Why Are IPO Successes So Rare Among Third-Party Independent Medical Institutions Despite a Market Size Exceeding RMB 400 Billion?

By Luo Mei and Gao Kangping

On September 15, at the Shanghai Guoxin Zijinshan Hotel, Haoyue Capital hosted a salon on “The Path to IPO for Third-Party Independent Medical Institutions.” Representatives from listed companies and related enterprises, securities firms, law firms, and accounting firms—including Dian Diagnostics (300244), Fuyi Tianjian, Yimai Yangguang, Kunya Medical (835689), Ganxin Information (836370), Zou Yunjian, an equity partner at Zhong Lun Law Firm and the signing lawyer for Dian Diagnostics’ IPO project, and Zhu Haiping, a partner at BDO China Shu Lun Pan CPAs and the signing CPA for KingMed Diagnostics’ IPO team—shared insights on the business models and IPO journeys of third-party independent medical institutions.

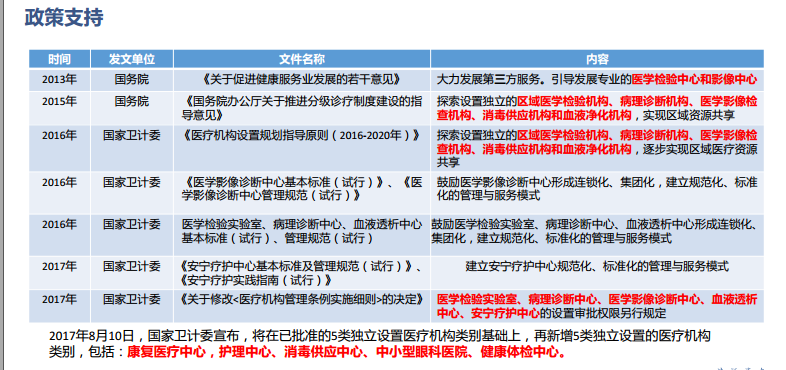

The so-called “third-party independent medical institutions” primarily refer to the five additional categories of independently established medical institutions announced by the National Health and Family Planning Commission (NHFPC), bringing the total to ten types: medical laboratory testing centers, pathological diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, palliative care centers, rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers. The NHFPC permits social capital to invest in these ten categories of independent medical institutions and encourages chain-based and group-oriented operations.

Third-party medical laboratories emerged more than a decade ago, initially experiencing slow chain expansion. It was not until the implementation of the new healthcare reform in 2009 that these laboratories achieved rapid development and attained a certain scale. Dian Diagnostics established its first medical laboratory in 2004, successfully completed Series A financing in 2009, subsequently engaged IPO intermediaries, and entered the pre-IPO compliance and guidance period, ultimately completing its initial public offering on the ChiNext Board in July 2011.

But why did KingMed Diagnostics, which started earlier and was also driven by capital, only complete its IPO this September? Is the path to an initial public offering (IPO) inherently difficult for third-party independent medical institutions? What are the main challenges?

Jin Liang, a partner at Haoyue Capital, has nearly a decade of experience in investment banking at domestic securities firms. He was fully responsible for the on-site execution of the IPO projects for Aier Eye Hospital and Dian Diagnostics. In his view, policy support is a prerequisite for a company’s successful IPO.

First, national policies encourage the development of third-party medical services by establishing regional medical institutions to foster regionalization and group-based operations. Second, there are already cases of domestic independent third-party medical institutions going public through initial public offerings (IPOs), such as Dian Diagnostics and KingMed Diagnostics.

“Although healthcare service providers rarely go public via IPOs on China’s A-share market, the information I have obtained from regulatory authorities indicates that they have never excluded such entities from listing on the A-share market. Only when healthcare service providers strengthen their internal capabilities, achieve sufficient operational standardization, and maintain sustainable profitability can they ultimately succeed in going public,” added Jin Liang.

Since market capacity is closely related to a company’s sustainable development and profitability, the market capacity of third-party independent medical institutions will also be one of the focal points for regulatory authorities during IPO reviews.

According to relevant research reports, the annual market size of the medical laboratory testing sector is at least RMB 200 billion; the medical imaging market also exceeds RMB 200 billion per year. The market penetration rate for hemodialysis treatment in China remains very low, with the current annual market size estimated at approximately RMB 30 billion. Based on these figures, the combined annual market size for the three major categories of third-party independent medical institutions—medical laboratories, imaging centers, and hemodialysis centers—is at least RMB 400 billion. Apart from independent medical laboratories, which have achieved a market share of approximately 5%, the market shares of independent imaging centers and independent hemodialysis centers are each below 1%, significantly lower than those in developed countries in Europe and the United States. Although the potential market for third-party independent medical institutions is substantial, the extent to which they can capture market share will have a significant impact on the initial public offerings (IPOs) of industry players. For instance, the market share of independent medical laboratories has risen from around 1% in 2010 to the current 5%.

Like other healthcare services, third-party medical services also face the challenge of service radius limitations. As a result, any individual third-party medical institution has an inherent growth ceiling, which is one of the factors hindering scale expansion for companies in this industry. Therefore, during the process of going public or pursuing growth, companies typically adopt a replicable chain model to overcome the constraints imposed by service radius.

Any chain business model must address the balance between growth speed and development quality. If expansion is too rapid, overall profits will decline; conversely, to maintain current profit levels, the pace of expansion should not be overly aggressive. According to Jin Liang’s recollection, during the 2010–2011 period when Dian Diagnostics was preparing for its initial public offering (IPO), the company deliberately slowed down its expansion. In a fiercely competitive market environment, going public is a crucial strategic move; those who list earlier gain the initiative. Therefore, once an IPO plan is confirmed, it is preferable to sacrifice some expansion speed rather than easily allow profits to drop, and certainly not to let annual profits turn negative. Otherwise, the goal of listing on China’s A-share market would become increasingly elusive.

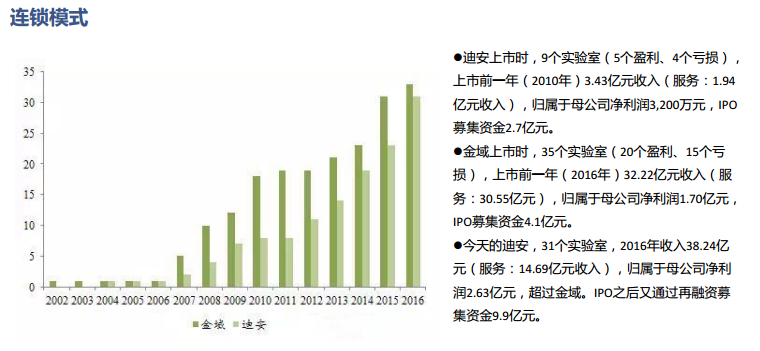

According to Jin Liang’s recollection, when Dian Diagnostics went public in 2011, it had only nine laboratories, whereas KingMed Diagnostics already operated nearly 20, marking a significant gap. However, following its successful IPO and continuous acquisitions leveraged through its capital platform, Dian Diagnostics managed to catch up and surpass its competitor. Today, the two companies are roughly equivalent in terms of the number of laboratories.

Second, there is the issue of centralized procurement and unified management in the chain model. When third-party independent medical institutions go public, regulatory authorities have consistently focused on the headquarters’ control capabilities. Without robust headquarters-level oversight, the replication advantages inherent to the chain business model become merely nominal, rendering future growth prospects untenable.

Third is the replicability of the chain model. It is well known that capital markets favor leaders in niche sectors, and regulators also encourage such leading companies to go public. How to replicate the chain model and either outperform competitors or secure a favorable position within the sector is a critical issue that every independent third-party medical laboratory chain must carefully consider. The ratio of profitable to loss-making sites is one dimension for assessing the replication capability of independent third-party medical institutions. Chain operators with only one or a few profitable locations will face significant challenges during the IPO review process. According to Jin Liang, Dian Diagnostics had nine laboratories (five profitable and four loss-making) when it went public in 2011. KingMed Diagnostics currently operates 35 laboratories (20 profitable and 15 loss-making), reflecting a relatively balanced and appropriate profit-to-loss ratio.

The origins of independent laboratories in the United States can be traced back to the 1950s and 1960s. After successive rounds of mergers, acquisitions, and consolidation, the U.S. independent laboratory market has evolved into an oligopoly dominated by two giants, Quest and Labcorp, which together hold approximately 70% of the market share.

The emergence of independent clinical laboratories in China can be traced back to the healthcare reforms at the beginning of this century, while their rapid growth was driven by the 2009 healthcare reform. In just 20 years, China has accomplished what took the United States 60 years. Future trends are already evident: cost containment within medical insurance is inevitable, tiered diagnosis and treatment systems are being encouraged, and the expansion of private medical institutions is unstoppable. The combined effect of these factors will further elevate the market share of independent clinical laboratories beyond its current 5% to new heights.

For independent clinical laboratories that currently lack the conditions to become leaders in their niche sectors, blindly pursuing scale is inadvisable. Instead, they should pursue differentiated competition. In addition to refining and strengthening certain specialized testing services, they can extend their business horizontally into areas such as forensic judicial appraisal, health check-ups, and food and environmental testing. Indeed, industry leaders KingMed Diagnostics and Dian Diagnostics have long since expanded into these other niche segments, including forensic judicial appraisal and health check-up services.

Globally, the outsourcing of third-party services by healthcare institutions has become an inevitable trend. Third-party medical services refer to an organizational model in which healthcare institutions outsource non-core business functions—excluding clinical services such as inpatient care, outpatient consultations, and surgeries—to third-party providers. This model offers three major advantages: first, it reduces costs through economies of scale; second, it ensures service quality and outcomes through specialized expertise; and third, it effectively facilitates the implementation of tiered diagnosis and treatment systems.

Beyond the third-party medical testing sector, Haoyue Capital also specially invited representatives from four client organizations: Chen Chong, General Manager of Fuyi Tianjian; Wang Shihe, Founder of Yimai Yangguang; Shao Jianying, Deputy General Manager of Kunya Medical; and Xu Hongzhen, Founder of Ganxin Information. These four companies are leaders in China in the fields of logistics outsourcing, independent third-party imaging centers, medical equipment maintenance outsourcing, and infection control information technology outsourcing, respectively.

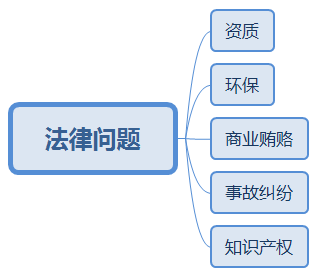

During the initial public offering (IPO) process of third-party independent medical institutions, regulatory compliance constitutes the most critical review principle for regulators, encompassing both legal and financial compliance.

Any service for which a hospital is required to make payments must have a legal basis. According to Zou Yunjian, an equity partner at Zhong Lun Law Firm and the signing lawyer for Dian Diagnostics’ IPO project, third-party independent medical institutions differ from general medical facilities; legally, they constitute outsourced service providers for hospitals. A legal relationship exists between the patient and the hospital, whereas the legal relationship between the hospital and the third-party independent medical institution is distinct from that between the patient and the third-party independent medical institution. It is through national legislation that it is stipulated which institutions qualify as third-party independent entities.

In recent years, the state has intensively issued a series of administrative regulations and detailed facility standards to support third-party independent medical institutions. Among these, the most significant is the "Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions," which incorporates third-party independent medical institutions into the regulatory framework for medical institutions. This represents a relatively new development, signaling state recognition and encouragement of the growth of third-party independent medical institutions. Therefore, investors should keenly seize this trend.

Regulatory authorities impose numerous legal review requirements for IPOs, mandating that lawyers conduct thorough due diligence on the company across more than a dozen aspects and issue a lawyer’s work report and legal opinion. These cover qualifications, environmental compliance, commercial bribery, disputes over medical incidents and service quality, independence, intellectual property rights, and other common issues.

First, qualifications are the most basic requirement. What should we focus on? The primary concern is whether the enterprise’s Medical Institution Practicing License is classified as non-profit. If it is non-profit, it should be converted to for-profit status as soon as possible. Secondly, it is necessary to examine whether the enterprise’s upstream suppliers and downstream customers possess the relevant qualifications. For instance, if the enterprise purchases pharmaceuticals or medical devices, attention must be paid to whether it holds the required Pharmaceutical Production and Operation License or Medical Device Production and Operation License. If such licenses are not held, corresponding measures should be taken promptly, as qualification issues often involve government actions and constitute uncontrollable factors.

In terms of environmental protection, relevant laws and regulations require enterprises to obtain full approval for environmental impact assessments (EIA) before commencing operations. In practice, however, many companies only apply for EIA approval and acceptance after their business operations are already underway. Given the complexity of EIA approval procedures and the lengthy processing time, regulatory authorities generally tolerate companies completing the EIA approval process prior to filing for an initial public offering (IPO).

In the realm of commercial bribery, the healthcare industry cannot sidestep this issue. Since commercial bribery is inherently illegal, companies that employ illicit means to secure business are clearly ineligible for initial public offerings (IPOs). This year, IPO applications from healthcare and medical enterprises have been frequently rejected, many due to concerns related to commercial bribery. In one notable case, despite reporting a net profit of RMB 200–300 million, a company failed to provide a clear explanation for its marketing and promotion expenses, ultimately leading to the rejection of its IPO application.

In addressing issues related to diagnostic accidents, diagnostic disputes, and service quality, intermediary agencies will verify relevant information through methods such as online searches, visits to client hospitals, and consultations with local regulatory authorities.

Regarding intellectual property issues, as some medical institutions often collaborate with universities and research organizations to develop related technologies, regulatory authorities will also focus on matters such as the ownership of intellectual property rights and the distribution of benefits.

According to Zhu Haiping, a partner at BDO China Shu Lun Pan CPAs and the signing accountant for KingMed Diagnostics’ IPO project, initial public offerings (IPOs) of medical service companies share both similarities and differences with those of companies in other sectors, necessitating case-by-case analysis.

Zhu Haiping introduced the framework of financial issues that third-party medical service providers should focus on during their initial public offerings (IPOs), including revenue, costs, research and development expenses, government subsidies, and other related matters. Among these, the revenue and cost components can be consolidated to form an analysis of gross profit margin.

Regarding revenue, the principles, timing, basis, and methods of revenue recognition are key areas of regulatory focus. In essence, the services provided by third-party medical service institutions constitute service income; therefore, the general principle for revenue recognition is as follows: if the outcome of a service transaction can be reliably estimated at the balance sheet date, the percentage-of-completion method shall be applied to recognize service revenue.

Regarding customers, third-party medical service providers should pay particular attention to: the specific methods used for business development and order acquisition; whether order acquisition is compliant with regulations; and whether there are any instances of paying fees on behalf of others or commercial bribery. Additionally, they should assess the nature of transactional cooperation with customers; the reasons behind significant changes in service pricing; and whether any related-party relationships or other利益 arrangements exist with customers.

Regarding cash settlements, third-party medical service providers should pay special attention to: (1) the reasons for cash transactions and whether they are reasonable and compliant; (2) the scale of cash transactions; (3) whether the enterprise has designed and implemented sound and effective internal control systems for cash transactions; and (4) the measures taken by the enterprise to reduce cash transactions and the trend in the proportion of cash transactions.

Regarding costs, third-party medical service providers should pay attention to the following three issues: (1) the specific principles and methods for allocating operating costs across various business lines; (2) year-over-year changes in cost structure, along with comparative analysis against industry peers; and (3) the completeness and accuracy of cost accumulation and carryover, as well as the matching of labor service costs with revenues. In addition, other areas such as suppliers, inventory, and outsourced services also warrant attention.

Following the assurance that revenue recognition and cost accounting are truthful, accurate, and complete, horizontal and vertical analyses of gross profit margins become a critical focus in IPO reviews. This primarily includes the overall structure of gross profit margins, trends in gross profit margin changes, trend changes in gross profit margins by business segment, specific reasons for gross profit margin fluctuations and their rationality, as well as comprehensive comparisons incorporating service pricing, unit costs and their composition, customer structure, and service content.

Finally, other financial issues such as R&D expenses, selling and administrative expenses, long-term assets, and government subsidies also require attention.

Zhu Haiping stated that, judging from KingMed Diagnostics’ IPO process, the financial due diligence for an initial public offering is extremely rigorous and should never be taken lightly. Some details scrutinized by regulators were even unexpected to professional intermediary institutions.

Jin Liang, Partner at Haoyue Capital, draws on his many years of experience in the securities industry to offer the following insights and recommendations for companies planning an initial public offering (IPO):

First, select appropriate intermediaries, with a securities firm serving as the lead coordinator, supported by accountants and lawyers. Securities firms are most familiar with shifts in regulatory focus and can propose the most accurate response strategies. In particular, do not rely on so-called “advisors” circulating in the market.

Second, it is crucial to select an appropriate time window and carefully balance the speed and quality of expansion for chain institutions. Advance planning is essential to avoid missing the optimal filing opportunity. Furthermore, since commercial bribery leaves traces in financial records, a strategy of trading time for space must be adopted to ensure a clean record during the reporting period. All of these matters rely on the professional judgment of the securities underwriter.

Third, thoroughly reshape mindsets and instill a strong sense of compliance. Chinese private entrepreneurs have long been accustomed to autocratic decision-making within their enterprises. However, a well-regulated modern enterprise must have a sound corporate governance structure. Entrepreneurs should become accustomed to the practice of submitting major issues for collective deliberation at formal meetings. Furthermore, a clear firewall must be established between the company and its individuals: the company belongs to all shareholders, and corporate funds are not personal assets and must not be misappropriated at will.

Fourth, be fully transparent and address issues at an early stage. Entrepreneurs should not rely on luck or assume that strict confidentiality will prevent intermediaries or regulators from detecting irregularities. Currently, initial public offerings (IPOs) on China’s A-share market require financial due diligence, through which even subtle clues can be uncovered using various verification methods. Moreover, if problems are identified only after materials have been submitted to the China Securities Regulatory Commission (CSRC), it may already be too late, leaving no room for remediation. Therefore, entrepreneurs must maintain genuine openness with their intermediaries, fully disclosing all existing issues and resolving them promptly. If resolution is not immediately feasible, they should consider deferring the filing to ensure a successful debut.

Fifth, maintain firm confidence; an initial public offering (IPO) is just around the corner. Going public is a complex systemic engineering project. The greatest pitfall is taking the initial step but retreating when encountering difficulties, which risks turning previously incurred costs into sunk costs, resulting in losses that outweigh the gains. This is a significant reason why many well-known enterprises have yet to achieve an IPO. Had they maintained firm confidence and avoided fear of challenges back then, many obstacles could have been readily resolved, and their IPO aspirations would have long been realized.