Why Country Garden-Originated Real Estate Giant ThaiHop Group Is Passionate About Healthcare: A $50 Billion Bet Over Five Years

In recent years, the convergence of real estate and healthcare has become a hot topic in both industries. From Wanda Group, which planned to invest RMB 144 billion to establish a large health group and deploy its medical services through an “asset-light” model, to Vanke, which has deeply cultivated senior living real estate, and Yihua Real Estate, which has undergone a comprehensive transformation, real estate companies are showing increasing enthusiasm and making ever-larger investments in the healthcare sector, signaling a potential reshaping of the healthcare landscape.

Amid the wave of real estate companies transforming or expanding into healthcare, Taihe Group—a top-50 listed real estate developer that originated in Fujian Province and specializes in high-end residential and commercial properties—has also demonstrated strong enthusiasm for the medical sector. Its founder, Huang Qisen, even declared, “We will invest RMB 50 billion in healthcare within five years; it is acceptable to subsidize this venture with profits from our real estate business,” underscoring the company’s resolve.

But how exactly to do it still depends on "insiders" to actually operate. Taihe Group has hired Pan Hong, a professional manager who previously worked at Bayer and China Resources, as the general manager of the medical group, fully responsible for medical business.

Recently, VCBeat (WeChat ID: vcbeat) conducted an exclusive interview with Pan Hong, reviewing Taithe Group’s healthcare layout and providing a detailed explanation of its “real estate + healthcare” strategy.

A Multi-Billion Real Estate Developer Originating from Eastern Fujian

Tahoe Group was founded by Huang Qisen in 1996. He attended Fuzhou No. 1 High School, entered university at the age of 15 majoring in architectural engineering, and joined the Fujian Branch of China Construction Bank after graduation. In 1996, he resigned to venture into the private sector, entering the real estate industry.

Fuzhou, also known as the “City of Banyans” and abbreviated as “Rong,” is where Taihe Group originated. After its establishment, Taihe launched the landmark project “Tianyuan Villa” in 1999, which rapidly gained prominence and established Taihe as a leading real estate brand in Fuzhou’s housing market. Subsequently, Taihe rolled out additional branded projects such as “Tianyuan·Meishu Guan” and “Tianyuan·Hetang Yueshe,” all of which were well received by Fuzhou’s property buyers. At that time, any residential development bearing the “Tianyuan” name could command a price premium of at least 10% per square meter compared to other brands.

Around the turn of the millennium, when the “Tianyuan” brand was at its peak, Huang Qisen decided to expand northward. He stated, “No matter how well you do in Fuzhou, you are merely a ‘local model worker’; but in Beijing, success makes you a ‘national model worker.’” Taihe acquired over 3,500 mu of land along the Tongzhou Riverbank. After two years of development, the “Courtyards on the Canal Bank” project achieved remarkable success, becoming one of the most renowned high-end residential developments in China at the time and setting a record by increasing the total project value from RMB 600 million to RMB 8 billion.

Subsequently, Taihe pursued a dual-track development strategy in Beijing and Fuzhou, achieving stable high returns through its high-end and commercial real estate projects. In 2008, Taihe Group announced its plan to go public via a reverse merger with ST Sannong. After a year and a half of efforts, the latter completed its shareholding reform in July 2009, marking Taihe’s successful backdoor listing.

Following the successful shareholding reform, Huang Qisen stated publicly that Fujian Sannong was located in the center of Sanming City, Fujian Province, and possessed over 300 mu of industrial land. Prior to participating in the restructuring, the Sanming State-owned Assets Supervision and Administration Commission (SASAC) had held negotiations with more than ten companies. However, many of these companies sought to “gain something for nothing,” primarily targeting the 300-plus mu of prime land. In contrast, Taihe and the government reached an immediate consensus. The reason was that Taihe did not seek the 300-plus mu of land. “Business operations require foresight; one should not be overly concerned with gains or losses in any single battle or territory.”

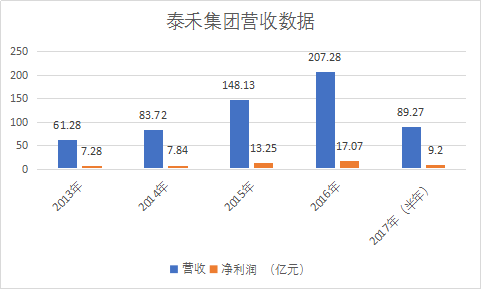

From the financial data, Taihe's performance surged after the backdoor listing. In 2015, its revenue exceeded RMB 10 billion for the first time, with net profit surpassing RMB 1 billion. In 2016, revenue reached RMB 20.728 billion, and in the first half of this year, revenue was RMB 8.927 billion, with a net profit of RMB 920 million.

Tahoe Group’s interim report disclosed that its high-end residential products, centered on the core brands Tahoe “Courtyard” and “Grand Courtyard” series, and its commercial real estate products, centered on the core brands “Tahoe Plaza,” “Tahoe New World,” and “Central Plaza,” have established considerable brand influence across China.

Taihe adheres to the real estate strategic layout of “being rooted in Fujian and deeply cultivating first-tier cities.” Its projects are primarily concentrated in major economically developed regions, including the Beijing-Tianjin-Hebei region centered on Beijing, the Yangtze River Delta centered on Shanghai, the Pearl River Delta centered on Guangzhou and Shenzhen, as well as Fuzhou and Xiamen in Fujian Province, while gradually extending its reach to provincial capitals and core second-tier cities. During the reporting period, the company entered several hot second-tier provincial capital cities, including Zhengzhou, Jinan, Nanchang, Hefei, Taiyuan, and Wuhan, thereby accelerating its nationwide strategic expansion.

In terms of overall strategy, Taihe remains committed to real estate as its core business, with finance and investment serving as two complementary pillars. The company actively explores opportunities for extending the real estate industry chain, pursues diversified development, and plans for transformation and upgrading. Healthcare constitutes a crucial component of this broader diversification strategy.

Real Estate’s Cross-Industry Expansion into Healthcare Becomes a Prevailing Trend

Since the 1990s, real estate companies have been keen on developing “senior living real estate,” integrating senior care centers and services into their projects. These operations were managed by in-house teams established and operated by the real estate firms themselves, which can be regarded as the nascent stage of real estate companies’ cross-sector expansion into the broader health and wellness industry.

Since the turn of the new millennium, cross-sector expansion by real estate developers into the healthcare industry has become increasingly active. Companies such as Solar City, Greentown, and Poly have successively launched their own “real estate + healthcare” projects. After 2009, the real estate sector entered a period of transformation, gradually extending from single-purpose commercial and residential property development to upstream and downstream segments of the industry chain. Centered on their core real estate operations, these companies have strategically deployed comprehensive hospitals, outpatient clinics, and elderly care services, resulting in more diversified business models.

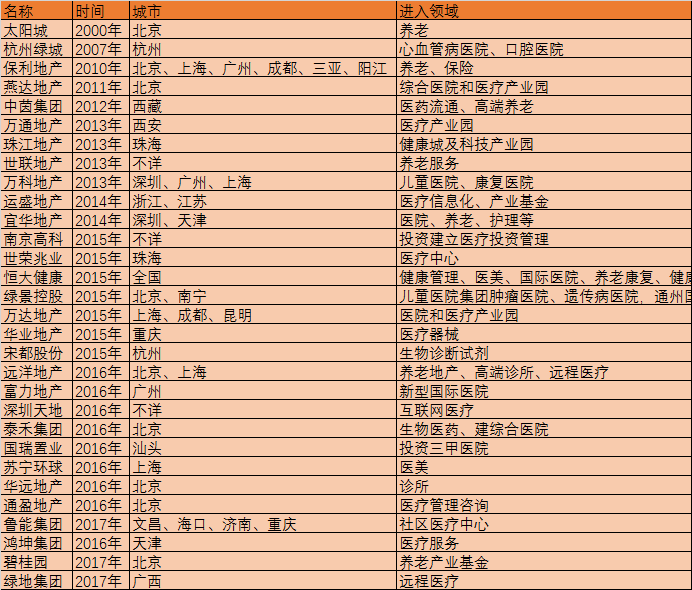

According to previous statistics by VCBeat, since the turn of the new millennium, 30 mainstream large-scale real estate companies have made moves in the medical and health sector, including Wanda, Vanke, Evergrande, R&F, Greenland, and Country Garden. The investment projects basically cover all areas of healthcare, including general hospitals, specialized hospitals, elderly care and rehabilitation, medical devices, and biopharmaceuticals.

Domestic Real Estate Companies' Involvement in Health: Case Studies

There are several reasons why major real estate developers are keen on entering the healthcare sector: first, the traditional real estate industry has hit a growth bottleneck and is undergoing a wave of transformation; second, external factors such as rising resident demand for medical care, an aging population, and the emergence of privately-run healthcare institutions are driving this trend.

From a granular perspective, since the real estate market adjustment in 2010, speculative activities in the property sector have been curbed. The previously extensive, high-profit growth model—primarily driven by land acquisition and construction—is no longer sustainable. Real estate companies need to identify additional business drivers, align with public demand, extend their presence across the upstream and downstream segments of the real estate industry chain, and stimulate property consumption.

From the perspective of demographic structural adjustment, aging is an unavoidable topic. Statistical data show that by the end of 2015, China’s population aged 60 and above reached 220 million, accounting for 16.1% of the total population. This figure is projected to exceed 350 million by 2030, representing approximately one-quarter of the total population. This indicates significant growth potential in the elderly care and rehabilitation sector. Centered on this theme, senior living real estate has become highly favored by developers, while the integration of medical and elderly care services has emerged as a key trend.

Furthermore, residents' demand for health-related consumption is steadily increasing, the share of healthcare expenditure in the national economy continues to rise, and there is a vast base of consumers willing to pay for health services and products.

Since the implementation of the “New Healthcare Reform,” the trend toward privately run healthcare has gained significant momentum, unleashing the initiative of private investment in the medical sector. This has provided favorable policy support, talent resources, and medical resource backing for the “real estate + healthcare” model.

From the perspective of development pathways, there are four main directions for real estate companies diversifying into the broader health sector: elderly care and rehabilitation real estate, wellness tourism real estate, health services real estate, and medical-health cities.

Among these, health service real estate and medical health cities are emerging new directions in recent years. Health service real estate integrates community health management, chronic disease management, early disease screening, diagnosis, and treatment into traditional real estate projects, with medical resources developed either independently or through partnerships. The medical health industry city model, inspired by the overseas “Medical Mall” concept, has been implemented in eight cities across China to date, with total investments exceeding RMB 4 billion, all of which are now fully operational.

Against this backdrop, it has become a widespread trend for real estate companies to diversify into the broader health and wellness sector. In terms of timing, Taihe is among the late entrants; whether it can achieve “late-mover advantage” will depend on the acumen of its operators and the determination of its leadership.

An Analysis of Taihe's Cross-Industry Path into the Greater Health Sector

Taihe’s investment in the big health sector began with the acquisition of Fujian Huitian Pharmaceutical Co., Ltd. Currently, Taihe Investment Group Co., Ltd. holds a 96.62% equity stake in Fujian Huitian, making it the largest shareholder. Founded in 1969 as the former Sanming Pharmaceutical Factory of Fujian Province, Fujian Huitian subsequently underwent changes in ownership. The company is primarily engaged in the business of active pharmaceutical ingredients (APIs), finished dosage forms, and proprietary Chinese medicines, with some of its drug products being exclusive varieties.

Taihe Investment Group Co., Ltd. is the controlling flagship platform of the Taihe group of companies, holding a controlling stake in the listed company Taihe Group (000732). Currently, Taihe Group’s healthcare business has not been injected into the listed company’s structure.

Starting in 2015, Taihe Group began seeking to acquire Alliance Healthcare Services, a leading U.S. outsourced medical service provider. By August of this year, the transaction was completed, with Taihe Group holding 100% equity in Alliance Healthcare Services, and Huang Qisen appointed as Chairman of the company.

Alliance operates independent radiology outpatient clinics, oncology treatment and interventional services clinics, as well as mobile treatment centers, providing services to over 1,000 hospitals and clinics across the United States. Following the acquisition, Taihe plans to introduce Alliance’s technology, talent, and brand into China.

In May last year, Taihe Group signed a cooperation agreement with the International Division of the U.S. Medical Alliance to jointly establish a high-end hospital in Tongzhou, Beijing.

Pan Hong, General Manager of Taihe Medical Group, disclosed to VCBeat: In China, Beijing Yuhe Integrated Traditional Chinese and Western Medicine Rehabilitation Hospital is the first operational tertiary general hospital acquired by Taihe in the domestic market. In Chengdu, the tertiary general Lanhai Hospital, built as a regional medical center, and the Xilian Hospital, positioned for high-end obstetrics, gynecology, and pediatrics, are both under construction and are expected to commence trial operations by the end of 2018. Furthermore, Taihe Medical’s self-developed chain of health management centers, adhering to the “international standards, whole-process care” model, will be launched in major Chinese cities by the end of this year. Soon, clinic services will gradually be implemented across dozens of Taihe communities to serve property owners.

Pan Hong, General Manager of Taihe Medical, Provides a Detailed Explanation of Taihe Medical’s Strategic Path

On September 28, Taihe Group signed a cooperation agreement with the Administrative Committee of Zhangzhou Taiwan-Invested Zone in Fujian Province, under which both parties will collaborate to advance healthcare services. Taihe plans to invest RMB 2.5 billion in the Zhangzhou Taiwan-Invested Zone to build an internationally standardized general hospital, while introducing advanced overseas technologies to provide high-quality medical services to the public.

Huang Qisen, Chairman of Taihe Group, previously stated that Taihe will invest at least RMB 50 billion in the healthcare sector over the next five years. “Healthcare is a capital-intensive industry with a slow return on investment; it may even take eight to ten years before turning a profit. However, this slower pace is acceptable, as healthcare is fundamentally about saving lives and fulfilling social responsibilities. At this stage, profitability should not be the primary concern; instead, we must prioritize building and maintaining high-quality services.”

One notable detail from the interview is that Huang Qisen demonstrated a thorough understanding of cancer survival rates in China and the United States, as well as the shortcomings of current domestic screening mechanisms and the negative impacts of overtreatment. His extensive preparation further corroborates that Taihe’s entry into the healthcare sector was a well-planned strategic move.

Overall, Taihe’s approach in the healthcare sector primarily involves acquiring or building hospitals, representing long-term strategic investments. This strategy differs somewhat from those of other real estate companies that focus on senior living properties and supporting medical facilities. In the future, healthcare is poised to become a highly significant and independent segment within Taihe’s business portfolio.