Building a Robust Rehabilitation System: Lessons from the U.S., U.K., and Japan for China’s Community-Centric, Hospital-Coordinated Model

Drawing on the concept of the “automotive aftermarket,” the industries involved after hospital visits are also referred to as the “hospital post-care market.” This concept primarily encompasses three major sectors: rehabilitation medicine, the elderly care industry, and chronic disease management. Today’s discussion focuses on one of these three sectors: rehabilitation medicine.

Rehabilitation Medicine, academically known as Physical Medicine and Rehabilitation (PM&R), is a medical specialty that addresses functional impairments resulting from disabilities, geriatric conditions, and various acute or chronic diseases. It employs a multidisciplinary approach, primarily utilizing physical therapy and other medical interventions, with the aim of preventing, restoring, or compensating for patients’ functional deficits.

In 2011, the Ministry of Health issued the “Notice on Launching Pilot Programs to Establish and Improve the Rehabilitation Medical Service System,” explicitly calling for the adoption of best practices from developed countries to build a three-tier system. The three-tier rehabilitation medical service system originated in the United Kingdom and has been well established in countries such as the United States and Japan. Even in Hong Kong, just across the border, there is a rehabilitation medical service system worthy of our reference. Therefore, VCBeat analyzes the rehabilitation medical service systems in the United Kingdom, the United States, and other regions, with the aim of providing insights for future entrepreneurs and developers.

I. Scale of Rehabilitation Demand in China and Its Main Sources

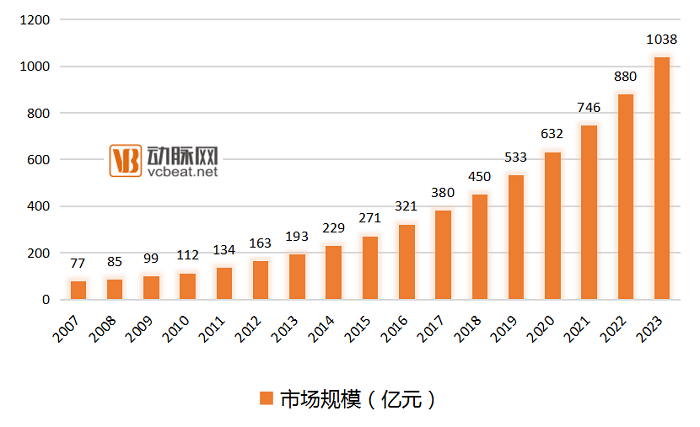

As of 2016, the scale of China’s rehabilitation market was only RMB 20 billion, equivalent to RMB 15 per capita. In contrast, the U.S. rehabilitation healthcare market stood at USD 20 billion, a sixfold difference. When long-term care is included, per capita rehabilitation expenditure reaches USD 800, with the overall market size amounting to USD 200 billion. If calculated based on the level required to basically meet China’s rehabilitation needs, the market size would exceed RMB 100 billion; if benchmarked against standards in developed countries, it would surpass RMB 600 billion. It is projected that by 2023, the scale of China’s rehabilitation healthcare industry is expected to reach RMB 103.8 billion, with a compound annual growth rate (CAGR) of no less than 18%.

Core Population for Rehabilitation

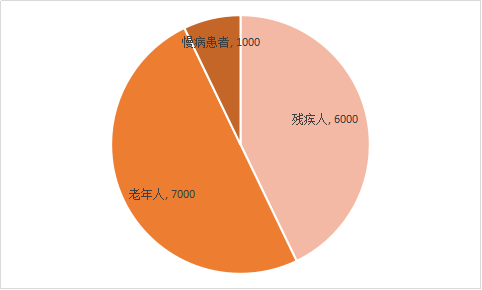

Currently, the population with rehabilitation needs falls into three categories:

Target Population and Volume for Rehabilitation Needs (Unit: 10,000 people)

1. People with Disabilities

Data: According to estimates based on the Second National Sample Survey on Disability conducted by the China Disabled Persons’ Federation, the total number of people with disabilities in China reached 85.02 million by the end of 2010, affecting 260 million family members. Among them, more than 70% (over 59.5 million) had rehabilitation needs. Furthermore, the number of individuals disabled due to accidents increases by approximately 1 million annually, the majority of whom require rehabilitation services.

2. Elderly Population

Data: China is gradually transitioning into an aging society, with a steady rise in the overall incidence rate of diseases among its population. According to statistics from the National Bureau of Statistics of China, by 2016, the number of people aged 65 and above reached 150.03 million, accounting for 10.8% of the total population. Approximately 50% of this elderly population, exceeding 70 million individuals, had rehabilitation needs. However, more than four-fifths of those requiring rehabilitation therapy did not receive timely and standardized rehabilitation treatment.

3. Patient Population with Chronic Diseases

Data: With the rising incidence of chronic diseases in China, coupled with a large number of patients disabled by these conditions, the demand for rehabilitation services is substantial. According to 2015 statistics from the National Health and Family Planning Commission, there are currently over 260 million people with chronic diseases in China, among whom more than 10 million require rehabilitation.

Sources of Rehabilitation Needs

Primary Sources of Rehabilitation Needs

According to a survey by PwC, the primary rehabilitation needs in China currently stem from postoperative rehabilitation for conditions treated in neurology and neurosurgery, orthopedics, cardiology and pulmonology, pediatrics, and obstetrics and gynecology. Among these, due to the high case fatality rate (ranking first in China), high incidence, and high disability rate associated with stroke, there is widespread public recognition of the need for postoperative rehabilitation for these patients, resulting in this group accounting for the largest proportion of individuals undergoing rehabilitation.

Furthermore, the high incidence of mobility impairment and disability following orthopedic surgery results in a substantial proportion of patients requiring rehabilitation. Another key demographic comprises children and postpartum women; due to factors such as strong family emphasis on care, most families demonstrate the highest willingness to pay for pediatric and postpartum rehabilitation services.

II. Three Major Constraints on Rehabilitation Medicine

An entrepreneur in the rehabilitation sector once remarked to a journalist, “Rehabilitation is not about curing disease, but about alleviation.” Traditionally, post-surgical patients, particularly the elderly, are advised by their physicians to return home for rest and recovery. In reality, however, most home-based convalescence amounts to a “low quality of life.” Consequently, entrepreneurs in the rehabilitation field emphasize that rehabilitation focuses not on treatment, but on function, with “restoring patient function” as its primary objective.

Meanwhile, a set of data shows that, taking stroke rehabilitation as an example, rehabilitative therapy enables 90% of patients to regain walking ability and independence in daily living, and 30% to return to light-duty work. In contrast, among patients who do not undergo rehabilitative therapy, the proportions achieving these two rehabilitation outcomes are only 6% and 5%, respectively.

For nearly all entrepreneurs in the rehabilitation sector that we have engaged with, the shared sentiment is that “it is truly difficult to penetrate this market.” During interviews, when discussing profitability, those with stronger revenue performance may reach break-even or begin to achieve stable profitability; however, attaining this milestone typically requires as long as three to four years.

So, why is the market response still relatively lukewarm despite the data clearly demonstrating significant rehabilitation outcomes? We believe that three major constraints are currently hindering the development of rehabilitation medicine in China.

Hospital Side: The Department of Rehabilitation Has Long Been Neglected Under the Current Medical System

At the current stage, rehabilitation services lack sufficient specialization and exhibit indistinct quality differentiation. Most rehabilitation services are concentrated on stroke and orthopedic conditions, while the demand for specialized postoperative rehabilitation—such as for traumatic brain injury, post-brain tumor surgery, spinal (cord) injuries, and artificial hip/knee joint replacements—remains largely unmet. Consequently, the entire rehabilitation process for such patients is confined to inpatient settings, resulting in low turnover rates of medical beds.

In 2011, the Ministry of Health issued the “Guidelines for the Construction and Management of Rehabilitation Medicine Departments in General Hospitals,” mandating that all general hospitals at Level II and above establish rehabilitation medicine departments. Despite these policy requirements, rehabilitation departments in general hospitals remain undervalued in practice. Unlike healthcare institutions in developed countries, where revenue is primarily derived from patients paying for physicians’ expertise and technical skills, medical institutions in China rely mainly on pharmaceutical sales for income. Since rehabilitation therapy largely employs physical modalities, it does not generate this type of revenue for healthcare providers.

Patients receiving rehabilitation medical services are generally in a relatively stable phase of their disease, requiring fewer surgical interventions and less reliance on diagnostic and technical support. Expenditures on pharmaceuticals and consumables are comparatively lower (the proportion of pharmaceutical costs in rehabilitation hospitals averages around 20%, significantly below the approximately 40% seen in general hospitals). It is understood that a single rehabilitation bed in a general hospital can generate daily revenue of RMB 300–500 for the institution, whereas allocating the same bed to a surgical department would yield daily revenue of RMB 3,000–5,000. Consequently, some large general hospitals establish rehabilitation departments merely to comply with regulatory requirements, going through the motions without genuine commitment. These departments often have very few beds and incomplete equipment, rendering them unable to provide effective treatment.

Supply Side: Shortage of Both Personnel and Institutions

Rehabilitation Talent

According to statistics from the International Federation of Physical Medicine and Rehabilitation, developed countries and regions such as Europe, the United States, and Japan typically have 30–70 rehabilitation therapists per 100,000 population. In China, the ratio of rehabilitation physicians to the general population is approximately 0.4 per 100,000 (calculated according to international standards). Currently, China has fewer than 20,000 rehabilitation healthcare professionals. Only 75 universities and 158 vocational colleges in China offer undergraduate or associate degree programs in rehabilitation therapy, with an annual total of only about 8,000 graduates, more than 70% of whom hold associate degrees.

Currently, most rehabilitation institutions have a low proportion of business and technical staff, a low proportion of specialized rehabilitation professionals, and an overall lower educational level among these specialists. In some rehabilitation service organizations, there is even an inversion where non-specialized personnel outnumber specialized professionals, which seriously affects the provision of rehabilitation services and the development of the rehabilitation industry.

Discipline and Program Development Are Severely Lagging. In contrast to developed countries, where rehabilitation therapy programs commonly offer well-established bachelor’s, master’s, and doctoral curricula, China has only 34 institutions authorized to enroll master’s students and merely 9 for doctoral students in rehabilitation medicine and physiatry. Furthermore, there is a lack of standardized norms across all levels of rehabilitation medicine education regarding training models, curriculum design, instructional content, and faculty qualifications, leading to issues such as fragmented standards, dispersed resources, and low educational caliber.

In the construction of China’s three-tier rehabilitation system, there is a significant mismatch between demand and supply in terms of the number of rehabilitation institutions.

Shortage of Rehabilitation Hospitals. According to data from the "Current Status and Market Size Forecast of China's Rehabilitation Medical Industry in 2016" released by China Information Network, there are 3,800 rehabilitation departments in general hospitals and specialized rehabilitation institutions in China, accounting for 28.4%; the number of rehabilitation beds is 98,992, accounting for 2.2%; and the number of rehabilitation medical staff is 39,833, accounting for 0.72%. Meanwhile, there are 8,973 hospitals at Level II and above in China (including 2,002 Level III hospitals and 6,971 Level II hospitals), with less than 50% of these hospitals having established rehabilitation departments. A systematic, comprehensive, and sufficient supply system for rehabilitation medical services has not yet been formed.

The proportion of rehabilitation departments in general hospitals and specialized rehabilitation hospitals is less than 50%. In 2012, there were a total of 3,288 rehabilitation departments in general hospitals and 338 specialized rehabilitation hospitals in China (excluding nursing homes and community-based rehabilitation services), including 206 in urban areas and 116 in rural areas. Among more than 600 cities nationwide, over half had not yet established independent specialized rehabilitation hospitals.

In community healthcare settings, 56% do not have rehabilitation departments established, and the professional titles of community rehabilitation personnel are predominantly at the junior level. Only 25% of rehabilitation staff participated in rehabilitation training within a year, which is far from meeting the public's demand for rehabilitation medical services. The insufficient development of community rehabilitation institutions has prevented the effective implementation of the tiered and phased rehabilitation medical service system proposed in the "Guiding Opinions on Rehabilitation Medical Work during the 12th Five-Year Plan Period."

Imperfect Two-Way Referral System

At present, the two-way referral system for tiered diagnosis and treatment and phased rehabilitation is not yet fully operational. Since rehabilitation medical services primarily cater to patients in the post-acute phase, the key to their operation lies in establishing collaborative networks with general hospitals and developing sound referral mechanisms.

A seamless referral mechanism between clinical departments and rehabilitation departments or rehabilitation hospitals provides a "green channel" for postoperative patients with rehabilitation needs, effectively eliminating barriers to referrals between upstream and downstream departments. This is key to the development of rehabilitation medicine. According to a report by PwC, the current referral mechanisms for rehabilitation patients in China are mainly divided into three types: intra-hospital inter-departmental referrals, deep collaborative referrals at the hospital level, and referrals based on individual recommendations by clinicians.

From the current perspective, intra-hospital departmental referrals are relatively simple and feasible. High-end private hospitals in China, such as Beijing United Family Hospital, have already established rapid and comprehensive internal referral mechanisms. Based on postoperative patients’ rehabilitation preferences, they can be transferred to United Family Rehabilitation Hospital within 3–5 days after surgery to receive professional rehabilitative care. However, in the vast majority of public Grade A tertiary hospitals, the extremely limited number of rehabilitation beds fails to meet the demand for internal referrals.

Implementing referral agreements at the hospital level proves challenging, and it is difficult to guarantee the treatment standards of lower-tier rehabilitation hospitals. Consequently, clinicians are concerned that inappropriate rehabilitation therapies may adversely affect patient recovery. Therefore, in-depth collaborations between tertiary (Grade 3A) hospitals and secondary rehabilitation hospitals often involve extensive participation of clinicians in rehabilitation consultations, consuming considerable time and effort.

When clinicians recommend referrals, the in-house rehabilitation department is often the primary choice, followed by partner rehabilitation institutions. Referrals at this level are largely influenced by physicians’ personal experience, leading to limited coverage and excessive concentration of resources.

III. Rehabilitation Healthcare Systems in Developed Countries and the Hong Kong Special Administrative Region, and Their Commonalities

In its "In-Depth Research and Investment Strategy Report on China's Rehabilitation Medical Industry (2016–2020)," China Investment Consultant noted that rehabilitation medicine in China originated in the 1980s, gained momentum after the 2008 Wenchuan earthquake, and entered a period of significant growth starting in 2012. This development lags far behind the nearly century-long advancements made by European and American countries, where the field originated in the 1920s.

By comparison, the United States currently leads in acute-phase rehabilitation, while Japan has developed distinctive strengths in subacute and maintenance-phase rehabilitation. In China, Hong Kong, just across the border, has established a comprehensive three-tier rehabilitation care model spanning from hospitals to the community.

1. United Kingdom

When discussing the UK’s rehabilitation healthcare system, it is essential to first introduce the National Health Service (NHS). Established in 1948, the NHS is the world’s largest government-funded healthcare system. Operating on the principle of “free at the point of use,” it provides free medical services to 60 million people in the United Kingdom.

The NHS is divided into two parts. Primary care is the first point of contact for most patients. Secondary care, also known as acute care, typically encompasses rehabilitation institutions or rehabilitation departments. In other words, rehabilitation services are accessible only to inpatients or patients referred by general practitioners (GPs). Even rehabilitation outpatient clinics in general hospitals and community rehabilitation centers require a referral from a GP.

The UK’s three-tier rehabilitation medical service system comprises emergency hospitals (initial consultation), specialist rehabilitation hospitals funded through government procurement of services (inpatient rehabilitation), and community-based rehabilitation. A rehabilitation workflow based on functional assessment is established across these three tiers, thereby forming an interconnected rehabilitation medical consortium.

To standardize the establishment of rehabilitation institutions and improve the quality of rehabilitation medical care, the British Society for Rehabilitation Medicine (BSRM) published the “BSRM Standards for Rehabilitation Services for Chronic Conditions within the National Health Service” (hereinafter referred to as the “BSRM Standards”) in 2009. Although this document focuses on neurorehabilitation facilities, it can also be used to standardize the setup of specialized institutions in other rehabilitation fields.

The BRSM standards emphasize that rehabilitation services must be accessible to patients 24 hours a day; all major rehabilitation conferences must involve multidisciplinary participation; timely and effective rehabilitation information must be provided to patients, their families, and friends; a comprehensive activity plan must be provided to patients prior to discharge; upon discharge, patients should receive a detailed medical report and access to outpatient or day rehabilitation services, with readmission guaranteed if their condition deteriorates; and follow-up assessments should be conducted 12 to 18 months after discharge.

The UK adopts a social model of rehabilitation, emphasizing the acquisition of independent living skills for patients. Referrals among general hospitals, specialized rehabilitation hospitals or clinics, and community-based rehabilitation institutions follow established clinical pathways and guidelines, facilitating rapid transition from acute care hospitals to community rehabilitation. Upon returning to the community, patients are assessed by healthcare professionals who, in conjunction with the patients’ self-identified needs, comprehensively determine appropriate interventions to help them achieve independence and improve their quality of life.

Therefore, the range of rehabilitation processes in the United Kingdom is not limited to providing medical rehabilitation services; rather, it places greater emphasis on professional guidance and education, the use of orthotic devices, social support and encouragement, and psychological counseling.

2. United States

The United States has a large number of rehabilitation medical institutions, approaching 30,000, with the figure stabilizing in recent years. The most numerous type is skilled nursing facilities, numbering 15,000 and accounting for over 50% of the total. Another significant segment is home health agencies, which comprise approximately 40%. The overall distribution exhibits a “positive pyramid” structure, characterized by a limited number of acute-care rehabilitation institutions and a substantial number of post-acute care facilities, effectively channeling a large volume of patients into specialized rehabilitation institutions.

In the United States, rehabilitation medical services are structured by establishing various types of rehabilitation institutions tailored to the acute phase, rehabilitation phase, and long-term follow-up phase of diseases.,Various institutions have clearly defined divisions of labor and rehabilitation scopes, supported by reimbursement policies with varying ratios.established a clear division of labor among institutions, effectively alleviating patient pressure on emergency hospitals,Its three-tier system includes:

Inpatient Rehabilitation Facilities (IRFs): Limited to patients who are expected to achieve significant functional improvement within a reasonable timeframe and have the potential to return to a community setting. These facilities may be either distinct units located within acute care hospitals or standalone institutions.

Long-Term Acute Care Hospitals (LTACs): Inpatient facilities that provide post-acute rehabilitation care.

Skilled Nursing Facilities (SNFs): Provide rehabilitation therapy for patients requiring daily skilled nursing or rehabilitation services.

Rehabilitation institutions are established according to the acute phase, recovery phase, and long-term follow-up phase of diseases, with clear division of labor and defined rehabilitation scopes among them. The United States has a streamlined triage and referral pathway. After admission, the attending physician determines the rehabilitation treatment plan based on the results of the Functional Independence Measure (FIM) assessment and the patient’s tolerance level. If the patient’s condition is stable and they can tolerate three hours of rehabilitation training per day, five days a week, they receive intensive rehabilitation; if they can tolerate less than three hours but at least one hour of rehabilitation training per day, they are referred to subacute rehabilitation wards, specialized rehabilitation facilities, or long-term care institutions.

In the United States, the rehabilitation process begins with a consultation by a physiatrist, who prescribes rehabilitation therapy and related interventions based on the patient’s condition. The U.S. rehabilitation care model is characterized by strict monitoring of patients’ functional status across all levels of rehabilitation facilities, refined and comprehensive insurance reimbursement policies, and seamless triage and referral systems.

3. Japan

In Japan, the construction of rehabilitation facilities is categorized into seven major types based on the diseases treated: cerebrovascular disease rehabilitation facilities, cardiovascular system rehabilitation facilities, musculoskeletal system rehabilitation facilities, rehabilitation facilities for children with disabilities, respiratory system rehabilitation facilities, rehabilitation facilities for intractable neurological diseases, and group communication rehabilitation facilities. The primary service population for most of these institutions consists of patients in the recovery phase of their illnesses. Each category is further classified into Type I, II, and III based on facility scale and staffing levels, a system analogous to the three-tier classification used in Hong Kong or the United States.

In Japan, rehabilitation medical services are charged based on units and points. Every 20 minutes of treatment is counted as “1 unit,” and the number of “points” equivalent to “1 unit” varies depending on the scale of the rehabilitation facility. The point-based charging standard is uniform, with “1 point” valued at 10 Japanese yen. In community rehabilitation facilities, “1 unit” is credited as 100 points, resulting in a treatment cost of 1,000 yen. In contrast, in larger comprehensive rehabilitation facilities, “1 unit” is credited as 235 points, corresponding to a treatment cost of 2,350 yen. Health insurance allocates the total number of points based on the severity of the patient’s condition. This policy encourages patients to choose community institutions for long-term rehabilitation therapy, thereby promoting the development of community-based rehabilitation medical institutions.

The characteristics of Japan’s rehabilitation medical model are as follows: comprehensive classification of rehabilitation facility infrastructure, emphasis on long-term rehabilitation treatment for patients in the recovery phase, and a diversified fee structure.

4. Hong Kong

Rehabilitation medical services in Hong Kong are similar to those in mainland China, divided into three tiers:

·Rehabilitation Institutions within Regional Hospitals

· Specialized Rehabilitation Hospital

· Community-Based Rehabilitation Service Network

Patients are hospitalized at regional hospitals for approximately 5–7 days, then transferred to designated rehabilitation hospitals or centers for inpatient care lasting around 15 days, before finally being transitioned to community-based rehabilitation service providers. A well-established three-tier rehabilitation medical network has facilitated the improvement of the two-way referral system. Additionally, patients may return home and receive treatment on an outpatient basis at rehabilitation clinics on a daily basis.

Currently, rehabilitation hospitals at all levels in Hong Kong are fully equipped and capable of adopting individualized treatment plans based on patients’ functional status. Most specialized rehabilitation medical service institutions have 100–300 beds, primarily providing inpatient rehabilitation services for common age-related conditions, as well as day-care rehabilitation, daily living assistance, and recreational and social activities.

Within the three-tier system, community-based rehabilitation primarily targets patients and individuals with disabilities within the community, providing them with health education, lectures, basic rehabilitative treatment, and counseling. This approach aims to facilitate the swift reintegration of all individuals affected by illness, injury, or disability into society. The refinement of this system relies on substantial financial investment from the Hong Kong Government. Statistics indicate that annual government appropriations to rehabilitation hospitals have ranged from a high of over HK$2 billion to a low of HK$370 million, with particular emphasis placed on funding for community-based rehabilitation medical institutions.

In summary, the characteristics of Hong Kong’s rehabilitation medical model are: a well-established three-tier rehabilitation healthcare system, broad insurance coverage, and substantial funding allocated to community-based rehabilitation institutions.

Advantages

Specialized Professionals

In regions with well-developed rehabilitation medical services, rehabilitation care teams are typically established with a physiatrist at the center. The basic unit of rehabilitation service delivery consists of various roles collaborating across multiple disciplines. For instance, rehabilitation care teams in the United States comprise physiatrists (PD), physical therapists (PT), occupational therapists (OT), speech-language pathologists (ST), swallowing therapists, psychotherapists, social workers, and nurses. As the central leader, the physiatrist (PD) is responsible for coordinating the entire team, formulating treatment plans, and ensuring their implementation.

Rehabilitation Service Process

The referral processes in developed countries offer two key insights: first, the proactive concept of front-loading rehabilitation. In the United States, early rehabilitation intervention is manifested as bedside rehabilitation during the acute phase, implemented by non-rehabilitation departments in acute care hospitals, providing patients with moderate-intensity rehabilitation therapy at an early stage. In the United Kingdom, clinical departments maintain close communication with rehabilitation departments to ensure that the latter are promptly informed of patients’ conditions, thereby facilitating early initiation of rehabilitation treatment.

Second, a streamlined triage and referral pathway. Taking the United States as an example, after patients with acute conditions are admitted, attending physicians initiate rehabilitation therapy based on assessments using standardized independent functional scales and the patient’s tolerance level. Once the patient’s condition stabilizes, they are promptly triaged and referred to acute rehabilitation wards, subacute rehabilitation wards, specialized skilled nursing facilities, or long-term care institutions. Patients who can recover without inpatient rehabilitation may also be discharged as soon as possible to home- and community-based settings.

Medical Insurance Payment System

A standardized, function-oriented health insurance payment system is key to improving the rehabilitation medical care system. Taking the United States as an example, the development and refinement of its rehabilitation medical service system rely heavily on the guiding role of its health insurance payment mechanism. The U.S. health insurance payment system is a prospective payment model based on the Uniform Data System for Medical Rehabilitation (UDSMR), utilizing the Functional Independence Measure (FIM) as the assessment tool, and structured around Function-Related Groups (FIM-FRGs).

FIM-FRGs offer two key insights: first, the establishment of scientifically grounded health insurance payment standards. FRGs classify patients into groups based on standardized criteria, then assess each group’s level of functional impairment, age, and comorbidity severity using the Functional Independence Measure (FIM), ultimately determining rehabilitation cost benchmarks. Second, reimbursement is contingent upon tangible functional improvements in patients, which incentivizes hospitals to prioritize functional recovery, promotes the development and refinement of rehabilitation medical institutions, meets patients’ healthcare needs across different levels and treatment stages, and facilitates timely, proactive, and seamless patient referrals.

In the United Kingdom, the National Health Service (NHS) extends beyond rehabilitative care, offering free treatment for all medical conditions. Only 11% of NHS funding comes from National Insurance contributions, while 81% is derived from the national fiscal budget, with the remainder coming from prescription charges and charitable donations, among other sources. In the 2015–2016 fiscal year, the NHS budget amounted to £116.4 billion. The UK government’s expenditure on resident health insurance is substantial, effectively achieving “universal health coverage.”

IV. Case Studies of Listed Rehabilitation Companies Abroad

HealthSouth Corporation (HLS): Positioned in Post-Acute Care, Focusing on Inpatient Rehabilitation Services

HealthSouth Corporation (hereinafter referred to as “HLS”) commenced operations in 1984 and was listed on the New York Stock Exchange (NYSE: HLS) in 2006. HLS operates a total of 107 inpatient rehabilitation hospitals in the United States, including 75 wholly owned subsidiaries, 32 hospitals with ownership stakes ranging from 50% to 97.5%, and one joint venture hospital. In addition, the company manages the inpatient rehabilitation departments of three hospitals through contractual agreements. As of December 31, 2014, HealthSouth’s inpatient rehabilitation hospitals had a total of 7,095 licensed beds, excluding the 41 beds operated by the joint venture hospital.

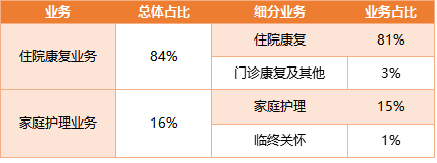

As the largest operator of inpatient rehabilitation hospitals in the United States, HLS reported in its 2015 annual report that inpatient rehabilitation accounted for 84% of its revenue, encompassing both outpatient and inpatient rehabilitation services. Ninety-two percent of its patients were referred from acute care hospitals, primarily through physician referrals. Most of these patients suffered from severe physical and cognitive impairments due to conditions such as stroke, hip fractures, or neuromuscular disorders, which were typically unmanageable in outpatient settings and required inpatient rehabilitation treatment.

HLS Company: 2015 Operating Revenue Statistics

In HLS’s business model, a key distinguishing feature is its focus on “inpatient rehabilitation.” On one hand, inpatient care enables the provision of superior rehabilitation services to patients with severe disabilities; on the other hand, U.S. Medicare regulations stipulate higher prospective payment rates for Inpatient Rehabilitation Facilities (IRFs), thereby effectively enhancing the company’s marginal gross profit.

Since 2007, the company has officially adopted a focused strategy and divested a series of unrelated businesses. In 2007, the company sold its outpatient rehabilitation business to Select Medical Corporation, its ambulatory surgery center business to Texas Pacific Group, and its diagnostics business to Gores Group.

Since 2008, the company has aggressively acquired inpatient rehabilitation hospital targets with prime locations and sound financial conditions. It successively acquired Rehabilitation Hospital of New Jersey, an inpatient rehabilitation hospital under the RehabCare Group (located in Midland, Texas), among others. These continuous annual acquisitions have provided the company with a substantial volume of rehabilitation patients, while also enabling the widespread replication of its business model across the United States.

Youxuan Medical Holdings (SEM): Volume Advantage Drives Economies of Scale, Delivering High-Intensity, Long-Term Rehabilitation Services

Select Medical Holdings Corporation (hereinafter referred to as “SEM”) commenced operations in 1997 and is one of the largest holding companies in the United States owning specialized hospitals and outpatient rehabilitation clinics. As of December 31, 2015, the Company operated 127 specialized hospitals across 27 states and 1,038 outpatient rehabilitation clinics in 31 states and the District of Columbia.

SEM Company's Annual Revenue Structure (2013–2015)

Through departmental outsourcing services, the company provides medical rehabilitation services to nursing homes, hospitals, assisted living facilities, skilled nursing centers, schools, and workplaces. On June 1, 2015, SEM acquired Concentra, entering the home healthcare industry. Concentra offers occupational therapy services and community-based medical care, operating 300 medical centers across 38 states. It also provides contracted medical services, primarily targeting employees at workplace locations and outpatient clinics under the Department of Veterans Affairs in local communities.

SEM is positioned to serve patients with severe acute conditions and those with progressively worsening wounds, who cannot recover in low-intensity settings such as skilled nursing facilities. Patients admitted require longer hospital stays and have access to specialized rehabilitation outpatient services that are not available in general acute-care hospitals. In 2015, the average length of stay at this hospital was 24 days. This segment indirectly contributes to the company’s revenue.

Kindred Healthcare: Providing Home Care Close to the Patient

Kindred Healthcare is the largest provider of acute care services in the United States, primarily offering critical care and post-surgical rehabilitation. It operates approximately 2,700 hospitals across 46 states and employs more than 100,000 people. With over 1,000 rehabilitation service locations nationwide, Kindred provides comprehensive geriatric rehabilitation services, including cardiovascular rehabilitation, short-term post-discharge rehabilitation, geriatric orthopedic rehabilitation, and stroke rehabilitation.

Kindred Healthcare’s rehabilitation facilities fall into two categories: one consists of relatively independent, decentralized skilled nursing centers that prioritize nursing care with rehabilitation as a secondary service; the other comprises inpatient rehabilitation hospitals, where hospitalized patients receive at least three hours of rehabilitation therapy per day, five days a week.

Unlike the first two companies, which focus on rehabilitation hospitals and outpatient clinics, Jinde Health’s rehabilitation services are centered on nursing and long-term care. By positioning itself closer to patients and leveraging its brand along with in-home and community-based services, the company adopts a volume-driven strategy.

V. Possible Implications

Even in the hottest healthcare capital markets, rehabilitation medicine remains an untapped “virgin territory” for investors, as can be glimpsed from its valuations. Despite uncertainty about profitability, investors are still spending to gain a foothold. This tentative approach is primarily driven by the economic potential of the vast rehabilitation patient population, particularly the enormous future market for elderly rehabilitation in China.

Collaborate with upstream and downstream partners of general hospitals to establish cooperative relationships

The relatively high average length of stay in public hospitals in China provides ample room for the expansion of rehabilitation medical services. Currently, the average length of stay for patients in public hospitals in China (approximately 10–11 days) is significantly higher than that in other regions and countries worldwide (Hong Kong: 7 days; Japan: 5 days).

Rehabilitation medical services primarily cater to patients in the post-acute phase. By referring rehabilitation patients from general hospitals to partnered rehabilitation institutions, general hospitals can enhance their revenue and bed turnover rates, thereby improving profitability and operational efficiency for both parties. Furthermore, the development of the rehabilitation sector helps alleviate the financial burden on medical insurance schemes (as daily treatment costs in rehabilitation hospitals are lower than those in general hospitals) and provides patients with superior rehabilitation care, creating a win-win scenario for all stakeholders. This is one of the key reasons why many securities firms remain optimistic about the market prospects of the rehabilitation medical industry.

According to GTJA Investment, both domestic and international experience indicates that rehabilitation institutions serve as a key channel for diverting patients from large hospitals. In the United States, after completing acute-phase treatment, patients are promptly transferred to subacute care hospitals, rehabilitation medical institutions, or long-term care facilities based on their conditions. During this process, physical function assessments conducted by rehabilitation medicine provide a critical basis for triaging acute-phase patients, while the presence of rehabilitation medical institutions also offers a diversion pathway for certain patients requiring rehabilitation.

Precisely because comprehensive tertiary (Grade 3A) hospitals have limited rehabilitation beds and inadequate equipment, resulting in minimal internal referrals, establishing a robust rehabilitation referral system—particularly through collaboration with these hospitals to accept post-acute patients and create streamlined referral pathways—is crucial. Given the substantial demand for postoperative rehabilitation, this approach provides downstream rehabilitation institutions with a stable source of patients.

Community Rehabilitation Holds Great Promise

According to international data, the per capita cost of institutional rehabilitation is $100, covering only 20% of individuals requiring rehabilitation. In contrast, community-based rehabilitation services cost just $9 per capita yet cover 80% of this population. Among patients discharged after the acute phase, 15%–30% are transferred to nursing homes, while 35%–60% return home. This indicates that the vast majority of patients either return home or enter nursing homes following the acute phase. Therefore, vigorously developing community-based rehabilitation services can effectively meet patients’ needs for long-term rehabilitative care.

Community-based rehabilitation provides patients with hospital-level treatment and services within their communities. The advantages of this care model include lower costs and broad accessibility, making it well-suited to meet the current demands for rehabilitation therapy in China.

In August 2016, President Xi Jinping proposed at the National Conference on Health and Wellness the goal of ensuring that “all persons with disabilities have access to rehabilitation services.” In this regard, small-scale, specialized community-based rehabilitation serves as a crucial approach, characterized by low investment, broad coverage, and strong accessibility. However, currently only 16.7% of patients in China with rehabilitation needs are able to receive such services, indicating that the substantial gap also represents significant opportunities.

Currently, community-based rehabilitation services in China are primarily delivered by community health service centers, which have a strong public-service orientation. Consequently, their level of specialization and staffing configurations are suboptimal. Following the elevation of rehabilitation medicine to a national strategic priority, private capital has increasingly turned its attention to community-based rehabilitation. The typical approach involves first establishing specialized rehabilitation institutions, which generally target the mid-to-high-end market and serve a relatively narrow population segment. After gaining a foothold in specialized rehabilitation care, these entities then expand into community-based services. According to VCBeat, most companies currently providing community-based rehabilitation services are still in the pilot phase, lacking guidance from mature business models.

Currently, many publicly listed companies are actively positioning themselves in the interventional rehabilitation medical services industry. Among them, rehabilitation institutions with strong brand resources and robust capabilities for replication and expansion are generally favored by investors. According to VCBeat’s current observations, the rehabilitation medical sector in China is still in its early stages of development. With the growth of the other two major segments of the hospital aftercare market—chronic disease management and elderly care—the rehabilitation market has reached the starting line for rapid growth. Therefore, in subsequent reports, VCBeat will focus on investment models in the rehabilitation field and the community-based rehabilitation segment, starting with the most widely covered rehabilitation institutions to identify emerging market trends.