China's Medical Mall Sector: 8 Operational Projects Across Major Cities with Over RMB 4.1 Billion Invested

Not long ago, Hangzhou’s 501 Tower quickly rose to prominence for its “Medical Mall” concept. Various labels have been affixed to the Medical Mall, such as “China’s First Medical Mall” and “Shared Hospital.”

"Full-Cycle Healthcare" is a Medical Mall approved by the Zhejiang Provincial Health and Family Planning Commission. Its partners include Sir Run Run Shaw Hospital, New Jiebai Group, Dian Diagnostics, and entities from the healthcare, retail, and real estate sectors under Baida Group. Floors 1 to 5 are designated as shopping areas, while floors 6 to 20 are entirely dedicated to the medical mall. Consumers can enjoy a multidimensional experience combining shopping and healthcare services at the Medical Mall, thereby alleviating the anxiety associated with visiting traditional hospitals.

Medical Malls, such as Quancheng Medical, are not entirely new; in fact, Shaanxi Province saw the emergence of a healthcare-focused commercial complex centered on pharmaceuticals as early as 2005. According to incomplete statistics from VCBeat (WeChat ID: vcbeat), eight regions across China have developed healthcare commercial complexes, with total investments exceeding RMB 4.1 billion, all of which are fully operational.

What are the characteristics of Medical Malls in these regions? How are they positioned, and how do they operate?

The term "Medical Mall" referred to here denotes facilities located within commercial complexes that combine retail shopping functions with convenient consumer-oriented medical services, such as traditional Chinese medicine (TCM), health management, medical aesthetics, and dental care. Investors involved include real estate developers, healthcare institutions, and retail entities, with a minimum investment of RMB 20 million and cumulative capital inflows exceeding RMB 4.1 billion. This indicates that the model is capital-intensive, focused on resource integration, and demands high operational expertise from operators.

As can be seen from the statistical list, details regarding the establishment date, floor area, capital investment, business segments, functions, and operational status of these eight Medical Malls are provided. In terms of investors, most have a medical background. For instance, Quancheng Medical was jointly established by three companies, with Hangzhou Jiebai Group Co., Ltd. holding a 45% stake, Zhejiang Dian Diagnostics Technology Co., Ltd. holding 35%, and Baida Group Co., Ltd. holding 20%.

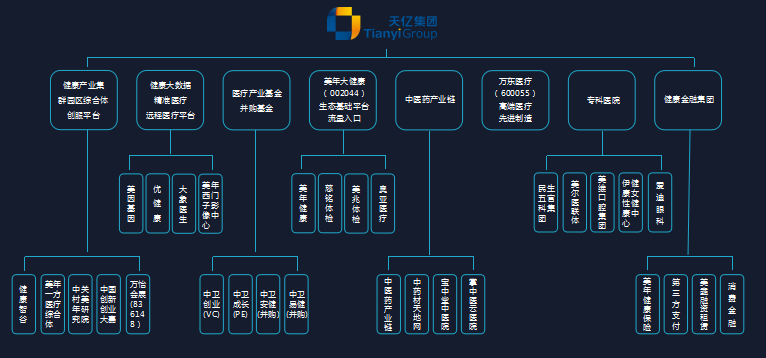

Shanghai Tianyi Hongfang Enterprise Management Co., Ltd. is a wholly-owned subsidiary of Shanghai Tianyi Investment (Group) Co., Ltd. Established in 1998, Shanghai Tianyi Investment (Group) Co., Ltd. is the parent company of Shanghai Meinian Onehealth Healthcare Industry Co., Ltd. and operates as a diversified comprehensive enterprise group engaged in multi-sector investments. The organizational structure of Tianyi Group is shown below:

Another category of investors is primarily composed of pharmaceutical companies, such as Gansu Zhongyou Health City and Xi’an Zhongxin Saihao Pharmaceutical Health City. These Medical Malls mainly focus on the sale of pharmaceutical products. Among them, Xi’an Zhongxin Saihao Pharmaceutical Health City covers an area of 3,000 square meters, offers more than 13,000 product categories, and spans four floors. It is a new business model newly established this year by Shaanxi Zhongxin Pharmaceutical Supermarket Co., Ltd., integrating traditional Chinese medicine clinics, Western medicine clinics, beauty and body care services, health examinations, and a pharmaceutical supermarket.

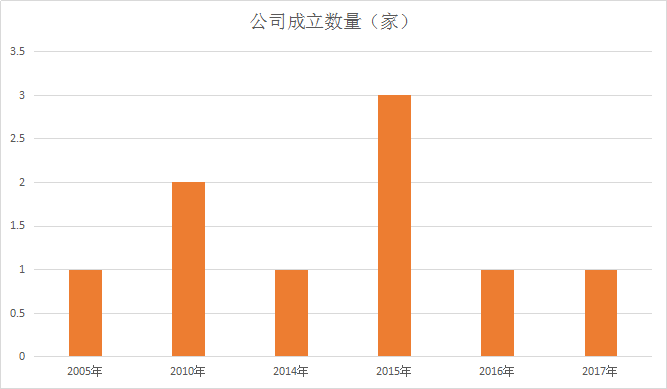

According to statistics from the VCBeat database, the earliest year in which regions became involved in health city projects was 2005, with one city; the highest number occurred in 2015, with three cities; and the most rapid development took place in 2010.

The primary reason is that, following the Sixth National Population Census in 2010, population aging has become more pronounced both nationwide and regionally, marking a phase of continued aging after the population had already transitioned to an aged structure.

According to the census data bulletin, among the population of the 31 provinces, autonomous regions, and municipalities directly under the Central Government on the mainland, as well as active-duty military personnel, the number of individuals aged 60 and above was 177,648,705 at the time of the census, accounting for 13.26% of the total. Of these, those aged 65 and above numbered 118,831,709, representing 8.87%. Compared with the Fifth National Population Census conducted in 2000, the proportion of the population aged 60 and above increased by 2.93 percentage points, while the proportion of those aged 65 and above rose by 1.91 percentage points.

China’s elderly population continues to grow rapidly, with pronounced trends toward an aging and very old demographic. The level of pension and medical security has been further improved, the construction of community-based service networks for the elderly has accelerated, grassroots organizations for older adults have been strengthened, facilities for elderly care have been further enhanced, and significant progress has been made in safeguarding the rights and interests of older persons. Culture, education, and sports programs for the elderly have developed steadily, leading to comprehensive advancement across all areas of aging-related initiatives. Consequently, a series of “Healthy Cities” have emerged.

The second reason lies in the fact that on December 3, 2010, the General Office of the State Council forwarded the “Notice on Further Encouraging and Guiding Social Capital to Establish Medical Institutions,” issued by the National Development and Reform Commission, the Ministry of Health, and other departments. The notice indicated that market access for social capital in healthcare would be relaxed; eligible private hospitals would be included in the network of designated medical insurance providers and enjoy the same tax and pricing policies as public medical institutions. Additionally, foreign investors were permitted to establish wholly owned hospitals in China. The introduction of this policy meant that private hospitals would benefit from a fairer market environment and policy treatment, with promising prospects for development.

On the other hand, the overall tone of “public welfare” in the new healthcare reform plan was further clarified in the Proposal for the 12th Five-Year Plan. Over the past two years, among the five major tasks established by the new healthcare reform, the task of basic medical insurance has been completed ahead of schedule, continuing to advance toward a higher level.

It can be said that the introduction of these policies has greatly facilitated the subsequent development of the Medical Mall. According to Guo Feng, Chairman of Kangning, policy support is a prerequisite for the development of Health City. “In the past, policies in the Xinjiang region were relatively rigid, making it difficult to obtain approval for many business projects. However, significant changes have occurred over the past two years. The local government has responded swiftly to national initiatives such as Healthy China and state-supported development of traditional Chinese medicine. Just as Kangning began planning and preparing for the Medical Mall, the government set a target to establish one within that year. As a result, our subsequent approval process proceeded smoothly.”

Therefore, the Medical Malls established between 2010 and 2016,The relationship with the platform is primarily based on leasing, characteristic of early-stage Medical Malls.This is consistent with the report released by VCBeat on September 19.“Tracing the Development of 30 Medical Malls Over More Than 50 Years: Is This the Easiest Way for Chinese Real Estate Developers to Transition into Healthcare?”There are similarities to the Medical Mall mentioned in the article.

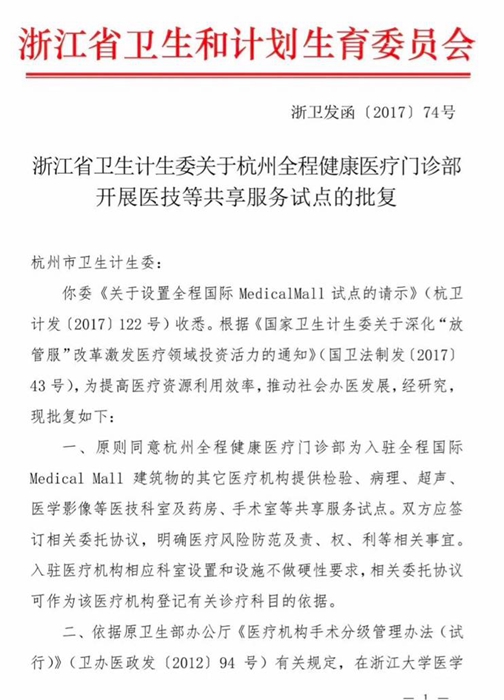

It was not until September 2017 that the Zhejiang Provincial Health and Family Planning Commission officially issued documents on “Medical Mall,” formally designating such centralized healthcare service venues as “Medical Malls.” The initiative also elevated their function to the level of “sharing,” aiming to enable medical enterprises within the Medical Mall to share resources and maximize the value of healthcare services. This concept was later interpreted by the media as “shared hospitals.”

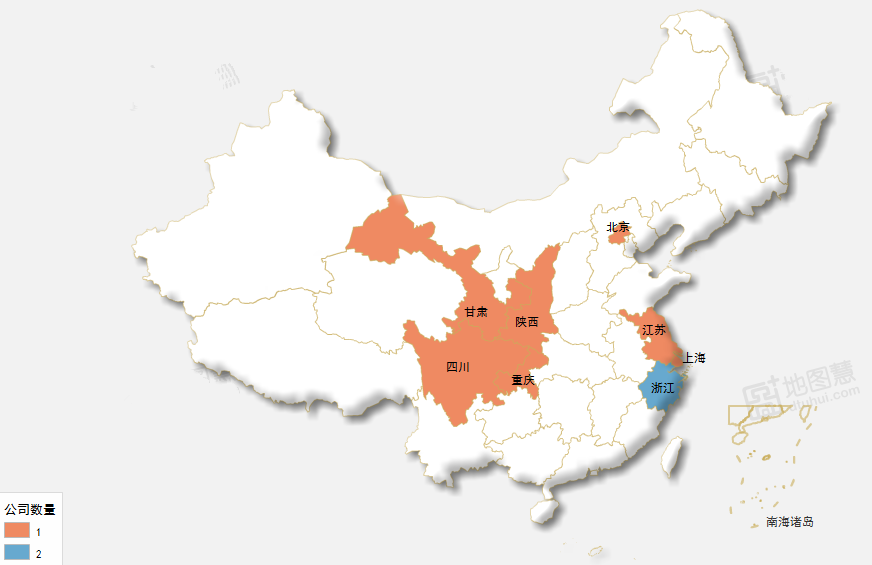

From a geographical distribution perspective, Medical Mall projects are located in the western and coastal regions of China, with two in Zhejiang Province, and one each in Chongqing Municipality, Gansu Province, Shaanxi Province, Jiangsu Province, and Sichuan Province.

Services offered by the Medical Mall vary by region. In coastal areas, the focus is primarily on premium healthcare, such as end-to-end medical services. By integrating a pool of expert physicians from Sir Run Run Shaw Hospital and clinics under the Medical Mall brand, along with top-tier international medical institutions, these resources are made accessible to customers to deliver a one-stop, multi-dimensional healthcare experience.

In terms of health checkups alone, it differs from all Grade A tertiary hospitals in Hangzhou, particularly with its “residential-style health screening.” On the evening of their arrival, all guests undergoing health checkups are invited to attend a “Health Salon” held on the rooftop garden on the 20th floor, which may feature a guided meditation and yoga session or a physiotherapy lecture on joint protection during exercise.

Gansu Zhongyou’s Medical Mall model is relatively mature and was established early on, classifying it as a traditional Medical Mall. The health complex is designed with a tiered operational model, encompassing various business formats such as product retail, professional pharmacies, wellness and physiotherapy services, and optometry and eyewear stores. According to Zhang Fuxiang, Executive President of Zhongyou Health, the core philosophy of the Medical Mall is diversification centered on professionalism. In terms of product structure, pharmaceuticals serve as the core of the health complex, while complementary services—including local specialty products, traditional Chinese medicine (TCM) diagnosis and treatment, health check-ups, medical devices, and wellness care—are sequentially integrated to expand the ecosystem.

On the other hand, Zhongyou has integrated market resources to establish distinctive operational features: it introduces and develops authentic medicinal herbs and local specialty products from Northwest China, such as Angelica sinensis, Astragalus membranaceus, Lily bulb, walnut, and jujube, forming a complete industrial chain encompassing production, processing, retail, and supply and marketing; it invites renowned traditional Chinese medicine (TCM) practitioners within the province to conduct regular consultations, leveraging their expertise to promote refined decoction pieces and authentic medicinal herbs; and it collaborates with upstream industrial enterprises to develop category-specific zones for business operations.

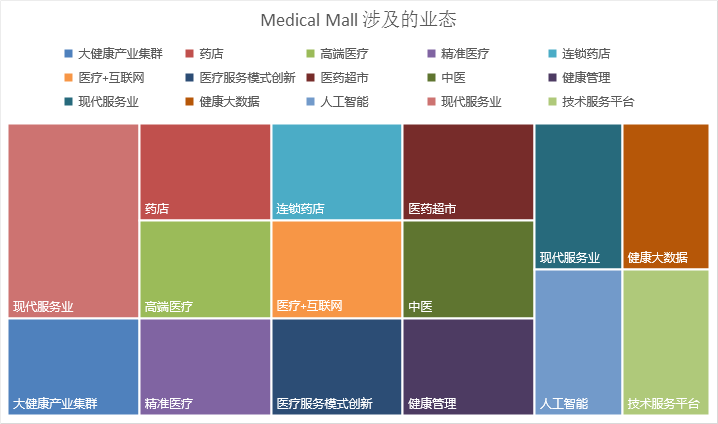

As shown in the chart, Medical Malls across China have diversified into a wide range of sectors, primarily including health big data, modern service industries, independent third-party pharmaceutical commerce, technology service platforms, large health industry clusters, and chain pharmacies.

According to a survey conducted by RET China Commercial Real Estate Research Center in late 2015 on three types of medical clinics—dental, physical examination centers, and traditional Chinese medicine (TCM) wellness—dental clinics have become the most preferred medical format to enter shopping malls due to their flexible space requirements and concentrated demand for personalized medical services. Among more than 300 sampled dental clinics, physical examination centers, and TCM wellness merchants in first-tier cities in China, 16% have chosen to locate in commercial projects, representing a significant increase from 5% in 2010.

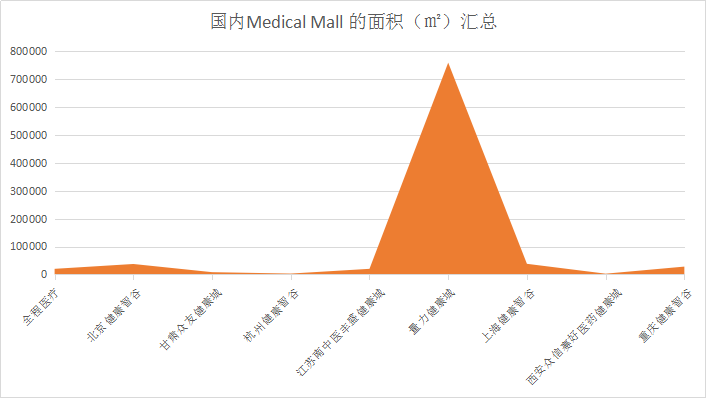

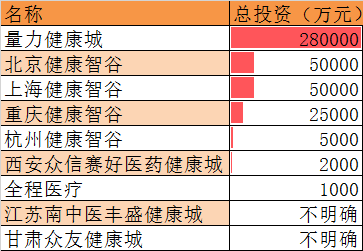

Based on the floor area of Medical Malls established across China, Liangli Health, developed by Chengdu Liangli Group, is the largest, with an area of 760,000 m²; followed by Shanghai Health Intelligence Valley, Beijing Health Intelligence Valley, and Chongqing Health Intelligence Valley.

Although Health Cities across China cover a vast area, the list shows that all of them have been put into operation.

From the perspective of investor types, investors in Medical Malls across China are predominantly enterprises, with relatively few investments from universities and hospitals. Among them, the Jiangsu Nanjing University of Chinese Medicine Fengsheng Health City is a “comprehensive health service complex” jointly developed by Nanjing University of Chinese Medicine and Fengsheng Group. It integrates TCM-specialized medical services, renowned physicians and premium herbal medicines, wellness and healthcare, health management, wellness culture, and conditioning services, dedicated to leading and creating healthy lifestyles. By showcasing Traditional Chinese Medicine (TCM) culture and highlighting the distinctive concept of “preventive treatment,” it aims to become a pioneer in the TCM health industry and establish itself as a “new calling card for the city of Nanjing.”

The hospital joining the initiative is Hangzhou Quancheng Medical, which has partnered with Sir Run Run Shaw Hospital to leverage its superior medical resources and better serve the users of Medical Mall.

The enterprises are primarily those with backgrounds in the health sector, such as Shanghai Tianyi Hongfang Enterprise Management Co., Ltd., Zhejiang Dian Diagnostics Technology Co., Ltd., Gansu Zhongyou Health Co., Ltd., and Shaanxi Zhongxin Pharmaceutical Supermarket Co., Ltd., with real estate developers also joining the fray, such as Chengdu Liangli Group.

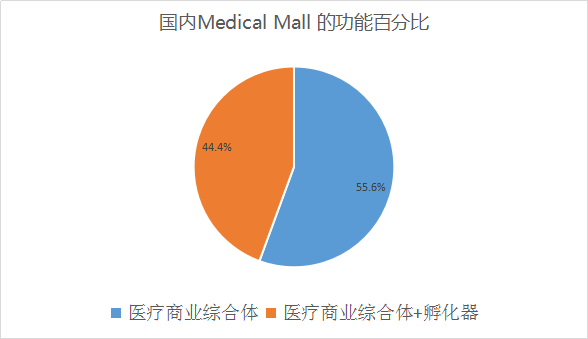

From the perspective of the functional positioning of Medical Mall, there are mainly two models: the medical commercial complex and the medical complex plus incubator.The operation of medical complexes is primarily driven by investment promotion.According to Bi Ling, Chairman of Quancheng Medical, in addition to inviting Sir Run Run Shaw Hospital to join its network, the Quancheng Medical Center has also onboarded 11 well-known specialized clinics from Beijing, Shanghai, Taiwan, and other regions, including the Zhang Qiang Doctor Group, Aiding Fertility and Assisted Reproduction, Weienuo Pediatrics, and Taixue Ophthalmology. These medical institutions possess cutting-edge medical technologies aligned with international standards and can connect with top-tier overseas specialized medical resources, enabling patients to more conveniently access world-leading medical advancements.

“The integrated medical services serve as the brain of the entire Medical Mall. Adhering to the health management philosophy of ‘whole-person, whole-process care,’ we focus on six core modules: health promotion (physical examinations), anti-aging, specialist outpatient clinics, medical technology support, medical services, and membership services. We not only provide guests with scientific, comprehensive, and high-quality full-cycle healthcare and health management services but also create a genuine, multi-dimensional healthy lifestyle for them through cutting-edge international medical fields such as genetic screening and functional medicine,” said Bi Ling.

On the other hand, medical complexes + incubators are represented by Health Intelligence Valley’s Medical Mall.According to Wang Xiaojun, Vice President of Tianyi Investment Group and General Manager of Health Intelligence Valley, although Health Intelligence Valley is distributed across four cities in China—Beijing, Shanghai, Hangzhou, and Chongqing,However, its business model is designed to attract healthcare companies by charging low rent and assisting them with financing. In other words, Health Intelligence Valley charges minimal rent from tenant companies, with the majority of its revenue generated through facilitating their fundraising efforts. “We established Health Intelligence Valley to gather companies in the health industry, select a cohort of high-quality enterprises for incubation, and provide support including financing and fostering business interactions among tenants within the park, similar to WeWork in the United States.”

Beyond conventional incubation services, the greater value lies in leveraging the resources of Health Intelligence Valley, such as public R&D platforms, a health big data center, resource integration with hospitals and academic clinical institutions, and specialized investment funds. These professional services are not available in other industrial parks.

Meanwhile, Health Intelligence Valley hosts an annual innovation and entrepreneurship competition for enterprises within the park, invites startup mentors to provide pre-competition training to participants, and offers a dedicated roadshow hall.

Since 2015, Health Intelligence Valley has introduced more than 40 projects, served over 500 enterprises, hosted more than 60 events, facilitated matchmaking for over 100 projects, assembled a mentor team of more than 40 experts, and provided guidance to over 100 projects. Currently, more than 70 enterprises are registered and settled in the park, with investment promotion activities basically completed. Since early 2016, the park has served more than 100 innovative and entrepreneurial enterprises.

“In January next year, the first medical-commercial complex we are co-developing with Yifang Group (the second-largest shareholder of Wanda Group) will be established at the Jinniu District Wanda Plaza in Chengdu, jointly creating the [Meifang Health] experience platform. Driven by [Health Intelligence Valley] and centered on [Health Management] and [Healthy Living], this platform leverages commercial centers as its carrier. Through precision medicine and personalized services, it builds a one-stop health experience platform integrating functions such as industry incubation, pop-up exhibitions, prevention, screening, treatment, rehabilitation, and experiential services. This initiative marks the first introduction of the internationally leading ‘health complex’ model to China, enabling citizens to enjoy comprehensive, professional, and accessible one-stop health experiences within commercial centers. The platform is similar to the ‘Hangzhou 501 Building’s full-process healthcare’ model. In the future, we also aim to replicate [Meifang Health] across Wanda Plazas nationwide,” added Wang Xiaojun.

So, is the development of Medical Mall a fleeting bloom or a spark that starts a prairie fire?

From the conditions for the emergence of Medical Malls abroad:

First, over the past two decades, as the U.S. economy has grown, competition among major shopping malls has become increasingly intense; coupled with factors such as poor management, sluggish consumer spending growth, and the impact of e-commerce, many shopping malls are facing the predicament of closure and bankruptcy.

According to relevant statistical data, more than 19% of the current 2,000 regional shopping malls have ultimately become what people refer to as “Dead Malls (Zombie Shopping Malls).”

To survive in a fiercely competitive market, major shopping mall developers are seeking new uses for existing spaces, such as adding educational, medical, and office facilities. Physicians believe that these vacant mall spaces offer an ideal opportunity to provide differentiated healthcare services that are more accessible and patient-centric.

Second, medical consultations at the Medical Mall are more affordable than those at hospitals.Under the Affordable Care Act (ACA) of the Obama healthcare reform, more than 10 million Americans gained health insurance coverage, which also drove up demand for convenient clinics. Some ACA plans have lower monthly premiums, but at the cost of higher out-of-pocket expenses for emergency room visits. Data from Maryland-based insurer CareFirst shows that in 2013, the average cost for treating a sore throat at an urgent care clinic was $94, whereas the same treatment in an emergency room cost $590.

Third, for shopping mall owners, emergency medical clinics are ideal tenants.Compared to traditional retail stores, clinics typically feature higher rents (approximately $25 per square foot), stronger creditworthiness, and longer lease terms.

Dave Henry, CEO of Kimco Realty, a mall operator based in New Hyde Park, New York, pointed out in an interview with Bloomberg News that urgent care clinics enjoy a strong reputation, often enabling them to pay higher rents (around $25 per square foot, equivalent to approximately 0.09 square meters) and tend to sign longer-term leases. In 2014, Kimco Realty signed leases with 40 medical clinics, an increase from 34 in 2013 and 27 in 2012. Henry stated, “For industry players like us who operate numerous shopping centers, this trend is encouraging.” Emergency medical clinics such as City Practice Group and Concentra are rapidly expanding at an annual growth rate of 20%, with many clinics beginning to occupy vacant retail spaces in shopping malls to meet growing customer demand.

Compared with the development path of Medical Malls abroad, China still faces at least the following four issues:

First, although major domestic real estate developers have increasingly entered the big health sector, few are genuinely developing medical commercial complexes.Most achieve this through mergers and acquisitions of companies across the upstream, midstream, and downstream segments of the healthcare industry, such as Yihua Health, or by partnering with foreign medical institutions to co-establish high-end hospitals.

Second, regulations on the approval of licenses for medical institutions vary across different regions in China.According to Sun Yinguang, founder of Hangzhou Pumai Medical, the company’s first clinic was established within The MixC shopping mall, where the approval process proved to be fraught with difficulties. Issues such as environmental pollution concerns, local resident consent, and healthcare zoning regulations had to be addressed.

Third, most medical service providers entering the Medical Mall are positioned in the high-end segment and are not integrated with the national health insurance system; their outpatient fees are higher than those of standard Grade 3A hospitals.Although there are many shoppers in malls, and the price of a single garment can range from hundreds to thousands of yuan, how many people are willing to pay the substantial consultation fees charged by such institutions? In other words, even if a shopping mall has heavy foot traffic, how many of these visitors can actually be converted into patients seeking medical care within the mall?

Fourth, has there been a shift in people’s awareness of seeking medical care?Most people, when ill, would rather spend the night queuing at a hospital to register than visit a nearby clinic, let alone a high-end medical institution located in a shopping mall.

Judging from the development trajectory of Medical Malls abroad, China’s Medical Mall sector is still in its infancy. Although Wanda Plaza plans to upgrade its healthcare offerings next year, it remains uncertain whether this model will gain widespread adoption. Even with strong capital interest and favorable policies, there is still a long road ahead.

Certainly, with the rise in health awareness and increased consumer spending power, people’s demand for healthcare is shifting from “treating existing diseases” to “preventing disease,” and from “passive medical care” to “proactive health management.”If the functions of Medical Mall are not focused on medical services that heavily overlap with hospital operations, such as treating diseases and saving lives, but instead target consumer healthcare, integrated medical and elderly care, and health management within the broader health ecosystem, there should be room for development.

Furthermore, from a global perspective, there are ten development models for the broad health industry: Medical Mall (health industry clusters), extension of traditional pharmaceuticals, tourism collaboration, commercial real estate partnerships, government cooperation, e-commerce, integration of medical and elderly care, comprehensive community health services, healthcare real estate, and health service organization models. Compared with the traditional health services sector, the broad health industry provides not merely products but holistic solutions for healthy living, thereby creating greater business opportunities. In this context, selecting optimal locations for Medical Malls and identifying precise service entry points are critically important.