and large in scale but also cover a wide range of application areas, with in-depth research conducted in radiological imaging, diabetic retinopathy fundus images, thyroid imaging, and cervical cancer pathological images.

There are few European companies combining artificial intelligence with medical imaging; well-known examples include France’s Keen Eye Technologies and Germany’s FetView. There are also several U.S. companies in the AI-powered medical imaging space, such as Bay Labs, Enlitic, and Eyenuk.

The primary reason lies in the substantial gap between the supply and demand for medical imaging services in China. The annual growth rate of medical imaging procedures in China is 30%, whereas the number of radiologists increases by only 4.15% per year. According to media reports, there are currently just over 10,000 registered pathologists in China; based on the number of hospital beds, this indicates a shortfall of 60,000 to 80,000 pathologists.

In contrast, medical resources in Europe and the United States are relatively abundant. According to a healthcare professional who has lived in the U.S. for an extended period, the cancer screening system in the United States is already well-established. Additionally, although hospital efficiency is low, once patients secure appointments, they have ample time to communicate with their physicians, who also have sufficient time to review imaging studies. Consequently, there is not an urgent demand for AI-assisted image interpretation.

In the field of AI-driven drug discovery, China lags far behind, with only XtalPi utilizing artificial intelligence technology in drug polymorph research.

The UK’s BenevolentAI is the most prominent company in this field. From the fourth quarter of 2013 to the third quarter of 2015, BenevolentAI completed four rounds of financing, totaling £87.72 million (approximately $100 million), and reached a valuation of $1.781 billion. In terms of funding raised, BenevolentAI has become Europe’s most valuable artificial intelligence startup and ranks among the top five globally. In January 2017, it was named to CB Insights’ “Top 100 Artificial Intelligence Companies Worldwide.”

Although the United States has not produced a “unicorn” similar to BenevolentAI, its overall strength surpasses that of the United Kingdom. There are 15 such companies in total, with Atomwise, Insilico Medicine, Numerate, and Lam Therapeutics standing out as leaders in the field of AI-driven new drug development.

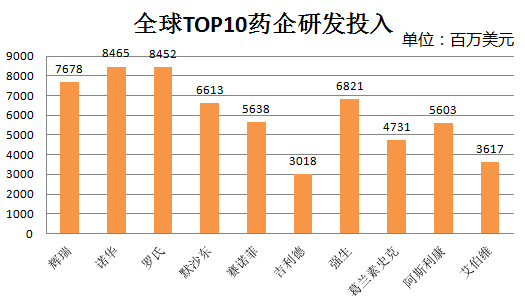

This situation is primarily attributable to differences in the environments and levels of investment in drug research and development (R&D) across countries; for instance, none of the top 10 global companies with the highest drug R&D output are Chinese.

Data sourced from the internet

In the field of AI-powered medical record text analysis, although China has 16 companies, the United States has 13, and Europe has 4, U.S. firms have secured better funding outcomes than their Chinese and European counterparts. This advantage is primarily attributable to the U.S. government’s emphasis on electronic health records (EHRs) and its substantial financial investments in this area. Some companies have even secured funding annually; for instance, GNS Healthcare raised tens of millions of dollars in financing for four consecutive years from 2012 to 2015.

As demand for structured electronic medical records grows in China and related laws and policies are progressively refined, Chinese companies are poised to reap the benefits of this emerging opportunity.

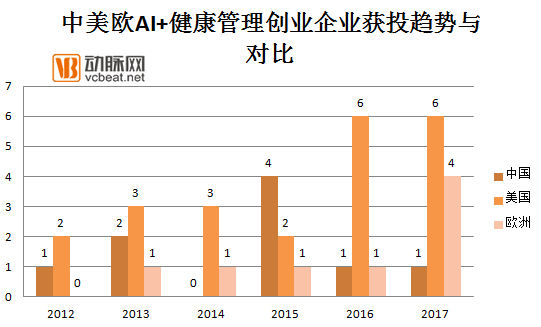

In the field of AI-powered health management, the United States is at the forefront, with 14 startups in this sector, compared to 8 in China and 6 in Europe. Most financing rounds for such U.S. startups occurred in 2015, whereas in China and Europe, funding activities have grown year by year, peaking in 2016 and 2017.

In this field, four out of five UK companies focus on mental health management. For instance, the most prominent among them, Biobeats, centers its approach on collecting various health-related data and leveraging artificial intelligence algorithms to transform these data into content, thereby creating “Adaptive Media” that provides users with stress therapy and healthy lifestyle solutions.

The coverage of companies in the United States and China is more extensive, encompassing chronic disease management, maternal and child health, and mental health management. Chinese companies demonstrate a higher level of focus on chronic and specialized disease management. Chinese companies include YueTang, YiSuifang, and Jinglun Century. U.S. companies include HealthReveal, Ovia Health, and Ginger.io.

Through comparison, we find that in the development of medical AI, China lags significantly behind Europe and the United States only in new drug discovery. In other areas, however, we are not inferior at all—in fact, we have surpassed them by a considerable margin. Nevertheless, it is evident that China needs to increase investment in talent reserves and data standardization.

Cultivating AI Talent with Integrated Medical and Engineering Expertise

VCBeat noted in its article, “China’s AI Talent Landscape: 15 Universities Are Poised to Produce Over 2,000 Master’s and Doctoral Graduates in the Next 3–5 Years, with One-Tenth Entering the Healthcare Sector,” that among a list of 47 CTOs and chief scientists at AI healthcare companies, excluding 14 individuals whose specialties were unclear, only 21% had backgrounds in medicine-related fields, while 52% specialized in artificial intelligence.

Medicine is a rigorous science. For entrepreneurs in medical artificial intelligence to integrate their products into clinical workflows, they must possess a certain medical background to better understand physicians’ needs. Therefore, cultivating interdisciplinary talent at the intersection of medicine and engineering contributes to the healthy development of companies.

Establishing a Sound Medical Data Ecosystem

Standardized data is a key factor in training AI systems, attracting talent, and accelerating innovation. This is also the foundation for China’s leadership in global medical AI. To build a more robust data ecosystem, China can establish and implement data standards and open up public data for individual research and development.

Standardization is a critical prerequisite for widespread data sharing and interoperability within systems, enhancing the value of IoT and AI technologies. Given the vast volume of data with untapped potential across China, the country is uniquely positioned to take the lead in ensuring the adoption of Chinese-language data standards.

For the healthcare sector, a unique industry, the government can urge existing regulatory bodies to establish necessary rules. While promoting open data, attention must be paid to privacy protection; meanwhile, regulation should appropriately tolerate non-malicious errors arising from innovation.

To enhance the diversity of available data in support of artificial intelligence development, governments can expand the availability of public datasets and take the lead in establishing industry-specific datasets.