Is 'Leaning on a Big Tree' the Key to Success in Elderly Care PPP Projects? Insights from 306 Projects

Within the PPP industry, there is a saying: “PPP is not just a wedding; it is a marriage.” On one side are the enthusiasm and urgency of local governments; on the other, the hesitation and wait-and-see attitude of private capital. This perspective is particularly apt for the elderly care sector, which is characterized by high upfront investments and long payback periods.

According to data disclosed by the Public-Private Partnership Center (hereinafter referred to as the “PPP” Center) and China Investment Securities, as of June 2017, a total of 13,554 projects had been included in the national PPP project database, with a combined investment of RMB 16.36 trillion. Among these, only 306 were elderly care projects, accounting for merely 2.2% of the total number of projects, while their total investment amounted to RMB 181.6 billion, representing just 1% of the overall investment. These figures indicate that elderly care was not among the priority sectors for development.

However, an interesting perspective is that the first generation of the middle class since the reform and opening-up is about to retire, leading to an explosion in elderly care demand. High-quality elderly care services, including institutional and home-based care, will gain further favor among consumers. With strong demand in the mid-to-high-end segment, brand effects will drive revenue growth for mid-to-high-end brands.

On August 14, the Ministry of Finance and two other ministries jointly issued the “Implementation Opinions on Leveraging the Public-Private Partnership Model to Support the Development of the Elderly Care Services Sector” (hereinafter referred to as the “Opinions”), which outlined the general requirements and priority areas for applying the PPP model in the elderly care sector. Historically, elderly care has been regarded as a slow-burn investment due to its high capital intensity and long payback period. In recent years, a series of favorable policies targeting the sector have been introduced, including this joint issuance by the three ministries, underscoring the attention and support from top-level design for the elderly care industry.

Although policies have gradually shifted from “broad-brush” approaches to targeted implementation, elderly care remains a tough nut to crack.

Can the PPP model be effectively implemented? Through what channels can private capital participate? What is the current state of development for elderly care PPP projects? These questions form the starting point of this article. In response, VCBeat analyzed elderly care PPP projects disclosed in the PPP Center’s database to identify underlying patterns.

PPP and Elderly Care

PPP (an abbreviation for Public-Private Partnership), also known as the "government and social capital cooperation" model. It refers to a partnership between the government and private organizations, established on the basis of concession agreements, for the joint construction of urban infrastructure projects or the provision of certain public goods and services. By signing contracts to clarify the rights and obligations of both parties, this model ensures the smooth implementation of cooperation, ultimately enabling all parties to achieve more favorable outcomes than they would have through independent action.

According to the latest report released by MingShu Data, a technology company specializing in big data for China’s PPP industry, central state-owned enterprises (SOEs) and local SOEs led projects accounting for nearly three-quarters of the total investment value of PPP projects signed and implemented nationwide from 2014 to 2017, representing the majority market share; in contrast, the total investment scale of projects led by private enterprises amounted to only one-quarter of the total.

Private capital has a high level of participation in sectors such as social security, elderly care and healthcare, tourism, comprehensive urban development, agriculture, and sports, all of which require strong operational capabilities from social capital.

According to a survey conducted by China Investment Securities on demographic structure and home-based elderly care models, the current problems facing China’s elderly care industry are as follows:

By 2015, China’s population aged 65 and above had reached 145 million, accounting for 10.46% of the total population, with the aging demographic structure creating substantial demand for elderly care. According to international standards, the proportion of the working-age population (aged 15–64) has been in continuous decline since 2011. Currently, 90% of elderly care in China is provided through home-based care models. The declining share of the working-age population, coupled with population aging, will exacerbate the burden of elderly care on the workforce.

China’s current elderly care model follows the typical “90-7-3” pattern, with home-based, community-based, and institutional care accounting for 90%, 7%, and 3% of the total, respectively. Home-based care dominates the landscape, highlighting the market’s need for more diversified elderly care models.

Unclear Functions and Ambiguous Positioning: Public Elderly Care Institutions Urgently Need Transformation

Currently, the market features a dual-track system where public and private elderly care institutions operate in parallel. The market competition mechanism is imperfect: public institutions benefit from government preferential policies and subsidies, while private institutions are responsible for their own profits and losses. Despite competing in the same market, public nursing homes frequently face a severe shortage of beds. In some key cities, seniors may need to wait for several years or even decades to secure admission to a public nursing home.

Meanwhile, some public elderly care institutions suffer from insufficient operational vitality and low levels of specialization, making it difficult for resident seniors to receive comprehensive care. Industry experts believe that these issues are closely linked to unclear functional positioning, rigid management systems, and imbalanced allocation and utilization of resources in public nursing homes.

Furthermore, from the perspective of a core indicator of the development of the social elderly care service system—namely, the number of beds per capita—public data show that there are 31.6 elderly care beds per 1,000 elderly people, representing a 4.3% year-on-year increase. However, this figure still falls short of the target of “35–40 elderly care beds per 1,000 elderly population” outlined by the Ministry of Civil Affairs.

In fact, as early as 2015, Beijing Municipality issued three documents—the “Implementation Measures for the Public-Built and Privately Operated Model of Elderly Care Institutions in Beijing,” the “Administrative Measures for Admission and Assessment of Public Elderly Care Institutions in Beijing,” and the “Interim Measures for Fee Management of Public Elderly Care Institutions in Beijing”—to gradually privatize 215 public elderly care institutions in the city. The urgent need for transformation of public elderly care institutions has become a practical necessity.

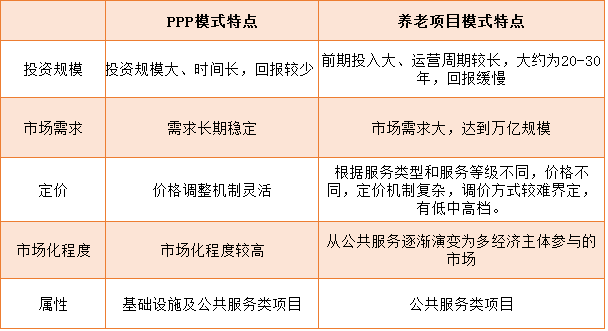

Comparison of the Characteristics of the PPP Model and Elderly Care Projects

Comparison of the Characteristics of the PPP Model and Elderly Care Projects

Given the respective characteristics of the elderly care service industry and the Public-Private Partnership (PPP) model, the PPP model can basically align with the elderly care service industry to address the funding gap it faces.

The similarities between the two are manifested in the following three aspects:

First, the PPP model and the elderly care industry are perfectly aligned in terms of their applicable domains.That is, the elderly care industry falls within the realm of public services, and Public-Private Partnerships (PPPs) are also applicable to infrastructure development and public service sectors;

Second, the PPP model and the elderly care industry share identical input-output characteristics., the PPP model involves substantial investment, long timeframes, and relatively low returns. The elderly care industry requires massive upfront investment and yields profits slowly; its quasi-public welfare nature precludes the generation of exorbitant profits. From this perspective, PPP and the elderly care service industry share a common foundation for integration;

Finally, the elderly care service industry is characterized by long-term stability and a high safety margin.This necessitates that investments also possess long-term orientation, stability, and high security, which aligns well with the characteristics of the PPP model.

Policy Interpretation

In late 2014, the State Council issued the “Guiding Opinions on Innovating Investment and Financing Mechanisms in Key Areas to Encourage Social Investment,” which stipulated that social capital should be encouraged to increase investment in social undertakings and to participate in elderly care infrastructure development through joint ventures, cooperation, and consortiums. The issuance of this document signaled the government’s initial encouragement for private capital to develop the elderly care sector through Public-Private Partnership (PPP) models.

At the same time, among the first batch of 30 PPP demonstration projects announced by the Ministry of Finance, no elderly care projects were included in the final list. However, in late June 2015, the Ministry of Finance issued a notice requesting local governments to submit nominations for the second batch of demonstration projects, marking the first time that it explicitly called for identifying and soliciting elderly care projects suitable for the PPP model.

In 2015, the State Council forwarded the Notice of the People’s Bank of China and Other Departments on Issuing the Guiding Opinions on Promoting the Public-Private Partnership (PPP) Model in the Field of Public Services, which explicitly encouraged the widespread adoption of the PPP model to provide elderly care services in public service sectors such as eldercare, thereby attracting private capital participation. The promotion of the PPP model in the provision of public services has offered a new paradigm and opportunity for the development of institutional elderly care services in China.

In 2015, the “Guiding Opinions on Promoting the Integration of Medical and Health Care with Elderly Care Services” (Guo Ban Fa [2015] No. 84) issued by the General Office of the State Council pointed out that social forces should be encouraged to establish medical-nursing combined institutions, and support should be provided for social forces to set up non-profit medical-nursing combined institutions through models such as franchising, public construction with private operation, and private operation with public assistance. At the same time, it emphasized improving policies related to investment and financing, fiscal taxation, and pricing. For medical-nursing combined institutions that meet the conditions, relevant support policies shall be implemented in accordance with regulations. Market-oriented financing channels should be broadened, and investment and financing models of government-social capital cooperation (PPP) should be explored. Equal participation of all types of entities shall be ensured.

In 2017, the Ministry of Finance and two other ministries jointly issued the “Implementation Opinions on Leveraging the Public-Private Partnership Model to Support the Development of the Elderly Care Services Industry,” prioritizing support for institutional and community-based elderly care, accelerating the transformation of elderly care models, actively promoting smart elderly care projects, and enhancing the profitability of elderly care institutions.

In terms of emphasizing risk control, the government has also issued relevant policies for the PPP model. In 2015, the Ministry of Finance released the Guidelines for Fiscal Affordability Assessment of Government and Social Capital Cooperation Projects, which clearly stated that the scale of new PPP projects should be prudently controlled to prevent exacerbating fiscal revenue and expenditure contradictions due to project implementation.

In 2017, the Legislative Affairs Office of the State Council organized a symposium on the Public-Private Partnership (PPP) Regulations to discuss the many challenges currently facing the regulatory framework. This move by the State Council signals an acceleration in PPP legislation, with the aim of further standardizing practices and addressing issues arising during the implementation of the PPP model.

An analysis of the specific provisions in the aforementioned policies reveals that, at the national level, priority support is directed toward institutional and community-based elderly care, with the aim of accelerating the transformation of elderly care models.

If the national government could issue operational guidelines on strengthening constraints on governmental responsibilities and ensuring value for money throughout the entire life cycle of PPP projects, the security and profitability of such projects would be significantly enhanced, thereby increasing their attractiveness to private capital.

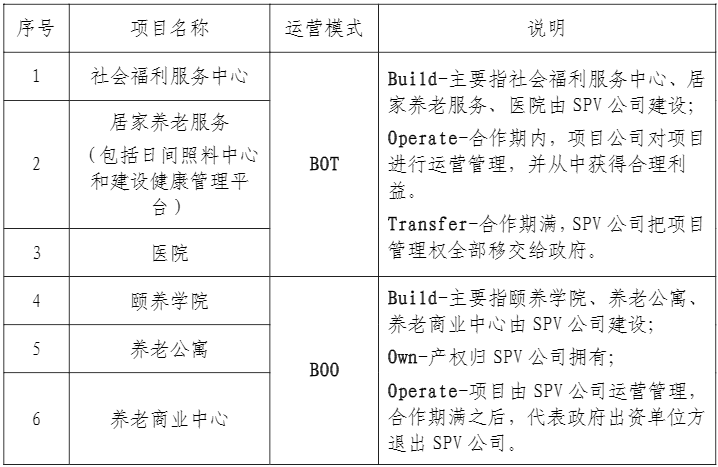

PPP Project Operation Model

According to the Ministry of Finance’s “Operational Guidelines for the Public-Private Partnership (PPP) Model,” PPP project implementation methods primarily include three major categories comprising nine specific models: Operations and Maintenance (O&M), Management Contract (MC), Build-Operate-Transfer (BOT), Build-Own-Operate (BOO), Transfer-Operate-Transfer (TOT), Rehabilitate-Operate-Transfer (ROT), and Lease-Operate-Transfer (LOT). As illustrated in the figure below, the level of private sector participation increases progressively from top to bottom.

Among them, the four most common operational models in the elderly care sector are BOT, BOO, TOT, and ROT.

PPP Project Operation Model (Source: Government and Social Capital Cooperation Center, Tospur Consulting Research Institute)

The operational models for each component specified in a certain smart elderly care service project (Source: PPP Center Database)

Taking a smart elderly care service project from the PPP Center Database as an example, its feasibility study report specifies that the project’s operational model adopts a hybrid BOT+BOO structure, with clear delineation of the components covered under the BOT and BOO models respectively.

Here, "SPV company" refers to a "Special Purpose Vehicle." A Special Purpose Vehicle is an overseas enterprise directly established or indirectly controlled by domestic resident legal persons or domestic resident natural persons for the purpose of conducting equity financing (including convertible bond financing) abroad using their held assets or equity interests in domestic enterprises. In short, it is a project company established to achieve risk isolation from a legal perspective.

Current Status of Elderly Care Development under the PPP Model

Number of Elderly Care PPP Projects and Total Investment Amount (Data compiled from: PPP Comprehensive Information Platform Project Database)

According to data disclosed by the Government-Social Capital Cooperation Center (hereinafter referred to as the “PPP” Center) and China Investment Securities, as of June 2017, a total of 13,554 projects had been included in the database, among which only 306 were elderly care projects, accounting for merely 2.2%. The total investment amount of PPP projects reached RMB 16.36 trillion, with elderly care projects totaling RMB 181.6 billion, representing 1% of the total investment.

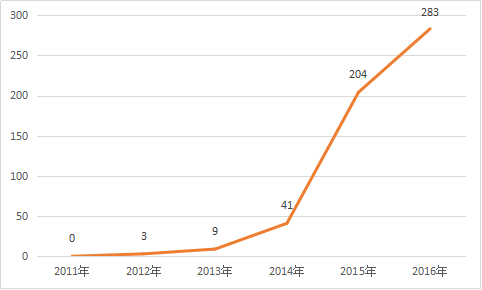

Trend in the Number of Elderly Care PPP Projects in China from 2011 to 2016 (Data Compiled from: PPP Comprehensive Information Platform Project Database)

As shown in the figure, the development of elderly care public-private partnership (PPP) projects started from zero in 2011, with the first project emerging in 2012. A surge occurred during 2014–2015, when the number of projects jumped from 41 in 2014 to 204, representing a growth rate of approximately 400%. By 2016, the sector entered a phase of steady growth. Although data for 2017 cover only the first half of the year and are therefore not included in the table above, the number of elderly care PPP projects reached 306 in just six months—an increase of 120 compared with 2016—indicating a clear upward trend.

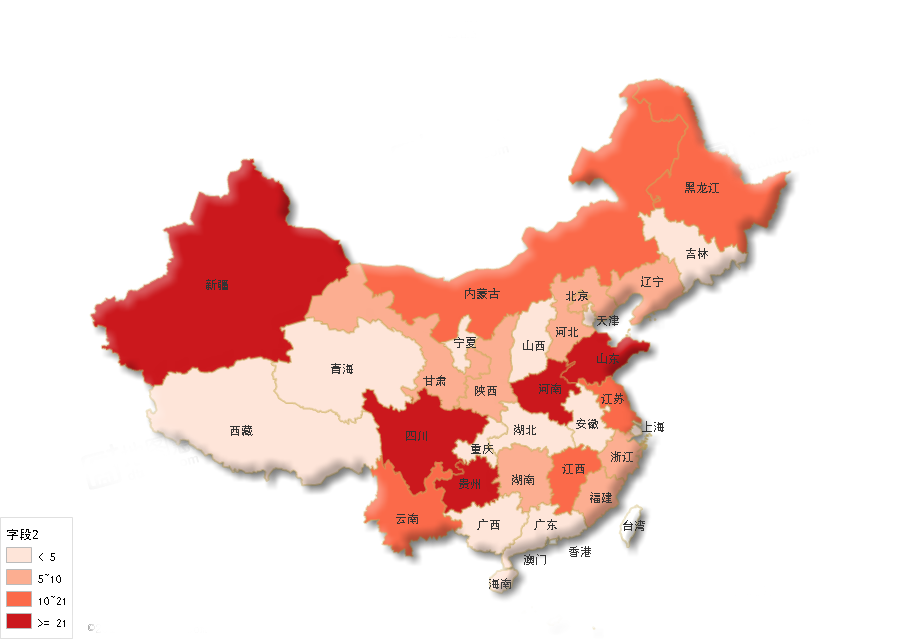

As of June 2017, Shandong and Guizhou provinces had the highest number of elderly care projects utilizing the Public-Private Partnership (PPP) model, with 46 and 43 projects, respectively. Henan (28 projects), Xinjiang (23 projects), and Sichuan (21 projects) followed closely behind. Seven provinces or municipalities directly under the central government, including Shanghai and Guangdong, currently have no PPP-based elderly care projects in their project databases, indicating an uneven geographic distribution.

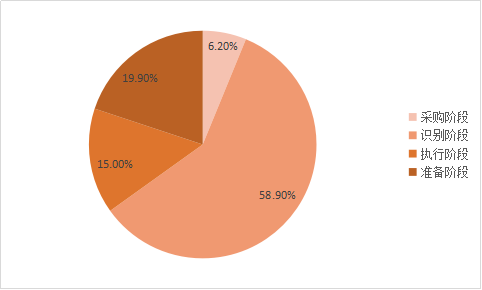

Statistics on the Stages of Elderly Care PPP Projects in China (Data Compiled from: PPP Comprehensive Information Platform Project Database)

Among these 306 elderly care PPP projects, the majority remain in the identification phase. Specifically, 180 projects are in the identification phase, accounting for 58.9% of the total; 61 projects are in the preparation phase; 19 projects are in the procurement phase; and 46 projects are in the implementation phase. No projects have yet entered the transfer phase.

As the development of elderly care public-private partnership (PPP) projects started relatively late, more than half of them are still in the identification phase. It is observable that, in the future, once this batch of projects matures, elderly care initiatives with dual government and social backgrounds will experience explosive growth.

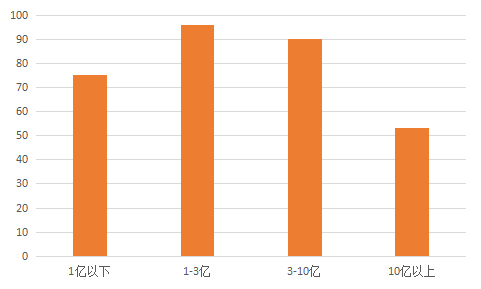

Distribution of Investment Amounts in China’s Elderly Care PPP Projects (Data Compiled from: PPP Comprehensive Information Platform Project Database)

The investment amounts for elderly care PPP projects vary significantly, with the majority of projects falling within the RMB 100–300 million range. Among them, the Jiaxiang Jiudingshan Elderly Care Services and Ecological Comprehensive Governance Project in Jining City, Shandong Province, has the highest investment amount, reaching RMB 13,078.3 million.

In terms of total investment, PPP elderly care projects are characterized by substantial capital outlays, with construction initiatives often named after macro-level plans such as industrial parks, eco-cities, demonstration bases, and integrated complexes.

In addition to the aforementioned statistical data, observations of specific project details reveal that China’s elderly care PPP projects also exhibit the following characteristics:

First, investments in elderly care public-private partnership (PPP) projects are concentrated in the elderly care services sector—a subsector of the broader elderly care industry—and in the integrated medical and elderly care model, with limited involvement in other areas.

The elderly care service industry is exhibiting a trend toward comprehensive development. Beyond traditional services such as daily living assistance, rehabilitation nursing, and the development of specialized products, it now encompasses numerous sectors including elderly-focused food, consumer goods, health supplements, insurance, tourism, and cultural and educational services.

Second, existing elderly care PPP projects primarily adopt BOO and BOT as their main operational models. Companies in the elderly care sector should select appropriate revenue models based on the specific circumstances of project implementation, striving to maximize both economic and social benefits.

Furthermore, given the substantial initial investment and prolonged payback period associated with elderly care Public-Private Partnership (PPP) projects, it is essential to adopt a multifaceted approach that prioritizes risk management. The development of elderly care PPPs will inevitably increase the number of available beds, thereby alleviating supply shortages. In addition to meeting the demand for basic, safety-net elderly care services, the participation of private capital can also cater to mid-to-high-end elderly care needs.

Discussions on PPP Projects: The Financial Sector’s PerspectiveXiao Guangrui, a Senior Project Officer at the Asian Development Bank, previously pointed out that public-private partnerships (PPP) are not, nor can they ever be, a panacea. Not all projects are suitable for the PPP model, and there have been numerous failed PPP projects internationally. As one of the methods for supplying public goods and services, PPP serves merely as a complement to, rather than a replacement for, the traditional government-led supply model. Even in the United Kingdom, where PPP application is most mature, investment in PPP projects peaked at only 22% of total expenditure on public goods and services.

Zhongtai Securities points out that the senior care real estate sector is currently developing under a dual-drive model of “policy + commerce.” Although the underlying rationale for senior care real estate is grounded in the cyclical nature of national demographic structures and social welfare orientation, the promotion of its commercialized model is based on rebalancing social welfare with market-oriented operations. Therefore, while relevant policy formulation provides substantial support in foundational areas such as land supply, both industrial scaling and service profitability require market-driven momentum. In the later stages, the core capital force of the entire industry should be led by private capital. Consequently, the extension of the Public-Private Partnership (PPP) model into the senior care real estate sector aligns with the specialized segmentation direction of private enterprises.

Compared with sectors such as rail transit and sewage treatment, which were early adopters of the Public-Private Partnership (PPP) model and have accumulated substantial experience, elderly care is a relative newcomer. Nevertheless, the government is actively facilitating the integration of elderly care with PPP. Therefore, in the face of urgent demand for elderly care services and vast market potential, it is imperative to promptly identify more effective and practical approaches for aligning elderly care with the PPP model.

Under the government's strong promotion, various regions have undertaken practical initiatives in elderly care public-private partnership (PPP) projects.Given the current state of projects, the concerning low implementation rate has become the biggest bottleneck hindering private capital entry.Unfortunately, there is still no truly mature experience to draw upon in the elderly care sector, with the vast majority of public-private partnership (PPP) projects in this field still proceeding by trial and error.Therefore, under the favorable conditions created by a series of policies, PPP projects require a deeper commitment to the “spirit of contract” to safeguard investment risks.