China's Elderly Care Industry Shifts from Service Mandates to Market-Oriented Support: Emerging Growth Sectors in the New Policy Era

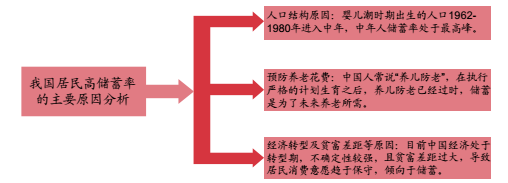

When discussing the elderly care industry, nearly all industry observers point to the trend of an aging society. Admittedly, changes in China’s demographic structure are one of the key factors driving the current growth in demand for elderly care services. However,VCBeat (WeChat ID: vcbeat)First, I would like to share another interesting perspective here—High savings rates provide a guarantee for the development of the elderly care industry.

According to research by Huarong Securities,The demographic transition driven by population aging has alleviated employment pressures, while the high savings rate among China’s elderly has provided capital for the upgrading of consumer services. The resulting increase in spending on life-oriented services has, to some extent, contributed to the “upgrading of the consumption structure.”

As of October 2016, the balance of household deposits in China had reached RMB 59.59 trillion. Following the release of the 2016 Global Savings Rankings, data showed that China’s household savings rate ranked third worldwide. In other words, in this sense,Elderly care services can be considered a form of “consumption upgrade.”

Analysis of the High Household Savings Rate in China (Source: Huarong Securities)

In light of the current state of elderly care services in China, the asset-heavy sector comprises over 40,000 various types of elderly care institutions, including social welfare institutes, nursing homes, senior apartments, and homes for the aged, offering more than 3.9 million beds. According to statistics from the Ministry of Civil Affairs, public elderly care institutions account for 72% of these 40,000-plus facilities, holding a distinct advantage.

Based on the development of overseas elderly care markets, the institutional care sector exhibits an olive-shaped distribution: the high-end segment accounts for 10%, the mid-range segment for 80%, and the low-end segment for approximately 10%. Following this structure, China’s elderly care market remains significantly underdeveloped. The future trajectory points toward private nursing homes and similar institutions comprising 80% of the market, with public institutions accounting for 20%, indicating substantial growth potential for the private sector.

The landscape of elderly care is gradually shifting, moving from a public-sector, service-oriented model to one driven by private capital aiming to build industrial scale.Since 2015, frequent releases of elderly care policies have led to a significant shift in the strategic position of elderly care within the industrial structure over just two years.

The 13th Five-Year Plan explicitly proposes to establish a multi-tiered elderly care service system with home-based care as the foundation, community services as the support, and institutional care as the supplement, while promoting the integration of medical and health services with elderly care.

On October 25, 2016, the Central Committee of the Communist Party of China and the State Council issued the “Outline of the ‘Healthy China 2030’ Plan.” As the action plan for advancing the construction of a Healthy China over the next 15 years, it places particular emphasis on developing and promoting the healthcare service system for the elderly, extending services to communities and households. Guided and incentivized by national policies, elder care is emerging as a new growth pole in the future development of the health and medical industry.

VCBeat has reviewed the relevant policies concerning the elderly care industry in recent years and, through analysis and summarization, aims to present a clear overview of the current policy landscape for readers’ reference.

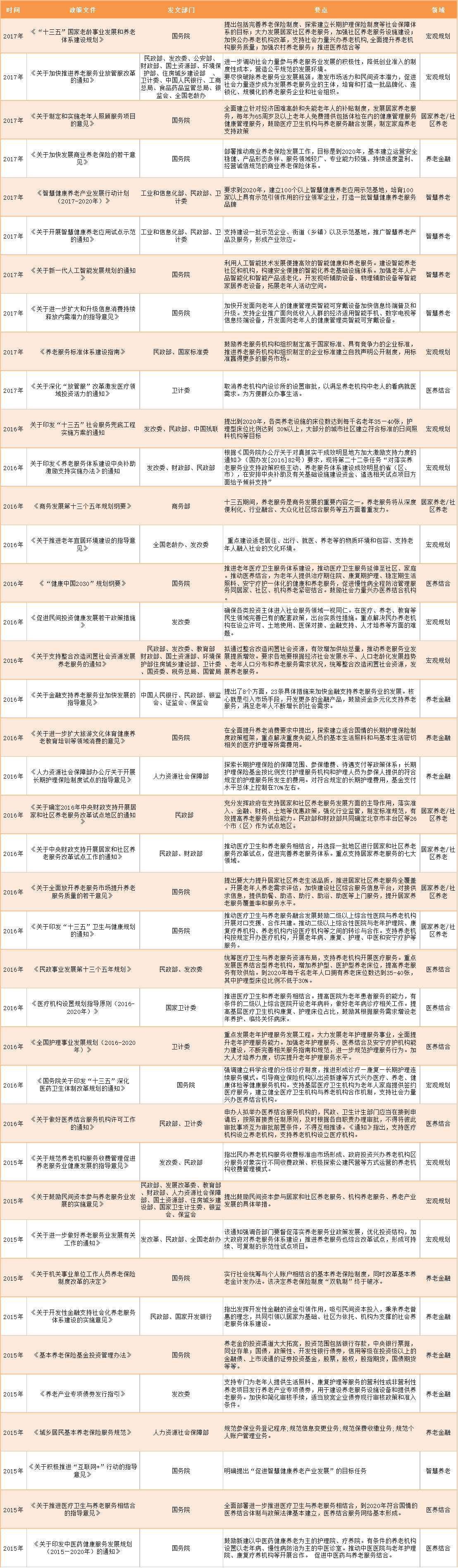

Analysis of Elderly Care-Related Policies from 2015 to 2017

(*Based on the scope of the inventory, heavy-asset policies such as PPP elderly care and elderly care real estate are excluded. The table is lengthy [40 items in total], with detailed analysis provided below.)

Timeline: 2015–2017, From Market Pivot to Targeted Breakthroughs

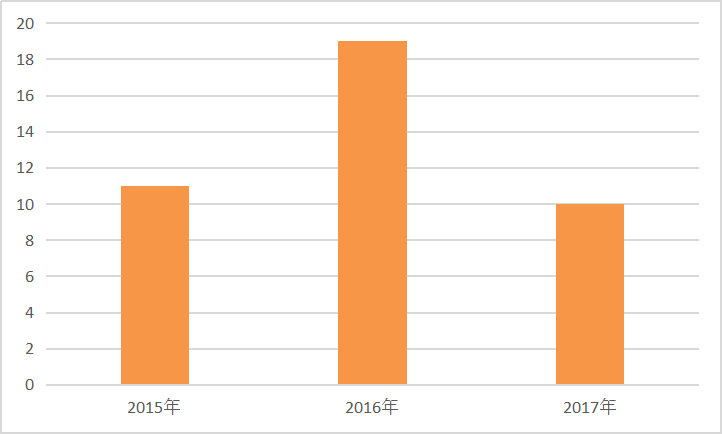

Number of Policies Issued by Year

An examination of elderly care policies introduced in recent years reveals a prominent feature, namelyPolicies themselves are undergoing a transformation. In the past, policy orientation leaned more toward social policies that directly served the elderly. Since 2015, policies have begun to shift toward supporting industry development and facilitating market transformation.. Initiatives such as pilot programs for long-term care insurance, the integration of medical and elderly care services, and financial sector involvement are all aimed at supporting the market. Issues concerning the quality of the elderly care service industry, along with policies such as fully liberalizing the elderly care service market, promoting the convergence of primary, secondary, and tertiary industries, and advancing integrated development related to new rural construction, have all been elevated to the national level.

2016 was the year in which China introduced the largest number and most comprehensive policies for the elderly care service industry. According to incomplete statistics from VCBeat, 19 central-level policies were issued, far exceeding the numbers in 2015 and 2017. The policy framework was relatively dense, and the role of market forces became increasingly prominent.

Furthermore, in 2016, President Xi Jinping issued four direct instructions and delivered speeches containing content related to elderly care, marking the highest frequency in a single year. These policies influenced capital flows, industrial trends, and the direction of future supply-side structural reforms in 2016, 2017, and even 2018.

Beyond the policies listed in the article, various provinces and municipalities have also formulated corresponding implementation documents based on the requirements of national policies related to the elderly care industry, taking into account local actual needs for elderly care, market characteristics, and other factors.

Following the joint issuance of the Notice on Accelerating the Reform of Streamlining Administration, Delegating Power, and Improving Services in the Elderly Care Service Industry by thirteen ministries and commissions including the State Council in February 2017, thirteen departments in Hunan Province, including the Provincial Development and Reform Commission and the Department of Civil Affairs, promptly released the Implementation Opinions on Accelerating the Reform of Streamlining Administration, Delegating Power, and Improving Services in the Elderly Care Service Industry in August. This initiative aimed to remove bottlenecks in the elderly care service industry by simplifying administrative procedures and strengthening supervision. Furthermore, in September, eleven departments in Hangzhou, including the Municipal Civil Affairs Bureau, also issued the Notice on Accelerating the Reform of Streamlining Administration, Delegating Power, and Improving Services in the City’s Elderly Care Service Industry.

From central implementation to various provinces and cities, from this perspective, 2017 was the year of concentrated implementation of elderly care policies.. Moreover, in 2017, with the penetration and development of the internet in the lives of the elderly, new changes will occur in their lifestyles and expenditure structures, and new models in the elderly care sector, such as smart elderly care and sojourn-based elderly care, have come into public view.

Issuing Authorities: Led by the State Council, with an increasing number of involved departments

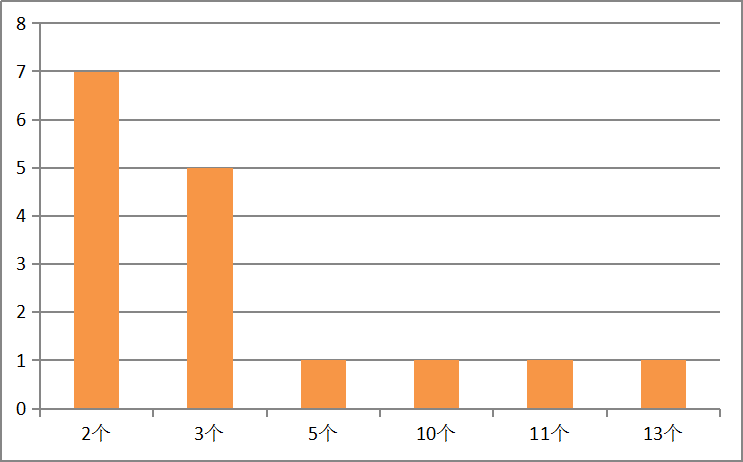

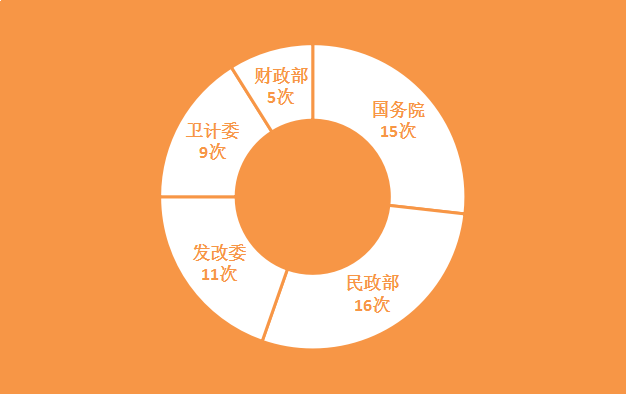

Over the past three years, policy effects have been comprehensive, shifting from single-department initiatives to coordinated multi-agency efforts—a phenomenon rarely seen in elderly care policies of previous years. Among the aforementioned 40 policies, 15 were jointly issued by multiple ministries and commissions.Elderly care involves not only the civil affairs department but also finance, taxation, development and reform, banking, health and family planning, human resources and social security, housing and urban-rural development, education, commerce, and other sectors.

Statistics on the Number of Departments Involved in Jointly Issued Documents

Top 5 Publishing Departments by Frequency of Publications

(*Involves joint issuance, with departments appearing multiple times)

Among these, documents such as the “Action Plan for the Development of the Smart Health and Elderly Care Industry (2017–2020)” and the “Notice on Launching Pilot Demonstrations of Smart Health and Elderly Care Applications,” which promote development from a macro level to targeted points within a specific field and exert efforts across multiple stages, can also be referred to as policy “packages.”

In addition to having the highest number of joint publications, involving up to 13 relevant ministerial-level departments. The issuance of typical macro-level planning outlines, such as the "Healthy China 2030" Planning Outline, the 13th Five-Year Plan for Commerce Development, and the Implementation Plan for the Social Service Safety Net Project during the 13th Five-Year Plan period, also involves macro-level planning goal formulation by departments including the Ministry of Commerce and the National Development and Reform Commission, in addition to direct administrative bodies such as the National Health and Family Planning Commission and the State Council. In these macro-level plans, elderly care is included among the core development objectives.

Policy formulation involves not only a single industry but, more importantly, inter-departmental and regional collaboration, entailing the coordinated and comprehensive development of the entire economy and society, with some aspects even extending to the advancement of cultural undertakings.The “Opinions on Further Expanding Consumption in Tourism, Culture, Sports, Health, Elderly Care, Education and Training, and Other Sectors,” issued by the State Council in 2016, covered multiple areas including tourism, culture, and elderly care.

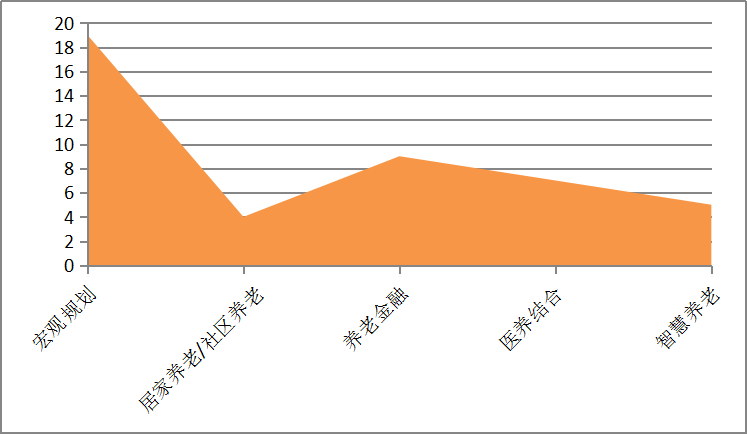

Policy Coverage of Subsectors

In this review, apart from macro-planning categories, which are most frequently addressed by policies, the remaining four niche sectors in elderly care are all asset-light models. Capital-intensive elderly care real estate projects with long construction cycles, institutional elderly care, and PPP projects are excluded.

Statistical Classification of Elderly Care Policies

If the period from 2011 to 2014 marked the initial stage of China’s elderly care policy framework, characterized by overarching guidelines, then the policy orientation primarily focused on rational market layout and stimulating corporate vitality. The central theme was the establishment of a multi-tiered elderly care service system with home-based care as the foundation, community services as the support, and institutional care as the supplement.Thus, the trend from 2015 to the present has been that elderly care has entered a phase of specialization and formal implementation.However, as the profit model for China’s elderly care industry is still being explored, the high entry barrier for asset-heavy elderly care services—such as establishing nursing homes and developing senior housing projects—requires capital outlays that are beyond the reach of many small and medium-sized enterprises.

Among the aforementioned policies concerning asset-light elderly care, four key subsectors are primarily addressed: home- and community-based elderly care, elderly care finance, integration of medical and elderly care services, and smart elderly care. In terms of volume, policies related to elderly care finance are the most numerous, whereas relatively few direct guidance documents have been issued for home- and community-based elderly care.

However, based on the author’s observations, many macro-level policies—particularly those concerning the integration of medical and elderly care, rehabilitative nursing, and even long-term care insurance—primarily advocate for small-scale, lightweight elderly care models centered on home- and community-based settings.As emphasized in the “Outline of the ‘Healthy China 2030’ Planning Program,” there is a strong push to extend medical and healthcare services into communities and households. The “13th Five-Year Plan for Commerce” also highlights that elderly care services will focus on five key areas: deepening convenience, industry integration, and mass-oriented comprehensive community services, among others. Furthermore, the “Notice on Issuing the Implementation Plan for the Social Service Safety Net Project during the 13th Five-Year Plan Period” explicitly establishes the construction of standardized day-care facilities in most urban communities as one of the goals of this social service safety net initiative. Therefore, from this perspective, home- and community-based elderly care has emerged as the most prevalent subsector.

Interpretation of Policy Trends by Year

2015

Key Policies:"Implementation Opinions on Encouraging Private Capital to Participate in the Development of the Elderly Care Service Industry," "Guiding Opinions on Promoting the Integration of Medical and Health Services with Elderly Care Services"

Keywords:Private Capital Market Access; In-House Medical Institutions within Elderly Care Facilities

Key Interpretation:Innovation in investment and financing mechanisms for elderly care services, increased financial support, expanded channels for investment and financing in the elderly care service industry, and meeting the credit needs of elderly care institutions reflect the state’s support for private capital participation in the elderly care sector.

In the past, traditional public institutions were prohibited from obtaining loans. Private non-enterprise units—such as private nursing homes and service organizations for persons with disabilities—were classified under the category of non-governmental organizations (NGOs). Consequently, asset-light elderly care development also faced significant challenges. To foster growth in social capital, it is imperative to liberalize market access for private capital.

Furthermore, due to the shortage of hospital beds, medical and nursing care remain a significant challenge. Some elderly individuals even engage in “bed-blocking for elderly care” by staying in hospitals to meet their medical needs, thereby occupying medical resources and creating a burden. In 2015, the State Council issued the Guiding Opinions on Promoting the Integration of Medical and Elderly Care Services, calling for comprehensive deployment to further advance the integration of medical and elderly care services. By 2020, a system and policy framework for integrated medical and elderly care suited to China’s national conditions were to be basically established, and a service network for such integrated care was to take shape.

This policy directly and explicitly underscores the importance of the “integration of medical and elderly care” model, while also signaling that detailed legal regulations and specific implementation systems will be introduced in the next phase. In practice, the integration of medical and elderly care has already been achieved in many areas, including community-based elderly care, home nursing, and smart elderly care.

2016

Key Policies:"13th Five-Year Plan for the Development of Civil Affairs," "13th Five-Year Plan for Health and Wellness," and "Outline of the 'Healthy China 2030' Plan"

Keywords:"Ensure Basic Coverage, Establish Systems"

Core Interpretation:In 2016, both the national government and provincial and municipal authorities attached great importance to elderly care services. Most macro-level plans issued at the national level were released in this year, as 2016 marked the inaugural year of the 13th Five-Year Plan period; thus, policy documents first outlined the development goals for various initiatives over the subsequent five years.

Furthermore, provinces and municipalities across the country have successively issued detailed implementation rules for these policies, continuously improving the investment environment and industrial support measures for China’s elderly care industry to meet the growing demand for elderly care services.The General Office of the State Council and relevant ministries and commissions of the central government are shifting their focus to the elderly care service industry,Successively issued documents such as the “Guiding Opinions on Financial Support for Accelerating the Development of the Elderly Care Service Industry,” the “Notice on Properly Handling Licensing for Medical-Nursing Combined Service Institutions,” and the “Guiding Opinions on Launching Pilot Programs for the Long-Term Care Insurance System.” These documents, issued individually or jointly by relevant ministries and commissions, constitute the most direct policy instruments in the elderly care service industry, providing guidance and indicating emerging trends.

This year, policy initiatives covered areas including but not limited to: financial support for the elderly care service industry; policies integrating medical and elderly care; licensing of service institutions; pilot programs for long-term care insurance; the elderly consumer market; private capital participation in the elderly care service industry; central fiscal support for home-based and community-based elderly care; integration and repurposing of idle social resources to develop elderly care services; comprehensive liberalization of the elderly care service market to enhance service quality; consumption in sectors such as tourism, culture, sports, health, elderly care, education, and training; and regulatory reforms (decentralization, regulation, and service optimization) in the elderly care service industry.

Nineteen policies, either directly or indirectly addressing direct elderly care services and related industrial policies, constitute a crucial component of China’s top-level design for elderly care.The 2016 policies were comprehensive, forming a “coordinated package” with a depth and breadth unmatched by previous policy initiatives. Thus, 2016 marked a year of intensive rollout and synergistic implementation of elderly care policies, representing a significant shift.

2017–Present

Key Policies:"Notice on Accelerating the Reform of Delegating Power, Improving Regulation, and Upgrading Services in the Elderly Care Service Industry", "13th Five-Year National Plan for the Development of Aging Causes and the Construction of the Elderly Care System", "Action Plan for the Development of the Smart Health and Elderly Care Industry (2017–2020)"

Keywords:"Streamlining Administration, Delegating Power, and Improving Services"; Smart Elderly Care

Key Interpretation:“Fang Guan Fu” refers to streamlining administration and delegating power, combining regulation with oversight, and optimizing services. It requires the elderly care service industry to intensify efforts in “delegation,” strengthen regulatory “capacity,” and enhance the “quality” of services. According to Tang Jun, a researcher at the Chinese Academy of Social Sciences,To accelerate the development of the elderly care service industry, it is necessary to shift from the previous “threshold-based management” and the subsequent “accountability-based management” to “process-based management.” The reform of decentralization, regulation, and service (Fang-Guan-Fu) shifts the focus of management to the process management of elderly care service operations.

Meanwhile, the national strategy for smart elderly care fully leverages the rapid advancements in big data and informatization, aiming to achieve efficient and high-quality elderly care management.It is required that by 2020, a smart health and elderly care industrial system covering the entire life cycle be basically established. This initiative will facilitate the widespread adoption of smart health and elderly care services, such as health management and home-based elderly care, and significantly enhance the quality and efficiency of these services. Meanwhile, formulating standards for smart health and elderly care products and services will help strengthen information security safeguards.

Strategic Direction:2017 was a crucial year for implementing the 13th Five-Year Plan and a year for deepening supply-side structural reform. In Premier Li Keqiang’s Government Work Report, elderly care was mentioned six times. The overall shortage of elderly care beds alongside the significant underutilization of existing ones constitutes a severe structural imbalance on the supply side.Therefore, supply-side reform in the elderly care sector will be a key direction for the development of eldercare services in 2017.

Elderly Care Policies Highlight Three Major Commonalities

A review of elderly care policies over the past three years reveals that, despite ongoing changes, they share many common attributes in their orientation and underlying principles:

Lowering Market Entry Barriers for the Elderly Care Service Industry

To change the current situation in which public elderly care institutions dominate the market, policies aimed at lowering barriers to entry into the elderly care sector—such as allowing private capital access and simplifying approval procedures—have been continuously introduced. Among the 40 elderly-care-related policies compiled by VCBeat across various levels, 14 include measures that encourage private capital participation, lower entry thresholds, and streamline approval processes, thereby directly or indirectly promoting private investment in the elderly care industry.

Among these, the “Implementation Opinions on Encouraging Private Capital to Participate in the Development of the Elderly Care Services Industry,” jointly issued in 2015 by ten ministries and commissions including the Ministry of Civil Affairs, the National Development and Reform Commission, and the Ministry of Education, explicitly set forth specific measures to encourage private capital participation in home- and community-based elderly care services, institutional elderly care services, and the development of the elderly care industry. This policy represents the most direct measure to facilitate market access for private capital.To balance the current dominance of public institutions in elderly care, investment approaches such as encouraging private capital participation and adopting public-private partnership (PPP) models are being gradually promoted.

Strengthen Market Attributes

If the senior care industry is viewed as a service sector, it requires greater leverage from market forces. The diverse needs of 230 million elderly people in terms of clothing, food, housing, and transportation constitute a vast market. Previously, the government played more of a planning role in elder care, even serving as the primary provider of elderly care services, with over 90% of elderly care institutions being public. Government subsidies and fiscal support have been substantial. However, as consumption structures continue to upgrade—including the rise in household savings rates mentioned earlier—relying solely on public services is clearly insufficient to meet the enormous demand for elder care.

Relying solely on government regulation would represent a regression to the mindset of a planned economy. Therefore, under current circumstances, the government should focus more on leveraging the advantages of the market, with its primary orientation being to ensure basic livelihood, basic medical care, and basic long-term care for the elderly, while establishing a social elderly care service system.

Within the elderly care system, market forces should play a pivotal role; rather than relying solely on government subsidies, elderly care should be positioned as both a service and a form of consumption.The government is undergoing a transformation, and the direction of elderly care will also change.Therefore, the current policy emphasis on improving the quality of elderly care services has effectively shifted to a behind-the-scenes role, focusing more on regulating, cultivating and supporting, and guiding the market.

The Elderly Care Service Industry Becomes Mainstream

As healthcare service reform policies are gradually implemented, elderly care service enterprises have become promising players in the senior care sector. Driven by both urgent demand and policy incentives, the elderly care industry is poised for significant growth opportunities.

Previously, Cheng Haijun, Director and Professor at the Training Center of the Ministry of Civil Affairs and the Institute of Civil Affairs Policy and Theory, expressed the view that during the “12th Five-Year Plan” period, policy resources were predominantly directed toward institutional care, with subsidies focused primarily on infrastructure construction—namely, “bricks, beds, and staff.” This approach was favored because policies targeting institutions yield immediate, visible results.

Following the advent of the 13th Five-Year Plan, home-based elderly care services, along with the cultivation of the related market and industry, have gained significant momentum. Influenced by traditional Chinese culture and national conditions, the vast majority of elderly individuals in China continue to age in place. In fact, home-based care remains the predominant model for elderly care in most mainstream countries as well.Therefore, in light of the current policy priorities, improving the quality of elderly care services, with a specific focus on implementing home-based care and integrated medical and elderly care services, has become the mainstream approach.

Three Major Industrial Bottlenecks in the Elderly Care Sector

Three Major Bottlenecks

Barriers to Capital Entry

A significant amount of private capital is eager to enter the elderly care industry, yet many potential investors remain hesitant. The fundamental reasons are twofold: First, China currently lacks a universal pension insurance system comparable to its universal medical insurance scheme. Second, it is difficult for governments at all levels in China to provide substantial financial support to privately-run elderly care institutions from their inception, as seen in Europe and Japan. Consequently, these privately-run facilities face numerous challenges throughout the entire process, from land acquisition and opening to daily operations.

Furthermore, Wu Danxing, an expert in the elderly care industry and a member of the Expert Committee on Elderly Care Services under the Ministry of Civil Affairs, pointed out that unclear mechanisms for investment entry and exit have led to hesitation and a wait-and-see attitude among enterprises. Regarding approval mechanisms, invested capital is constrained by policies and institutional frameworks; if the financial market remains closed, capital will be unwilling to enter.

Lack of a Mature Profit Model

Profitability remains a major challenge plaguing elderly care enterprises, as high upfront investment and slow payback periods are prominent characteristics of such investments. Consequently, most companies operating in the elderly health sector are currently running at a loss due to the lack of mature business models. For enterprises establishing elderly care institutions or providing related services, the approval process is relatively complex, requiring submission of feasibility studies, proof of fixed premises, funding sources, environmental impact assessments, and other documentation, while also involving coordination with national and local civil affairs, industry and commerce, and tax authorities.

Shortage of Professional Talent

As public legal awareness grows and service standards improve, extensive, non-specialized medical care is no longer suitable for the current development of China’s elderly care sector. In the eyes of many entrepreneurs in this field, establishing a comprehensive risk assessment mechanism is a top priority. Previously, an entrepreneur in the elderly care sector told reporters, “In people-to-people services, uncontrollable factors are prone to arise; what matters most is the establishment of professional expertise and standardized processes.”

In ChinaThe elderly care workforce is currently facing the so-called "four lows": low educational attainment and professional competence, low level of formalization, low compensation and benefits, and low social status.The total number of caregivers falls far short of the demand in an aging society, with a shortage of at least several million; the scarcity of caregivers in rural and grassroots areas is even more severe.

Can policies solve the problem?

The effectiveness of public policy often does not depend on the good intentions of policymakers. Reality shows that society’s sensitivity to elderly care policies is not as high as expected, and policy benefits have not been effectively responded to when a mature service system has not yet been established.

For many entrepreneurs seeking policy guidance, what they desire is not merely an understanding of trends, but more importantly, direct guidance and concrete measures, or specific provisions related to industry standardization, including the implementation of regulatory measures. While policies reflect strategic direction and demonstrate governmental resolve, their primary role is to address existing problems. Therefore, whether current elderly care policies can fully resolve the prevailing bottlenecks remains a question with an answer less optimistic than we might have imagined.

① Addressing Barriers to Capital Entry

In October 2016, the Central Leading Group for Comprehensively Deepening Reforms reviewed and approved the “Several Opinions on Fully Opening the Elderly Care Service Market and Improving the Quality of Elderly Care Services,” requiring lowered market entry barriers to guide social capital into the elderly care service industry. Three days later, the State Council’s executive meeting determined policy measures to further expand domestic consumption, calling for the removal of institutional and mechanistic obstacles constraining consumption in sectors such as elderly care, education, and sports.

Currently, policies aimed at lowering entry barriers for elderly care services, encouraging private capital investment, and streamlining approval processes are being introduced with increasing frequency. These measures primarily seek to stimulate market vitality, leverage the government’s guiding role, and promote prosperity in the elderly care market.

Meanwhile, the concentrated development of PPP projects in recent years has also contributed to the diversification of funding channels in the elderly care sector. Hence, there is a view that the elderly care market has ushered in its “spring” in recent years.

② Addressing Issues Related to the Profit Model

China has not yet developed a large-scale market for elderly care services. The formation of a market typically begins with demand, which then drives supply; under the influence of the price mechanism, resources are allocated through the process of moving toward equilibrium. As a market where “services” constitute the product, the elderly care sector is clearly still in its developmental stage.

On one hand, potential buyers have limited purchasing power; on the other, there is a lack of supply for essential, inelastic healthcare services, while the limited available supply exceeds the affordability of the general population. In such circumstances, policies aimed at broadly stimulating supply often prove ineffective.

In China, the elderly and their children are primarily concerned with nursing and caregiving services, which exhibit strong inelastic demand. Consequently, current policies are increasingly oriented toward home-based care and nursing services, emphasizing supply-side guidance while simultaneously focusing on enhancing the purchasing power of the elderly.

③ Addressing Talent Issues

The author has observed that recent documents issued by relevant ministries and commissions have scarcely addressed support for the training and education of personnel in private elderly care services. This clearly represents a policy gap. Without large-scale, standardized training and education for elderly care professionals, it will be impossible to fundamentally reverse the “four lows” situation, and the elderly care sector will struggle to achieve significant development. In this regard, government resources are inherently limited, making reliance on societal forces essential. For many years, although there have been numerous capable individuals in the private sector dedicated to cultivating elderly care talent, they have been hampered by the lack of effective platforms, ultimately forcing them to seek careers in other fields.

Currently, although governments at all levels and across various regions have recognized the importance of supporting private elderly care services, they have not yet attached sufficient importance to the cultivation of personnel for private elderly care institutions or to the development of related educational initiatives. This gap represents both a deficiency and an opportunity. While no mature system has yet emerged, it may be possible in the future to draw on the mechanism of government procurement of elderly care services by piloting the purchase of training and educational services for personnel in private elderly care institutions.

Analysis of Investment Opportunities in Potential Sub-sectors

In physics, there is a principle known as Pascal’s Law, which originally refers to the physical formula for pressure: Pressure = Force / Area. This implies that applying the greatest force, resources, and investment to a small area can generate the highest pressure. When this pressure reaches a critical state, it results in rupture, referred to as the critical bursting point. Gong Yu, Director at iQIYI, termed this concept the “Blockbuster Pascal’s Law” and explained it as follows: All blockbusters emerge from innovative areas that have previously received no attention.

In narrower vertical niches, allocating greater resources and exerting more pressure creates higher intensity, eventually reaching a critical tipping point that triggers explosive growth. This principle is universally applicable to the elderly care sector or any subsector within an industry. In other words, pursuing elderly care services should not involve overly “comprehensive development.”

Reviewing elderly care policies from 2015 to the present, certain emerging fields and adjustments to the existing elderly care service structure are poised to become “blockbuster” areas in the next phase of development:

With the introduction of a series of national action plans for smart elderly care and the concentrated implementation of pilot programs, the achievements of smart elderly care will become an indispensable tool for the offline elderly care industry to provide assistive services.

The Action Plan points out that the smart health and elderly care ecosystem, formed by leveraging next-generation information technology products such as the Internet of Things (IoT), cloud computing, big data, and intelligent hardware, can achieve effective integration and optimized allocation of individuals, families, communities, institutions, and health and elderly care resources. This will drive the intelligent upgrading of health and elderly care services and enhance the quality, efficiency, and overall performance of these services.

Following the further emphasis on the supportive role of artificial intelligence (AI) technology in elderly care outlined in the "Notice on the Development Plan for the New Generation of Artificial Intelligence," developing convenient and efficient smart health and elderly care services has become the goal of new-type elderly care enterprises, particularly internet-based elderly care companies.

Currently proposed smart elderly care products include several major categories:

· Key Focus Areas for Health Management Wearable Devices: Health bands, health watches, and wearable monitoring devices. Emphasis is placed on continuous monitoring and early warning management of health status indicators such as blood pressure, blood glucose, blood oxygen, and electrocardiogram (ECG).

· Key Focus of Portable Health Monitoring Devices: Integrated and standalone smart health monitoring toolkits for homes, family physicians, and community medical institutions. Emphasis is placed on real-time monitoring of various physiological indicators in home and mobile scenarios to facilitate remote health management.

· Key Focus of Self-Service Health Screening Devices: Self-service intelligent health screening devices designed for community institutions and public spaces. These devices emphasize convenient, on-demand, and accessible basic health status monitoring anytime and anywhere, thereby enhancing users’ ability to manage their own health.

· Key Focus Areas for Smart Elderly Care Monitoring Devices: Intelligent monitoring, rehabilitation, and caregiving equipment—such as smart wheelchairs and monitored beds—for both home-based and institutional elderly care, along with high-precision indoor/outdoor positioning terminals designed to prevent wandering in patients with dementia. Emphasis is placed on enhancing seniors’ autonomy in self-care and self-management, thereby improving the utilization efficiency of social and familial elderly care resources.

· Key Focus of Home Service Robots: Intelligent service robots equipped with functions such as household chores, emotional companionship, entertainment and leisure, disability assistance, and security monitoring, emphasizing the enhancement of seniors’ quality of life through modern home entertainment.

· Health and Elderly Care Data Management and Service System: Leverage information technologies such as the Internet, Internet of Things (IoT), and big data to promote the integration of smart health and elderly care application systems, and interface with medical institutions and elderly care service resources at all levels; develop health and elderly care data management and intelligent analysis systems to achieve intelligent interpretation, analysis, and processing of big data in health and elderly care.

As the quality of elderly care services continues to improve, elderly care apps, wearable devices, health and elderly care data management and service systems for day care institutions, intelligent elderly care monitoring devices, and POCT devices will constitute a significant demand side in the smart elderly care product sector.

“Chinese people have a particularly strong sense of family values. This cultural tradition and the current national context determine that only a minority are willing to reside in institutional care facilities; the vast majority rely on a combination of family-based and community-based elderly care.” Li Jiang, a member of the Internal and Judicial Affairs Committee of the National People’s Congress, believes that addressing the challenges of “elderly care with Chinese characteristics” requires solutions tailored to the Chinese context.“The ‘4-2-1’ family structure is becoming increasingly common, severely impacting the traditional model of family-based elderly care. This model is struggling to cope with the immense pressure of aging care, leading to a growing demand among the elderly for community-based elderly care services.”

In 2015, the State Council issued a series of documents to promote the integration of medical care and elderly care, as well as the upgrading of consumption structures. The 13th Five-Year Plan placed significant emphasis on the development of the elderly care industry system. The new business model of “integration of medical and elderly care” was mentioned for the first time in the Government Work Report, which specifically included the phrase “business models integrating medical and elderly care.” Currently, three primary consumption models characterize this integration: a care-dominant continuous care model; a care-dominant health recuperation model; and a care-dominant health-oriented community model with family ties. Therefore, the integration of medical and elderly care is closely intertwined with home-based and community-based elderly care models.

Among the 40 policies compiled by VCBeat, six directly target the home- and community-based elderly care segment, while six others indirectly advocate for home-based care as the primary model of elderly support. Driven by the growing demand for aging in place and further bolstered by these policy initiatives, the supply and demand for community-based home elderly care services are poised for explosive growth over the next three years.

In a previous analysis of the current state of the integrated medical and elderly care industry, VCBeat pointed out that community-based care models—such as day care centers and elderly care homes providing “doorstep” services—can offer seniors basic services including daily living assistance, rehabilitation therapy, emotional support, and emergency aid, as well as additional services such as entertainment, education, and social engagement. As elderly care gradually shifts toward marketization, various model explorations have emerged, including public-private partnerships (PPP), government-funded leasing, and private construction with community operation. Among these, government operational subsidies or the provision of venues at low cost or even free of charge help operators maintain a more “asset-light” structure.Through continuous exploration of the needs of the elderly, and by leveraging resources such as in-home services, mutual aid among seniors, and platform-based operations of diverse service providers, community-based care is gradually moving away from the traditional mindset that it is “unprofitable.”(See details《The Integrated Medical and Elderly Care Industry: Surpassing One Trillion Yuan in 2021, Where Do the Opportunities Lie in This “Blue Ocean” That Is Also a “Sea of Bitterness”?》)

Street-level community health service centers, township health centers, and community clinics, as primary healthcare institutions, can form natural partnerships with nearby community elderly care facilities. These collaborations may take various forms, such as dispatching medical experts to communities and establishing green channels for expedited medical consultations for the elderly. Conversely, primary healthcare institutions may also set up community-based elderly care points. Through such cooperation, community elderly care services gain access to professional medical support, while facilitating the integration and optimization of resources within community healthcare institutions, thereby improving bed turnover rates.

Meanwhile, as the long-term care insurance system is improved, demand for nursing care services for disabled and semi-disabled elderly individuals will rise accordingly. Small-scale, chain-operated, and specialized service providers, as well as community-embedded micro-institutions, are likely to become the mainstream models of elderly care in the future. The currently visible path involves serving elderly populations with essential community-based needs, leveraging professional service teams, and implementing chain operations through brand building.

Based on the experience of developed countries, financial and fiscal policies have played a significant role in supporting the development of the elderly care service industry and providing personal retirement services, such as Japan’s Long-Term Care Insurance (LTCI), America’s commercial long-term care insurance, and reverse mortgages.China may still urgently require supporting laws and policies to facilitate the implementation of pension finance policies; the subsequent rollout of relevant measures will promote further development in this sector.

Regarding commercial pension insurance products, there is a significant gap in both penetration and depth in China compared to developed countries. As the world’s second-largest economy, China needs to narrow this gap. In the process of closing it, bank-affiliated financial institutions, insurance companies, investment management firms, and financial institutions across society will face countless business opportunities.

However, this sector currently remains largely unregulated, and elderly individuals are often the primary targets of fraudulent schemes such as telecom fraud. Beyond pension fund management and commercial insurance—areas involving state or institutional capital—companies dedicated to safeguarding the financial security of seniors have long emerged in developed countries’ retirement finance models. Firms like True Link, which offer solutions for elderly financial safety, may provide valuable insights for future entrepreneurs and enterprises entering China’s retirement finance sector.

From VCBeat’s observations, we have encountered entrepreneurs who are eager to enter the elderly care sector but are uncertain about how to proceed, which entry point to choose, and what specific industry regulations apply. This article is inspired by such challenges. Therefore, now that the promising prospects of the elderly care industry have been widely recognized in recent years, the next key focus should be on introducing regulatory measures tailored to various sub-sectors and establishing standards for the elderly care field. Only in this way can potential service quality issues be avoided.

Therefore, we will continue to closely monitor the elderly care sector, a field with rigid demand, and analyze emerging growth drivers. We welcome readers to share their questions or perspectives on elderly care with us. Working in isolation is not a viable approach; we look forward to engaging in dialogue and discussion with our readers to offer potential insights for this evolving and exploratory domain.