Rock Health Q3 2017 Report: $4.7B Raised Across 261 Companies, Women's Health Tech Emerges as Top Performer

Rock Health’s Q3 report was recently released. To date, 2017 has become the most lucrative year for digital health financing, although the funding peak seen in the second quarter is unlikely to be surpassed.

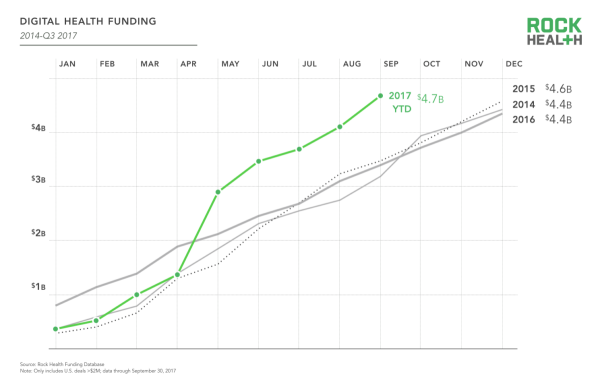

Total financing in the third quarter reached $1.2 billion,The cumulative total financing amount year-to-date has reached $4.7 billion., surpassing the 2015 historical record of $4.6 billion.

2017: A Brief Review. Given the strong performance in the first half of the year, 2017 has undoubtedly become the largest funding year on record. By the end of the third quarter, capital inflows into digital health companies had already surpassed those of any previous year.

Despite the significant bets placed by digital health investors in this sector, performance in 2017 was far from perfect: zero initial public offerings and fewer recorded mergers and acquisitions underperformed compared to previous years. It remains firmly evident that digital health is still in its early stages, with substantial room for growth. VCBeat (WeChat ID: vcbeat) has excerpted the key highlights from the report for you.

The Year of Peak Digital Health Financing, with the High Point in Q2

We have successfully entered a record-breaking phase for digital health financing: the first half of 2017 saw the highest funding amounts, the greatest number of deals, and the largest volume of major transactions.

Investors have never been as aggressive as they were from July to September this year, with financing in the third quarter alone reaching $1.2 billion, bringing the year-to-date total to $4.7 billion. As of now, 2017 has become a record-breaking year, far surpassing the previous high of $4.6 billion set for the entire year of 2015.

Annual Digital Health Financing Data

Among the 83 financing deals closed this quarter, 16% were led by female CEOs, and this figure continues to rise. Nevertheless, even this 16% share represents a significant increase compared to the past few years, when the proportion consistently remained at or below 11%.

# Record-High Number of Financing Cases in History

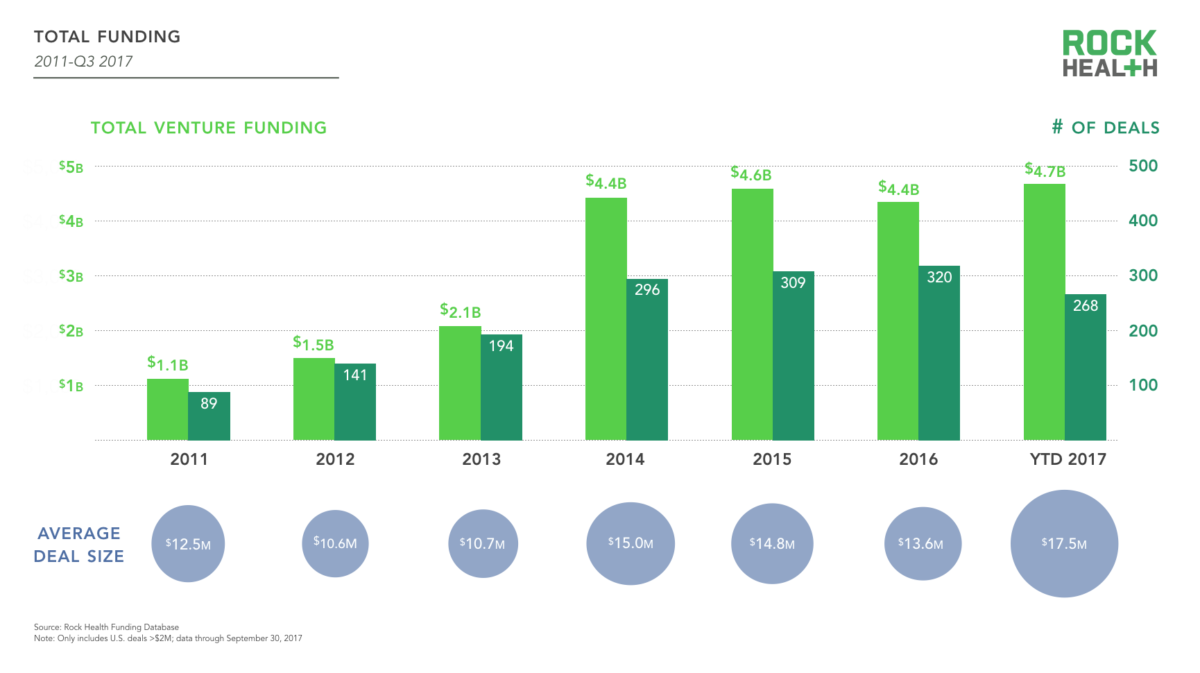

To date,In 2017, there were as many as 268 digital health financing deals, involving 261 companies.. In contrast, there were only 240 transaction cases in 2016 on a year-on-year basis.

Total Risk Financing Amount by Year

Total Risk Financing Amount by Year

Large-Scale Financing Cases Dominated the First Half of the Year

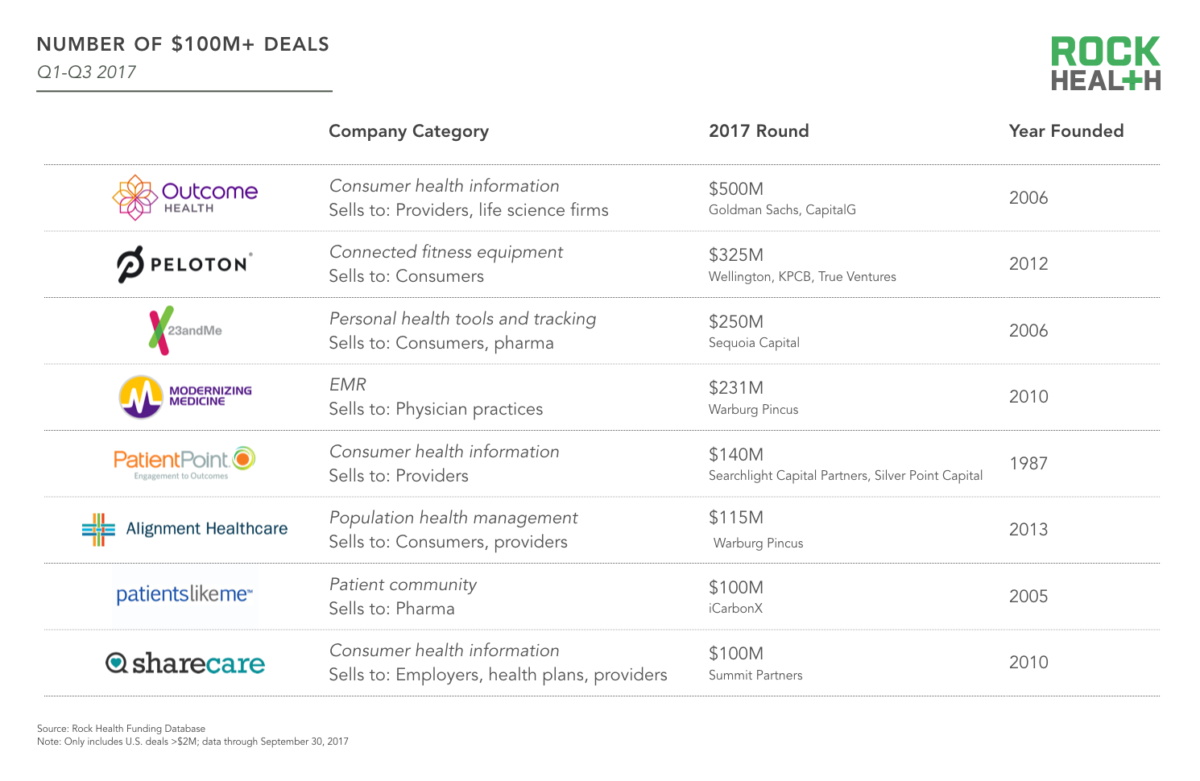

In the first half of this year, a total of seven healthcare companies secured over $100 million in financing. Since the beginning of the second half of the year, 23andMe alone raised $250 million in September, led by Sequoia Capital.

The second-largest deal in the third quarter was Tempus’s $70 million Series C financing round. The average deal size this year stood at $17.5 million, while the quarterly average dropped to $14.6 million.

Companies with Financing Amounts Exceeding $100 Million

1、 Outcome Health

Company Sector: Health Tech

Year Founded: 2006

Target Customers: Healthcare Providers, Life Sciences Companies

Transaction Amount: $500 Million

Major Investors: Goldman Sachs Investment Partners, Google Capital

2、Peloton

Company Sector: Internet-Connected Fitness Equipment

Year Founded: 2012

Target Customers: Consumers

Transaction Amount: $325 Million

Key Investors: KPCB, True Ventures

3、23andMe

Industry: Consumer Genomics

Year Founded: 2006

Target Customers: Consumers, Pharmaceutical Companies

Transaction Amount: $250 Million

Major Investor: Sequoia Capital

4、Modernizing Medicine

Company Sector: Electronic Medical Record (EMR) Systems

Founded in: 2010

Target Customers: Healthcare Providers

Transaction Amount: $231 million

Major Investor: Warburg Pincus

5、PatientPoint

Company Sector: Health Information Platforms and Healthcare Informatics

Year Founded: 1987

Target Customers: Healthcare Providers

Transaction Amount: $140 million

Major Investor: Searchlight Capital

6、Allignment Healthcare

Company's Sector: Population Health Management

Year Founded: 2013

Target Customers: Consumers, Healthcare Providers

Transaction Amount: $115 million

Major Investor: Warburg Pincus

7、Patientslikeme

Company Sector: Patient Community

Year Founded: 2005

Target Customers: Pharmaceutical Companies

Transaction Amount: $100 million

Lead Investor: iCarbonX

8、ShareCare

Company's Field: Health Information Platform

Year Founded: 2010

Target Customers: Employers, Health Plans, Healthcare Providers

Transaction Amount: $100 million

Major Investor: Summit Capital

The Digital Health Industry Is Shifting Toward B2B Business on a Larger Scale

Initially a consumer-facing genetic testing company, 23andMe now positions itself as a drug development firm. It has established a drug discovery laboratory, shares data extensively with Genentech, and has already published clinical analyses.

The trend of shifting from a B2C model to a B2B model is becoming increasingly common in the digital health industry. Based on recent corporate analyses, only 14% of currently operating digital health startups still maintain a pure B2C model, while 61% have expanded into B2B and B2B2C business models.

Most Favored Sectors by Investors

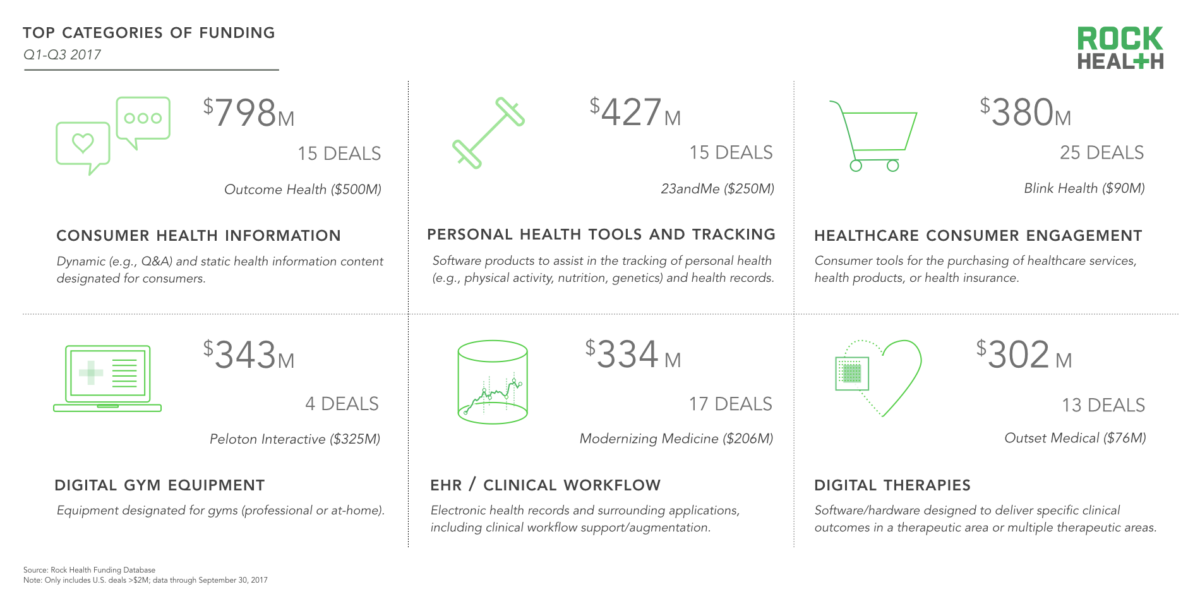

The sectors with the highest financing volumes, such as consumer health information and consumer engagement in healthcare, were primarily driven by large transactions in the first half of the year. The top six sectors accounted for 74.3% of the total financing amount in the third quarter.

Top Six Fundraising Sectors

Top Six Fundraising Sectors

1. Consumer Health Information

Content: Customizing personalized health information for consumers

Financing Amount: $798 million

Transaction Volume: 15 transactions

Largest Deal: Outcome Health ($500 million)

2. Personal Health Tools and Tracking

Content: Software Products for Assisting in Personal Health Tracking

Financing Amount: $427 million

Transaction Volume: 15 transactions

Largest Deal: 23andMe ($250 million)

3. Consumer Engagement in Healthcare

Content: Consumer tools for purchasing medical services, medical products, or health insurance.

Financing Amount: $380 million

Transaction Count: 25

Largest Deal: Blink Health ($90 million)

4. Digital Fitness Equipment

Content: Professional or Home Fitness Equipment

Financing Amount: $343 million

Transaction Volume: 4 transactions

Largest Deal: Peloton Interactive ($325 million)

5. Electronic Health Records/Clinical Workflows

Content: Electronic Health Records and Their Peripheral Applications, Including Support for or Enhancement of Clinical Workflows

Financing Amount: $334 million

Transaction Count: 17

Largest Deal: Modernizing Medicine ($206 million)

6. Digital Therapeutic Solutions

Content: Delivery of clinical treatment protocols using specialized software/hardware at one or more locations

Financing Amount: $302 million

Transaction Count: 13

Largest Deal: Outset Medical ($76 million)

Other Related Information

Other Related Information

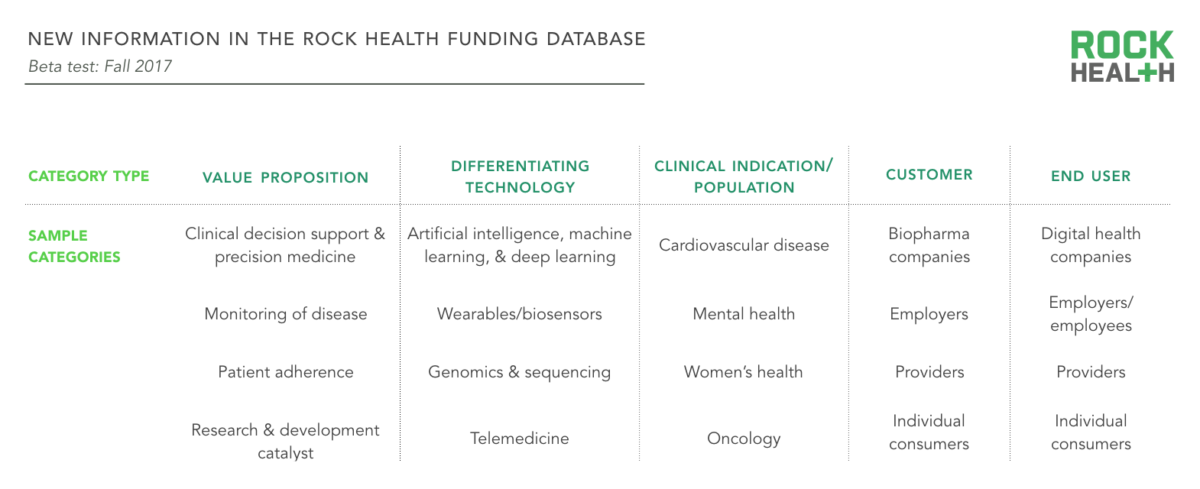

1. Clinical Decision Support and Precision Medicine

Special Technologies: Artificial Intelligence, Machine Learning, and Deep Learning

Clinical Indications: Cardiovascular Diseases

Consumer: Biopharmaceutical Companies

End User: Digital Health Company

2. Disease Surveillance

Specialized Technologies: Wearable Devices, Biosensors

Clinical Indications: Mental Health

Consumer: Employer

End Users: Employers and Employees

3. Patient Compliance

Specialized Technologies: Genomics and Sequence Analysis

Clinical Indications: Women's Health

Consumer: Healthcare Provider

End User: Healthcare Provider

4. Frontier Research and Development

Specialized Technology: Telemedicine

Clinical Indications: Oncology

Consumer: Individual Consumer

End User: Individual Consumer

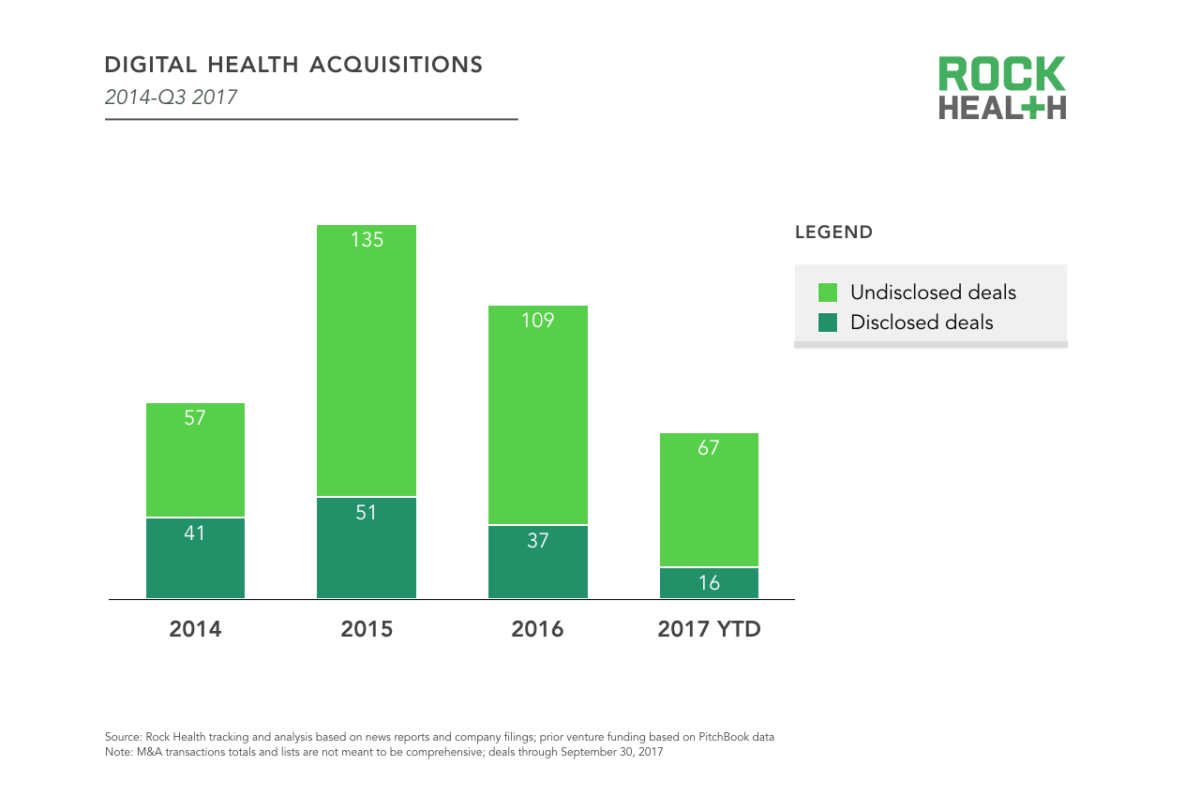

M&A activity continues to decline, with only 83 deals completed from the beginning of 2017 to date.

M&A activity in the digital health sector has been on a downward trend over the past two years: In Q3 2016, there were 112 M&A deals in the industry, down from 146 in the same quarter of 2015. As of Q3 2017, only 16 out of the 83 reported cases disclosed transaction values, making it unclear how companies and investors are faring.

Total Annual M&A Cases in the Digital Health Industry (Full-Year Data; 2017 Data Through Q3)

Compared with previous years, funding channels have become more consistent.

Electronic Health Records/Clinical Workflow ranked fifth in financing this year and was also the sector with the highest number of acquired companies.

In fact, since 2015, electronic health record (EHR) and clinical workflow companies have been the most frequently acquired type of enterprise. From early 2017 to the present, nine acquisitions involving such companies have been completed. Since 2015, a total of 66 acquisitions in this sector have been completed.

In addition, the consumer healthcare sector has seen robust activity in both financing and mergers and acquisitions (M&A). However, certain subsectors recorded the highest number of M&A deals without securing the largest volumes of funding: payer management (6 M&A transactions), physician practice management (5 M&A transactions), corporate health (5 M&A transactions), and hospital management (5 M&A transactions).

2017 Digital Health Industry May Not See an Initial Public Offering

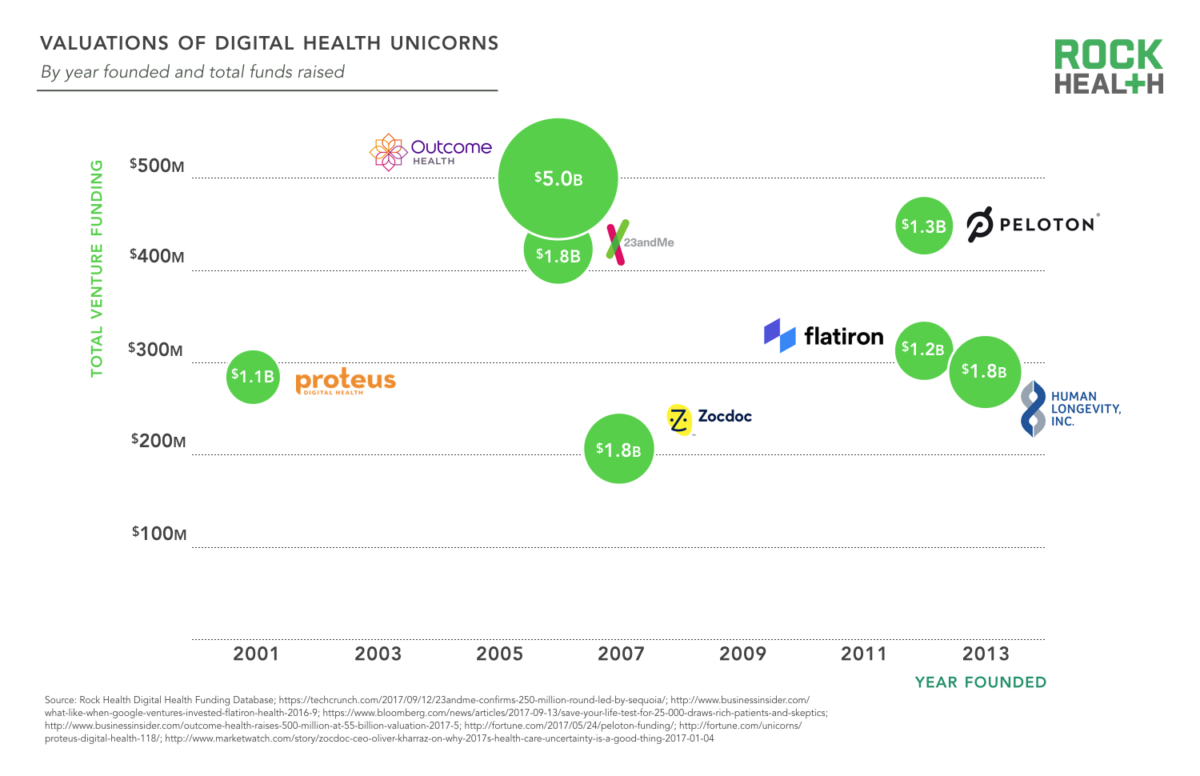

Since 2012, there has been at least one initial public offering (IPO) by a digital health company each year (with a peak of six in 2015), yet none have occurred from early 2017 to the present.

Although this year’s mega-deals have created numerous well-capitalized companies, including unicorns, whether these firms will go public remains uncertain.

23andMe, which had already become a unicorn before its last round of financing, is now valued at $1.75 billion. However, the company has decided to raise a larger round of investment rather than go public. Before keeping pace with fundraising in the public markets, shareholders can only rely on acquisitions to execute broader strategic moves.

Valuation of Digital Health Unicorns

Investors Need Patience: IPOs Take 10 Years on Average

Investors (especially newcomers to the digital health industry) may feel considerable anxiety about current exit market activity, while others view these challenges as side effects stemming from the healthcare industry’s lengthy sales cycles, high complexity, and relatively immature technology adoption.

As Steve Kraus of Bessemer Venture Partners in the United States stated, “We are at the very beginning of this race, and the digitalization of healthcare has just gotten underway.” Relevant data indicate that in the healthcare industry, both entrepreneurs and investors should adopt a long-term perspective.

For example, the average age of the eight companies that completed major transactions this year was 11 years. The oldest was Patient Point, founded in 1987, while the youngest was Alignment Healthcare, established in 2013. Furthermore, among the 18 digital health companies that have gone public, the average time from founding to initial public offering (IPO) was 10 years.

Digital Health Financing Shows Slight Geographic Diversification

California has long led in digital health financing, with companies in the state securing 38% of total investment. By comparison, California-based companies accounted for 48% of financing in 2014. This year, other major financing hubs, including New York and Illinois, contributed 15% and 14%, respectively, to total digital health financing activity.

The average funding size for companies led by female CEOs is $31.4 million.

Women in the digital health industry appear to be writing a different story. In Q3 2017, 16% of the companies involved in the 83 deals were led by female CEOs, compared to just 11% in the first half of this year.

The average funding size for companies led by female CEOs was $31.4 million, compared to just $11.4 million for those led by male CEOs. This disparity is largely attributable to Anne Wojcicki, the female CEO of 23andMe. Excluding the large transaction involving 23andMe, the average deal size for companies led by female CEOs in the third quarter of this year was $12.2 million.

Among the 462 investors, 45% (207) were first-time investors.

The share of first-time investors is the lowest since we began tracking in 2011. In 2015 and 2016, new investors accounted for 55% and 52%, respectively.

The most prolific investors year-to-date are: Kleiner Perkins Caufield & Byers, GE Ventures, F-Prime Capital, and Mayo Clinic, each with six deals; and StartX, SoftTech VC, and Flare Capital Partners, each with five deals.

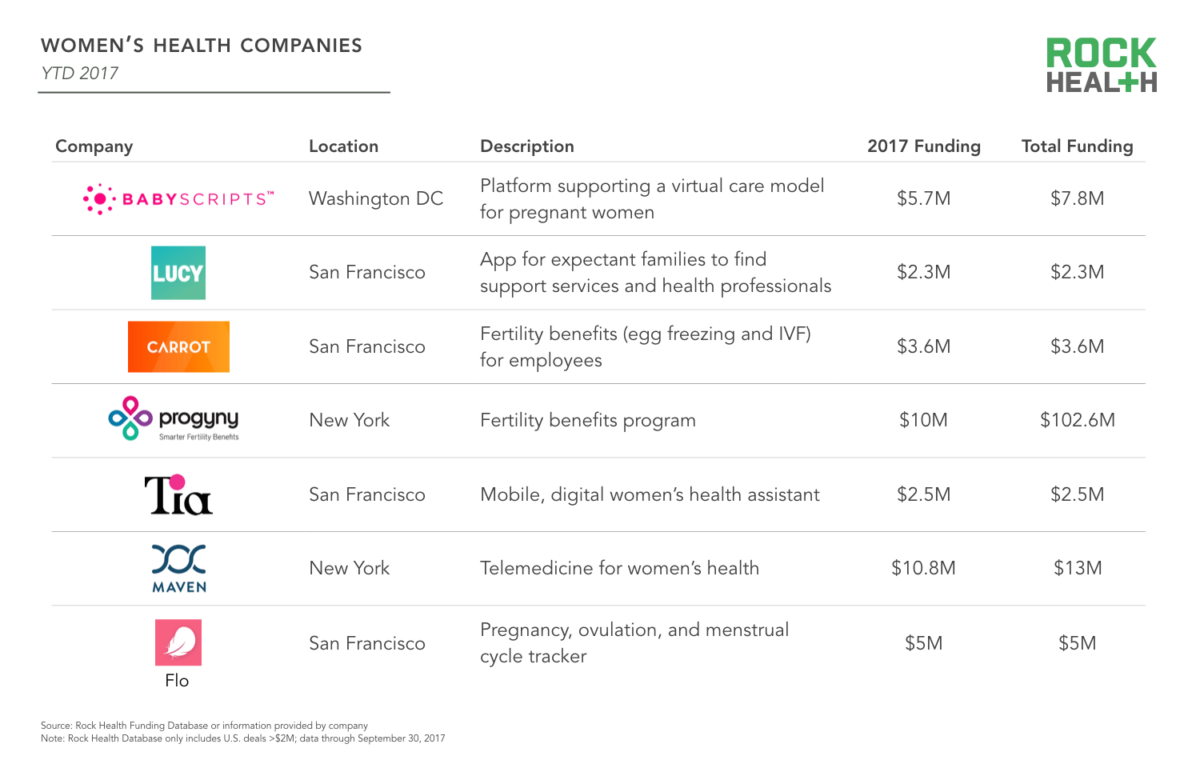

Women and Their Reproductive Health Companies Remain Increasingly Popular

Among these are companies such as Babyscripts and LUCY, which provide services to expectant parents and families during pregnancy, as well as enterprises like Carrot Fertility and Progyny, which focus on fertility benefits. Of the seven companies listed below, four are led by female CEOs, and the majority completed their first round of financing this year.

Women's Health Company

1. Babyscripts (Washington, D.C.)

Content: A platform designed for pregnant women that supports a virtual care model

2017 Funding Amount: $5.7 Million

Total Financing Amount: $7.8 Million

2. Lucy (San Francisco)

Content: An App for Expectant Families to Find Support Services and Health Experts

2017 Funding Amount: $2.3 Million

Total Financing Amount: $2.3 Million

3. Carrot (San Francisco)

Content: Securing Maternity Benefits for Employees

2017 Financing Amount: $3.6 million

Total Financing Amount: $3.6 Million

4. Progyny (New York)

Content: Maternity Benefits Program

2017 Financing Amount: $10 million

Total Financing Amount: $102.6 Million

5. Tia (San Francisco)

Content: Mobile Digital Women's Health Assistant

2017 Financing Amount: $2.5 Million

Total Financing Amount: $2.5 million

6. Maven (New York)

Content: Telemedicine for Women's Health

2017 Financing Amount: $10.8 Million

Total Financing Amount: $13 Million

7. Flo (San Francisco)

Content: Pregnancy, Ovulation, and Menstrual Cycle Tracking

2017 Financing Amount: $5 million

Total Funding Amount: $5 Million

Shareholder Profitability

Among the 26 companies, 11 featured in the Digital Health Public Company Index have profitable shareholders and substantial earnings per share.

Year-to-date, the digital health stocks with the highest returns are Teladoc (up 101%), Care.com (up 90%), and Tabula Rasa HealthCare Inc. (up 79%). The stocks with the largest year-to-date declines are Connecture (down 61%) and NantHealth (down 58%).